Absa’s ROE is moving higher, but watch those margins (JSE: ABG)

The recent momentum in the share price might be too strong

In the B-league of local banking, Absa and Nedbank (JSE: NED) fight it out for best of the rest. Their share prices have decoupled this year, with Absa pulling away with 17% growth vs. Nedbank down almost 10%.

The five-year picture is much closer, with the improvement in macroeconomic conditions in the rest of Africa giving Absa a lovely boost this year and helping it make back most of the lost ground:

For context, Capitec (JSE: CPI) is up 184% over the same period!

Absa’s strong share price momentum in the second half of 2025 is thanks mainly to the low valuation it was on. Yes, there’s growth in the business, but not much to get excited about.

In a voluntary trading update for the year ended December 2025, they flag mid-single digit revenue growth. From a return on equity (ROE) perspective, the good news is that growth in non-interest revenue was ahead of net interest income. Non-interest revenue is a more capital-efficient way to generate income, so it juices up ROE.

The credit loss ratio has been the biggest highlight, improving from 103 basis points (outside the target range) to be within the upper half of the through-the-cycle target range of 75 to 100 basis points.

The concern, like at Nedbank, lies in expenses. The cost-to-income ratio is going the wrong way, as expenses are up by mid-single digits and revenue growth is slightly lower than that.

Thanks to the mix effect of higher non-interest revenue and of course the reduction in the credit loss ratio, ROE is expected to improve from 14.8% to 15.0%. HEPS growth will be in the low double digits. This is difficult to extrapolate though, as the credit loss ratio moving back within range is a step change in the numbers that won’t happen every year.

Looking ahead to 2026, they expect mid-single digit revenue growth, slightly positive Jaws (this means revenue growth ahead of expenses and thus margin expansion – that’s a big one to watch) and further improvement in the credit loss ratio. This should take them to ROE of 16%. The ROE target range for 2027 to 2030 is 16% to 19%.

Let’s see if they can pull it off!

Capitec acquires Walletdoc for up to R400 million (JSE: CPI)

This is a classic example of the outcome that startups look for

The venture capital (VC) industry is built around pumping money into startups that stand a decent chance of being acquired one day. Very few such startups are built to be financially viable on their own, as the goal is to scale quickly and build something that would be appealing to a corporate buyer who could plug the company into a larger ecosystem.

I have no idea at this stage if Walletdoc is profitable on a standalone basis, but we do know that Capitec is going to pay up to R400 million to acquire the business. This will undoubtedly inspire a zillion LinkedIn posts by VCs who will point to this deal as an example of success in the local fintech sector.

R300 million is payable up-front in cash, with the remaining R100 million being structured as a deferred earn-out over three years subject to achieving certain milestones. The earn-out would be settled in Capitec shares.

What does it mean for Capitec? Well, Walletdoc has been building its payments business since 2015. They offer various payment solutions for merchants and all kinds of tech integrations that seem to focus on smartphones and digital wallets. There is a clear strategic fit around financial services accessibility and Capitec’s push into business banking as well.

Capitec is such a behemoth that the R300 million cash portion of this deal is only 0.06% of the group’s market cap!

No Christmas cheer at Italtile I’m afraid (JSE: ITE)

Sales are weak and margins are under pressure

Italtile released a trading update dealing with 1 July to 30 November 2025. I’m afraid that there isn’t much good news to report.

Management has been incredibly transparent for ages now when it comes to the challenges facing the industry. They’ve highlighted the risks from cheap imports combined with overcapacity in local manufacturing and weak demand. This has resulted in a 6.2% drop in manufacturing sales, which means reduced capacity utilisation and thus even more pressure on margins despite management initiatives around costs.

The retail side of the business (CTM / Italtile Retail / TopT) could only increase system-wide turnover by 1.2%. Average selling prices fell year-on-year due to high levels of competition and poor consumer confidence. Despite all the positivity around South Africa this year and the reduction in interest rates, Italtile hasn’t seen an uptick in construction activity.

The update doesn’t give a specific indication of profitability, but it’s not rocket science to read between the lines here. Italtile is suffering, with the share price down 36% year-to-date and no sign of improvement in the business.

Nampak’s results look good, but the share price lacked momentum to break higher (JSE: NPK)

This is the danger of buying stocks at or near the 52-week high

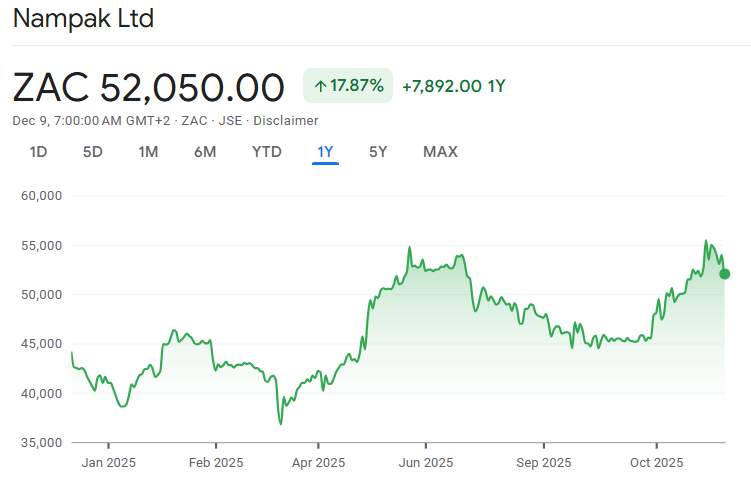

Nampak’s share price hit a new 52-week high on 27 November in response to the release of a trading statement. It can be very tempting in those situations to jump on the hype train and buy the trading statement.

Personally, I’ve learnt two lessons about these situations. The first is to always wait for the release of full results to see what’s actually going on. The second is to wait for a confirmed break higher vs. buying at a strong resistance level and then hoping it breaks through.

These lessons helped me avoid some pain on this one, as Nampak has dropped by nearly 9% since that recent high:

So, the break higher clearly wasn’t confirmed, but what do the full results look like?

Nampak is executing an impressive turnaround story, with revenue from continuing operations up by 8% and trading profit jumping by 26% as the trading profit margin improved from 10.5% to 12.3%. To add to the party on the income statement, net finance costs were down 45% as net debt excluding lease liabilities dropped by 52%. This is why HEPS excluding once-off items jumped by a delightful 46%.

HEPS as reported was actually up 213%, but that’s obviously not a reflection of maintainable growth. The fact that adjusted HEPS was up by 46% shows you just how well the company is doing.

It wasn’t a perfect year. For example, the Beverage South Africa segment kicked off this period by being unable to fully meet customer demand at the end of 2024 due to production challenges that have subsequently been addressed. They have significant can capacity in Beverage South Africa and will look to take advantage of improved local conditions. Even with these challenges, this segment delivered EBITDA growth of 13% for the year.

Diversified South Africa had a much tougher time, with EBITDA down 5% due to consumer spending issues in certain categories and major customers changing their packaging strategies.

Beverage Angola performed beautifully, with EBITDA up by 30% thanks to a stable currency and a more favourable operating environment. As a sense of size, this segment contributed EBITDA of R360 million – now higher than the R310 million in Diversified South Africa. And in case you’re wondering, Beverage South Africa is bigger than both of them combined, with EBITDA of R907 million.

Cash flow from total operations increased by 38% and free cash flow was almost 5x higher at over R1 billion.

There’s still a bit of cleaning up to do, like the disposal of Nampak Zimbabwe after the initial deal to sell that business fell through. On the whole though, Nampak is putting forward a strong story here.

If you use adjusted HEPS of R77.40, then the current share price is a P/E of around 6.7x. I think the reason for the drop from the 52-week high is that the trading statement created too much hype around HEPS due to the once-offs affecting that number. This adjusted P/E multiple suggests that there might be room for some upside.

Update: an earlier version of this Ghost Bite inadvertently used the prior year adjusted HEPS for an implied P/E closer to 10x. This error and the associated commentary has been corrected.

Spar sees a “clear pathway to shareholder returns” – but that path remains treacherous (JSE: SPP)

There is a severe lack of revenue growth

Spar has released results for the 52 weeks ended 26 September 2025. The past couple of years have seen Spar executing tough decisions related to the European businesses. With the strategic restructuring largely behind them, they now need to deliver improvement in the core business in South Africa and Ireland.

With group net debt down by 40% to R5.4 billion, they have more breathing room on the balance sheet to do it. The financial position was assisted by growth in cash generated from total operations of 13.3%. They still have the hangover of the debt incurred in South Africa to get rid of the business in Poland, but at least there’s now certainty over that situation.

The trouble lies in just how competitive this market is, with turnover in Southern Africa up just 2.3% and Ireland managing just 0.6% growth in euros. Both businesses experienced a minor improvement in gross margin, so gross profit was up 4.4% and 2.2% respectively. The story diverges at operating profit level though, with Southern Africa up 6.8% and Ireland down 2.8% due to pressure in that market on wage and overhead costs. We can only hope that Ireland won’t end up going the way of Poland and Switzerland for Spar.

It’s been an ugly year for the share price, down 28% in 2025. Spar may be talking about a “clear pathway to shareholder returns” but the market isn’t buying that story just yet.

Sygnia’s dividend growth is now really lagging profits (JSE: SYG)

It feels like this should be more of a cash cow

Sygnia is a solid business. With a focus on low-cost investment funds, the group has been pursuing a lucrative strategy. This is evidenced by the 12.8% increase in revenue for the year ended September 2025.

Having now decided that South Africa’s living conditions aren’t as bad as the UK’s tax burden, CEO Magda Wierzycka has moved back to the land of sunshine and Bokke. Her CEO report talks about concepts like wanting to promote venture capital growth in South Africa and being alert to opportunities around cryptocurrencies. She also talks about AI for Africa, but I think we are dreaming if we believe that South Africa has any role to play in the current global AI arms race.

It therefore seems likely that some interesting products could emerge from Sygnia in the near-term. But in the meantime, investors will have to stomach a worrying situation in which expense growth of 13.4% was higher than revenue growth. This means that profit after tax increased by only 10.4% – a solid result when viewed in isolation, but disappointing in the context of the revenue growth.

I’m afraid it gets worse when you look at the dividend, with growth of just 6.5% to 231 cents per share. In what is essentially a capital-light model, seeing the dividend grow at approximately half the revenue growth rate isn’t encouraging. This could be why the share price dipped 4.4% on the day of results.

It’s been a great year nonetheless, with Sygnia’s share price up 65% as sentiment has swung firmly in favour of emerging market businesses.

Nibbles:

Director dealings:

A director of a subsidiary of Invicta (JSE: IVT) bought shares worth R973k.

The spouse of a director of a major subsidiary of Growthpoint (JSE: GRT) bought shares worth R694k.

A director of Spear REIT (JSE: SEA) bought shares worth R275k. Separately, a family investment entity linked to the CEO of Spear refinanced a loan from Investec for R41 million, with R90.7 million in shares pledged as security for the loan. Top executives of REITs tend to make use of debt to increase their holdings over time.

The company secretary of Famous Brands (JSE: FBR) sold shares worth R56k.

Datatec’s (JSE: DTC) scrip dividend was a success. Based on the elections by shareholders to receive more shares in lieu of cash dividends, Datatec capitalised profits of R300 million and paid out cash dividends of R110 million. Of course, it helps that the company founder and other directors have so many shares, as they supported the scrip distribution alternative.

Nictus (JSE: NCS) has brought an extraordinary period to a close. This obscure small cap has almost doubled its share price in 2025, yet liquidity remains really low. For the six months to September 2025, HEPS jumped from 26.51 cents to 41.04 cents. It’s all about the jump in insurance revenue in the group, with furniture retail revenue actually dropping slightly.

Copper 360 (JSE: CPR) announced the results of the claw-back offer to raise capital. The full R400 million in fresh equity was raised, but that’s not a surprise based on how the offer was structured. The underwriter has ended up with a big chunk of the raise, as shareholders only subscribed for 63.3% of the rights offer shares. In addition to this raise, debt instruments worth R715 million will convert into shares. With the share price having shed over 70% of its value in 2025, this capital raise is the last roll of the dice for Copper 360. They cannot afford to miss any milestones now.

Southern Palladium (JSE: SDL) issued a tranche of shares to raise A$12.74 million at an issue price of A$1.10 per share. This relates to the approval granted at the AGM held on 28 November 2025.

MultiChoice (JSE: MCG) is bringing its JSE-listed era to an end. The delisting will proceed on 10 December. But remember, Canal+ will be back with an inward listing within 9 months. Best of all, this will include the entire Canal+ group, not just MultiChoice. I look forward to that day!

Now that the compliance certificate required from the Takeover Regulation Panel (TRP) has been received, Safari Investments (JSE: SAR) will be suspended from trading on 17 December and will then pay the clean-out distribution before being delisted on 23 December.

Anglo American (JSE: AGL) withdrew Resolution 2 from the agenda of the 9 December shareholder meeting. This resolution related to amendments to long-term incentive plans in light of the deal with Teck Resources. This only happens when engagement with shareholders before the meeting suggests that the resolution will fail to pass.

In case you’re wondering, Curro (JSE: COH) is still waiting for confirmation of the dates of the Competition Tribunal’s approval process.

Trustco (JSE: TTO) is never far away from drama, with the company refusing to entertain an attempt by the Riskowitz Value Fund to get various new directors appointed to the board. Trustco’s view is that the notice sent to the company by Riskowitz was legally defective. I can just about guarantee that this fight is only warming up.

Oasis Crescent (JSE: OAS) announced that holders of 57.05% of units elected to receive the cash distribution, while the holders of the remaining 42.95% of units elected to reinvest their distribution in the property fund.

As another reminder to the market that they are very serious about the bitcoin strategy, Africa Bitcoin Corporation (JSE: BAC) has appointed Dr Saifedean Ammous as Bitcoin Strategic Advisor.

As we look back on a fascinating year in the markets, Nico Katzke (Head of Portfolio Solutions at Satrix) delivered a fantastic mix of insights on this podcast that can be applied to your strategy in 2026 and beyond.

For example, it’s so important not to learn the wrong lessons from a particular investment or observation. It’s also important to avoid complexity for the sake of complexity – if there’s a simple solution that works, then that’s probably the right one.

Along with insights related to investment term, diversification, the AI “bubble” (a term that Nico isn’t a fan of), US hegemony, gold and REITs, there’s just so much in here. Get ready to apply more discipline and less drama to your portfolio decisions, assisted by the depth of knowledge and experience shared by Nico on this podcast.

Satrix Investments (Pty) Ltd & Satrix Managers (RF) (Pty) Ltd is an authorised financial services provider. The information does not constitute advice as contemplated in FAIS. Use or rely on this information at your own risk. Consult your Financial Adviser before making an investment decision. While every effort has been made to ensure the reasonableness and accuracy of the information contained in this document (“the information”), the FSP’s, its shareholders, subsidiaries, clients, agents, officers and employees do not make any representations or warranties regarding the accuracy or suitability of the information and shall not be held responsible and disclaims all liability for any loss, liability and damage whatsoever suffered as a result of or which may be attributable, directly or indirectly, to any use of or reliance upon the information. For more information, visit https://satrix.co.za/products

Full Transcript:

The Finance Ghost: Welcome to this episode of the Ghost Stories podcast. We are deep in December 2025 (although I must say that anything past the 1st of December starts to feel like ‘deep in December’ to me). I’m always caught out by how many company announcements there still are at this time of year, and I’m quite ready for a holiday, I must be honest.

My guest today, Nico Katzke, I suspect he’s also ready for a holiday. And of course, Nico is from Satrix. You’ve heard from him many times before. Nico has promised me that he’s ready to finish strong. He’s brought some solid insights here.

And then I hope, from here, you are going straight to the beach! Although I suspect it’s not quite that time of year yet for you, is it?

Nico Katzke: Yeah, definitely ready for a holiday. They say if you do what you love, you don’t need a holiday, right? But I still need one, I can tell you that.

The Finance Ghost: Yeah, they say this, but what they do not say is that if you do what you love for 70 hours a week, then you still need a holiday. That’s the little nuance that they seem to leave out quite often.

Speaking of doing things for a long time, Satrix has turned 25 (it’s almost as old as you, Nico), which is very exciting – 25 years of ETFs in South Africa!

I’ve got a discussion coming up with someone from Satrix regarding the history of the group and everything, which I’m really looking forward to. I won’t give away yet who it is yet.

But in the meantime, let’s just touch on this, because I know these birthday celebrations are nice and fresh. You’ve been very involved in this space – for how many years now, Nico? How many of those 25 years have you been doing this for?

Nico Katzke: I’ve been with Satrix now for just over five years. I joined, and shortly after I joined, we celebrated 20 years. So, yeah, it’s great to celebrate the next milestone.

The Finance Ghost: Yeah, that’s pretty cool. You’ve been with them for 20% of the journey, basically, so that’s a pretty big chunk. And of course, as with all growing businesses, what happens in the latter years just dwarfs what happened in the early years. It’s always amazing to see that snowball effect.

So, I think let’s start there, just a little bit. There’s been some regulatory stuff along the way. I don’t want to go into tons of detail on this, but it’ll be nice to just get your thoughts on looking back over this journey and ETFs in South Africa. What really stands out for you?

Nico Katzke: It has been a phenomenal journey. I think when ETFs were first introduced in the 2000s, the investment landscape was quite a bit different. So, this week, as part of our celebrations, we rang the bell at the JSE, and there were a few very interesting speakers as well.

One of them, Mike Brown, spoke about how when they introduced ETFs at the time (and literally this was 2000, so people had just survived Y2K, and a lot of uncertainty and things abound). But what he said that was interesting and which stuck with me was that, at the time, investing was considered extremely complicated, and you needed a lot of capital to invest in anything. So, what ETFs did was they really threw the cat among the pigeons in the investment landscape by introducing a very simple and low-cost way to actually invest.

What it enabled investors to do was, instead of investing in single shares, you could buy a share that represented a whole basket of shares. In other words, you could buy a portfolio – a well-diversified portfolio – at a low cost on the local index. And that certainly changed the game.

At the time, there was a lot of scepticism, “Will this take off? Is there a future in ETFs locally?” And well, if we’ve just seen the growth we’ve experienced over the last few years, and certainly over this period, it does indeed prove the early movers right.

The Finance Ghost: Yeah, absolutely. It’s been a huge part of the landscape now. It’s a big part of so many people’s portfolios, and ETFs are just so important, which is obviously why we do this.

But what I also love so much about the podcast that we do is we get to talk about the markets in general, because I think we’ve done a good job of showing people over time that there’s so much more to ETFs than just going and buying the JSE Top 40, for example. Although that would have been a smart thing to do this year, as time has taught us.

There are so many ETFs out there. There are so many different ways to take a view on the market. We’ve talked before about how it’s actually much more of an active thing than just this passive narrative that gets thrown around with ETFs, which I know you’re definitely not a fan of.

So, it’s really been good to understand more about that and to show the importance of ETFs. And congrats, Satrix! 25 years is really wonderful.

So, Nico, let’s tap into some of the lessons then, that you’ve learned in 2025, because this has been a very topsy-turvy year. We’ve had big geopolitical stuff. We’ve had this incredible resurgence in the South African market, actually.

Yes, a lot of it has been gold, but if you actually look in the past few months, a lot of it has also come from JSE mid-caps, from consumer stocks, and from companies like Tiger Brands and some really encouraging turnarounds.

It’s been very nice to see the momentum in South Africa specifically. And obviously, here we’re biased, you know, we’re wearing our South African hats. Everyone wants to see their own country do well, obviously.

Overseas, we’ve seen some huge moves again in the US market. Everyone’s talking about AI. Everyone’s throwing the word ‘bubble’ around, which I know is something you want to talk about.

So, I think let’s dive into it. I’m going to open the floor to you. You can take us through these lessons however you so choose. I’m looking forward to discussing them with you. What have been some of your big lessons from 2025?

Nico Katzke: So, just for the listeners, Ghost and I spoke before the recording about what we are going to be discussing, and I said I would jot down a few lessons, maybe not necessarily learned this year alone, but certainly that were relevant this year.

The first one that I jotted down is that inaction is sometimes the best course of action, right? And this is evidenced by equity’s strong recovery after quite a strong dip in April, and investors would probably know now – had you stayed the course, you wouldn’t have lost money. And at the time in April, inaction was actually the best course of action.

Remember, this was just after Trump’s unexpected, let’s call it ‘enthusiastic’ embrace of all things tariff and isolationism, etcetera. The MSCI World at the time was down 5% since the start of the year, and many investors would have been spooked. I know of a lot of people who sold their equity holdings at the time.

The only unfortunate thing is, since then, the same index has recovered more than 20%. Meaning, had you sold after losing ground in April, you wouldn’t have participated in the upside.

Now, there’s a lesson in this, right? The key is not to try and time your participation or be clever with technical moves and adjustments. Instead, just staying the course over lengthy periods of time takes the guesswork out of things completely and really allows compounding to start working its magic in your portfolio.

So, it comes down to a set-and-forget strategy when it comes to investing. And this is not just a way of staying sane. It’s actually really the best way to grow your wealth long-term.

So, we learned this lesson, very much, that long-term focus helps manage market anxiety, but really gets you to your destination.

The Finance Ghost: And I think it’s very important to understand what you own, because you’re not going to ‘set and forget’, as you say, unless you actually know the thing you are setting. So, you have to feel confident that what you’ve bought, you’ve bought for a reason – whether that’s single stocks, or ETFs, or whatever the case may be.

And you have to have a real idea of the difference between volatility and a material change to your investment thesis. Because it’s equally not useful if you buy (specifically single stocks), if a company is going down severely, and you’re just going to sit and hold and hope. That’s also not a great strategy. So, you have got to be able to tell the difference between market volatility and a company-specific problem.

If you go up to ETF level, then you don’t necessarily have the company-specific stuff, although there are some indices that’ve got some pretty big individual exposures, right? You look at some of these tech ETFs, and guess what? You’re going to find that Nvidia is a big part of the story, and AI is a big part of the story. So, this is why understanding what you’ve bought is actually really important.

Nico Katzke: Great point. This leads very nicely into the next lesson, and that is the importance (and I oftentimes emphasise this in my discussions with financial advisers) of investment term, right?

What I mean by this is that you should always, when evaluating risk versus reward, consider how long you intend to remain invested. In financial terms, we like to think of this as keeping in mind your ‘investment term’.

Now, what this means is, when answering typical questions – like whether investing in equities now is a good idea, whether I should buy this stock or not, or whether a more conservative approach currently is warranted – the answer must always be prefaced by how long you likely intend to remain invested.

And I so often see investors, and even professional investors, make this mistake. Where we think of the world very simply as, “It’s risky now to invest in equities.” Or, “It’s a great time to be investing in cash.”

And so, why investment term is very important – let’s take, for example, if there is a high likelihood of you needing to exit the investment in the short term. Then, one should always be wary of risk assets such as equities or commodities.

If you know you are going to access your investment probably in the next six months, I wouldn’t take much risk there. But if your investment term actually allows it, then taking on more risk is not irresponsible.

On the contrary, probably the biggest risk you can take with your long-term investments is not taking enough risk. And, think about it – cash and bonds should not, over the long term, make you wealthy. They should, at best, compensate you for inflation plus a small premium, right?

So, understanding what part of your income you should dedicate to setting aside for rainy days, savings, for example, where your investment term is definitely short, versus the part of what you set aside that you intend for investing for the long term.

This is a key step in your financial journey and, I would argue, probably one that you should consider getting an expert opinion on – both for tax and estate planning purposes, of course, but also just for the emotional support role that is played by your adviser.

I mean, I always think about it. We can all find a YouTube video that shows us what to do at the gym, but I promise you. If you’re alone at the gym, even if you’re watching the video, as soon as you get tired, you’re going to pause. You’re going to take a break, have a sip of water, and maybe check Instagram or something.

But I promise you, if there is someone standing there, motivating you, telling you, “You should do 20 reps.” You’re probably going to do those 20 reps. And that is where the financial adviser has a very important role to play. Helping you ground and understand what investment term you’re looking at.

If you are investing for retirement in 20 – 30 years, you should be far more inclined to expose your portfolio to those risk assets that allow long-term compounding, as opposed to having a large part of that in cash or bonds – which over the short term make you feel safe, but really over the long term are where you pay back a lot of the gains that you would’ve had, had you had more exposure to risk assets.

The Finance Ghost: Yeah, I mean, the truth of it is, if it were as easy as just using the information out there and not ever needing to get anyone to help or guide you, then everyone would be an expert in everything, because everything is on the internet.

And yet, here we are. In a world where coaching makes a huge difference because of discipline, mindset, expertise, and also just sticking to what you’re good at, as well.

It’s all good and well to say, “Okay, well, I’ll go and learn everything I need to know that my financial adviser might tell me.” Maybe you could, but your time would probably be much better spent going and getting even better at the thing you already do for a living, so you can go and earn more money and rather just use an expert where you need one.

That’s why experts exist. Because no one can be an expert at everything. So focus on what you can get really, really good at, and then get someone else who’s really, really good to help you with your gaps. That’s pretty much the point, right?

Nico Katzke: Absolutely. What I’ve found is also quite a nice tip that advisers should give their clients, especially, is to try to mentally… Because, as people, we compartmentalise things to make sense of the world. And so what you should ideally do is have two portfolios when it comes to investing.

One is long-term – kind of estate planning, retirement planning, etcetera, where you get that professional help. And then another part of your investment portfolio, you can actually use to play with that yourself.

So, have an EasyEquities account as an example. Buy a few ETFs, buy stocks, read Ghost Mail, try to find a nice stock pick, and play with that part of your portfolio where, if you lose some money, it’s not devastating.

But, making the right decisions with your long-term investment portfolio – that is where I mean you need to ‘set and forget’. That is where you should really be trying to get high exposure to risk assets, and then remain invested, because that’s the key.

And even if it’s R10,000, R5,000, just go play with it, right? And have fun, learn more about the markets. But your long-term investment approach – you should not be tinkering with that every month, or every day.

The Finance Ghost: No, exactly. It’s like taking a risk on redecorating a small part of your house as opposed to throwing everything out, then starting from scratch and seeing how well you do and whether or not you come right.

There is a lot to be said for just starting small – a small part of your garden, a small part of your house, baby steps at gym, as you say. Just go and play around in the markets with a piece of the money, and then make sure that the rest is paying you for time, because that’s a really good way to get paid in the market.

And of course, another good way to get paid in the market is diversification, right? That’s another classic example.

Nico Katzke: Absolutely. And another lesson that has become pertinently clear this year is the need to actually diversify your diversifiers. So, you mentioned at the top that we’re living in a topsy-turvy world. And in such a world, where there is a lot happening, information overload, a lot of uncertainty – in such a world, having appropriate diversifiers really helps investors stay the course.

And this applies in life more broadly. It always serves you to be well-diversified. Think about it with friends, hobbies, even upgrading your skills and ensuring you’re employable outside of your current role. It’s always a good thing to be diversified.

The only area I would probably say you should not be diversified is in romantic relationships and with your kids. I suppose there, it’s best to put your eggs all in one basket. But outside of that, spread your risk and always be on the lookout for improving your own diversification.

The Finance Ghost: You’re not taking the Alex Karp approach, Nico. No Alex Karp approach for you. What is it? ‘Regional monogamy’, I think, was the quote for him. You know, basically like, “I only have one partner per continent,” essentially. Global domination. Palantir, one of the more colourful companies.

Nico Katzke: I haven’t thought about that. I can guarantee you my diversification in the romantic landscape is global – I have zero diversification there. And I think that’s a good thing.

The Finance Ghost: Exactly. Highly concentrated. [laughing]

Nico Katzke: Yeah, I think so. Absolutely. So, all my eggs are in one basket there, and I think that’s a good thing. But outside of that, it’s always a good idea to just consider what might derail your current expectations – be it your employer status, or income, or whatever the case is.

Over the weekend, I was at a braai with friends, and one asked a really interesting question, out of the blue. He said, “What would you do if you were no longer able to apply your current trade?” And it’s actually more than simply a hypothetical question, because one needs to ensure that you’re not trapped in a role, right?

Really focus on your skills and interests, transcending your current day-to-day. Because we always get caught up in our day-to-day, but are you sure that your skills and what you can do can actually go beyond what you’re doing today? And that you’re able to navigate a future, of course, where skill requirements will likely be more fluid.

So, I really think we should all just stop and think about these things, right? If something upsets the apple cart and you need to pivot, are you able to do so? But it applies to more than just your personal and professional lives. It also relates very closely to investments.

The value of true diversifiers often, for investors, lies in soothing short-term fears and really helping investors stay the course. Because, to my earlier point, if you rewind the clock to just April this year, when markets corrected sharply. The best outcome would have been remaining invested, but having been diversified, you would not have experienced that pain so acutely.

So, investors really need to think about their own investment term. Have that chat with your adviser and then, within that portfolio, have diversifiers in place to make the journey a bit more palatable for you, especially if you’re keeping a close eye on your portfolio.

Then again, I kind of have to caveat there. As the adage goes, “If you want to protect what you have, you must diversify. But if you want to create, you actually need to concentrate.” Now, there is some merit in that, right?

So, once again, we need to consider your investment horizon. If you can remain invested for 10-plus years, you would probably want a very high exposure to risk assets such as equities or commodities. And in that scenario, the benefit of low-risk diversifiers will most likely be material only in managing your short-term anxiety, but it’s definitely going to come at the cost of long-term performance.

And so that is the balance that you need to find, right? Is having proper diversifiers in your portfolio, but then also asking yourself critically, “What am I willing to pay, in terms of insurance, to manage short-term volatility?” But just be cognisant that you’re not overpaying for long-term gain through risk assets.

The Finance Ghost: As a father of three, Nico, you certainly have shown that concentration strategies do lead to creation. So, well done on that front. But all jokes aside, you referenced there the tools of trade and what happens if you cannot apply your trade anymore and all of that.

There’s a bigger point there. Yes, diversify your diversifiers in the market, but also just always be alert to your income potential, long-term. Because I don’t care how good your investment strategy is. If you end up down a road where you run out of the ability to earn an income, it won’t matter how good your investments were, because you’re going to be in serious trouble.

So, while you’re spending time thinking about your portfolio, also make sure you’re spending time looking at the world around you, and in the industry you’re in. Especially at the moment, with everything going on in AI.

And of course, that leads us to this AI bubble – and I know that the use of the word ‘bubble’ is not something that you love particularly much, but that’s the term that is getting thrown around at the moment in the world of AI, isn’t it?

Nico Katzke: That’s another lesson – calling things ‘bubbles’ really doesn’t help. Now, we’ve heard it all this year, Ghost. Cryptos are in a bubble, gold is in a bubble, AI is in a bubble. Passive investing is in a bubble. I swear the Springboks’ success is also in a bubble, I suppose.

The Finance Ghost: Hey, hey, that’s controversial. That’s the most controversial thing you’ve said all year.

Nico Katzke: But it can’t all be right, right? Everything cannot be in a bubble. So, let’s maybe take a step back and unpack what we understand when we use the term ‘bubble’.

In my mind, ‘bubble’ refers to irrational pricing behaviour. With common examples including the dot-com crash in the early 2000s or even the tulipmania in the 1600s, where tulip bulbs literally sold for the value of houses. I mean, this is a plant being considered worth more than some houses. It was just a bizarre time.

But the key in labelling something as a ‘bubble’ in my mind is a recognition that hype has overtaken all sensibilities, and that prices reflect an urgency to gain exposure for the fear of missing out on the upside.

Now, the hype then causes further upward pressure and reinforces this positive sentiment. So, you can imagine this kind of self-creating loop where people are positive, the price goes up, they buy more, they get more positive, and so on, and so forth.

Now, the reality is we’re only ever able to label things as ‘bubbles’ after the fact. I recall an analyst saying many years ago on the radio that both Naspers and Kira at the time were clearly in bubble territory.

Naspers’s share price at the time, I think, topped R500 a share or something, and there were these dire warnings of an imminent price decline. Of course, in hindsight, this was clearly misplaced, right? The market was actually correctly pricing Naspers’s growth.

Another more recent example is Michael Burry. He is famous for profiting off the US housing market crash and predicting it, being the oracle of the market in 2008. But he’s since gone on – I don’t know, Ghost, you probably know the figures better – but he’s gone on to predict 15 of the last absolute zero crises.

The Finance Ghost: Yes, exactly. [laughing]

Nico Katzke: He was shorting both NVIDIA and Palantir this year, which has not turned out great for him, right?

The Finance Ghost: I actually did a podcast on him literally in the last week or so for Moneyweb, so I know exactly what you’re talking about. Because he has now started this whole Substack, and some of what he’s talking about is not news to anyone.

It’s like, “Oh, share repurchases by tech companies are not good for shareholders because they are really just reversing stock-based compensation.” Anyone who’s been reading a single set of American tech financials for the past five years knows that.

Nico Katzke: Exactly.

The Finance Ghost: So, it’s going to need some stronger arguments than that to make that work.

Nico Katzke: And, ultimately, you’re right. The price has maybe elevated beyond sort of where it reaches longer-term levels, but just calling things ‘bubbles’ is not helpful.

And I think it’s because markets tend to be remarkably resilient and efficient over time. Even the dot-com crash that I mentioned earlier – it simply preceded an era of enormous stock market growth, particularly in companies that succeeded in the internet age.

Now, were there failures? Of course. Sure. But many analysts, after the stock market correction, pointed to irrational behaviour and exuberance – wait for it – in companies being too enthusiastic in building the internet’s infrastructure, which included laying fragile fibre optic cables under the sea to enable this era of ‘global connectivity’.

But in hindsight, we’ve come to rely on this, right? And the technology is still here. I’m talking to you over the internet now, and our listeners are downloading this using the internet. So, naysayers wrote the obituary for an industry that, at the time, looked like it had died before it even matured.

And this is now, remember, early 2000s, the dot-com crash. A lot of analysts were saying, “Well, you know, we told you so. This was all hype, all bubble, no substance.”

But hindsight now perfectly shows us that the market was not irrational in valuing highly companies that would ultimately benefit from widespread internet adoption. It was simply a case of not all companies ending up being the winners.

I think there’s a lesson there, right? Labelling something as a ‘bubble’ creates fear among investors, who then view such industries or stocks as being irrationally priced. And so, at the end, it affects their behaviour, and they remain on the sidelines.

I think investors should instead be vigilant, but I would never recommend implying that markets are at any time irrational. That simply does not make sense to me.

Now, will there be pain from AI? Sure. I think some companies will certainly disappoint. Are valuations stretched today? I would probably be inclined to agree. But at the same time, I would point out that traditional accounting measures aren’t great at measuring the value of technology companies, right? And we’ve seen this.

So yes, it looks expensive based on fundamentals, but how relevant are those fundamentals as these companies are building the infrastructure for tomorrow’s AI world, in whichever way it matures?

So, I still think that building exposure to companies developing infrastructure in AI is a good idea, but – and here is maybe something that might be a bit controversial – gold and crypto, I’m less certain. Because both, for me, are assets whose value is intrinsically tied to sentiment and a need for storing wealth.

The functional value of both is not yet that clear to me, other than it’s store of value, which absolutely is a critical function, but one that is very cyclical in how markets perceive its information. And so, maybe there, the term ‘bubble’, I don’t know, if you want to use it? But even there, I’m less inclined to call things ‘bubbles’.

The Finance Ghost: Yeah, it is really interesting, and I mean, this is a year now in which people have actually jumped onto the gold bandwagon. And they’ve pointed to inflation, and they’ve pointed to the dollar, and we can talk about that now-now, and that’s done really well.

But as you say, it is, at the end of the day, a sentiment-driven asset class. Crypto certainly as well, without the benefit of the central bank buying, etcetera, etcetera, that gold enjoys.

And just to touch on that point you raised around the tech companies and the accounting, that’s absolutely right. So, for anyone who wants to go do some more reading on that, basically, the point is that more traditional industries, when they spend on capex, a lot of that goes onto their balance sheet.

They go and capitalise those assets. They depreciate them over time. It gives them a smoother earnings trajectory, whereas in tech, most of that R&D spend just gets expensed.

So, you end up with these situations where, in a period of significant investment in new technology or ramping up these teams, etcetera, the income statement takes a big knock. But they’re doing it so that they dominate with revenue in the next five years, for example.

In a traditional manufacturing-type company, you would not actually see that on the income statement. Everyone would be celebrating the fact that, well, they’re building up this asset base, etcetera.

So, people do sometimes underestimate the value on the actual balance sheet of these tech companies, and that’s why you sometimes see them trade at gigantic valuations versus the underlying accounting numbers and these big multiples.

Certainly not to say the big multiples are not a problem, because of course they can be. The point is, you’re not comparing like for like if you’re looking at an NVIDIA, for example, and a traditional company. The accounting doesn’t look the same.

It gets even worse when you get to very people-focused businesses like Meta and all of that, who are building out these huge systems where so much of it gets expensed.

Anyway, that’s enough accounting geeking out. I think let’s maybe then move on to – and I referenced it there, around gold, which is – what’s happened with the dollar.

That’s been another big focus this year, right? American excellence and US supremacy and all of that. Is that still a thing? Is it going to still be a thing?

Nico Katzke: That’s a very important lesson that we learned this year. That US hegemony is not a guarantee. And we actually need to start reimagining a world where the dollar and fair global trade are no longer a core feature of forecasting your business growth into the future.

Now, this kind of, let’s call it, ‘slide’ in the general psyche of the US’s central position in global trade. This, of course, has a bearing on the dollar’s reserve status, which in turn is bidding up the value of gold and crypto as alternative stores of value.

As people are becoming a bit more disillusioned by the stability of the dollar – I mean, the dollar has slid in value this year – and also maybe just asking questions about the fiscal sustainability trajectory, asking hard questions, people are finding comfort in actual physical gold, as well as alternatives like crypto. And I actually don’t believe this is completely irrational.

Let’s take a step back and ask why people are concerned today. So, I think if we strip it out to the basics, you’ve exchanged your labour, your time, your productivity for a currency, which is your claim on future goods and services. That’s why you go to work in the day.

Now, this works well as it removes our need to barter, of course, exchanging milk for bread and so on, and has allowed rapid societal development over time.

But if the currency that you have exchanged your time for is being debased and devalued due to inflation, that means the rand that you earned is not the same as the rand that you ultimately spend.

So, this is why inflation is often called ‘the silent killer’. You don’t feel it in your pocket over the short term, but it really makes a massive difference, or dent, in the value of what you exchange your time for over the long run.

This is also incidentally why the wealthy own very little cash. Their wealth is tied in assets typically (so real estate, equities, commodities, businesses, etcetera), where inflation does not really have that direct eroding effect.

Now, ultimately, this all means that wealth is transferred from savers, who are not well compensated for retaining their income – and what I mean by ‘saver’ is someone putting their money in the bank, under the mattress – and it’s transferred from those savers to asset holders as banks and governments continue to issue new debt (ironically, often to pay off existing debt), which in turn then devalues the currency.

So, if you think about this sort of roundabout circle of life at the moment, it’s certainly the case that those who are defensively positioned (i.e. the savers) are really losing out, and inflation is starting to make a big dent in that.

Now, one response to this is to hold as little of your wealth in assets tied to the dollar or the rand, for that matter, and instead to hold assets like gold or crypto. So, that’s why I said just a while ago, I don’t think it is irrational. And we’ve certainly seen a big shift towards these assets as a result of fiscal and debt pressures building up.

Even the US Treasury. If you look at it – $37 trillion of debt, 120% debt to GDP. Are these levels sustainable? And if not, then, well, what is the future prognosis of the value of the dollar?

But I don’t think holding gold and crypto only is the answer, as these are largely unproductive assets to hold. They don’t create anything of value. They should, in the long run, simply preserve value. There’s a big difference there.

Building your wealth should ultimately involve a productive element. And it would probably be why I would still prefer holding assets like equities for the long term. Gold doesn’t create anything. It’s shiny, but it’s a brittle element. We have mined enough gold to last us forever.

And so, it’s an interesting asset class and certainly adds diversity to your portfolio, but over the long term, I would still regard real assets as important for your portfolio.

So, notwithstanding all the concerns that people have – the debasing of their currencies, all these things, absolutely, I agree with that. But the answer probably lies in holding assets that are productive and that can grow, as opposed to holding cash or holding necessarily only crypto or gold.

The Finance Ghost: Yeah, and I think if you’re looking for something that gives you a yield along the way, that’s where property works really well. Specifically, for me, listed property. I always beat the drum that buying physical property yourself – all of the concentration-risk headaches and incredible costs of getting in and out and everything else – can be really difficult to actually make a proper return from.

It’s definitely better than not saving, and for some people, that is a really good forced save. To go and build up a property portfolio and have these bonds they need to pay. But that’s then a behavioural finance point alongside the actual finance point.

Whereas owning the REITs, for example. If you picked them properly, they’ve had a fantastic year. I’ve been very happy with a lot of my property positions on the JSE. It’s liquid, I can get in and out. There are great properties, very diversified. And really useful in a time of inflation, because again, these are real assets. They have replacement costs. They have underlying exposure, especially on the retail side – if you go and own shopping centres, then inflation goes up and so does the money going through the tills, which is great news for the landlord because it’s great news for the tenants. So, that’s a very powerful way to offset some of the inflationary risks.

Nico Katzke: Yeah, absolutely, and the benefit of that as well, if you hold property directly (so not in a REIT, but have a house or a flat), you can also enjoy those assets, right? Perhaps if you have a beach house or somewhere you like to go, there is also a utility value in actually having your money in those assets.

So, just being diversified as far as possible and having exposure to property, certainly, I agree with you. I think it’s a good idea.

And there’s another lesson this year that I have learned that we tend to unlearn as humans, and that is that we should avoid learning bad lessons. As humans, we have this ability to try and take lessons from our experiences. Which is generally a good thing – if you’ve learned that approaching a snake and it bites you hurts you, then great idea not to approach another snake, right?

But the trick is, I think, to differentiate when a lesson should be learned. One could easily have learned the lesson that investing is not safe in 2008 and that one should instead hold money in the bank, where it can’t lose value. But that lesson would have been incredibly costly since, and will likely be so over the next 17 years.

So, don’t learn bad lessons. It’s almost like (I think I’ve used it on this podcast before) the analogy of poker as well, right? If you get dealt a 2-7, a terrible hand, and the flop comes and out comes a 2, a 2, and a 7, and you have a full house.

Well, if you folded that 2-7, which is statistically the worst hand that you can be dealt, you should always fold that hand. And the fact that a 2 and a 2 and a 7 flop doesn’t mean that next time you get a 2-7 you should play it, right?

That’s a bad lesson. That’s the definition of a bad lesson. The outcome was random, right? And so, learning a lesson from that is a bad idea.

And so, I think as a society, we very often learn lessons. We look at the world, and we say, “Ah, see, I know I shouldn’t have invested in that. I know I should have bought that.”

And with crypto, I know a lot of people, personally, who feel they were interested in it, didn’t invest in it, and now have made large investments in it because they have learned the lesson that they missed out. We should think of the world more soberly than that.

And this kind of leads into another lesson, which is, I suppose, related in a way. We had a very interesting discussion recently, a team discussion, where the speaker was speaking about the sort of rise of cynics globally. And it got me thinking about – and there is – a difference between cynics and sceptics.

I think being sceptical is good. It’s always good. Don’t trust too easily. Ask the difficult questions, whether it is to your employer, your adviser. Those are fine. But being cynical seldom serves you well.

And our society has become quite cynical about various things, right? Quite polarised and cynical.

Now, cynics can be quick to adopt conspiratorial positions, as we know, and conspiracies often lead those people to be more manipulable and sucked into information feedback loops that can be quite counterproductive.

For example, believing that the system is somehow rigged or that governments will inevitably print vast amounts of money to dilute the value of your portfolio and so control you. I mean, I’ve heard it all, right?

Believing this, questioning the moon landing, or whether the earth is round, all of those are fine. You can question that. But it can actually have the effect of people making very bad real-life decisions and, in the process, missing out on sound long-term investment opportunities.

Now, this has, I believe, in no small part, bid up the value of crypto assets beyond any proven use case. Because that is a reality. What is the use case? How are we going to use this technology in our daily lives to the extent that it can be priced so highly, as it is currently priced?

Crypto absolutely appeals to a cynical mindset in that the world is inevitably going to implode, the value of fiat currency is going to go to zero, and so a lot of those people are bidding up crypto. Of course, I’m not saying everyone who holds crypto is a cynic, but it certainly feeds into that cynical mindset.

Now, if you happened to bet on the commonplace, let’s call it, ‘zeitgeist’ of cynicism that we currently face today, a decade ago, you have since enjoyed the value of crypto going up, and you would have been proven right and may yet be for some time still.

But I would still be quite cautious on betting long-term on stores of value without a proven use case. And this is, in my opinion, a more risky bet than longer-term betting that the global stock market will continue to innovate, continue to expand, and that we’re not going to see a complete currency debasement.

So, again, I’m not saying crypto should not be held in your portfolio, but I know a lot of investors have tied a lot of their wealth into crypto, have seen it grown, and so the lesson that they learned is that it is a good idea, that it should work, because we have this cynical mindset when it comes to the world at the moment.

The more we can replace cynicism with scepticism and a healthy questioning, and not sort of just believing that everything is rigged, I think that we’re going to be better for it. If we head in that direction.

The Finance Ghost: Yeah, I think what is important is to find what works for you, right? What is a natural fit for you? Because some people are naturally more cynical, others are more sceptical, and they recognise the danger, maybe, of being cynical. Others are naturally optimistic. Some are too optimistic.

You’ve got to find what works for you, and then you’ve got to learn what the weakness of that is, your particular personality type, and then just adjust for it over time.

And the only way to do that in the market is to try and to actually get out there, play around, take positions, and then, importantly, learn the correct lesson. As opposed to learning a bad lesson, which is worse than learning nothing, absolutely, because then you’re just taking it, and you’re saying, “Well, I learned something.” No, you didn’t. That was just a particularly weird outcome. If you keep applying that over time, you are going to hurt yourself.

So, there is some really, really good stuff coming through there.

And I guess as we start to bring this podcast home, I know one of the other points that is close to your heart is complexity, and that actually, complexity is not always your friend, right?

Nico Katzke: Yeah, a very important lesson that I learned this year as well, and a lot of advisers that are listening to this will be able to attest to this, is that the best portfolios are not always the most complex portfolios. And the reality is you can actually build quite sophisticated investment portfolios using very simple, low-cost building blocks.

There’s been a strong shift in our industry towards using terms like ‘AI’, ‘machine learning’, ‘deep learning’, and adding those to fund descriptions that sometimes make investors believe there is complexity involved in constructing portfolios, and that complexity in and of itself has value.

But at the JSE this week, where we celebrated 25 years of ETFs, it’s clear that we have had simple, low-cost building blocks that we can actually put together and create quite sophisticated portfolios.

I liken it to an analogy of playing with Lego. So, I have three boys, as you mentioned earlier. And the reality is, if you give them a Lego set with clear instructions, they can create quite complex creations using very simple, low-cost plastic building blocks.

There’s nothing complex about a Lego building block. But if you follow the manual and you actually put those blocks in the right order, you can create wonderful creations.

Now, of course, if I step on it and I break it and I take away your manual, yes, well, then you are left with cheap building blocks, and it might not be that easy to put something useful together.

And so, this is where I think an important thing to remember when it comes to investing and building your portfolio and investing for the long term, is to have this discussion with your adviser, right? Because they have the ability to use low-cost building blocks to actually create quite sophisticated portfolios that match your own investment term, your own risk-reward trade-offs, and that are designed to maximise your tax benefits and really create that wealth in your portfolio.

So, I would not recommend asking for complexity or wanting to see complex designs in your portfolio just for the sake of it. Oftentimes, the simplest solution gets the job done. If you look at the performance of ETFs over the last 12 months, some of the best-performing funds in our industry have been the simplest funds this last year.

Not to say that complexity cannot add value, of course, it can, but I wouldn’t just regard an investment process that is complex as necessarily good.

And so, maybe have that discussion with your adviser. Ask him or her, “Am I invested in low-cost investment vehicles that make sense, that add value, and am I putting these blocks together to create the Lego solution that is not only aesthetically feasible, but over the long term can actually create wealth in your portfolio?”

The Finance Ghost: Yeah, the Lego analogy is great. So, my kids also love Lego, obviously. I mean, I think all kids do, really. And there are these amazing YouTube channels that I found recently, one channel I think is called Brick Science, but there are a few of them. And they do robotics with Lego to kind of solve problems, and they’ll make it really fun.

They’ll try and sink a Lego ship using these different things they’ve built, or they’ll attack a Lego city using these different weapons they’ve built, like catapults and stuff. But all from scratch, just using Lego bricks and robotics. It’s really, really cool.

And some of the solutions they come up with are so simple to solve the problem, and it’s like, “That’s amazing!” And other times it’s this ultra-complex thing that failed. It’s no different when you are investing, and that’s definitely something to keep in mind.

It’s not about being clever. It’s about getting the best returns. The best return is the smartest return. That’s it. Over time, on a risk-adjusted basis, that’s the answer. No one cares how you got there. “Did you or did you not do well?” That’s the point.

And a big part of that is also just consistency, right?

Nico Katzke: Yeah, absolutely, and I wanted to add to that exactly that point. Consistency is key. So, look for the managers who have delivered consistently, not just recently, right?

If I can use a golf analogy. My golf game is such that every now and then I hit a blinder of a shot, perfectly down the middle, but I can promise you, I will not follow that up with another straight shot. And so, if you look at a fund manager’s performance, they might have just hit a great shot. But the question is more, “Can you repeat that over 18 holes?”

And so, look for managers who have performed consistently. Because they might not be the loudest in the market. Certainly, the ones who have performed more recently would be the loudest. But ask your adviser, and look at managers’ consistency, because that is incredibly hard to replicate and definitely gives you a higher probability of repeating that strong performance if consistent managers have been good as well.

The last lesson that I’ve learned is something that the Springboks actually taught me this year, and it’s that you can’t always please everyone. And if you want to be successful, you sometimes need to make very hard decisions.

Leaving out, for example, stars in your team to build depth is a risk and a hard decision, as you might be proven wrong in the short term. There might be short-term pain. Someone might say next week, “Ah, you should not have played this player.” This decision is a risk and a hard decision, but ultimately, this has built an enviable resilience in our Springbok team.

And I think the same applies to investment decisions. You sometimes get things wrong, other times get things right. But ideally, you shouldn’t dwell on past decisions, but instead focus on building long-term resilience in what you’re doing and in your portfolio. And knowing that that is the right thing to do, not just what is exciting or the most appealing in the short term.

The interesting thing that we can take from the Springboks rugby team – I don’t want to overstress the analogy – but a lot of our competitors are saying, “Well, South Africa has built this depth because they have that many players.”

It’s not that. England, France, many other nations have many players. It’s more a conscious decision that was made to do something that you know long-term is the right thing to do, but there may be pain in the short term.

I think when it comes to investing, you have to have the same mindset. Sometimes, yes, it’s painful investing in a long-term strategy, because you look at your mates, and you go, “Man, this guy has poured money into crypto. It’s up 30% – 40% over the last month.” And then you have that FOMO, because you look at your investment portfolio that’s kind of chugging along, and you go, “Oh, man, I missed this opportunity.”

And so, doing what you know is right – keeping an eye on the long term, focusing on what you pay, not overpaying for the strategies that you are investing, and consistently contributing to your investment portfolio and ideally, not touching it or tinkering with it in the short term, based on short-term news or short-term distractions – really just doing the right thing for the long term. That’s how you build resilience.

And then it doesn’t happen accidentally. It also doesn’t happen overnight. You have to really consciously decide to invest for the long term, do the right thing. And I promise you, over time, that’s what’s going to build reward in your portfolio.

The Finance Ghost: The sports analogy is good. I would highly recommend finding a manager who is nothing like my golf, because that will be a sad, sad journey for you and your money.

And the rugby analogy is good too, because the lesson, as we very recently learned, is that sometimes even your favourite stock, even that hero in your portfolio, can stick its finger in your eye and disappoint you, which is not great. Hence, diversification. Got to be careful with these things, right?

Nico, I think we’ve dealt with a lot of really, really cool concepts coming through here. And I guess just last question, conscious of time. This is so much for people to digest – and go back and listen to it again, and just really understand this stuff, because there has been a lot of good stuff coming through here.

We’re pretty much done with 2025. Next year is going to bring another fascinating year of insights that I certainly look forward to unpacking with you as the year develops. But perhaps, heading into the New Year, specifically from a Satrix perspective – and without giving away too much, or certainly sharing anything you are not supposed to share – what can we expect from the team in 2026, aside from just more good ETF stuff?

Anything specific that you can share with us? Or can we expect more of the same: 25 years of legacy and counting?

Nico Katzke: I think more of the same in terms of just bringing to market good value products and doing what we do exceptionally well (there’s always a temptation to just keep innovating, innovating, but at the end of the day, just keep doing what you are doing. If it works, it works), and even refining what we are doing.

So, we’ll definitely try to, for the next 25 years, repeat our success. But then, there are also quite a few exciting things coming to our market in the next year, so keep your eyes out for that.

We are definitely going to bring a few new ETFs to market. One that we recently announced is going to be a global property ETF. You mentioned property earlier. We’re going to bring to market a low-cost vehicle that allows you to invest in property ETFs globally – in other words, REITs companies.

And then there are a few other really interesting products that we’re going to bring to market or investment funds that I can’t speak to yet, but certainly, keep your eye on what we’re doing. There are some interesting things we’re going to bring to market.

The Finance Ghost: Absolutely, I can’t wait to see it. Nico, thank you so much for your time here. It really has been a treat chatting to you this year, as always. Enjoy your very well-deserved holiday with your wonderful family, and let’s do this again next year.

Nico Katzke: Absolutely. Thanks, and same to you, Ghost. Keep doing what you’re doing, keep enlightening us on the markets, and I look forward to chatting to you in the next year.

The year-end episode of the No Ordinary Wednesday podcast confronts a familiar contradiction: markets that looked buoyant, and an economy that often didn’t. In conversation with our Chief Investment Strategist Chris Holdsworth, we dissect the year’s dissonance and the lessons it leaves behind – above all, that in a noisy world, valuation discipline and diversification remain the investor’s most dependable anchors.

Please scroll down if you would prefer to read the transcript.

Hosted by seasoned broadcaster, Jeremy Maggs, the No Ordinary Wednesday podcast unpacks the latest economic, business and political news in South Africa, with an all-star cast of investment and wealth managers, economists and financial planners from Investec. Listen in every second Wednesday for an in-depth look at what’s moving markets, shaping the economy, and changing the game for your wallet and your business.

Also on Apple Podcasts, Spotify and YouTube:

Transcript:

Chapters

00:00 Introduction 01:51 What is the Global Investment Strategy Group (GISG)? 02:59 What are the core principles that anchor the GISG investment philosophy? 04:20 What defined global markets in 2025? 06:04 Why hold back at a time when markets appear optimistic 07:04 What does the GISG expect for the global economy in 2026? 08:03 What are the big risks ahead? 08:52 Outlook for the dollar 09:49 How should investors be thinking about constructing portfolios 10:14 What is South Africa’s risk score? 11:10 How does the GISG investment philosophy guard against behavioural errors? 11:58 What has 2025 taught you about investing in uncertain times?

00:00 – Introduction

Jeremy: As we reach the end of 2025, a year defined by contradictions, I’m reminded that the world of investing rarely moves in straight lines. Global markets have rallied strongly in parts, yet the mood has often felt uneasy. Inflation cooled, but not evenly. Interest rates fell, but cautiously, geopolitical tensions, flared supply chains were strained, and several major economies tiptoed along the edge of recession, while others surprised with resilience. Closer to home, here in South Africa, we’ve confronted familiar structural problems – sluggish growth, infrastructure constraints, and an unpredictable currency even as pockets of resilience have emerged. Hello, I’m Jeremy Mags, and this is the year-end episode of No Ordinary Wednesday Investec’s fortnightly podcast where we discuss the forces shaping the global economy and financial markets.

Now for investors, this has been a year of traversing fog. Moments of clarity, followed by sudden volatility, optimism punctured by risk, opportunities clouded by noise. Through it all though, one question keeps coming up – how do you invest with confidence when the world feels so chaotic? Well, to help answer that, I’m joined by someone uniquely placed to decode it all. Chris Holdsworth, the Chief Investment Strategist at Investec Wealth & Investment International. Chris is also a key member of the Global Investment Strategy Group or GISG. It’s a team that sets Investec’s global risk stance and advises on how to position portfolios across regions and asset classes. And today we are going to dig into that group’s latest quarterly global investment view, what it tells us about markets and what investors are considering as we head into 2026.

01:51 – What is the Global Investment Strategy Group (GISG)

Jeremy: So, Chris, a very warm welcome and thank you for joining us for the year’s final edition of No Ordinary Wednesday. Before we dive into the investment outlook, for listeners who may not know, maybe a good starting point is with the basics. What is the Global Investment Strategy Group and tell us what role it plays in shaping how Investec manages client portfolios.

Chris: Hi, Jeremy. As a starting point, our Global Investment Strategy Group, or GISG as we call it, is a committee populated by nine investment professionals across our UK, Switzerland, Indian and South African offices. This committee meets on a quarterly basis and the primary responsibility of this grouping of individuals is to come up with a risk score ranging from -3 to +3. Minus three would indicate they’d be very bearish, and plus three would indicate that we are very bullish. So, we take into consideration the global macroeconomic backdrop, we take into consideration valuation, we come up with a risk score and that risk score is applied throughout our business. At the moment, it’s minus 0.5 indicating that we mildly risk off and as a result our global multi-asset portfolios would all be slightly defensively positioned in the current environment.

02:59 – What are the core principles that anchor the GISG’s investment philosophy?

Jeremy: So, investment philosophies, Chris, are often tested when the markets become, and I’ll choose my word here carefully, let’s call it noisy – like we’ve seen this year. Maybe then what are the core principles that anchor the philosophy of this group and maybe which of those principles have proved most value during the course of what has been a very interesting year?

Chris: That committee looks at a variety of things, but the underlying principle is to gauge whether risk is appropriately priced in or not. So, we look at the global economy, we look at where we are in the cycle, and then we contrast that with valuation. Now that’s worked quite well this year. It doesn’t always work. And sometimes you can land up with a market that’s very stretched, becoming even more stretched. But what we have started to see in the market is some form of reversion to more normal multiples. And as a result in the US, even though the economy has been strong and earnings growth has been strong and much better than expected, the US stock market has underperformed the rest of the world. It’s underperformed Europe, it’s underperformed Japan, it’s underperformed South Africa, and I think a large part of that is starting multiples. It’s very difficult to outperform when you’re very expensive. And what we’ve seen over the last year is closer to a normalisation. It’s not complete normalistion, but closer to a normalization of valuation. And I would suggest that’s been the most important call, the most important driver, of returns over the past year.

04:20 – What defined global markets in 2025?

Jeremy: So maybe if we were to summarise 2025 – a year of dissonance might be an apt descriptor. Asset prices behaving as if the world is stabilising, but underlying data suggesting the opposite. From your perspective, then, tell us what you think defined global markets this year, and are there specific or were there specific developments that shaped your thinking?

Chris: I think there’s three. I think the defining characteristic of the past year was uncertainty. We had uncertainty with regards to trade policy in the US. We had uncertainty with regards to fiscal policy, but even so despite all of that, the global economy jus trundled along. And I think the underlying lesson from that aspect is that there is some form of resilience, which I think has been broadly underappreciated in the global economy. And maybe that’s because US households are less geared than they were before. There could be a variety of reasons for it. But the global economy has just continued to print the GDP growth rates of about 3% despite all of this uncertainty. The second point I would raise is the rally we’ve seen in commodity prices, and that typically tells us that the global economy is doing well, and I think it was a rally which wasn’t largely expected. If you look at what copper’s done over the last year, look at what iron ore has done over the last year – they’ve both been very strong, suggesting again that the global economy has been in pretty good shape. And then the third point I would raise is the weaker dollar. And that ties in with stronger commodity prices. And again, it’s been a weak dollar despite the fact that the US economy has been pretty good, strong and again, it comes back to the starting point of valuation. The dollar was very expensive. We’ve seen a normalisation in part of the year, and that’s been very helpful for emerging markets, been very helpful for commodities. So, I would suggest those have been the three defining characteristics over the past 12 months.

06:04 – Why hold back at a time when markets appear optimistic?

Jeremy: Yet your global risk score still signals caution. Why would you be holding back at a time when the markets, at least on the surface, appear to have a degree of optimism?

Chris: I think it’s because of the optimism we’re seeing in the market. We’ve got a US stock market, which is trading on a forward multiple of 23 times, which is close to the highest we’ve seen the last 30 years. And we still do have some questions around the outlook for the global economy and the US economy in particular, particularly around inflation. And if inflation proves to be sticky in the US at a 3% or maybe even above that, will the Fed be in the position to cut by as much as the market expects? And if they don’t cut by three times by September next year, which is what the market expects, what will that mean for US equities and US equities are 70% of the developed market index. So just given the combination of potentially sticky inflation and stretch devaluation, we’re mildly risk off if we’re not a -3 but we are at -0.5 and we do think some caution is justified in the current environment.

07:04 – What does the GISG expect for the global economy in 2026?

Jeremy: So, against that backdrop then, what does the group expect for the economy next year in terms of growth inflation and the trajectory of interest rates?