Glencore has disposed of its stake in BaseCore Metals (a base metal streams and royalties joint venture with Ontario Pension Plan Board) to NYSE- and TSX-listed Sandstorm Gold in a cash and equity deal valued at US$525 million.

In a similar deal, South32 is to sell a package of four non-core base metals royalties to LSE-listed Anglo Pacific Group for US$185 million plus contingent payments of up to $15 million. Of this $103 million will be paid in cash and $82 million in Anglo Pacific shares resulting in South32 holding a 16.9% stake in Anglo Pacific.

The Board of Transcend Residential Property Fund has received a firm intention offer from Emira Property Fund to make a general offer to acquire up to 100% of the ordinary shares in the company for a cash consideration of R5.38 per share on an ex-distribution basis. Currently Emira holds 40.69% of Transcends’ issued shares.

Capital & Regional has disposed of the residential development project in Walthamstow to specialist residential developer Long Harbour for c.£21,65 million. Proceeds will be used to reduce debt.

Old Mutual Africa (Old Mutual) has taken a significant stake in UAP Old Mutual Life Assurance Uganda following an injection of funds in a move to recapitalise the company. The life insurer’s compliance was threatened as it fell short of its solvency margins. UAP which has a 53% stake in the Ugandan business is owned by Old Mutual.

Unlisted Companies

Hyperclear, a Mauritian headquartered technology investment company, has acquired from Apex Partners, Principa, a local African and analytics software firm with operations in SA, the UK and Middle East. Principa provides data-driven solutions to the retail credit industry. Financial details were undisclosed.

DigsConnect.com, a local digital student accommodation platform which matches landlords with students seeking accommodation, has closed a pre-Series A extension round. The undisclosed investment was secured from Launch Africa, Goodwater Capital, Five35 Ventures and Delta Ventures. Funds will be used to drive international growth.

Juta and Company has acquired MedicalBrief, a weekly digest of local and global medical matters.

Infra Impact Mid-Market Infrastructure Fund 1, has acquired a minority stake in Cybersmart, a local internet service provider and fibre network operator. The funding will be used by Cybersmart to solidify its brand and accelerate the rollout of connectivity solutions.

Imperial, acquired in 2021 by DP World, has expanded its African presence with the purchase, via its Market Access business, of a controlling stake in Africa FMCG Distribution (AFMCG). Part of the Chanrai Group of Companies, Nigerian-based AFMCG is a multi-faceted business offering nationwide and route-to-market solutions across multiple channels.

California-based seller of fresh strawberries and other berries Driscoll’s is to purchase Haygrove Africa Trading, a local supplier of blueberries in sub-Saharan Africa. Financial details were undisclosed.

As part of its update to the market on its Yamana Gold deal, Gold Fields announced it will list on the Toronto Stock Exchange. This announcement together with the promise of higher dividends should sweeten its proposed takeover.

Naspers and Prosus continued with their open-ended share repurchase programmes. This week the companies announced that during the period 4th to 8th July 2022, a total of 6,240,339 Prosus shares were acquired for an aggregate €418,95 million and 659,095 Naspers shares for R1,75 billion.

British American Tobacco repurchased a further 960,000 shares this week for a total of £32,56 million. The purchased shares will be held in treasury with the number of shares permitted to be repurchased set at 229,400,000.

Glencore this week repurchased 7,529,983 shares for a total consideration of £31,92 million in terms of its existing buyback programme which is expected to end in August 2022.

One company issued a profit warning. The company was: Sebata,

Four companies this week issued or withdrew a cautionary notice. The companies were: Sebata, Pembury Lifestyle, African Equity Empowerment and Ascendis Health.

A company may reorganise its shares/securities by implementing a scheme of arrangement if approved by a supermajority of at least seventy-five percent of the shareholder votes exercised on the scheme, provided that other statutory requirements are satisfied.

Once shareholders approve a scheme of arrangement by a supermajority, it is binding on all shareholders. The dissenting shareholders, however, are not left without recourse. They may approach the court within ten business days after the date on which the shareholders voted on the arrangement, as contemplated in section 115(3), or exercise their appraisal rights in terms of s164.

Generally, when proposing an arrangement to holders of all shares rankingpari passu, all shareholders will be entitled to vote on such a proposition. However, which class of shares is entitled to vote on an arrangement proposed to holders of only one class of shares in a company with different share classes that do not rank pari passu? We will briefly respond to this question.

The Companies Act 71 of 2008

S114(1) of the Companies Act 71 of 2008 (the Act) provides that a company’s board may propose and implement an arrangement between the company and the holders of any class of shares. In other words, a proposition between a company and holders of one class of shares in a company with varying share classes is legally sound. Transactions in respect of consolidation of class securities, division of class securities, expropriation of class securities, exchanging securities in the company for other securities, reacquisition of securities, or a combination thereof may be implemented by way of a s114 arrangement.

Before a proposed arrangement is implemented, shareholder approval must be obtained in compliance with s115(2), read with s115(4) of the Act. S115(2) requires the proposition to be approved: (i) by a special resolution adopted by persons entitled to exercise voting rights on such a matter; (ii) at a meeting called for that purpose; and (iii) at which sufficient persons are present to exercise, in aggregate, at least 25% of all the voting rights that are entitled to be exercised on that matter, or a higher percentage as may be determined by the company’s Memorandum of Incorporation. Furthermore, the voting rights that are controlled by the acquiring party, a person related to the acquiring party, or a person acting in concert with either of them must not be included in calculating the requirements of a quorum or a special resolution for purposes of s115(2).

Share classes that do not rank pari passu

While s311(2) of the Companies Act 61 of 1973 (the 1973 Act) expressly provided that an arrangement proposed between a company and any class of its members must be agreed by a majority representing three-fourths of the votes exercisable by that class of members present and voting either in person or by proxy at the meeting, such expressive language regarding class resolutions does not form part of the wording in s115(2) of the Act. S311(2) of the 1973 Act also provides that if a class arrangement is approved, it will be binding on that class.

In Verimark Holdings Limited v Brait Specialised Trustees (Pty) Ltd NO and Two Others (2009) ZAGPJHC 45, Malan J held, for the purposes of s311(2), that an arrangement that is proposed to class members entitles those members “to whom the offer is made” to vote on such arrangement. In paragraph 10, Malan J confirmed that categorisation of a class of members for purposes of s311(2) involves a determination of the “similarity of rights and not the similarity of interests”. In a recent case, Sand Grove Opportunities Master Fund Ltd and Others v Distell Group Holding Ltd and Others (6378/2022) (2022) ZAWCHC 46, Binns-Ward J endorsed the approach adopted in the Verimark case on the issue of categorisation of classes of shareholders when observing that, for the purposes of differentiating shareholders into separate classes, the focus is on dissimilarity of shareholders’ rights, not interests. According to Binns-Ward J, the shareholders’ rights should be sufficiently similar to make it feasible for them to consult together regarding, for example, a proposed arrangement.

Unlike s311 of the 1973 Act, s115(2) of the Act requires,inter alia, approval by a special resolution adopted by “persons entitled to exercise voting rights on such a matter”. The Distell case in paragraph 81, states that “section 115 provides for a company meeting and not a meeting of classes of shareholders as used to be the case under section 311”. Binns-Ward J goes on to state that “it is incumbent on the directors, presumably following the advice of the independent board and with due attention to the content of the independent expert’s report, to consider and determine on the most appropriate manner in which to comply with section 115(2)”. Furthermore, Binns-Ward J states in paragraph 88 that “any company concerned with convening a meeting in terms of section 115(2) must conduct itself mindful of the same considerations that the court used when deciding an application in terms of section 311 of the Companies Act 61 of 1973”.

Being mindful of the above principles, we submit that the determination of the approval procedure required with regard to an arrangement proposed to holders of a share class must begin by establishing whether any existing share classes have distinguishable rights in relation to the arrangement or not. If so, it is such class that is entitled to vote on the arrangement. Put differently, the shareholders to whom the same proposition is made, and whose rights will be affected in the same manner by the proposed arrangement, will constitute the scheme participants and should be allowed to consult on common rights. General votes – for example, of all shareholders whose interests are affected in some manner by the arrangement, rather than those whose rights are affected in the same manner – would otherwise have the potential of leading to absurd results, in that a particular class of shareholders may have their shares reorganised in circumstances where none of them has consented thereto. By way of example, if the share class of the scheme participants constitute only 10% of the issued shares, a resolution approved by all shareholders, including those to whom a classification arrangement was not proposed, would result in the reorganisation of the share class of the scheme participants only.

The Distell case also establishes (correctly, we submit) that the responsibility to make the determination of whether a special resolution from a particular class of shareholders is required rests with the company’s board. In doing so, it should follow the advice of the independent board and have due regard to the content of the independent expert’s report.

The role of the TRP in respect of regulated companies

The Distell case also reaffirmed the mandate of the Takeover Regulation Panel (TRP) in relation to schemes of arrangement. In paragraph 81, the court held that the TRP is permitted “to direct the holding of an appropriately constituted separate meeting” by class shareholders for purposes of s115(2). Binns-Ward J cited s119(2)(b)(ii) of the Companies Act, in terms of which the TRP needs “to ensure that all holders of ‘voting securities of an offeree regulated company are afforded equitable treatment, having regards to the circumstances’”. As a result of this case, we believe that the TRP will be more vigilant in ensuring the equitable treatment of shareholders where an arrangement is proposed to a particular class of shareholders in a company with varying classes of shares, and that the principles set out in the Distell case are likely to be considered in the exercise of its mandate.

Conclusion

While all shareholders of a company may be entitled to vote on an arrangement that is proposed to all shares of the company for purposes of s115(2) read with 115(4), it might be difficult to determine whom the “persons entitled” to vote on a class scheme should be for the purposes of s115(2). In light of the Distell case, we submit that all circumstances, including the rights attached to the class of shares, the identity of the holders of such shares, the advice of the independent board, and the independent expert’s report should be taken into consideration when deciding on whether or not a special resolution passed by a specific class of shareholders is required for the purposes of s115(2).

Julius Oosthuizen is HOD, Prince Mathibela a Trainee Associate, and Olwethuthando Ndlovu, a Candidate Legal Practitioner in Corporate Commercial | ENSafrica.

This article first appeared in DealMakers, SA’s quarterly M&A publication

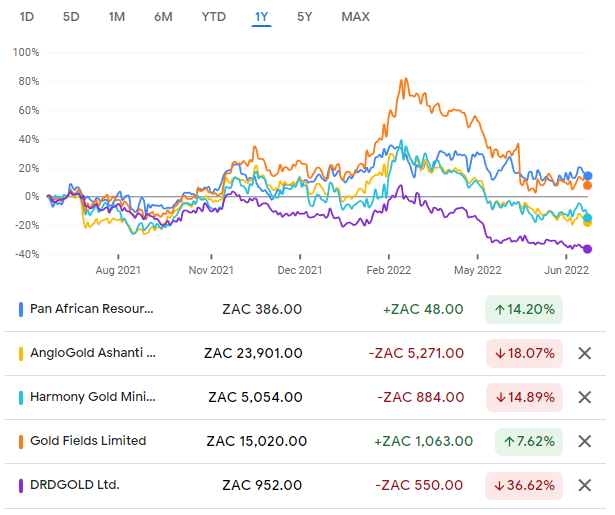

The gold sector has been a source of great disappointment for me. Most irritatingly, when I bought a basket of gold shares at the beginning of 2021 without spending enough time researching the sector, I managed to leave Pan African Resources out of the portfolio. That was a mistake.

Pan African has just wrapped up the financial year ended June 2022. With full reporting only due in September, the group has released an operational update that kicks off with an exciting headline:

“Record annual gold production and significant reduction in net senior debt.”

Every CEO dreams of being able to tell a story like that to the market, especially when competitors have either had major production hiccups or are busy chasing huge international deals.

Over the past year, Pan African has been the top performer in the sector:

More gold

Production is only up by 2% vs. FY21, so don’t get carried here with expecting tech company growth rates. Still, that’s a move in the right direction. Pan African didn’t expect such a favourable result this year, as actual production of 205,459oz of gold is around 5% higher than initial guidance.

There are five major mining operations in the group and four of them performed better than last year. The Sheba and Consort underground operations saw a disappointing drop of nearly 30% in production. This is thankfully the second smallest operation in the group.

Pan African has given conservative guidance for FY23, with a plan to maintain production at FY22 levels.

Less debt

The gold price hasn’t been terribly exciting over the last year, but it has been at a level that allows Pan African to make money. When coupled with strong production numbers, that means a year of debt reduction and value creation for shareholders.

The extent of the reduction is astonishing. Debt is down 71.5% year-on-year or 59.8% since the end of December 2021. Pan African Resources reports in US dollars and so these numbers are subject to the wildly volatile dollar movements. I checked in the integrated report and it looks like the debt is with local banks and denominated in rand, so I would prefer to consider the percentages based on the change in the rand value. In that case, debt is down 68% year-on-year, which is still excellent of course.

More energy

Pan African has commissioned a 10MW solar PV renewable energy plant at Evander, the first of this scale in the South African mining industry. The Barberton 8MW solar PV renewable energy plant site establishment has also commenced.

Fewer injuries

Pan African has a strong safety record. There were improvements in the recordable injury frequency rate (RIFR) and the lost time injury frequency rate (LTIFR). Far more impressively, Barberton Mines achieved 2 million fatality free shifts on 10 May 2022 and the Evander / Elikhulu operations achieved 2.5 million fatality free shifts on 19 January 2022.

More blueberries

I just couldn’t help but highlight an unusual ESG update. At Barberton, the commercial harvesting of blueberries has commenced.

Frankly, based on how the gold price is behaving at a time in the world when it should be doing well, perhaps blueberries would be the most profitable route forward.

I look forward to the full results in September, particularly with details around costs and margins. This is where things have gone wrong for gold miners, as the gold price isn’t increasing at a fast enough rate to offset the inflationary pressures on mining costs.

There’s more action in the property sector, with Emira Property Fund making a general offer to acquire all the shares it doesn’t already hold in Transcend Residential Property Fund. Emira holds a 40.69% stake, a position that has been built up since late 2018 through underwriting acquisitive growth by Transcend i.e. injecting capital for ongoing property purchases. Emira’s rationale talks to an overarching theme on our market: JSE investors have gone cold on multi-layered structures that offer various entry points into the same or a similar basket of assets, usually resulting in a significant discount to underlying value. The offer price of R5.38 per share looks somewhat stingy though, with a premium of just 10.5% to the 90-day volume weighted average price (VWAP). This is significantly lower than the control premium we typically see in JSE buyout offers. Despite this, a major holder of 16.7% of Transcend has already said yes. This tells you something about the lack of liquidity in the stock, as Transcend has a market cap of under R1 billion. Transcend’s net asset value at 31 December 2021 was R8.08 and the company has reiterated guidance for a FY22 dividend of 57.50 cents. The offer price is a guided forward yield of 10.7%. Transcend will issue a response circular in due course. Take note that this is a general offer, not a scheme of arrangement and attempted delisting. In other words, Emira is happy to mop up any number of shares at this price.

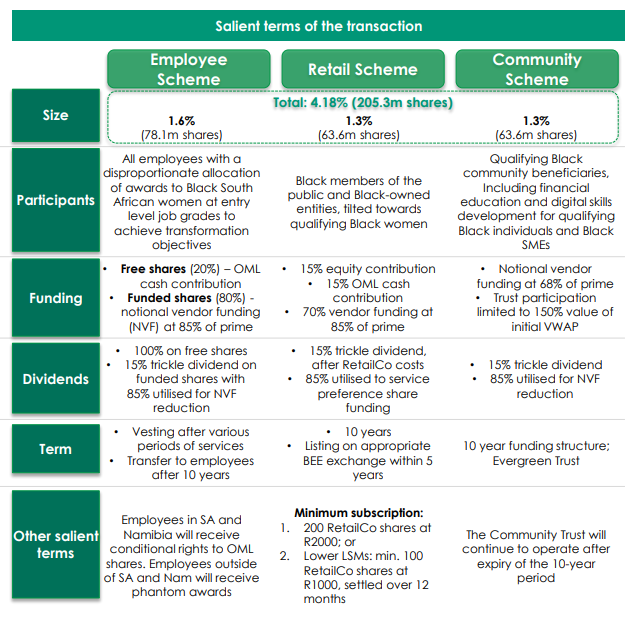

Old Mutual has released the circular related to the proposed Bula Tsela B-BBEE transaction. This is a complicated structure that will see a 4.2% stake held by three types of investors through the issuance of new shares. An employee ownership scheme will hold around 1.6%, a community trust will hold 1.3% and qualifying members of the public will hold 1.3%. The shares held by the public will be listed on a B-BBEE exchange within the next 5 years, so there’s no liquidity here for a long time. There’s a useful summary on the Old Mutual website that I’ve included below. You can find all the documents, including the circular and earnings transcript, at this link on the Old Mutual site.

Earnings updates

None – come back tomorrow!

Share buybacks and dividends

As there were no other buybacks or dividends, I may as well remind you that British American Tobacco and Glencore are buying back shares on a daily basis.

Notable shuffling of (expensive) chairs

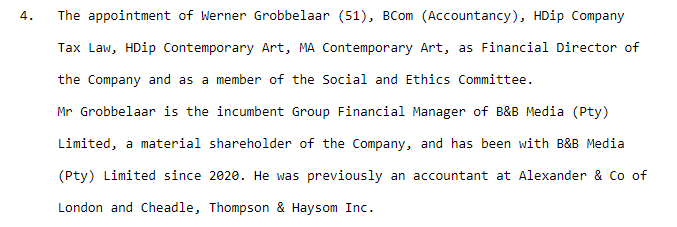

The board changes at Buka Investments (previously Imbalie Beauty and I can’t find a new website yet) have been made, with the ex-CEO staying on in a non-executive role. I have to highlight the appointment of a certain Werner Grobbelaar, who has such an interesting variety of degrees that it warrants a screenshot. For more on Buka Investments, read this feature article by Ghost Grad Kreeti Panday.

The CEO of Newpark REIT (the tiny property fund that owns the JSE building and 24 Central in Sandton along with a couple of other properties) has resigned to “focus on other opportunities” – I would also be bored if I was running a portfolio that I could count on one hand. Auri Benatar will be taking over and has previous experience as the Head of Acquisitions and Disposals at Redefine, so that’s an interesting development. Pun intended. This share almost never trades on the JSE, which is rather ironic since they own the building.

Director dealings

A director of PSG closed out a zero-cost collar structure with a South African bank that was related to a loan agreement. The bank exercised its call option and bought R8.7 million worth of shares at a price of R49.33. The current traded price is around R85.

Capitalworks is a long-standing partner of listed food business RFG Holdings. After the private equity investment house bought R195k worth of shares at the end of June and another R154k earlier this month, there have been more purchases with an aggregate value of nearly R108k. This is announced on the market because two of the RFG Holdings directors are from Capitalworks.

Unusual things

I don’t usually comment on institutional ownership, as this can change significantly for a multitude of reasons. With the Tiger Brands share price having caught a bid in the past month, I’ll highlight that the PIC has increased its stake above 15%. At least we know who one of the recent buyers was.

Steinhoff is going to bleed more cash for its poor prior behaviour, with an administrative fine from BaFin (the financial regulator in Germany) for late publication of the 2016/2017 annual financials and for failing to publish voting rights notifications within the prescribed period. They don’t play games in Germany. The fine is a whopping €11.3 million (R192 million) payable in three similar-sized tranches between March 2023 and September 2024. Steinhoff has lost around half its value this year, so I’m very glad I took my profit after the strong run in 2021. The company will be hosting a virtual analyst day on Friday 29th July.

Jubilee Metals has announced important updates regarding the copper and cobalt strategy in Zambia. The cobalt refining circuit at the Sable Refinery entered the commission phase during June 2022 and commercial production is targeted for August 2022. The Project Roan concentrator has reached 65% of designated capacity and should reach 100% by the end of July, which would mean 830 tonnes of copper concentrate per month. Jubilee has come a long way, with operations across PGMs and chrome in South Africa and cobalt and copper in Zambia.

If you enjoyed Ghost Bites, then make sure you’re on the mailing list for a daily dose of market insights in Ghost Mail. It’s free! SIGN UP HERE >>>

At times when global markets are falling, inflation is rising and there are no clear signals on whether to buy or sell – like now – a diversified portfolio that includes an alternative asset class looks appealing. In OrbVest’s view, medical real estate in the US can be considered a “safe-haven asset” because it offers a stable income stream alongside wealth preservation.

Medical tenants are reluctant to move, so they enter into long-term leases. With net leases commonly in place (i.e. costs are for the account of the tenant) and escalation clauses generally built into the leases, these medical real estate assets offer attractive US dollar returns and protection against inflation.

OrbVest has now made this even more attractive for South African investors, with a minimum investment size of just $1,000 and the ability to invest into OrbVest Diversified Holdings (ODH), spreading risk beyond a single tenant or building.

To help us understand more about the OrbVest business, Justin Clarke (Operational Director at OrbVest) joined me on this episode of Ghost Stories. Before delving into this asset class and the structure behind the investment opportunity, Justin shared his fascinating back-story as the founder of Private Property. The business managed to survive two global crises and attracted funding from Tiger Global Management as part of a wild journey of building a tech platform during the early days of the internet.

This episode includes great insights into Justin’s life as a founder and now his role at OrbVest, so there’s truly something here for everyone.

Click here to read more about OrbVest. Please remember that past performance is no guarantee of future returns. OrbVest SA (Pty) Ltd is a registered FSP with registration number 50483.

Listen to the episode using the podcast player below:

There’s been some buzz around MultiChoice recently, as French investor Groupe Canal+ has built its stake up to over 20%. Ghost Grad Sinawo Bikitsha wonders whether there’s something bigger on the horizon.

There is no word on this planet that irritates South Africans like the word “MultiChoice” (Ghostly editor’s note: I would wager that Eskom takes first place). With the company facing a tough consumer climate and plenty of new competition from streaming players, why is a massive French broadcasting empire so interested in cute and vulnerable MultiChoice?Hmm.

Slow and steady

Last week, MultiChoice Group announced that a French broadcaster named Groupe Canal+increased its shareholding in the JSE-listed South African broadcaster to 20.1%. Canal+ has been building up the stake since 2020, when it moved through the 5% threshold to hold 6.5% in MultiChoice.

Local regulations require an announcement to be made whenever a shareholder moves through a 5% shareholding level. This helps us keep track of potential corporate actions.

It’s usually cheaper for a company to build up a stake slowly, as the price paid for the initial shares is the market price. When a buyout offer is made, a control premium needs to be offered to entice shareholders to accept the offer. This premium is usually between 20% and 40% over the traded share price. If you can be patient, it’s better to go slowly in the beginning and mop up a decent stake before potentially making the big offer.

Who is Canal+?

Canal+ is a French broadcasting and streaming company that operates in Europe, Asia and Africa. The French broadcaster has around 24 million subscribers worldwide.

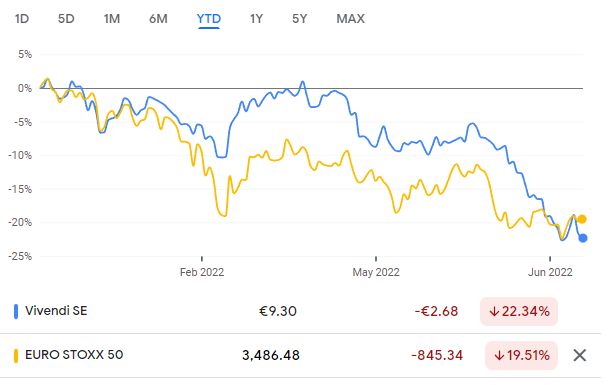

Canal+ is owned by Vivendi, a French company with artistic diversity in television and cinema, publishing, videogaming and live entertainment, just to name a few. Vivendi is listed on Euronext Paris. In addition to Canal+, the parent company owns stakes in publishing company Editis, French multinational advertising company Havas, media press Prisma Media, distribution platform Dailymotion and video gaming company Gameloft.

In 2022, Vivendi has underperformed the EURO STOXX 50 index (though both have taken plenty of pain):

French kiss number 1: an offer in 2018

There was a rumoured deal in 2018 that most people aren’t aware of.

Before Canal+ bought MultiChoice’s shares, various news sources suggest that Vivendi tried to acquire MultiChoice Group in 2018. At that stage, MultiChoice was still part of Naspers and the deal was rejected. In 2019, MultiChoice was unbundled by Naspers and separately listed.

The French lover clearly didn’t handle the rejection well. With MultiChoice now separately listed and the shares trading on the open market, Canal+ put plan B into action and began building its stake in 2020, having doubled its shareholding in the MultiChoice Group by November 2021.

MultiChoice stated that the Group would keep an “open mind” in the relationship with Canal+. The commentary coming from Canal+ painted a story that it viewed the MultiChoice stake as a financial investment. It’s unusual (though certainly not unheard of) to see a company holding a financial investment in another company in the same industry. This would typically be a strategic investment, opening the door to something bigger.

Interestingly, Groupe Canal+ has been acquiring other rising African media houses. The parent company Vivendi is vigorously searching for new pay-television and magazine acquisitions. In fact, Vivendi has quite the reputation for taking part in aggressive takeovers.

In 2019, Groupe Canal+ acquired ROK studios, a Nigerian TV and film production house. This year, the French media house acquired Rwandan streaming service ZACU TV, enhancing the group’s position in East Africa. Canal+ maintains that the Group’s main target is to produce pleasing content for African subscribers. Evidently, Vivendi is steadfast in growing its presence in Africa’s TV and film industry, with the French empire criticised at times for being a bit bullish.

French kiss number 2?

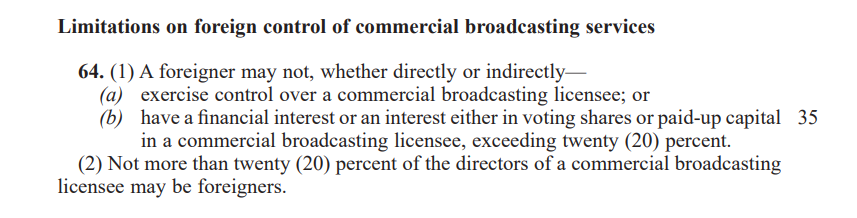

Here’s the problem: section 64 of the Electronic Communications Act, 2005 says that foreigners cannot have an interest in a commercial broadcasting licensee of more than 20%. There’s clearly already a problem, though the word in the market is that MultiChoice’s MOI limits voting rights to 20% for foreigners regardless of how much they hold. This doesn’t deal with the “financial interest” point though, which is in black and white in the Government Gazette:

It’s not obvious how Groupe Canal+ could increase its stake from here. This means that either (1) it really is a financial investment, (2) Groupe Canal+ is looking to do a content deal with MultiChoice or (3) there’s a chance that the rest of Africa business gets carved out and sold to the French, which would make some sense from a language perspective. These options aren’t mutually exclusive.

For now, I’m an unhappy consumer. MultiChoice has increased DSTV subscription prices and reduced channels. Whilst I must commend MultiChoice for being able to secure Disney+ for DSTV Explora Ultra subscribers, I just don’t find the story very appetising. If this was breakfast in Paris, MultiChoice would be the overbeaten egg whites with an irreversible curdled texture rather than foamy soft deliciousness .

Yet, Canal+ is interested in MultiChoice. They clearly see something more interesting in the story than I do. If anything, the Phuthuma Nathi B-BBEE structure is where I would invest.

In Tiger Brands’ results for the six months to March 2022, the company noted that the structured disposal of the Deciduous Fruits business had been terminated. In other words: there was no sale. The social impact of the closure of this business in Ashton would’ve been severe. Although a “significant number of parties have expressed an interest in further discussions on the possible acquisition of the business” (note the fluffy wording as there is nothing concrete on the table), a new deal can’t be done in time to put the preparations in place to process the next crop. After engaging with various stakeholders, Tiger Brands has agreed to extend operations for a further season, with the terms of that agreement “significantly mitigating the risk of operating losses” in this season. This preserves 250 permanent and 4,300 seasonal jobs. The announcement doesn’t give further details on the terms that were agreed, so I’m not sure who is taking the financial knock here. Although this story is by no means over, I’m glad that a solution has been found for the town for another season.

Tongaat Hulett announced that Artemis Investments has increased its stake in the company to over 10%, which was enough to send the share price over 32% higher before things “calmed down” to be up 20% by afternoon trade. When a company is very sick, any good news sends the market into a frenzy. In this case, people were clearly inspired by an important shareholder increasing its stake.

South32 has agreed to sell a package of four non-core base metals royalties to Anglo Pacific Group (listed in London) for a price of between $185 million and $200 million depending on whether certain conditions are met. The royalties will be paid for with $103 million in cash ($48 million immediately and $55 million over 18 months) and $82 million in Anglo Pacific shares. After this deal, South32 will hold a 16.9% interest in Anglo Pacific. Even after this sale, South32 owns a package of 36 royalties at different stages of maturity, weighted towards base metals. The royalties were carried as an intangible asset with nil value, so South32 will recognise a large gain on sale here.

City Lodge has confirmed that it has received the proceeds from the sale of the East African operations and has used them to repay debt. In addition to this good news, loan facilities have been refinanced at more favourable terms. The SENS ends off on a strong note to say the least:

“The Company…together with the improved operational performance…finds itself in a robust operational and financial position.”

City Lodge update 12 July 2022

Ascendis seems to be juggling many balls at the moment and most of them are usually on fire. The Skin business was disposed of in June 2022 and the sale of the Medical business has been terminated. The Pharma business is still earmarked for disposal to a joint venture between Pharma-Q and Imperial. In the event that shareholders don’t approve that deal, the company is negotiating a backup sale of the Pharma business to Austell Pharmaceuticals. The Category 1 circular was supposed to cover the Medical and Pharma sales, so it had to be amended to only make reference to the Pharma sale. The Takeover Regulation Panel (TRP) has given dispensations regarding the timing of the distribution of the circular, as the proposed strategy to fix the balance sheet has changed so many times in recent months. Shareholders can now expect to receive the circular before the end of August 2022.

Silverbridge Holdings is currently under offer from ROX Equity Partners at R2.00 per share. Three directors have given notice of their intention to accept the offer, including the CEO, deputy CEO and chairman. That sends a pretty strong message to shareholders. The offer circular will be published by 21 July.

Redefine is busy with a debt capital markets roadshow this week. Of course, the presentation to debt investors about the fund is just as relevant to equity investors. If you would like to work through the presentation, you’ll find it here.

Earnings updates

Tharisa has released a production report for the third quarter ended June 2022. PGM production was slightly down from the preceding quarter and chrome production was higher. The Vulcan Plant is delivering a steady improvement in chrome recoveries. The PGM basket price has dropped by 4.6% vs. the second quarter but chrome has headed in the right direction and with a vengeance, up 39.5%. Tharisa notes that the “growth strategy remains firmly on track” and highlights its positive net cash position of $48 million. The group also highlights that its 10MW of standby power means it has had negligible disruption from Eskom. PGM guidance for the full year has been maintained but chrome guidance has been decreased by 10% due to lower chrome feed grade and a slower ramp-up than expected at the Vulcan Plant. The management team joined us on Unlock the Stock at the end of June to give a presentation on the business and respond to questions. You can find the recording here.

Sebata Holdings has released a trading statement for the year ended March 2022. The headline loss per share has skyrocketed to between -440.83 cents and -446.53 cents vs. -28.46 cents in the prior year. Don’t let the 18.6% share price jump on the day fool you – there was one trade in the morning that drove that, with the large jump a result of the bid-offer spread that you could park a truck in.

Share buybacks and dividends

Lewis Group is perhaps the best example on the JSE of the power of share buybacks. Despite operating in a country and sector that hasn’t exactly been easy, shareholders have enjoyed a great run. Share buybacks have been a major driver of this growth, with Lewis repurchasing shares at a low valuation multiple. The company has already used up the 10% buyback authorisation from the last AGM and has requested another 10%. This needs to be approved at a special general meeting and a circular has been sent to shareholders that you’ll find at this link.

Accelerate shareholders have already been told about a cash dividend of 21.98051 cents for the year ended March 2022. There is a share reinvestment alternative based on a price of R0.70 per share, significantly lower than the current market price of R1.29. Like all companies that offer such an alternative, Accelerate is hoping to entice shareholders to reinvest the cash so that the company effectively hangs onto it.

Industrials REIT has announced the exchange rate applicable to the dividend, which will result in a dividend of 70.08172 cents per share. There is a scrip dividend alternative (shareholders can receive shares instead of cash) but the price for that alternative is R29.80 which is slightly higher than the current market price.

The numbers at Prosus and Naspers are just staggering. Last week, the companies repurchased shares worth $429 million and almost R1.75 billion respectively.

Notable shuffling of (expensive) chairs

I tend to ignore changes in non-executive directorships, as these are usually focused on governance rather than strategy and such changes are common on the JSE. The latest appointment at Afine Investments is different, with Gary Du Preez appointed to the board in a non-executive role. He has over 36 years of experience in developing service stations, with direct responsibility for over 90 service station developments. Mr Du Preez is a director of Terra Optimus, a company you’ll recognise from the shareholder register of Afine. Notably, Peter Todd has resigned as a non-executive director of the company. I’m sure he will pop up soon in a new listing!

Director dealings

The ex-CEO of KAP Industrial Holdings (now a non-executive director) has disposed of shares in the company worth nearly R1.6 million, just before the closed period started in July. It’s small relative to his total stake but isn’t a great signal.

An associate of the CEO of Sirius Real Estate has bought shares in the fund worth around £4k.

The CFO of Famous Brands isn’t messing around, taking on more leveraged positions in the stock. This time, the value is R439k. The stock is down over 20% this year, with the removal of mask mandates hopefully providing the catalyst for a recovery in this sector.

Unusual things

Anglo American has announced first production of copper concentrate from its Quellavaco Project in Peru. It’s taken four years since project approval to reach this point, which is impressive when you consider that this included a couple of years of the pandemic. The mine will increase Peru’s copper production by 10% and create 2,500 direct jobs. The mine is now in final testing before being given clearance for full commercial operations.

Harmony Gold’s financial year ended in June and the group has given us an update on production numbers and various other matters. Harmony has achieved the total production guidance of between 1,480,000 and 1,560,000 ounces. We have to wait for further announcements to get more financial information about the FY22 performance. Loss-of-life prevention remains at the top of the priority list, after 13 mineworkers sadly lost their lives in FY22. Related to safety, it’s interesting to note that the Bambanani mine near Welkom is being closed by Harmony due to increased seismic activity in the region, with the staff redeployed to other Harmony mines. The announcement also reminded the market that Harmony raised R1.5 billion in a sustainability-linked debt facility that will be used for renewable energy projects.

If you enjoyed Ghost Bites, then make sure you’re on the mailing list for a daily dose of market insights in Ghost Mail. It’s free! SIGN UP HERE >>>

Imbalie Beauty recently released its last integrated annual report under that name. There has been yet another name change for this listed company, along with a significant change of strategy under new owners. Ghost Grad Kreeti Panday books a nail appointment and unpacks this story for us.

Back in 2007, Placecol Holdings acquired the Dream Nails group and the entity was listed on the AltX, which is where companies list on the JSE in the hope of eventually growing into large groups with a vibrant shareholder register. Sadly, liquidity is virtually non-existent on the AltX and most companies never move from the AltX to the Main Board.

A 2007 listing marked the top of that bull market cycle, a golden period in South Africa when the Ghost was starting university and I wasn’t even in primary school. The top of a cycle is when you see the more unusual, risky listings come to market, as there is strong appetite from investors to take a chance and win a prize (or not, as is often the case).

Having survived the Global Financial Crisis, the name change to Imbalie Beauty only took place in 2012 after the group acquired the Perfect 10 group of beauty salon franchises. Our country had embarked on a “lost decade” by then and Imbalie doesn’t have a pretty story to tell, despite operating several skincare brands in addition to the beauty salons and skin care clinics.

There were problems long before Covid

Imbalie was reporting headline losses long before Covid came to our shores and replaced beauty masks with cloth masks. After a painful rights offer in 2018 to recapitalise the business, the JSE censured the business in 2019 for publishing information related to the underwriting of the rights offer that was misleading to shareholders.

In 2020, Imbalie Beauty suffered great losses due to the Covid-19 lockdown as beauty salons were forced to close for 87 days. The financial losses arguably paled in comparison to the tragedy of women being forced to endure their unibrows and cracking nails for 3 months.

The group’s loss worsened from R2.16 million in 2020 to R9.37 million for the year ended February 2021, a deterioration of around 332%!

Manicures, pedicures and (attempted) financial cures

If things were tough before the pandemic, you can imagine how quickly things fell over during the lockdowns. The group fought for survival, but it was just too hard.

The i-BLOOM name was launched to the market during lockdowns, with an increased push into training and education with the i-BLOOM Beauty & Wellness Academy. This is an international training platform directed at cultivating specialists in the beauty and wellness industry. To complement this, Imbalie created a Customer Solutions Division in August 2020, with the aim of building salon-quality products that customers could use within their own homes as well as the training of therapists to provide home-based solutions.

CEO Esna Colyn described this initiative as a way to give new opportunities to women who were looking for an additional source of income, especially due to the numerous retrenchments taking place during the pandemic and the intensified duties that women were forced to take on in the home, including taking on responsibility for the schooling of their children.

In my case, my mother wasn’t trying to help me with my calculus, yet she still couldn’t wait to get rid of me so she could use the WiFi again.

The goal of the division was to develop a community of 1,000 women over the subsequent three years, providing a “beautiful experience” for clients. Sadly, the experience was not beautiful for shareholders, as the pandemic was the (ugly) nail in the coffin for the business.

Along came a banker

In October 2020, it was announced that the group had procured a R6 million loan from ABSA to help ride out the Covid-19 losses. When a company burns through equity and needs to replace that capital with debt, there is often a permanent loss to shareholders.

This loan came with the condition that the subsidiary that receives the loan must operate in the private market in order to save costs. In other words, the JSE would be bidding farewell to this business. With Long4Life also gone (the owner of Sorbet), there’s nowhere to get your nails done on the local market.

The beauty business is no doubt enjoying a resurgence in trade at the moment, in line with what we are seeing in other service businesses. Listed shareholders won’t get to enjoy that, as the subsidiaries of Imbalie have now been sold to the privately-held i-BLOOM Group. This deal was effective on 31 January 2022.

Vuka, Buka

Vuka is the Zulu word for “wake up” and that’s hopefully what this listed shell will be doing. After the acquisition of a 61.26% stake in the listed company by new investor B&B Media (also with an effective date 31 January 2022), Imbalie Beauty changed its name (again!) to Buka Investments.

Little is known about B&B Media, a company primarily engaged in advertising in addition to holding “various fashion and retail assets” based on media reports. Some of those assets will be reversed into Imbalie Beauty as a “listed shell” which is a cheaper way to achieve a listing for your assets.

It didn’t cost B&B terribly much to take control of the listed vehicle. The price was 0.09 cents per share, so the total investment was R7.6 million. This triggered a mandatory offer to other shareholders, which was only accepted by holders of 1.5% of shares in issue. This took the stake to 62.76%.

Those who rode Imbalie all the way to the bottom are clearly hoping that the new strategy will pay off. Once you’ve lost practically everything, just holding onto the shares gives decent “option value” as there’s only upside from there. Either that, or shareholders were too busy getting their nails done to notice the offer.

We won’t know for sure whether operating in the private environment helps i-BLOOM achieve financial sustainability. The most we can do is judge this based on the growth (or lack thereof) of the underlying franchises.

As for Buka, we can only look forward to learning more about the fashion and retail assets that will be coming to market. Many shareholders are hoping for a more beautiful experience than before.

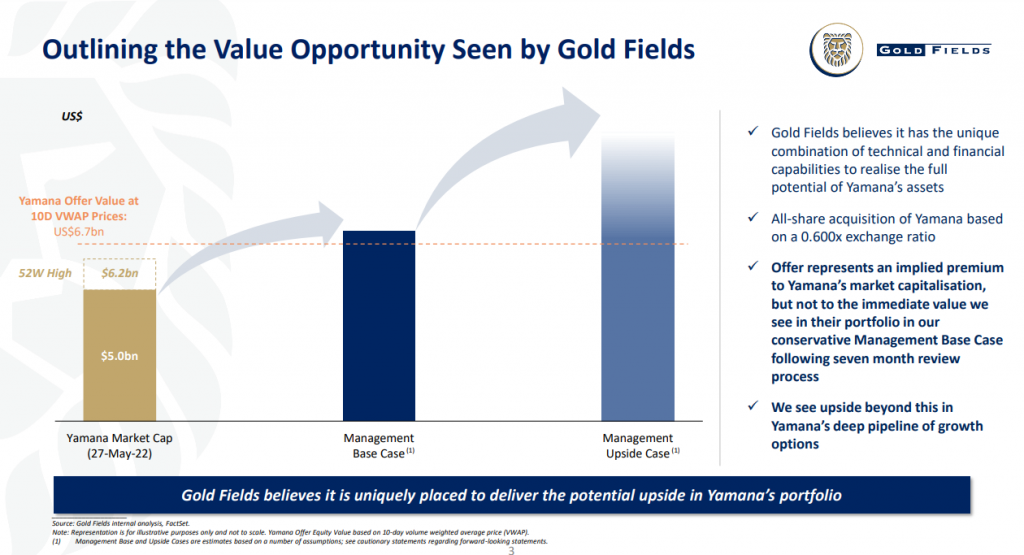

Gold Fields really upset the market at the end of May when the company announced the major acquisition of Yamana Gold, an offshore business trading at a much higher multiple than Gold Fields. To help cheer shareholders up, the company has announced an update on its dividend and listing strategies, as well as rationale of the deal. The first bit of good news is that the revised dividend policy is to pay 30% to 45% of normalised earnings each year, with the 2023 payout ratio expected to be at the top end i.e. 45%. Another important update is that Gold Fields will list on the Toronto Stock Exchange as part of this deal, which will hopefully attract international investors. In terms of Yamana itself, Gold Fields sees this as a strategic fit that will bring high-quality, long-life assets into the group in attractive jurisdictions. There are still major shareholder approvals required (two-thirds of Yamana Gold shareholders and at least 75% of Gold Fields shareholders), so the deal is by no means a certainty. To help get it across the line, Gold Fields has released a detailed presentation that you can find at this link. As a Gold Fields shareholder, I’m hoping this chart from the update comes to fruition:

Capital & Regional Plc has completed the £21.65 million sale of the Walthamstow residential development to Long Harbour. This project is found at a community shopping centre in London. The proceeds will be used to reduce debt. This is a classic “precinct” strategy, with the residential development expected to drive stronger performance at the retail centre. The share price showed its appreciation with a 7.6% rally.

Super Group has raised R500 million in a debt issuance under its Domestic Medium-Term Note Programme on the JSE. It could’ve raised far more if it wanted to, as bids of over R1.7 billion were received for the tranches.

FirstRand is in the process of proposing a scheme of arrangement with a standby general offer to holders of the B preference shares in the bank. If you are the proud owner of such a preference share, I suggest you refer to this circular for more information.

Sebata Holdings is now trading under cautionary after noting that the company is in negotiations for a potential disposal of one or more businesses.

Earnings updates

None – come back tomorrow!

Share buybacks and dividends

As there were no other buybacks or dividends, I may as well remind you that British American Tobacco and Glencore are buying back shares on a daily basis.

Notable shuffling of (expensive) chairs

The expensive chairs stayed where they were today.

Director dealings

The ex-Naspers financial director (who still sits on the board) exercised share options and disposed of shares to the value of over R149 million. To put that number in perspective, if he invests it in fixed income instruments at just 7% per year, the interest would be R200k per week in round numbers. Aah well, back to work the rest of us go.

Capitalworks is a long-standing partner of listed food business RFG Holdings. After the private equity investment house bought R195k worth of shares at the end of June, it has topped up the position with a further purchase of nearly R154k. This is announced on the market because two of the RFG Holdings directors are from Capitalworks.

There’s yet another purchase of shares in Kaap Agri by one of the directors, this time to the value of nearly R72k.

The financial director of Dipula Income Fund has bought nearly R54k worth of Dipula B ordinary shares.

The management team of The Foschini Group has been granted chunky forfeitable share awards, which is a common long-term incentive mechanism. Buried deep in the announcement is a note that the company secretary sold a batch of shares previously granted, putting over R233k in the bank in the process.

Unusual things

Renergen is still using SENS to provide an unofficial online course to anyone who wishes they had studied engineering. The latest update is the introduction of “gas to plant” at the Virginia Gas Project, which sets the scene for final commissioning workstreams over the coming weeks. Commercial operation is anticipated once customer sites are ready to begin accepting product, which Renergen expects towards the end of July 2022.

If you would prefer to study geology online rather than engineering, Orion Minerals is an ongoing source of technical updates about the Prieska project. I usually skip to the quote from the CEO, which is the only bit I really understand. In this case, he continues to sound very happy. Orion is working on an early production strategy at Prieska and latest drilling results seem to be supportive of this.

Old Mutual’s shareholding in Quilter has now moved below the 5% mark, a symbolic step in the Old Mutual story after Quilter was separated from Old Mutual in 2018, rebranded and listed as a UK wealth investment business.

Pembury Lifestyle Group has renewed its cautionary announcement as the company is still trying to pull enough money together to just settle the bills from its auditors. Once that is sorted out, audits need to be done for the 2019 – 2021 financial years. A property in Northriding that was originally built as a school has now been converted to a commercial building, which should provide the cash flows needed to pay the auditors. The designated advisor and company secretary have also resigned, so things are just going SO well there.

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept All”, you consent to the use of ALL the cookies. However, you may visit "Cookie Settings" to provide a controlled consent.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. These cookies ensure basic functionalities and security features of the website, anonymously.

Cookie

Duration

Description

cookielawinfo-checkbox-analytics

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics".

cookielawinfo-checkbox-functional

11 months

The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional".

cookielawinfo-checkbox-necessary

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary".

cookielawinfo-checkbox-others

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other.

cookielawinfo-checkbox-performance

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance".

viewed_cookie_policy

11 months

The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Advertisement cookies are used to provide visitors with relevant ads and marketing campaigns. These cookies track visitors across websites and collect information to provide customized ads.

")

")