RCL FOODS is a South African food manufacturer with nearly 16 500 employees producing 30 much-loved brands. These include Yum Yum peanut butter, Nola mayonnaise, Ouma rusks, Pieman’s pies, Number 1 mageu, Sunbake and Sunshine bread, Supreme flour, Selati sugar, Simply Chicken, Rainbow chicken, Bobtail and Catmor pet food, and Epol and Molatek animal feed.

Key Features

Load‐shedding impacts all operations

Volumes and margins under pressure in a challenging trading environment

Earnings materially impacted by sugar industry special levy

Key Grocery brands continue to grow despite declining market

Strong underlying Sugar performance

Rainbow turnaround hampered by unrecovered feed costs

Disposal of Vector Logistics completed on 28 August 2023

We have weathered a tremendously difficult 12 months, delivering a solid underlying performance in our core Value-Added Business while negatively impacted by continued unrecovered cost pressure in Rainbow. Given the key role that we play in maintaining food security and employment in South Africa, we have focused on ‘controlling the controllables’ to deliver a stable profit while supporting cash-strapped consumers. This has included careful management of price increases, value innovation, operational efficiencies and better understanding consumer needs. As a Group we are committed to being part of the solution for a more stable and prosperous future for all South Africans.”

Are dividends always worth celebrating? Does a company paying a dividend really reward shareholders, or is this just shuffling money around?

These are the kinds of questions that Nico Katzke of Satrix discussed with The Finance Ghost on this episode of Ghost Stories. Nico is a wealth of information about the markets and these podcasts are always highly interactive.

Topics covered included:

Headlines were all over the place recently about Michael Burry shorting the US market – did the media get it wrong? What does it actually mean to short the market?

After many investors learnt the hard way that “stonks” don’t always go up, how should investors manage their mindset around volatility? Does the difference between saving and investing come in here?

What is the danger of fully allocating your portfolio to fixed income vehicles in an environment of high yields?

How important is it to include dividends when looking at equity performance?

What is the peril of trailing dividend yields vs. forward dividend yields?

What is capital allocation policy and what are the pros and cons of a management team paying dividends?

How do share buybacks work as an alternative to dividends?

Can you directly compare dividends on shares to yields on fixed income investments?

What are the dangers of the “Dividend Aristocrat” label in the US market?

What role might Artificial Intelligence play in asset management and investment strategies?

To end off the show, Nico shared how he manages his own investing every month.

Disclosure Satrix Investments (Pty) Ltd is an approved FSP in term of the Financial Advisory and Intermediary Services Act (FAIS). The information does not constitute advice as contemplated in FAIS. Use or rely on this information at your own risk. Consult your Financial Adviser before making an investment decision. While every effort has been made to ensure the reasonableness and accuracy of the information contained in this podcast (“the information”), the FSP’s, its shareholders, subsidiaries, clients, agents, officers and employees do not make any representations or warranties regarding the accuracy or suitability of the information and shall not be held responsible and disclaims all liability for any loss, liability and damage whatsoever suffered as a result of or which may be attributable, directly or indirectly, to any use of or reliance upon the information.

For more from the Satrix – Ghost Mail partnership, visit this link to find various podcasts and articl

The deal caused a substantial new issuance of shares

In what I still believe was a missed opportunity for the broader investor community in South Africa, Absa has concluded its new B-BBEE deal and issued shares that represent 7% of total shares in issue with all said and done.

In my view, the bank was in a perfect position to execute a successful structure for external Black investors. The bank can give unbeatably cheap funding and would’ve added a banking structure to the existing universe of listed B-BBEE structures.

But alas, this deal isn’t open to the public.

Sable Exploration and Mining unveils a joint venture (JSE: SXM)

The deal on the table is to beneficiate ore into magnetite

Sable Exploration and Mining is an obscure listed company with a tiny market cap. The company is raising capital and has announced a joint venture transaction that potentially gives it a cash flow positive asset.

The joint venture will commission, operate and maintain a Dense Medium Separation beneficiation plant using the ore from the Ironveld Mining Lapon mining right. Ironveld Mining is one of the indirect joint venture partners.

Sable Exploration and Mining will invest R15 million in the plant. Once the loan and interest have been repaid, a 50% share in the plant will be transferred by Sable to the joint venture partner for nominal value.

To fund the R15 million, Sable will use the proceeds of the R52.2 million rights offer that is underway. PBNJ Trading and Consulting is the anchor shareholder in Sable and has ensured that at least 90% of the rights offer amount will be raised. This takes the form of a commitment to follow rights on existing shares and an underwriting agreement.

This is a combined circular as the parties are working together on this transaction

When the board of the target company supports a buyout offer by another listed company, you’ll see them issue a combined circular. When deals are hostile i.e. the target board doesn’t support the offer, then we are in an entirely different regulatory framework where each company releases circulars.

This transaction is firmly the former, with Emira already holding 68.15% of shares in Transcend and looking to acquire the rest at a price of R6.30 per share.

Sadly, the rationale for this buyout is a story that we are seeing over and over again on the local market:

If you would like to read the full circular, you’ll find it here.

Trustco founders to convert debt to equity (JSE: TTO)

A circular will be issued to shareholders for this transaction

The founding family of Trustco has an outstanding loan of N$1.479 billion to the company. In an effort to get rid of this legacy structure, the company wants to grant a conversion option to the family to receive a similar value in shares in settlement of the loan.

The issue price would be N$1.41 per share. The Namibian dollar usually trades at 1:1 with the rand, so this would imply R1.41 per share vs. the current share price of R0.50.

This loan was the cause of a huge fight between Trustco and the JSE around the application of accounting rules. In great news for the lawyers on both sides, that fight is currently under appeal at the Supreme Court of South Africa, with the High Court having ruled in favour of the regulators and against Trustco.

The family trust of a non-executive director of Nedbank (JSE: NED) bought shares worth nearly R393k.

An associate of a senior executive of Renergen (JSE: REN) has bought shares worth over R285k.

An associate of a director of Afrimat (JSE: AFT) sold shares worth R149k.

In case you are following Kibo Energy (JSE: KBO), subsidiary Mast Energy Developments has extended the completion date for its joint venture to 21 September. This is to finalise the international flow of funds that is part of the deal.

Trematon Capital (JSE: TMT) has renewed its cautionary announcement that has been in place since July. There are no details about what the company is busy negotiating.

Sasfin (JSE: SFN) announced that Sasfin Bank’s credit rating has been affirmed by Global Credit Rating Co with a stable outlook.

I warned from the very beginning that the aReit (JSE: APO) listing looked like a dog to me. Time has proven me correct, with the latest announcement being the rather shocking update that auditors Mazars have resigned because of non-payment of fees. Despite the company trying to convince them otherwise, Mazars will not change their minds. It really does tell you everything you need to know about this company.

Unlock the Stock is a platform designed to let retail investors experience life as a sell-side analyst. Corporate management teams give a presentation and then we open the floor to an interactive Q&A session, facilitated by the hosts.

This year, Unlock the Stock is delivered to you in proud association with A2X, a stock exchange playing an integral part in the progression of the South African marketplace. To find out more, visit the A2X website.

In the 23rd edition of Unlock the Stock, we welcomed Barloworld for the first time to talk to investors about the recent performance and the way forward.

As usual, I co-hosted the event with Mark Tobin of Coffee Microcaps and the team from Keyter Rech Investor Solutions. Watch the recording here:

Clientèle managed to grow even in this environment (JSE: CLI)

The dividend hasn’t kept up with HEPS though

For the year to June 2023, Clientèle grew revenue from contracts with customers by 59% thanks to rewards revenue and single premium products. Net insurance premiums fell by 1.7% though, with higher than expected withdrawals due to tricky economic conditions.

Operating expenses jumped by 20% because of acquisition costs linked to a funeral parlour insurance transaction.

The growth in HEPS of 15% hasn’t really been driven by the core operational performance, which I think is why the dividend is only 4% higher at 125 cents per share. That’s still a very good yield on a price of R11.55 per share.

If you’re wondering what gave HEPS a boost, the major contributor was the recognition of future funeral parlour profits based on expectations around that book.

Insurance results are difficult to understand and require a lot of specialist knowledge. If you remember nothing else, just remember that this result was largely driven by improved assumptions in the long-term insurance segment. The short-term insurance book (Clientèle Legal) saw a 10% drop in profit.

Fortress: as I suspected, there’s life after REIT (JSE: FFA | JSE: FFB)

The portfolio is larger than ever and portfolio vacancies are the lowest since 2009

After all the noise around Fortress losing its REIT status, things seem to be chugging along for the company. The focus has been on recycling capital, which has led to a portfolio with a vacancy of 3.7%, the lowest since the company listed in October 2009.

Despite higher net operating income, an environment of higher prevailing rates has led to flat investment property valuations. Speaking of rates, 85% of interest rate risk is hedged for 3.5 years.

It’s worth remembering that Fortress holds a 23.9% stake in NEPI Rockcastle (JSE: NRP), one of the best performing property funds on the local market.

There’s a rather cryptic comment in the announcement about how the new Real Estate Investment Company structure might have tax benefits that reduce leakage. I’m not sure what those might be and the announcement doesn’t give any details.

The announcement notes that the A and B shares remain a difficult structure to live with. The suggestion from the company is to buy A and B shares in equal numbers to get a share of the equity of the company. Because of the threshold rules for the classes of shares, there’s no dividend on either of them for this period despite the company having nearly R1.8 billion in distributable earnings.

Hammerson makes a tender offer (JSE: HMN)

No, this isn’t something you say to your significant other

Companies like Hammerson actively manage their balance sheet, which typically includes a variety of different instruments that mature on different dates. Sometimes, a company will take proactive steps on debt that is maturing a couple of years in the future. This can be to reduce debt costs or manage the asset-liability maturity ladder on the balance sheet, depending on what the group is planning.

Hammerson has invited holders of 3.5% bonds due 2025 and 6% bonds due 2026 to tender their bonds for purchase by the company for cash. Before you panic about why this cheaper debt is being purchased early, the price for each bond isn’t 100% of the face value. It will be at a discount, so the effective purchase yield is higher.

This is complicated stuff. Fixed income instruments aren’t easy to understand. The thing to remember is that the income doesn’t change (hence the name) but the traded value does change based on the effective yield that the market is willing to pay for the instrument.

To help pay for this tender offer, Hammerson is issuing a further £100m of its existing 7.25% bonds due in 2028. This is called a “bond tap” as the company is issuing more bonds of a type that already exist in the market.

Corporate treasury management is a fascinating thing.

Volumes and revenue per ounce fell at Impala Platinum (JSE: IMP)

The release of annual results fully explains the 43% drop in HEPS

The year ended June 2023 will be remembered by Impala Platinum for the acquisition of Royal Bafokeng Platinum rather than for happy news around earnings. This is because refined 6E production fell 4%, 6E sales volumes fell 6% and rand revenue per 6E ounce declined 4%. To add further pain into the mix, the 6E unit costs increased by 14% per ounce. There’s only one direction for HEPS to move in with numbers like that, in this case a 43% drop.

The only thing that shielded this result from being a lot worse was rand depreciation. This is why Impala Canda suffered a R10.9 billion impairment, as the decrease in dollar palladium pricing was material.

Even capital expenditure increased substantially, with “stay-in-business” spend up by 16%. Replacement capital expenditure jumped 61% and expansion capital increased by 41%.

The outlook isn’t great, with a tight PGM market thanks to discounted metal flows from Russia and destocking by major PGM users. Coupled with an inflationary environment that drives higher mining costs, there’s absolutely no room for error in operations.

Nampak announces the rights offer price (JSE: NPK)

R450 million of this R1 billion raise is underwritten

The rights offer price for the Nampak capital raise has been announced as R175, which is a 23.49% discount to the 30-day VWAP of the shares.

As a reminder, R450 million of the R1 billion raise is underwritten by three investment houses. The underwriting fee is 2.33%, which is higher than I’m used to seeing but Nampak doesn’t exactly have a choice. A further R500 million of the raise has been committed to by shareholders, so in theory Nampak should get this one away.

Sanlam expects earnings to more than double (JSE: SLM)

There are many IFRS adjustments in these numbers

The introduction of the IFRS 17 Insurance Contracts accounting standard is going to cause some big movements in the numbers for insurance companies. Sanlam is a perfect example, with HEPS for the six months to June expected to rise by between 113% and 123%.

Before you get out the champagne bottles, take note that the net result from financial services per share is 20% to 30% higher. Net operational earnings per share increased by between 60% and 70%. Without taking anything away from those impressive numbers, this shows how significant the distortions are in the HEPS number for this period.

Some of the underlying drivers of the positive result include a better risk experience in life insurance, improved underwriting performance in general insurance, higher investment returns on insurance funds and stronger performance in India.

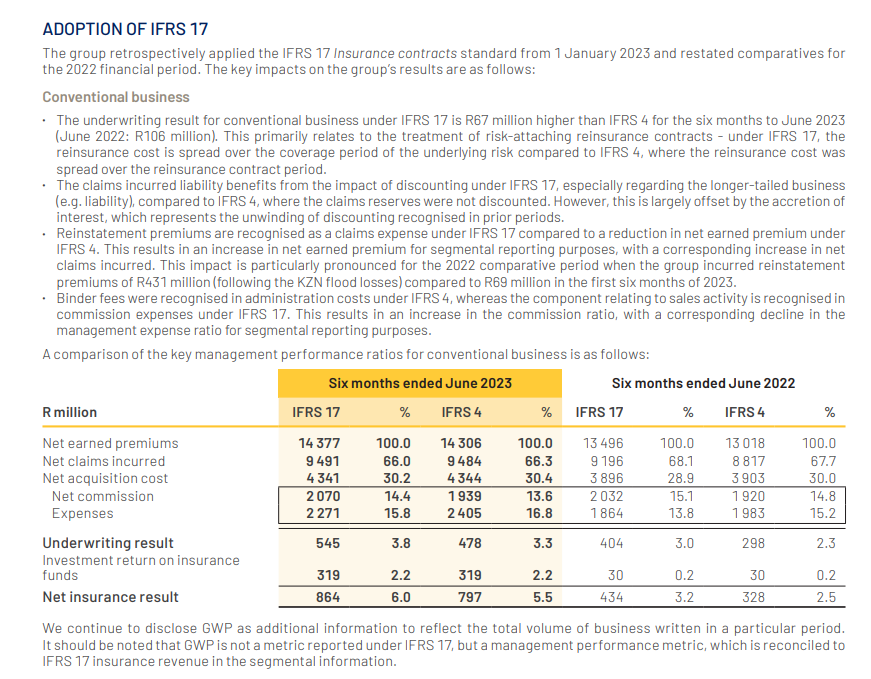

Santam has also reported a big jump in HEPS (JSE: SNT)

Like at Sanlam, the IFRS 17 insurance standard is really distorting things

Sometimes, accountants wonder why investors ignore most of what they see in odd IFRS adjustments and focus on the cash instead. IFRS 17 appears to be just as silly as the recent changes in lease accounting that caused so many distortions in retailer financials.

It’s hard to feel supportive of a change in accounting policy that leads to an outcome like a 146% increase in HEPS at Santam for the six months to June, while the dividend has only increased by 7%.

The conventional insurance business achieved gross written premium growth of 7%. Net underwriting margin of 3.8% was below the group’s target range of 5% to 10%, but was higher than 3% in the comparable period (as restated for IFRS 17). As we’ve seen at other insurers, investment returns on insurance funds also increased substantially.

Here’s an excellent example of how IFRS 17 is making it so much easier for investors to understand financial statements:

Truworths grows by high single digits on a comparable basis (JSE: TRU)

In retail, you always have to be aware of 53-week trading periods

Make no mistake, this was a decent result for Truworths. It’s just important to compare apples with apples, not apples with a fruit basket that has extra stuff in it. The comparable period is a 53-week trading period and that makes a difference. There is also a tax settlement that means SARS owes Truworths R105 million based on a long-outstanding VAT dispute.

Normally, results compared to 53 weeks would look worse than when compared to 52 weeks, as an extra week of trading in the base period means an extra week of profits to be compared to. This is the case for sales revenue but not for HEPS, as the VAT settlement has a positive impact on HEPS in this period.

For a genuine operational view on the company, the right metrics are retail sales up 13.2%, operating margin under pressure (down from 24.3% to 22.7%) and diluted HEPS (which takes into account share options etc.) up by 8.7%.

As reported, diluted HEPS is up 11.8% and the dividend is 12% higher, so they’ve maintained the payout ratio year-on-year.

Although the HEPS result is solid but not thrilling, the low valuation of the retailer relative to peers means a year-to-date share price performance of around 30%!

Little Bites:

Director dealings:

A director of a subsidiary of Dis-Chem (JSE: DCP) has sold shares worth R15.7m. That’s a pretty big disposal, with the share price down around 16% this year.

Value Capital Partners (which has board representation at the company) has bought shares in Altron (JSE: AEL) worth R10.2m.

Maria Ramos has bought R1.28m worth of shares in AngloGold Ashanti (JSE: ANG).

Equites Property Fund (JSE: EQU) released pre-close investor presentation that gives further details on the strategic focus areas of the group. You can find it here.

In case you wonder why I have such little interest in Blue Label Telecoms (JSE: BLU), here’s another perfect example of how shareholders are treated. Despite a share price that is basically flat over 3 years, management has banked a substantial tranche of 2020 share options as the performance criteria exceeded the targets. I don’t think the performance exceeded targets for investors.

Putprop (JSE: PPR) released a trading statement for the year ended June, noting that HEPS has decreased by between 16% and 21%.

Acquisitions aren’t easy, especially large ones that carry significant integration risks. Afrimat (JSE: AFT) has announced to the market that the current CFO will also act as the integration officer for the Lafarge South Africa transaction when it becomes effective, with an expected period of 6 to 10 months. He will remain as CFO, but will be assisted by internal resources who will step up for that period. This is a good indication of the bench strength at Afrimat.

DRA Global (JSE: DRA) is another JSE-listed company that doesn’t trade very often. In results for the six months ended June, the company noted a significant swing into profitability despite an 11% drop in revenue. Underlying EBIT was A$23.5 million vs. a loss of A$16.4 million in the comparable period.

Randgold & Exploration Company (JSE: RNG) is an obscure company with almost no liquidity, so I’ll give the results for the six months to June 2023 only a passing mention here. The headline loss per share deteriorated to 16.61 cents. The net asset value per share is down 19.4% to 105.39 cents. The share price isn’t very helpful because liquidity is so low, but the last trade was at 60 cents.

There might be an improvement in liquidity in Trustco (JSE: TTO) shares, with the company initiating a share buyback programme from 1 September. The maximum price is 10% above the 5-day VWAP. With such a huge bid-offer spread, the price tends to jump around a lot, so that will be an interesting one for the appointed broker to manage.

In further news related to Trustco, Finbond (JSE: FGL) is acquiring Trustco Finance Namibia and the parties have agreed to extend the fulfilment date for the conditions precedent from 31 August to 30 September.

Shareholders of Investec Property Fund (JSE: IPF) approved the change of name to Burstone Group Limited (JSE: BTN), with the new name and ticker becoming effective on 26 September.

PSG Financial Services (JSE: KST) (previously PSG Konsult) has had its credit rating affirmed by Global Credit Rating Company, which isn’t much of a surprise if you’ve been following the solid results from the group.

Aspen Pharmacare has concluded an agreement with Eli Lilly Export, a subsidiary of US pharmaceutical company Eli Lilly and Company. In terms of the agreement, Aspen will distribute and promote Eli Lilly’s products in South Africa and in certain other sub-Saharan African countries for an initial term of 10 years, automatically renewable for two further periods of five years. Aspen will pay US$41,5 million for the distribution rights.

Subdued demand for metal can products manufactured at Nampak’s Nigerian operation resulted in its closure from 31 July 2023. Nampak has since entered into an agreement to dispose of the Nigeria Metals property and equipment to Associated British Foods’ subsidiary Twinings Ovaltine Nigeria for NGN7,5 billion (c.R180 million).

In a move to internalise its asset management function, Delta Property Fund will acquire Delta Property Asset Management from the DPAM Employee Benefit Trust. The purchase consideration of R1000 will be settled by the issue of 7,692 shares to the Trust.

Sebata has acquired Valley View Industrial Park in New Germany, KZN from Reunert for R32 million. The acquisition is a Category 2 transaction and as such does not need shareholder approval.

Unlisted Companies

UEM Sunrise, a Malaysian property developer will divest from the South African market with the disposal of an 80.4% stake in Roc-Union, a provider of real estate services, to Azishe Properties for R118,4 million. The disposal is in line with the company’s turnaround strategic plan to realign its operations geographically and redirect resources to businesses and areas which offer greater potential.

South African on-line subscription platform Rentoza has raised US$6 million in funding from Alitheia IDF and Vumela Enterprise Development Fund. Rentoza dematerialises ownership of technology devices and appliances for consumers and is South Africa’s first pure play subscription model for digital goods and appliances, providing an affordable, accessible and flexible e-commerce ecosystem. The investment will be used to scale the technology enabled platform and business regionally.

InsureTech platform LeaseSurance, has raised R3 million in a seed funding round led by Fedgroup Private Capital. The platform offers lease insurance to SA’s residential operators and asset owners, reducing the administrative burden by replacing cash deposits with affordable monthly fees and so lowering bad debts. The capital injection will be used to enhance its insurance offering by further developing its technology solutions for the industry.

The Nampak Board and management are in the process of implementing various turn-around initiatives to restructure the group from a conglomerate to a business focused on specific packaging operations. To optimise the capital structure of the group, management intends to raise R1 billion via a rights issue and R2,6 billion via an asset disposal plan. In terms of the rights offer, which is to be partly underwritten to a maximum of R450 million, shareholders will receive the rights to subscribe for rights offer shares on the basis of 2.20902 rights for every one Nampak ordinary share at a 23.49% discounted price of R175.00 per rights offer share. The results of the offer will be announced on 26 September 2023.

Northam Platinum has disposed of 30,065,866 Impala Platinum shares which the company received as part payment for the sale of its stake in Royal Bafokeng Platinum. The shares were sold on the open market, raising R3,15 billion.

As part of its capital optimisation strategy, Investec Ltd acquired a further 3,146 Investec Plc shares on the open market at an average price of R105.75 per share.

Trustco has announced it is to undertake a share repurchase programme. The maximum number of shares that can be repurchased in terms of the programme is 197,447,716 shares.

As part of Investec Ltd’s share repurchase programme, the company reported this week that it had repurchased 28,461 shares at an average price per share of R104.88. Since 21 November 2022, the company has repurchased 13,6 million shares at a cost of R1,45 billion.

Prosus and Naspers continued with their open-ended share repurchase programmes. During the period 21 – 25 August 2023, a further 2,150,482 Prosus shares were repurchased for an aggregate €135,99 million and a further 322,464 Naspers shares for a total consideration of R1,03 billion.

Glencore intends to complete its programme to repurchase the company’s ordinary shares on the open market for an aggregate value of $1,2 billion by February 2024. This week the company repurchased a further 5,970,000 shares for a total consideration of £25,98 million.

South32 continued with its repurchase programme, repurchasing a further 931,147 shares this week at an aggregate cost of A$3,19 million.

Suspended in July 2020 for failure to submit its provisional report, Pembury Lifestyle Group will be delisted from the JSE on 5 September 2023 with shareholders remaining invested in an unlisted company.

The Cape Town Stock Exchange has welcomed two new listings – Thibault REIT and GAIA Renewables REIT. Thibault, a property holding and investment company with a 10.02% stake in Safari and 14,46% stake in Texton listed on the CTSE on 25 August 2023 with a market capitalisation of R103 million. GAIA Renewables which listed on 31 August 2023 is a ring-fenced REIT providing investors with access to commercial and industrial renewable energy investments in South Africa.

DRDGold will join other mining companies on A2X with a secondary listing effective 5 September 2023. This latest listing brings the number of instruments listed on A2X to 179 with a combined market capitalisation of over R10,6 trillion.

Three companies issued profit warnings this week: Murray & Roberts, Afristrat and Putprop.

Nigeria’s Dangote Sugar Refinery (DSR) has announced the terms of the proposed merger with NASCON Allied Industries and Dangote Rice. The internal restructuring will be executed through a Scheme of Merger. The offer will be 11 ordinary shares in DSR for every 12 NASCON shares and 14 DSR shares for every 1 Dangote Rice share.

Namibian investment holding company, Stimulus has announced that its subsidiary, Desert Trade Investments, has disposed of its 79.95% stake in Namibia Media and an 80% stake in Newsprint Namibia to its co-shareholder, Emeraldsand Properties, the shareholders of which are various members of the Namibia Media and Newsprint Namibia management teams. Financial terms were not disclosed.

Morocco’s fintech, Cash Plus, has acquired a strategic stake in Moroccan B2B marketplace, SLE3TI, through its cash Plus VC investment vehicle, for an undisclosed sum.

Record Resources has signed a non-binding agreement with African Minerals Exploration & Development Fund III Sicar (AMED Fund II) and Red Sea Gold and Nurtureex to acquire preferred shares in a gold exploration property in Djibouti. AMED, Red Sea and Nurtueex collectively control 69% of Thani Stratex Djibouti. Pursuant to the execution of a definitive agreement, Record Resources will acquire half of the AMED shares in return for investing US$7,5 million.

SDX Energy has entered into a non-binding Heads of Terms for the sale of all of its Egyptian assets to a large multinational operator. Additional information will follow in due course.

Tunisian startup, SeekMake has raised US$539,000 from European PE firm Lafayette Group. The company connects clients with manufacturers across 40 countries and will use the funding to accelerate its global expansion plans, predominantly into Germany and France.

HEDG, an Egyptian fintech that provides pension plans for the private sector, has raised a six-figure pre-seed funding round from local Egyptian and Sudi Arabian investors.

FMO, the Dutch entrepreneurial development bank and British International Investment have each committed US$20m to Ethiopian private sector bank, Dashen Bank. The loan will provide much needed capital for the expansion of the country’s agricultural sector.

Osino Resources Corp, the Canadian owner of the Twin Hills Gold Project, has taken a secondary listing on the Development Capital Board of the Nambian Stock Exchange, effective 29 August 2023. The company’s primary listing is on the TSX Venture Exchange.

In the cut-throat realm of corporate power plays, where alliances crumble and ambition knows no bounds, one manoeuvre stands out as the epitome of audacity and strategic cunning – the hostile takeover.

At its core, a hostile takeover is an act of calculated aggressive opportunism, whereby the acquiring firm seeks to seize control of the target entity against the wishes of the target’s incumbent board of directors, the majority of whom are at risk of being replaced.

With weakening share prices, predatory acquirers seek to obtain attractive targets at opportunistically lower prices, particularly at a time when a sufficient majority of shareholders may be looking to exit their investment in the company, perhaps also disgruntled with the incumbent executive management.

If the hostile acquirer pitches their bid to the shareholders at the right price, they can gain control of the target entity. Unlike an amicable acquisition, where the boards of both the target and acquiring firm negotiate and reach a mutual agreement on pricing, which can be pitched to shareholders through a cooperative scheme of arrangement, a hostile takeover bid is made without the cooperation of the present board of directors.

The poison pill defence

When faced with a hostile takeover attempt, the target company and its board of directors may attempt several defensive measures to try to fend off the unwanted acquirer. One of the most common methods, frequently employed on a global scale, is the shareholders rights plan, aptly coined the “poison pill” defence. This strategy involves making the target firm less attractive and more financially onerous to acquire through a series of rights and privileges that are afforded to pre-existing shareholders in the event of a hostile takeover attempt.

When triggered by a hostile bid, the poison pill provisions entitle current shareholders to subscribe for the target’s shares at a heavily discounted subscription price, thereby increasing the number of issued shares and diluting the share value, making it more difficult for the hostile firm to obtain a controlling stake. This “flip-in” share purchase arrangement was implemented by Twitter in April of 2022 in an attempt to thwart Elon Musk’s initial takeover attempts.

Restrictions on the target company’s board

However, poison pills are not without controversy, as critics argue that they can entrench management and impede shareholders’ rights. In a South African context, section 126 of the Companies Act 71 of 2008 (the Companies Act) applies, and outlines the restrictions placed on a target company’s board of directors in relation to its ability to frustrate takeover actions. In terms of this section, and in the event of a bona fide offer, the board of the target company is prohibited from engaging in any conduct or taking any action that could result in such a bona fide offer being frustrated or which could deny the target company’s shareholders a genuine opportunity to deliberate the offer on its merits.

S126 further prevents the issuing of any authorised but unissued securities; the granting of any options in respect of any unissued securities; and also prohibits any sale or acquisition of any assets of a material nature – other than in the ordinary course of business – along with any distribution that is abnormal with regard to its timing and/or amount. The impact of s126 is evident – poison pill defences, as envisaged by the Companies Act, are not permissible within the framework of South African company law.

So why, despite the prohibition of one of the most effective tools to counteract hostile takeovers, do these types of acquisitions seldom succeed in South Africa?

The role of Competition law

One of the principal reasons may be contained in the stipulations of the Competition Act 89 of 1998, as amended (the Competition Act), as well as the Competition Commission’s Rules of Conduct (the Competition Rules). In the event of a proposed acquisition, whereby a change of control would be effected, the provisions of the Competition Act and the Competition Rules dealing with merger control are triggered.

Depending on the scale of the merger, that is, if it meets the specified thresholds for either an intermediate or large merger, as determined with reference to factors such as annual turnover and asset value, the Competition Commission (the Commission) must be notified. In the event of such, notification, the merger parties (being both the acquiring and target firms) are expected to cooperate and submit a joint notification entailing, inter alia, their financial statements and board reports, as well as comprehensive business plans.

Furthermore, it is customary for the merger parties to submit a collective report to the Commission, outlining the competitive landscape of the markets within which they operate. This report also evaluates the potential impact of the merger on competition within those markets.

Alternative procedures

The cooperative nature of these engagements means that it is incredibly difficult for a hostile acquirer to secure the active participation of a target firm that is being subjected to a hostile bid. Accordingly, rule 28 of the Competition Rules anticipates this and makes provision for an alternative procedure, allowing the acquiring firm to apply to the Commission for permission to file a separate merger notification. However, there is no prescribed period within which the Commission must furnish the hopeful acquirer with its decision to permit this alternative procedure. While this can delay a merger filing, even with the Commission’s approval of the acquiring firm’s separate notification, rule 28 still affords ample opportunity for the unwilling target entity to prolong proceedings within the confines of the Competition Act.

In the event of a rule 28 notification, the target firm will be directed to prepare the relevant filing documentation pertinent to their company. As a hostile takeover generally entails resistance, the target may not be so acquiescent to this instruction; in which case, if more than 10 business days have elapsed, the acquiring firm must again approach the Commission for permission to file the aforementioned documentation on behalf of the target.

Further scope for delay

The significance of these protracted and delayed filing proceedings is that s13A of the Competition Act mandates that no merger that requires notification shall be implemented until the requisite approval has been obtained by the Commission and, on referral in the case of large mergers, the Competition Tribunal. Further, the rule 30 review period, under which the Commission deliberates on whether or not to approve a merger, can only commence once the filing process has been completed. Accordingly, delays stemming from the target’s lack of cooperation in the filing process can severely obstruct the attempted takeover.

Even if the acquiring firm is able to navigate a successful filing without the participation of the target firm and place the merger before the Commission for consideration, s13B(3) of the Competition Act allows for any party to voluntarily file any document, affidavit, statement or other relevant information with the Commission in respect of the merger in question.

If the merger is hostile, the unwilling target can use this mechanism to make submissions to the Commission, including petitioning them to prohibit the merger on the grounds that it would be anti-competitive and harmful to competition in the markets within which the merger parties operate, if such grounds exist. This could give rise to a litany of new legal complications, all of which could hinder and further delay the hostile takeover bid and its chances of success.

Difficulties with implementation

Evidently, the South African corporate landscape presents a potentially challenging terrain for the implementation of hostile takeovers, even in the absence of obstacles such as poison pill remedies and other director-driven interference. The strictures of the Competition Act, as well as the co-operative complexion of South Africa’s merger control regime, provide a resistant target firm with a plethora of opportunities to prolong merger proceedings to the point where they may become untenable for the acquiring firm. It is, therefore, unsurprising that hostile takeovers tend to fail in South Africa.

Nicholas De Decker is a Candidate Attorney. Supervised by Jeff Buckland, Director, Head of Corporate & Chairman of the Management Board | Lawtons Africa.

This article first appeared in DealMakers, SA’s quarterly M&A publication.

In the past few months, the United States’ (US) Treasury Office for Foreign Assets Control (OFAC) and the Department of Commerce’s Bureau of Industry and Security (BIS) have announced significant violations of US sanctions and export controls while imposing further sanctions on Russian and Belarussian entities. The interconnectedness of global markets means that the sanctions imposed on Russian and Belarussian entities have ripple effects on African and linked entities, particularly those involved in trade and business partnerships with the sanctioned entities. The impact of such sanctions on African entities is often indirect but existential, as they can create economic and trade disruptions, limit access to financial services, and impact reputation.

This article unpacks the OFAC listing and delisting process (OFAC listing) and discusses some of its likely impacts for African businesses.

Entities are listed by OFAC as part of a process which develops from identifying entities which may be engaging in sanctionable activities, investigating those entities and their activities, and coordinating a review with other US government agencies before publishing an OFAC listing. Collectively, the OFAC-listed individuals and entities are referred to as Specially Designated Nationals or SDNs. Being listed by OFAC imposes economic and trade sanctions on the listed entity. Upon listing, an entity is likely to experience several immediate impacts which disrupt trade and limit access to financial services.

The listed entity is likely to first be notified of its designation by its banks, which would typically inform the entity that its bank accounts will be closed. Further notices may follow from other sources, including that the entity’s US assets will be frozen, and that existing commercial relationships may be severed (especially with US companies and citizens).

After being OFAC-listed, an entity will need to apply for delisting and take other immediate actions to prevent further harm. The process of being removed from OFAC listing is complex, time-consuming and arduous.

A formal application seeking OFAC delisting must be submitted to the US Department of Treasury. The adjudication of an application is not an objective judicial process, and no third-party, independent oversight exists for OFAC delisting applications. Delisting applications also have a higher legal standard of evidence than OFAC listings, so it is easier to be listed by OFAC than it is to be removed from the OFAC list with the same evidence. Nevertheless, the US government is required to operate broadly under sets of rules and cannot act arbitrarily. Should an entity wish to engage with OFAC, OFAC is required to respond, provide information and engage with the listed entity. Further, OFAC is held to the reasons that it used to make the listing determination in the first place.

The OFAC listing of individuals poses a major challenge as people cannot change their family or their relations, but commercial businesses are different. If a commercial business becomes OFAC listed, it is important that it severs ties with any OFAC-listed entities to limit its exposure. This can include disinvestments by designated entities, removal of designated entities from commercial structures, disengaging in existing commercial ties, and changing business approaches.

US entities are generally prohibited from any commercial relationship with OFAC-listed entities. Since listed entities cannot transact with US persons, US-exposed entities may experience the most significant financial impact. Non-US persons should also be cautious of transacting with listed entities as they may be subjected to secondary sanctions. If a sanctioned entity has a controlling interest in any other entities, each of these entities is also automatically designated. Accordingly, it is important for businesses to be aware of these designations and their potential bearing on commercial activities, particularly if they have significant connections to US entities or operate and trade in US dollars.

Most financial institutions with US relationships will prevent transactions with listed entities, and financial institutions based in the European Union and United Kingdom may also adopt OFAC decisions. Financial institutions may initially be inclined to summarily terminate their relationships with designated entities, but they have a duty to act fairly and reasonably in all their dealings with clients. While the banking sector understands the scope of OFAC’s jurisdiction and ensures broader compliance with OFAC and the Organisation for Economic Cooperation and Development (OECD) guidelines, these may contradict the contractual agreements between the banks and their now OFAC-listed clients. Should African Banks service any designated entities, the banks are placed in a challenging position as they face conflicting demands in servicing or terminating their relationships with sanctioned entities.

African bank accounts may also be needed for sanctioned intermediaries to conduct their business and pay their employees and suppliers. Should a bank proceed to close its accounts, sanctioned intermediaries will have no option but to seek urgent relief from the courts and pursue a claim for damages and costs against the appropriate bank.

The only way for designated entities to reassure the banking sector is to approach the US Treasury for removal of the designation. Hence, it is important for sanctioned intermediaries to seek proper legal recourse and explore options for delisting to avoid financial, reputational and commercial damages. Given the unique nature of the application and issues to delist from the OFAC list, it is best attended to by experienced attorneys who specialise in this area.

Brandon Irsigler is a Partner, Noushaad Omarjee a Senior Associate and Davin Olen a Legal Professional Assistant | Dentons South Africa

This article first appeared in DealMakers AFRICA, the continent’s quarterly M&A publication.

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept All”, you consent to the use of ALL the cookies. However, you may visit "Cookie Settings" to provide a controlled consent.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. These cookies ensure basic functionalities and security features of the website, anonymously.

Cookie

Duration

Description

cookielawinfo-checkbox-analytics

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics".

cookielawinfo-checkbox-functional

11 months

The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional".

cookielawinfo-checkbox-necessary

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary".

cookielawinfo-checkbox-others

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other.

cookielawinfo-checkbox-performance

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance".

viewed_cookie_policy

11 months

The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Advertisement cookies are used to provide visitors with relevant ads and marketing campaigns. These cookies track visitors across websites and collect information to provide customized ads.

")

")

")