HEPS at Gold Fields has more than doubled (JSE: GFI)

The consolidation of Gruyere in Q4 has further boosted the numbers

Gold Fields released a trading statement dealing with the 12 months to December 2025. They’ve indicated HEPS growth of between 110% and 123%, while normalised earnings per share will be between 112% and 126% higher. Whichever way you cut it, that’s a delightful outcome that we’ve become accustomed to seeing in the gold sector.

The obvious driver of this boost to earnings is the higher gold prices. The company also enjoyed increased sales volumes of gold, as well as the positive impact of the full consolidation of Gruyere (the stake was increased from 50% to 100% at the beginning of Q4). To add to the happiness, Salares Norte reached steady-state production in Q4, with a 43% increase in production vs. Q3.

It wasn’t all good news, though. Mining inflation is impacting the all-in sustaining cost (AISC), coming in at $1,673/oz in Q4 vs. $1,557/oz in Q3. That’s obviously much lower than current gold prices, but the mining houses will still need to keep an eye on costs.

For the full year, attributable gold equivalent production was 18% higher year-on-year and at the upper end of the guided range. All-in sustaining cost (AISC) was 1% higher at $1,645/oz, within the guided range. This shows how variable the quarterly numbers can be vs. taking a full-year view.

Discovery buys Phase 1 of their head office from Growthpoint and others (JSE: DSY | JSE: GRT)

And Growthpoint is buying 45% in Discovery Phase 2

Here’s an interesting one for you to ponder: when two large, financially sophisticated companies do a transaction, which one is getting the better deal? And can they both win at the same time?

Let’s start from the perspective of Growthpoint, the iconic South African REIT that owns too much office property in Sandton (especially of the lower grade variety). They’ve made it clear several times that they are looking to simplify and focus their portfolio. The Western Cape has certainly come up as a desired area, but perhaps most of all they need to reduce their exposure to Sandton office space, something that was a fantastic asset a decade ago and isn’t so great anymore.

Now let’s do Discovery, who occupy a beautiful head office building in Sandton that immediately irritates anyone who had a medical aid claim denied. They have 7 years left on that lease and it would be a disaster to try move the entire company again, so it makes sense to just lock in the space and occupy it forever.

We are talking about R4.05 billion changing hands here for the Grove and Park buildings (Phase 1), so shareholders of both companies will want to understand the dynamics here.

Discovery talks about how interest rates and property prices in Johannesburg have reduced significantly, so they can switch from a lease to property ownership at a lower overall cost. In fact, they believe they will save a net present value of R800 million over the remaining lease period!

What about Growthpoint? They talk about capital allocation discipline and portfolio balance, along with a reduction in concentration risk as Discovery is a single tenant. Unfortunately, this means that the vacancy rate for the office segment at Growthpoint will go up, as they are selling a fully tenanted building and being left with other buildings that aren’t in such a favourable situation.

It feels to me like Discovery is coming out on top in this transaction, although I can understand the rationale from Growthpoint’s perspective as well. Truzen, the other shareholder in the property, is also willing to sell under these terms. It therefore can’t be too bad a deal.

Growthpoint owns 55% of Phase 1 (Truzen owns the other 45%), so they will receive R2.3 billion of the deal consideration. Their share was valued at R2.2 billion as at 30 June 2025, so this is a disposal at a premium to book value.

Remember, two things can be true here: (1) Growthpoint can be selling at a premium to book value, and (2) Discovery might be getting it right in terms of believing that Sandton property is a decent investment right now.

Now we reach the second part of this transaction: Phase 2 of the building. Discovery will cancel the lease for that building as part of this deal, as they have optimised their space requirements over time. Growthpoint clearly sees an opportunity here, as they are acquiring the other 45% in Phase 2 from Truzen. This investment of R323 million will give Growthpoint 100% ownership of Phase 2.

The trick here is that Phase 2 is a multi-tenanted P-grade office building, so Growthpoint can retain a presence in the area going forwards and spread the tenant risk.

The net proceeds for Growthpoint (the sale of Phase 1 less the investment in Phase 2) come to just under R2 billion.

It will take a while to be finalised, as this is classified as a Large Merger for Competition Commission purposes.

If nothing else, this is an interesting example of the art of the deal – finding what works for each party and structuring an outcome where both feel like winners.

Nibbles:

Director dealings:

An associate of Pepkor (JSE: PPH) CEO Pieter Erasmus sold shares worth R531 million.

There’s been an unexpected change of top management at Copper 360 (JSE: CPR). Graham Briggs, the ex-CEO of Harmony Gold who came out of retirement to help the company when it was in dire straits, has now taken a “leave of absence” – and so has Commercial Executive Stephan Du Plessis. They are being replaced on a transitional basis. Current COO Gordon Thompson comes in Transitional CEO, while Seten Naidoo moves from Chief Risk Officer to Transitional Commercial Executive. This announcement came out after market close on Friday, so get ready for some fireworks in the share price when it opens on Monday.

Eastern Platinum (JSE: EPS) has secured another credit facility with Ka An Development Co. Limited for up to C$1 million. This is in addition to the previously announced facility, taking the total to C$2 million. The debt is priced at 10.25% per annum, in line with the local prime interest rate. The company is focused on ramping up the Zandfontein underground mine to target 70,000 tonnes of run-of-mine ore per month by the end of 2026.

With the Bytes Technology Group (JSE: BYI) share price suffering tremendously in the greater tech sell-off that we are seeing (down 20% year-to-date), Coronation’s funds have reduced their stake slightly in the company. This is the exact opposite of buying the dip.

If you’ve ever watched an Olympic podium ceremony and thought, “Wow, must be nice,” you’re not alone. But the truth is far less glamorous than the gold glinting under those stadium lights. Behind every medal is a paper trail of budgets, grants, sponsorships and support staff invoices. Somewhere in a government office, there’s a spreadsheet that makes the Minister of Sport choke on a coffee.

At the end of 2024, Minister of Sports, Arts and Culture Gayton McKenzie revealed that South Africa spent just under R30 million sending Team SA to the 2024 Paris Olympics. That price tag covered 146 athletes, plus the technical and logistical battalion needed to get them from Polokwane, Pietermaritzburg, and Plumstead to Paris (and hopefully onto the podium). The return on investment was six medals, and only one of them gold.

New Zealand, for the sake of comparison, took home 20 medals, of which 10 were gold. They sent more athletes than us, sure, but not that many more – 195 vs. our 146.

In response, McKenzie has launched Project 300, a plan to double our Olympic team size by 2028. Lotto, SuperSport, and a few other unnamed corporate players have already been tapped for funding. The talent search to drum up these team members will happen in every corner of the country, including rural villages where the nearest training “facility” is comprised of a dusty soccer pitch and a dream.

It’s an expensive gamble. And it raises a question that South Africa has been trying to answer for years: what does it really cost to build an Olympian?

The price of potential

You might think that world-class athleticism is something you’re either born with or you’re not – some combination of genetics, grit, and a coach shouting “HARDER!” from the sidelines. But the truth is more complicated (and more costly).

At the elite level, talent alone gets you almost nowhere. Funding is the invisible scaffolding holding up every podium success. Without money, athletes scrape by in the gaps between training shifts, part-time work, and whatever side hustle pays for petrol to get to physio. With money, athletes enjoy what wealthier nations consider non-negotiable: nutritionists, psychologists, physiologists, specialist coaches, sports scientists, recovery tech, and international competition exposure.

Think of athlete development like a Jenga tower. Every missing block, from diet and rest to coaching and equipment, makes the structure wobblier. Wealthy nations start with a perfectly aligned tower. Smaller economies start halfway through the game, and someone’s already taken out all the centre blocks.

And then there’s the brutal catch-22: to get funding, you must perform. But to perform, you need funding. It’s a system that rewards the already-successful and punishes the promising-but-poor. Many South African athletes know this tension intimately. When your stipend depends on your last race time, every training session carries the weight of your livelihood.

The Olympic arms race

The world’s biggest sporting nations spend big in their pursuit of Olympic glory. The US Olympic and Paralympic Committee threw $327 million at athlete development in 2022. The UK spent the equivalent of over R7 billion ahead of Tokyo 2020. These programmes include everything from training technology to psychological support and even marketing.

Then there’s the second category of spending: the rewards. Once the medals are won, the prize money kicks in, and this is where things get eyebrow-raising. Hong Kong pays an athleteR14.7 million for a gold medal. They don’t do badly over in Serbia either, with a cool R4.1 million. Some countries even hand out property portfolios! Poland’s gold medallists at Paris 2024 enjoyed diamonds, holidays, artwork, and actual apartments in Warsaw.

Research finds a strong correlation between elite sport funding and international success. Countries investing heavily in facilities, coaching, and athlete support tend to feature more often on podiums. That’s why wealthier countries with well-financed sports programmes still dominate the medal tables.

But that relationship, while statistically significant, also reveals exceptions. Some lower-income nations continue to achieve rare but remarkable success, often punching above their “expected” weight. This suggests that performance depends on more than just bankroll: sometimes, environmental, cultural, physiological and personal factors tip the balance.

Take long-distance running, for instance. Most elite athletes in these events come from high-altitude or rural areas, where daily life involves long endurance tasks like running to school, walking for kilometres to get to a shop, and growing up in an oxygen-poor environment. For many, those conditions deliver a built-in advantage that no high-tech gym can simulate.

Who pays, and who profits?

That said, structural support cannot be ignored. Studies of elite-sport funding models show countries achieve more consistent results when they prioritise sustained investment over hit-and-miss cycles. Well-funded national programmes generally deliver better coaching, injury prevention, recovery protocols, sports science support, and logistical backing, which is especially important in high-performance sports and for athletes outside globally dominant disciplines.

The absence or weakness of those systems in poorer countries often means talent goes unrefined, potential remains unrealised, and consistency fades. For athletes who lack stable funding, sacrifices may build discipline, but they seldom build a career.

So who pays to build a champion? And who benefits when the medals come home?

The answers are messy. In wealthy countries, government-backed systems invest heavily in athlete development because sporting success is good national PR. Gold medals translate into international prestige, influence, and a type of soft power. In nations with fewer resources, the funding question becomes a tug-of-war between government budgets, private sponsors, athletes’ personal finances, and pure willpower. South Africa finds itself in the awkward middle. We’re not broke – but we’re also not the UK.

R30 million feels like a lot until you compare it to the countries we’re trying to compete with. And while sport is a powerful unifier in South Africa (ask anyone who had a Springbok flag painted on their face in 2023), we are also a nation with some urgent fires to put out – sometimes quite literally.

On one hand, Project 300 is a credible idea: a nationwide search for hidden talent, especially in under-resourced communities, could unearth athletes with raw potential. South Africa has a history of producing remarkable underdog performances, and a project like this could expand the pool significantly. But on the other hand, without sustained investment in infrastructure, coaching, sports medicine, recovery programmes, nutrition, and long-term athlete support, Project 300 risks becoming a nationwide talent audition with no runway. We might spot raw diamonds, only to have them fade because the polishing tools aren’t there.

If the plan merely identifies potential athletes but doesn’t build a support structure comparable to those used by leading sporting nations, then we may end up expecting world-class performances “on the cheap”. And that seldom works.

One thing is for sure: the Olympic Dream continues to capture the imagination.

About the author: Dominique Olivier

Dominique Olivier is the founder of human.writer, where she uses her love of storytelling and ideation to help brands solve problems.

She is a weekly columnist in Ghost Mail and collaborates with The Finance Ghost on Ghost Mail Weekender, a Sunday publication designed to help you be more interesting.She now also writes a regular column for Daily Maverick.

Diamonds continue collapsing at Anglo American, with all eyes on near-term copper (JSE: AGL)

But copper production in 2025 was at the lower end of guidance

Anglo American has carved its group into two segments called “simplified portfolio” (the stuff they are keeping) and “exiting businesses” (the stuff they are selling).

That makes it sound like the businesses they don’t want are now someone else’s problem, but that’s not the case. At this stage, there are no concrete deals on the table for diamonds or steelmaking coal, with only a sales process running in the background. At least they have a buyer for nickel, with that deal currently going through approval processes.

Average diamond prices were down 7% year-on-year for full year 2025 and 17% for the fourth quarter. This is despite a 35% drop in fourth quarter production, so even a sharp drop in supply hasn’t sent prices the right way. Full year production was down 12%. At this rate, they might have to pay someone to drag De Beers away! Jokes aside, they’ve flagged that an impairment is likely in the full year numbers based on negative EBITDA in 2025. The lab-grown diamond disruption went beyond even my expectations when I first started writing about it.

In steelmaking coal, production fell by 15% in the fourth quarter and 43% for the full year. Thankfully, this drop is largely (but not exclusively) due to disposals of assets that were in the base period and not in this period.

Anglo would like to sweep these businesses under the carpet and move on. As you can see, it’s not quite that easy.

Let’s move on to the stuff they actually want to own.

We know that copper is the big focus, yet production actually fell 14% in the fourth quarter and 10% for the full year. They produced 695 kt in 2025, right near the bottom of the guided range of 690 – 750 kt. Great numbers at Los Bronces were offset by lower grades at Quellaveco and Collahuasi. Unfortunately, copper guidance for 2026 and 2027 has been revised lower. The 2026 revision is no joke – the lower end of the guided range has been dropped by 8%.

In premium iron ore, you can read further down about how well Kumba Iron Ore (JSE: KIO) performed within the Anglo stable. The other asset is Minas-Rio in Brazil, where production dipped by 1% for the full year. Guidance for 2026 is much more encouraging for that asset, revised higher thanks to recent operational performance.

The third and final business they plan to keep is manganese ore. Production jumped by 22% for the quarter and 30% for the year, with production now at normalised levels after a tropical cyclone hit Australia in March 2024.

Despite highlights appearing to be thin on the ground in this update, Anglo’s share price is up 34% in the past year thanks to exuberance around copper.

Losses down and debt up at ArcelorMittal (JSE: ACL)

Is a government bailout the only hope for this company?

ArcelorMittal released results for the year ended December 2025. It’s hard to imagine how much longer this can go on for, as the company has generated R8.4 billion in headline losses over the past two years. They are sitting with net borrowings of R6.5 billion, so we are firmly in “too big to fail” territory here.

Or are we? Will this thing be allowed to collapse? And is the South African government, via the IDC, the only potential saviour?

It’s hard to find positives here unfortunately. Even though the headline loss of R3.4 billion was much better than in 2024, it’s still a huge number. The net borrowings number is R1.3 billion higher than the year before. And perhaps most shockingly, this is despite the “Longs” business being EBITDA neutral in 2025! The group EBITDA loss in 2025 was R1.1 billion instead of almost R3 billion in the prior year.

Now get ready for the worst news of all: the stronger rand makes everything worse for ArcelorMittal. It makes imports cheaper and exports less attractive. This is a company that couldn’t keep it together when the rand was weak, so what do you think happens in 2026 with a stronger rand?

The company has flagged a commitment by the DTIC to address fair trade protections in the first quarter of 2021. The cynic in me can’t help but wonder whether government will give the business a helping hand before or after doing a deal to acquire these assets.

The share price of R1.27 is up 12.5% over 12 months. This is despite a headline loss per share of R3.01. There is only one reason why this is possible: the market is hoping with everything it has that government will swoop in with a deal.

I’ll keep my money far away from that “investment” thesis, thank you very much.

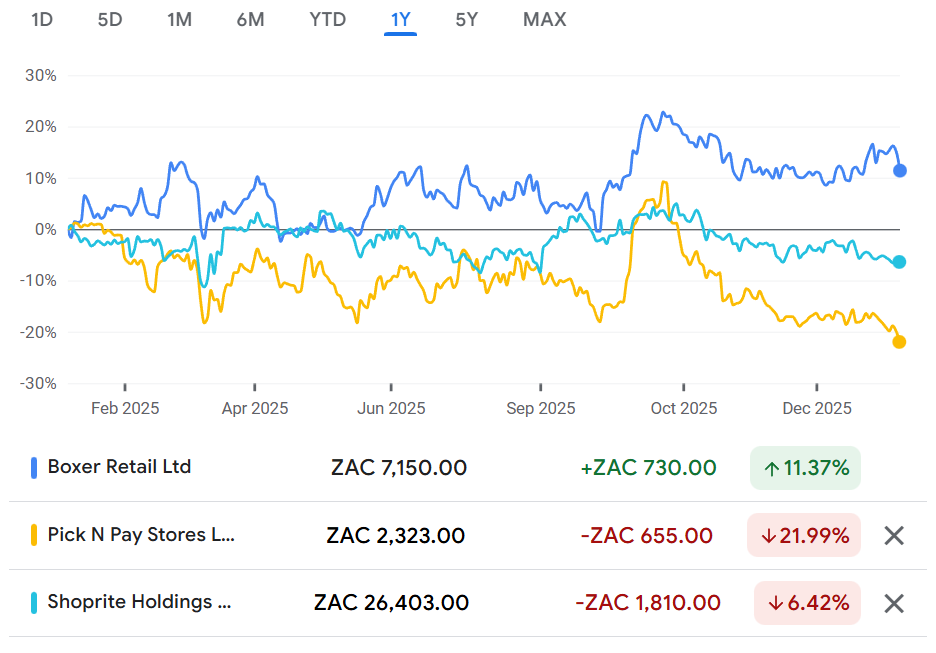

Boxer is certainly a worthy adversary for Shoprite (JSE: BOX)

The periodsaren’t directly comparable, but Boxer is looking good

Boxer is by far the best part of the Pick n Pay (JSE: PIK) stable. The grocery chain competes very well for lower-income customers, giving Shoprite (JSE: SHP) something to really think about in the Shoprite and Usave chains. The winners are of course the consumers who get to enjoy a period of price deflation as these grocery stores fight over the most price sensitive customers in the country.

If you look over the past year, Shoprite is a victim of its valuation and a slowdown in growth. Pick n Pay is a victim of… well, a whole lot of things. And Boxer is the one you wanted to own, up 11.4%:

It gets tricky to compare the performance, as Boxer has a different reporting period to Shoprite. Due to factors like two-pot withdrawals at the end of 2024 and the timing of inflationary changes, it’s dangerous to compare the performance of companies over different periods and draw any conclusions.

Starting with just Boxer’s numbers, turnover for the 48 weeks to 1 February 2026 was up 11.9%, with like-for-like growth of 3.9%. For the 22 weeks to 1 February 2026, turnover growth slowed to 9.8% and 2.4% on a like-for-like basis. Interestingly, November was the month that they highlight as being the biggest struggle! Clearly, Black Friday at Boxer isn’t a thing.

For the 48-week period, there was deflation of -1%. For the 26 weeks to 31 August 2025, deflation was -0.7%. The closest comparable period we have at Shoprite is the six months to December 2025, in which deflation at Usave (the closest in spirit to Boxer) was -0.7%.

As you can see in the gap between total growth and like-for-like growth, Boxer is aggressively rolling out stores. They are on track to hit their targets for the 52 weeks to 1 March 2025 (the full financial year). They also believe that they will meet the trading profit growth targets based on an expectation of strong year-on-year numbers in February.

It’s a great business, that’s for sure.

Glencore doesn’t want to be swallowed up by Rio Tinto (JSE: GLN)

Mining mega-mergers remain rare things

The year kicked off with news of Glencore and Rio Tinto circling each other on the dancefloor. As is so often the case in huge mergers like these, one party decided to go home early and leave the other one hanging.

In this case, it was Glencore who decided that they weren’t comfortable with the value being put forward by Rio Tinto. At least Glencore was honest about one of the other issues: Rio Tinto insisting on retaining the Chairman and CEO roles. The mining industry does have a reputation for having bigger-than-average egos in the boardroom!

The official record will show that Glencore feels that the copper assets were being undervalued in the negotiations. I would’ve loved to be a fly on the wall for some of these deal discussions.

Glencore fell over 5% on the day, but the market hasn’t had an opportunity to digest this news yet.

Double-digit dividend growth at Hudaco (JSE: HDC)

The engineeringconsumablessegment is doing all the heavy lifting

Hudaco has released results for the year ended November 2025. Turnover increased 4%, operating profit was up 9%, HEPS grew 16% and the dividend was up 10%. That sounds like a perfect story of leverage, with top-line growth translating into a much better outcome for shareholders by the time you reach the bottom of the income statement.

The segmental story is somewhat less steady.

Consumer-related products suffered a turnover decline of 2%, although they did well to increase operating profit by 0.6% despite this dip. The battery and alternative energy business is almost a lost cause, with Hudaco impairing the goodwill in that business in full. Other businesses like automotive, CADAC and data networking did well.

Engineering consumables brought the growth, with turnover up 10.1% and operating profit increasing by 11.2%. But what is the source of that growth? Acquisitions contributed R58 million in operating profit, so it looks as though the existing businesses only added R12 million in incremental operating profit (total operating profit was R696 million, up by roughly R70 million).

By now, the main thing you should be wondering is whether the stronger rand is a risk. Sure enough, the prospects section does note that it will put selling prices under pressure. They hope that some consumer relief will accompany this.

I wonder if anyone at the SARB reads these things when making interest rate decisions? Because until rates start coming down, I fear that the consumer relief isn’t going to happen.

KAL Group has a new CEO (JSE: KAL)

The group enters this new chapter in excellent shape

At KAL Group’s AGM, they announced that Sean Walsh will be retiring as CEO with effect from 28 February 2026. That’s a rather sudden change, not least of all after a 15-year term! Walsh will be available to the board on a consulting basis in the coming months.

This paves the way for Johann le Roux to take the reins. If that name sounds familiar, it’s because le Roux has just stepped down at Zeder (JSE: ZED) in the wake of the Zaad disposal being announced. I’m sure he’s excited to move into a growth business rather than a value unlock story.

And growth is the word: at the AGM, the company reiterated its 2030 goal of 15% compound annual growth in profit before tax at Agrimark and PEG. They are also targeting a 15% return on equity with a 40% gearing ratio.

These are lofty targets, representing an acceleration from the profit before tax growth of 12.8% in 2025. With considerable exposure to fuel retail and the whims of the fuel price, it’s important to remember that not everything is within their control.

The AGM update included news on trading during the first quarter of 2026. Recurring HEPS increased 13.4% and debt dropped by R385 million year-on-year, with a gearing ratio of 34.3%.

The share price is only up 4.7% in the past year, but that doesn’t tell the full story. It went as low as R36.69 before recovering to the current level of R49.00 (pretty close to the 52-week high of R53.49).

Kumba Iron Ore had a pretty good year in 2025 (JSE: KIO)

Earnings are up and there’s a more positive narrative around Transnet

Kumba Iron Ore released an update for the fourth quarter of 2025, which means we have full year numbers as well. This was accompanied by a trading statement indicating growth in HEPS of between 11% and 23% – a strong outcome. The share price is only up 6% over 12 months though, so the market is taking a cautious approach on this one.

Production in the fourth quarter was up 10% year-on-year. For the full year, they were up 1%. Kolomela was up 7% for the year and Sishen (which is 2.5x larger) was down 1% due to planned maintenance.

Kumba is responsible for getting the stuff out of the ground, but Transnet then needs to rail it to Saldanha. This is historically where things have gone wrong. Despite two derailments, there was a 2% increase in ore railed to the port in Q4!

Once it gets to the port, it then needs to be put on a ship. With high wind speeds and other issues, this is where things went south in Q4. Sales were down 5% year-on-year for the quarter, and up 2% for the full year.

As you can see, it’s not easy running this business. Nonetheless, it was a successful year, with earnings up thanks to better export ore prices, the 2% increase in sales volumes and penalty income from Transnet.

Production guidance for 2026 is unchanged at 31 to 33 Mt, while 2027 and 2028 sit at 35 to 37 Mt.

Lesaka Technologies finally delivers positive net income (JSE: LSK)

They’ve met profitability guidance and reaffirmed full-year guidance

Lesaka Technologies has released results for the second quarter of the year. Before we dig in, I want to remind you that I recorded a podcast in November last year with Executive Chairman Ali Mazanderani. It’s still a really great resource to help you understand the company, so check it out here.

In terms of the latest numbers, net revenue (a non-GAAP measure) was up 12.2% in dollars and 16% in rand. If you work with revenue as reported, it was up 1.4% in dollars and down 3% in rand.

That won’t really blow anyone’s hair back in terms of growth, but we haven’t gotten to the numbers that really count yet.

Operating income jumped by a lovely 265% in rand as the company started to climb the J-curve (or the S-curve, depending on your long-term view here). Curve shapes aside, profits are now starting to climb as the company has reached that inflection point that all successful technology companies must move through.

Most encouragingly, there was positive net income this quarter, a massive positive swing from where they were a year ago. This is a big deal for the company, as this is the first positive net income since Lesaka was put together in 2022. It’s also worth noting that this is the 14th consecutive quarter of meeting guidance.

Based on these numbers, further revenue growth will likely have a great impact on the bottom line. We can therefore move on to look at Lesaka’s three segments.

The largest is Merchant, where net revenue dipped 2% and adjusted EBITDA was down 6%. This is why the group revenue picture isn’t as inspiring as one might hope in this quarter.

The Consumer segment is much smaller on the net revenue line, but almost as big on the adjusted EBITDA line as Merchant. This is especially true after adjusted EBITDA more than doubled (up 106%) based on revenue growth of 38%.

The Enterprise segment is scaling rapidly, with revenue up 58% and adjusted EBITDA swinging from a loss to a solid positive of R24.3 million. For context, that’s still much smaller than Consumer’s EBITDA of R159 million, or Merchant at R170 million.

The guidance for the year ending June 2026 reflects expected growth in adjusted earnings per share of more than 100%. Most importantly, they expect positive net income. This excludes the acquisition of Bank Zero, a critical additional step in this journey.

The Lesaka share price hasn’t really captured the imagination of the market. Will a swing into profitability change that?

MTN is potentially acquiring the remaining 75% in IHS (JSE: MTN)

This seems like a slightly odd allocation of capital

As I wrote about in the Vodacom (JSE: VOD) update earlier this week, the macroeconomic situation in Africa is giving telcos like MTN a golden opportunity to cement their positions on the continent and generate proper cash flows.

It therefore makes sense for the companies to be allocating more capital to Africa. But I’m not so sure that it makes sense for this to take the form of owning the towers that are leased to the telco companies. The trend in the sector has been to separate the towers from the telco operators, as one is essentially a property company and the other is a technology company.

Despite this, MTN has confirmed rumours that they are at an advanced stage of discussions with IHS to acquire the remaining 75% in the company that it doesn’t already own. They are looking at an offer price close to the recently traded price of IHS on the New York Stock Exchange.

The MTN share price closed 5.8% lower on the day. I can’t say that I’m surprised.

Prosus is focused on execution, not M&A (JSE: PRX | JSE: NPN)

The real test of new management has arrived

Whenever there’s an exciting new thing out there (like AI), there’s always a flurry of capital that flows into it. When every dart is thrown at the dartboard, some of them are bound to land in weak positions – and others will fall off altogether. You can only see the outcome once the chaos of the initial throws has subsided.

Prosus is now 32% off its 52-week high. This gets me excited as a long-term investor. At nearly 38 years old, I still have plenty of time for the market to pay me for duration. In other words, riding out volatility in core positions is something I have no difficulties in doing.

Why the drop? Well, unless you haven’t been paying any attention at all to the big tech names globally, there’s been a shaking of the tree in anything related to AI and software. The market is treating almost everything with suspicion. This creates an opportunity for investors to identify the good stuff that gets sold off with the bad.

A letter to shareholders from CEO Fabricio Bloisi is no doubt an effort to remind investors of the long-term story. But he’s also given an important update about the near-term strategy: “I don’t have plans for any major M&A while we focus on this” – and by “this” he means execution on what they already own.

In fact, instead of doing major acquisitions, they will be selling more than $2 billion in assets in this fiscal year and even more the following year. Share repurchases remain a core focus, something that you absolutely want to see when a share price has come off the boil. It’s worth noting that they fund a large part of the buybacks through selling shares in Tencent, where the share price is also under pressure. It would be ideal if the buybacks were funded fully by cash profits in the group.

Speaking of profits, Prosus indicates that they are still on track to do over $7.3 billion in revenue and over $1.1 billion in adjusted EBITDA in FY26. For context, in FY25 they achieved $6.2 billion in revenue and $655 million in adjusted EBITDA.

This is only possible if the major acquisitions are performing well. In Brazil for example, Despegar is up more than 30% year-on-year in local currency and 50% in dollars, with strong sales synergies delivered with other Prosus businesses in the region. At Just Eat Takeaway.com in Europe, new management is in place and initial testing is encouraging, but there’s a very long way to go. At La Centrale, they are giving a positive overall view, but again these are early days and there’s a lot of integration to do with OLX.

On the topic of classifieds, OLX is on track for $450 million in EBITDA. They will be hosting an investor event soon that will be focused on the classifieds opportunity.

iFood, which is Bloisi’s area of deepest expertise, is facing strong competition in Brazil from new entrants who are burning through VC money with unsustainable pricing structures. I remember the exact same thing happened with Bolt Food in South Africa. Today, Bolt is gone and Uber Food is still here. I therefore understand when Prosus talks about how customers return to the best product and service once the subsidies are over, but that doesn’t mean that there won’t be short-term pain.

I remain long here. And if it keeps dropping, I’ll buy more.

A nasty knock to earnings at Sasol (JSE: SOL)

Better fuel volumes can’t offset the weak prices

Everyone’s favourite wild child is back with another day of volatility. Sasol closed 3.8% lower on Thursday, which means that it is flat over 90 days despite swinging wildly between R99 and R127 per share over that period.

The previous update on manufacturing performance was positive, indicating progress made in the South African fuel business. But that’s only half the battle won for any industrial company, with the other half being the selling price of the products. With a 17% decline in the average price of Brent Crude (on a rand per barrel basis) for the six months to December, Sasol’s earnings didn’t stand much chance.

To rub salt in the wound, the average chemicals basket price in dollars fell 3% over the period as well.

Despite the mitigating factors like much better refining margins, a 3% increase in sales volumes and a drop in costs, Sasol still suffered a decline in HEPS of between 29% and 40%. Adjusted EBITDA fell by between 4% and 21%.

I’ve been wondering how it is possible that the Sasol share price is up 35% over the past year despite a stubbornly flat Brent Crude price and a strengthening rand. Now that we know where HEPS has gone, I’m asking myself that question even more.

Results will be released on 23rd February.

Super Group is acquiring 70% in DIG Group (JSE: SPG)

The deal is valued at R447 million

After releasing an interesting update that laid bare the challenges in the UK automotive segment, Super Group announced that they are acquiring 70% in the DIG group of companies. They have the option to acquire the remaining 30% after the 5th anniversary of the effective date, so there’s a pathway to effective control here.

This business will fit into the fleet solutions offering at Super Group, with DIG’s niche being in sectors (like mining and civil engineering) that have strict safety compliance requirements and complicated induction and onboarding protocols. DIG is currently active across 19 mining sites, with exposure to clients in various commodities like coal, chrome and gold.

The fair value has been set at R576 million, with profit after tax for the year ended February 2025 of R191.5 million. I can’t help but wonder why the seller is happy to accept a Price/Earnings multiple of just 3x for this asset!

The purchase price is R448 million settled up-front in cash, with up to R160 million as a deferred profit warranty payment. The put option down the line will be based on the fair value of the business, with a cap in place as well.

The profit warranty is based on a profit after tax of over R200 million per annum in FY26 and FY27. The Price/Earnings multiple applicable to the profit warranty payment is 3.2x.

And no, your mental maths isn’t wrong – the numbers don’t reconcile particularly well in terms of the fair value and the 70% being acquired at this stage.

Despite Super Group trading on a P/E of over 7x, the market reacted negatively to this news of an acquisition at 3x. The share price closed 3.4% lower on the day.

Valterra took advantage of PGM prices in the fourth quarter (JSE: VAL)

They did what they needed to do in terms of production

As I’ve written many times, mining management teams are judged on production performance and capital allocation. This is because they have control over these factors, unlike commodity prices where they are merely passengers on that journey.

In the quarter ended December 2025, Valterra Platinum needed to take advantage of strong PGM prices (the basket price in rand was up 41% year-on-year). Total production increased by 1% and so did refined PGM production on a year-on-year basis. Momentum was good, with refined PGM production up 6% on a quarter-on-quarter basis.

PGM sales volumes were up 4% for the quarter, with some missed sales in Q3 rolling into this quarter.

Still, even if you adjust for the timing distortion of Kroondal, full year PGM sales volumes were down 10% based on refined PGM production falling 13%. Valterra may have had a decent end to the year, but the full year picture isn’t nearly as strong thanks to the flooding at Amandelbult (among other challenges).

Production guidance for 2026 to 2028 is identical across the three years: annual refined PGM production of between 3.0 and 3.4 million ounces. For context, 2025 was 3.4 million ounces. This tells you that earnings growth depends on efficient mining and especially ongoing improvement in PGM prices, rather than an uptick in production.

Nibbles:

Director dealings:

Two directors of Calgro M3 (JSE: CGR) exercised options and received a total value of R1.14 million, settled in cash. They seem to have retained the post-tax shares.

Exxaro (JSE: EXX) successfully refinanced R10 billion in corporate facilities due in April 2026 and added another potential R3 billion of debt on top for good measure. The funding structures range from term loans to recurring credit facilities, with an accordion of R3 billion applicable to all facilities. This is essentially a mechanism that allows for the facilities to be increased without renegotiating all the terms. Financial flexibility is never a bad thing to have.

There have been numerous announcements about Ninety One (JSE: NY1 | JSE: N91) acquiring stakes in South African listed companies of between 5% and 10%. I am sure that this is because the transaction with Sanlam (JSE: SLM) for the South African active investment management business has closed, so the ex-Sanlam stakes now fall under the Ninety One umbrella.

I’m confused once again about these weird stakes that Standard Bank (JSE: SBK) is picking up in other banks. One theory is that they are held by Liberty as part of a broader investment strategy. That seemed plausible, but now Nedbank (JSE: NED) has announced that the communication sent by Standard Bank to Nedbank was actually sent in error, and that they do not in fact own more than 5% of the shares. Very, very odd.

Southern Palladium (JSE: SDL) gave an update on the drill programme for the definitive feasibility study (DFS) at the Bengwenyama Project. The DFS remains on track for completion by the end of August 2026.

Argent Industrial (JSE: ART) announced that Fred Litschka will be retiring as an executive director after an incredible innings of over 22 years. That’s a well-deserved retirement I think!

Water scarcity is no longer a future risk. It is already reshaping how businesses operate, invest and grow in South Africa.

With water demand in Gauteng at record levels and ageing infrastructure under strain, water has become a material constraint on business continuity, supply chains and long-term competitiveness. For many companies, water security is now as critical as energy security.

In this episode of No Ordinary Wednesday, recorded after an Investec and Proparco water-resilience event, Jeremy Maggs is joined by Dr Sean Phillips, Director-General of the Department of Water and Sanitation; Helen Hulett, water-security advisor; and Melanie Humphries, Head of Sustainable Solutions at Investec.

Hosted by seasoned broadcaster, Jeremy Maggs, the No Ordinary Wednesday podcast unpacks the latest economic, business and political news in South Africa, with an all-star cast of investment and wealth managers, economists and financial planners from Investec. Listen in every second Wednesday for an in-depth look at what’s moving markets, shaping the economy, and changing the game for your wallet and your business.

Rainbow Chicken’s earnings have doubled (JSE: RBO)

There may not be a pot of gold at the end of this rainbow, but the chickens ain’t bad either

The poultry industry is a bit like going on a night out with your wildest friend. You’re either going to have an absolutely incredible time, or you’re going to lose your phone and end up sleeping under a tree as the precursor to a morning of serious regret.

In other words, if you’re the type who prefers a quiet night with a book, then chicken is best left for your plate rather than your portfolio.

For the six months to 28 December 2025, Rainbow Chicken achieved growth in HEPS of between 94.9% and 114.9%. As jols go, this is the one you look back fondly on when you turn 35 and realise that you’re probably too old for this now.

The reason for the volatility in earnings is that poultry businesses run at paper-thin margins. A relatively modest improvement further up the income statement has a significant impact on margins by the time you reach the bottom. Likewise, a seemingly minor deterioration in e.g. gross margin can have a nasty impact on profits.

When several things go well, you can see earnings double like this. In this case, Rainbow enjoyed a lovely cocktail of operational efficiencies, strong demand and lower feed costs thanks to improved commodity input prices.

Detailed results are due on 11 March. It’s a pity I’m not a shareholder, otherwise I could treat them as my birthday present that day!

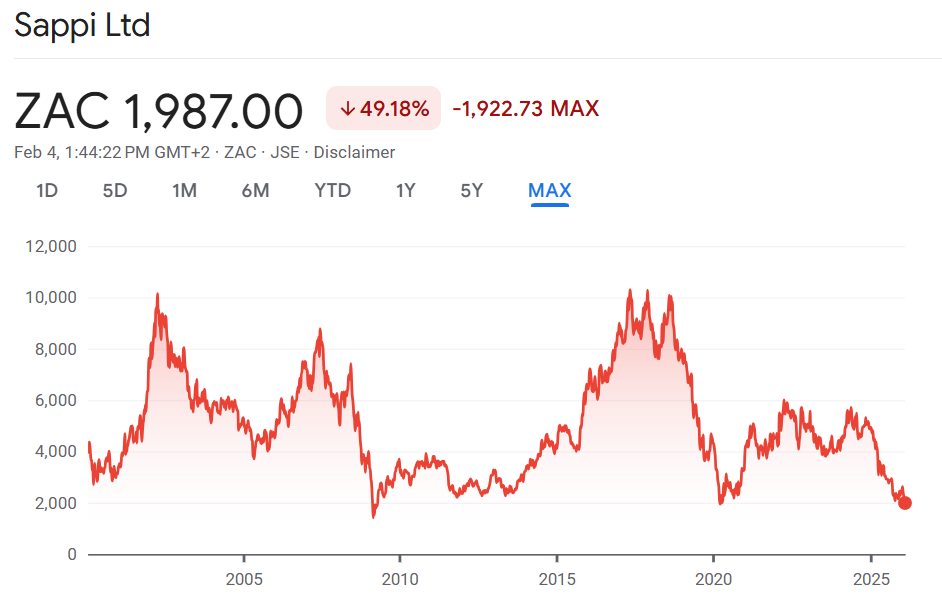

Another loss-making quarter at Sappi (JSE: SAP)

At least Q1’26 was a bit better than Q4’25

Sappi released results for the quarter ended December 2025, the first quarter of the 2026 financial year. Although they reflect a smaller net loss than in the quarter ended September 2025 (a sequential view), adjusted EBITDA is actually lower. And if you apply a year-on-year view rather than sequential, it’s particularly ugly.

This isn’t a surprise to the market, with the share price down 60% over 12 months coming into this release. If anything, the market got a better set of numbers than expected here, based on the share price trading nearly 5% higher by lunchtime and closing 3.6% higher.

The announcement only provides the year-on-year comparison, so a sequential view requires you to dig out the September 2025 results. Revenue fell 6% year-on-year and 7.4% quarter-on-quarter. As for adjusted EBITDA, they were down by a nasty 56% year-on-year and 19% quarter-on-quarter.

Net debt spiked 39% year-on-year, but is only slightly higher sequentially.

The headline loss per share for the quarter was 6 US cents. That’s smaller than the headline loss per share of 19 US cents in Q4’25, so there’s some sequential improvement at least. But compared to positive HEPS of 12 US cents a year ago, it makes for unpleasant reading.

The trouble for Sappi investors is that there are numerous external factors that affect the results each quarter. For example, as we’ve seen in other industrial names, the stronger rand actually creates difficulties for profitability in the Southern African region, particularly when combined with lower international prices for products like dissolving wood pulp.

It’s a real pity that even a 10% increase in pulp segment volumes year-on-year wasn’t enough to offset the pricing declines. Volumes in packaging and speciality papers were also higher by 6%, yet lower prices impacted that business as well. Graphic papers suffered a 9% drop in sales volumes, but managed to keep margins above historical trends.

Then you get all the usual risks in a manufacturing business, like scheduled maintenance shuts and unplanned operational disruptions. This is what we’ve seen play out at the Somerset Mill in North America.

Sappi has been reducing costs in Europe and rationalising the business, but it wasn’t enough to offset these pressures.

There aren’t many highlights in here, but one thing that investors will like is that capex was $56 million in this quarter. That’s way down on $101 million a year ago. When Sappi released full year FY25 numbers, they committed to the market that capex would be below $300 million per annum for the next two years in an effort to repair the balance sheet. This is a promise that they seem to be keeping, with a revised target of $260 million for FY26.

The guidance for the second quarter is filled to the brim with forecasting risk, as Sappi operates in such a difficult environment with multiple factors at play. Overall, they expect adjusted EBITDA to be worse in the second quarter than in the first quarter. Ugh.

Cyclical stocks tend to offer the best buying opportunities when it appears as though nobody could possibly want the shares. That’s what a chart of this phenomenon looks like:

Your eyes are not deceiving you – Sappi is trading at COVID and Global Financial Crisis levels! Have we reached the bottom or will rand weakness drag it even lower? Thanks to a fun new element in Ghost Bites, you can vote in the poll below and we can do a proper sentiment check as a community:

Even more good news at Sea Harvest (JSE: SHG)

Both the seafood and dairy businesses had a strong year

Primary agriculture is a tough gig, especially when you involve the unpredictability of the ocean. Financial performance tends to reflect the volatility of Mother Nature herself: some years are glossy blue days with perfect skies, while others look like they could inspire disaster movies.

Thankfully, the 12 months to December 2025 was a financial year straight out of a tourism brochure. Sea Harvest released an initial trading statement in November that indicated a jump in HEPS from total operations of at least 200%. Fast forward to February and we have a further trading statement that is even better, with an expected increase of between 293% and 303%!

This means that group HEPS has approximately quadrupled from 55 cents to between 216 and 222 cents. You can almost imagine the coconut cocktails with a view of sunset over the ocean.

One of the nuances in the results is that Ladismith Cheese is being sold to Fairfield Dairy based on an enterprise value of R840 million. This deal was announced in November 2025 and makes sense in the context of the company’s push to reduce debt. This means that Ladismith Cheese is reflected as a discontinued operation.

If we therefore dig deeper into the numbers, we find that discontinued operations (i.e. Ladismith Cheese) achieved HEPS growth of 25% to 35%. The continuing operations were particularly crazy, up by between 434% and 444%! The oceans are a lot more unpredictable than fields of cows and cheese facilities.

Aside from the higher catch rates that make a significant positive difference to the numbers, Sea Harvest also locked in efficiency gains in the hake business. To add to the party, pricing improved significantly. This combination can only ever lead to higher earnings, especially in a business with high operating leverage (it costs the same to send out a fishing boat regardless of how much you catch and what the fish are worth).

It’s not all good news of course. There are some impairments that sit in Earnings Per Share (EPS). As a reminder, these impairments are excluded from Headline Earnings Per Share (HEPS).

The impairments relate to the Shark Bay prawn fishery in Australia, the mothballing of abalone farms based on depressed consumer demand in the East, and Cape Harvest Food in relation to the disposal of Ladismith Cheese where the assets exceed the selling price of the business.

The share price closed 4.9% higher on the day.

Egypt takes Vodacom to new heights (JSE: VOD)

The share price has continued where it left off in 2025

2025 was a year to remember for the telcos sector. With the dollar giving frontier markets a breather, Vodacom (and MTN (JSE: MTN)) took full advantage. Suddenly, those earnings in Africa actually meant something, as they weren’t being washed away by currency depreciation.

Africa became investable in 2025 thanks to a new era of US politics. It turns out that when the elephants are fighting, most of the grass has a surprising opportunity to grow.

Results for the quarter ended December 2025 reflect ongoing momentum in the business, especially in Egypt. Group revenue was up 11%, but the segmental view really tells the story. South African service revenue was up just 1.4%, while Egypt grew by 39%!

There’s been a lot of focus on local prepaid revenue recently, with a price war underway across the South African service providers. Vodacom doesn’t give an exact number, merely referring to “revenue under pressure” based on the consumer backdrop and promotional pricing. With contract revenue up 2.6% and data traffic up 32.3%, prepaid revenue must be a fairly nasty number to drag South African service revenue growth down to just 1.4%.

Financial services revenue is another important growth lever, up 24.7% at group level and 59.4% in Egypt.

Encouraged by the current macro environment and the opportunity in Africa, Vodacom announced in December that they would be acquiring an additional 20% stake in Safaricom. Kenya and Ethiopia are attractive markets, so I can see why Vodacom would want to have a controlling stake (55% after the acquisitions) in this business.

In South Africa, the major deal is of course the Maziv fibre transaction, which Vodacom had to fight incredibly hard for at the Competition Commission. Approval finally came in November and implementation began on 1 Deember 2025.

Vodacom and MTN look like heroes right now, but a different result in the US election would almost certainly have resulted in a very different conversation around African earnings. Policies can change quickly, so investors need to always remember that frontier markets are risky places.

With 27.5% of Vodacom group revenue now being generated in Egypt, they will ride this macro wave for as long as possible and be rewarded for it in the market. But if the dollar starts putting pressure on these currencies again, Vodacom will be highly exposed.

There isn’t much of an alternative though, as sitting back and defending market share in South Africa is a strategy that would attract a very low valuation. It’s also incredibly difficult to do acquisitions here, as evidenced by the Competition Commission’s approach to the Maziv deal.

It’s literally a case of nothing ventured, nothing gained. Africa is where the opportunity lies.

Nibbles:

Director dealings:

A director of Stefanutti Stocks (JSE: SSK) bought shares worth R34.7k.

The spouse of a director of Afine Investments (JSE: ANI) bought shares worth R7k. There’s very little liquidity in this thing, with average daily value traded of around R15k!

With Zeder (JSE: ZED) having announced the disposal of Zaad, the company has relooked at its management function and decided to restructure things in light of how much smaller the group is becoming. Johann le Roux will step down as CEO and FD with effect from 28 February 2026. He will be replaced by Dries Mellet as FD and acting CEO. Don’t feel too sorry for le Roux here: in a separate announcement, Zeder noted net cash settlement of options to le Roux worth around R5.2 million! That’s like a memorable goodbye kiss after a successful first date.

It’s now Investec’s (JSE: INL | JSE: INP) turn to welcome Standard Bank (JSE: SBK) to the share register, with a shareholding of 5.95%. I’m now even more convinced that these must be stakes held via Liberty within the Standard Bank group, or some other broad investment vehicle. You may recall that Nedbank (JSE: NED) recently announced a similar stake held by Standard Bank.

Datatec continues to increase its international footprint through bolt-on acquisitions that add to the business without creating significant risk. This is a clever and effective way to grow, although it does take longer. This is the benefit of investing alongside a founder CEO, rather than a “manager” CEO trying to move the dial and maximise earnings during a term of only a few years.

The latest deal is an acquisition by Logicalis US of Maple Woods Enterprises, a long-term cybersecurity partner of Logicalis US. The Maple Woods Overwatch offering is built for the US defence industry, so it’s clearly robust.

Cybersecurity is a priority area for the group, so I expect to see more deals like this in future.

Glencore does a deal with Orion for its DRC assets – but no, it’s not that Orion (JSE: GLN)

Orion Critical Mineral Consortium is a US-based entity

Glencore announced that Orion Critical Mineral Consortium will look to acquire a 40% stake in Glencore’s interests in the DRC assets. The implied combined enterprise value of the assets is around $9 billion, so this is a large transaction.

Orion Critical Mineral Consortium is focused on securing critical minerals (as the name suggests) for the US and its partners. This consortium was only established in October 2025, so this is firmly a Trump-era initiative. In this case, the minerals in question are copper and cobalt.

Encouragingly for the DRC and the people near the mines, Glencore will look for opportunities to expand and develop these mines. They will also be open to additional critical mineral projects and assets in the DRC alongside their new partner. There’s certainly no shortage of capital in the US, so being able to tap into the world’s deepest capital pool is helpful.

Harmony Gold had a wobbly, but they believe they can still achieve guidance (JSE: HAR)

Here’s another reminder that the commodity price is only half the battle won

The other half, of course, is getting the stuff out of the ground. For the six months to December 2025, Harmony Gold had some challenges in doing that.

A mill motor failure and a deferment of the final gold shipment at Hidden Valley to January 2026 will impact the interim numbers, but should be fine on a full-year basis. Other issues included disappointing recovered grades and an industry-wide cyanide shortage in South Africa.

Despite this, the company hopes to meet full-year production guidance and achieve the planned all-in sustaining cost.

The CSA copper operation in Australia is being integrated into the group after the recent acquisition, while the Eva Copper Project has an appointed EPC contractor that is expected to be on site during the March 2026 quarter.

Hyprop confirms the retail trend that we can all see: a shift from December to Black Friday (JSE: HYP)

South Africans love a deal even more than they love decorated trees

Hyprop released an update for the six months to December. We’ve seen in retailer commentary that sales growth in November seems to be stronger than December. The words “record Black Friday” have come up at various retailers. Hyprop has confirmed this trend, noting a pull-forward of sales from December to November.

This is of course great news for online adoption, as I would wager that Black Friday sales have higher online penetration rates than Christmas shopping when people are on holiday. In an omnichannel environment where orders are fulfilled from stores, my understanding is that Hyprop and other landlords still get a slice of that action.

In the South African portfolio, tenant turnover increased 5.6% in November and only 4% in December, so the trend is clearly visible there. Foot count is even more interesting, up 3.6% in November and thus similar to October at 3.5%. But December was only up 0.8%, supporting my thesis that a shift from Christmas to Black Friday will simply pull a portion of foot count out of the system forever. People aren’t going to the shops as often as they used to.

For the six months, tenant turnover was up 5% and trading density improved by 7.5%. These are decent metrics, particularly in a lower inflation environment.

In Eastern Europe, online adoption is even more obvious. Foot count has declined in every single month in the period, down by 3% overall. Tenant turnover was up 3.8% and trading density climbed 3.6%.

I’m fascinated by the concept of grocery stores as anchor tenants and how things just aren’t what they used to be in terms of these stores attracting people to the malls. It feels like it’s only going to get worse, not better.

Impala Platinum’s profits go to the moon (JSE: IMP)

This is what happens when commodity prices increase sharply

Impala Platinum has released a trading statement for the six months to December 2025. As you might expect, the numbers are incredible.

HEPS is expected to increase by between 392% and 411%, coming in at between R10.15 and R10.54 per share. Although these are interim numbers, annualising is a dangerous game in this sector because things can change so quickly. The share price trading at around R304 shows you how much is baked into this story in the market.

377 jobs on the line at Mpact’s Springs Mill (JSE: MPT)

The rand doesn’t help, but neither do hostile policies in South Africa towards employees and businesses

A weak rand has historically propped up local industrial companies who have managed to compete locally and globally despite the substantial inefficiencies that come with manufacturing in South Africa. We really don’t make it easy down here, with issues ranging from labour laws through to energy availability and costs.

With the rand now strengthening (and the SARB absolutely obsessed with avoiding any rate cuts), our manufacturers are coming under pressure. It’s a two-pronged issue, with exports becoming less lucrative and imported alternatives becoming cheaper.

Mpact is one of the first public examples of this issue playing out, but there will be others.

Mpact’s Springs Mill is the only domestic producer of cartonboard, competing directly with imports that have found a home in South Africa in an environment of overcapacity in the global cartonboard market. The largest customers of the mill can import cartonboard at prices that are 20% lower than the cost of local production. You can guess where this is going.

When you consider that operating profit for the year ended December 2024 was just R32 million based on revenue of R1.74 billion, you can see that there was no room to absorb this pricing pressure.

With the largest remaining customer notifying Mpact that they will be importing going forwards and no longer procuring from Springs Mill, the show is over for that facility. Production will run until the end of March, at which point 377 people are likely to lose their jobs.

Of course, in a vibrant economy, there should be 377 new jobs waiting for these people at companies that can flourish in a stronger rand environment. Alas, this isn’t a vibrant economy.

Hold on to your seats: the TFG bloodbath isn’t over (JSE: TFG)

The Foschini Group’s offshore results are going from bad to worse

The Foschini Group (TFG) is having a really tough time at the moment. It looks even worse in the context of 2025’s Capital Markets Day. Analysts felt that the targets shared that day were spicy to say the least, but I don’t think anyone expected this level of underperformance. I’m becoming concerned that TFG and Pick n Pay (JSE: PIK) might be in the same WhatsApp group.

TFG has released a trading update for the quarter and nine months ended 27 December 2025. There’s a lot of detail to unpack, but the overall theme is that TFG Africa is losing ground and the offshore businesses barely know where the ground is anymore.

Group sales increased 2.9% for the quarter, which is much lower than the 7.5% year-to-date growth. One of the reasons is that TFG Africa grew 3.5% for the quarter vs. 4.2% year-to-date, a noticeable slowdown. Another big reason is that White Stuff, part of TFG London, was acquired in October 2024 and was thus in the base for Q3. This is why TFG London was only up 6.5% for the quarter vs. 37.2% year-to-date where Q1 and Q2 weren’t comparable to the previous years.

It’s easy to grow by acquiring revenue, so that year-to-date number isn’t reflective of performance. Here’s the number that does show you the performance: if you strip out White Stuff, TFG London’s sales fell 2.4% in the third quarter and 2.6% over nine months. Yuck!

That’s still better than retail widowmaker Australia, down 2.6% for the quarter and 1.9% for the nine months.

And if you exclude White Stuff from the group numbers, then sales growth over nine months is only 2% instead of 7.5%. You get the idea.

The clear highlight is online sales. At group level, they increased 23.4% in the third quarter and 36.6% year-to-date, now contributing 14.3% to total retail sales. In TFG Africa, Bash did what it says on the tin and dished out pain to the competition, growing online sales 54.9% in the third quarter and 46.7% year-to-date. Online sales are now 7.9% of total sales in TFG Africa.

I’ll say the same thing that I said in the Pepkor (JSE: PPH) update this week: Mr Price (JSE: MRP) is asleep at the wheel in online sales and needs to stop throwing away market share by barely participating.

We may as well deal with TFG Africa, where like-for-like sales were up 1.2% in the third quarter and 2.9% year-to-date. I cannot for the life of me understand how Cellular sales can be down 2.5%, as that has been a very strong performer at major competitors. I guess for others to be winning, someone had to be losing! At least Beauty is a real highlight, up by 20.3% in the third quarter.

A meaty 26.1% of TFG Africa’s sales are on credit. The debtors book is 6.8% higher year-on-year, a surprising increase in the context of the credit sales performance of 5.3% year-to-date. They call it a steady risk environment, but that doesn’t seem particularly steady to me. Hopefully we won’t see credit challenges coming through as well, as TFG has more than enough to deal with already!

TFG London and TFG Australia continue to be huge headaches, with the group now expecting impairments of up to R750 million. This doesn’t impact HEPS, but it does indicate the extent of value destruction in those offshore businesses in recent times. This is just one of the many cautionary tales that Mr Price has opted to ignore in pursuit of NKD in Europe.

Before you feel that HEPS is safe, I must point out that TFG London’s gross margin has contracted by 90 basis points year-to-date based on inventory clearance. When you combine this with the pressures across the board, I suspect that investors are in for another rough ride in terms of HEPS. The company hasn’t given a range for HEPS in this update.

In terms of outlook and recent trading, TFG Africa’s sales grew 5.8% for the 5 weeks to 31 January 2026. TFG London increased 5.6% in local currency, which is an encouraging outcome. TFG Australia remains a mess, down 1.1% in local currency.

The share price is down 39% over 12 months. I personally don’t think we are anywhere near the bottom yet, but we will see how the market reacts to this update that came out at the close of play on Tuesday.

A bitter outcome for HEPS at RCL Foods (JSE: RCL)

The sugar is to blame

RCL Foods released a trading statement dealing with the six months to December 2025. I’m afraid that it isn’t good news, with HEPS expected to be at least 25% lower year-on-year.

The move is much bigger in earnings per share (EPS), but that’s because of numerous adjustments related to non-cash gains and insurance proceeds. This is exactly why the market focuses on HEPS instead, as it gives us a standardised metric that strips away as many of these distortions as possible.

So, what happened in HEPS? The answer lies in the sugar business.

A once-off partial recovery of the sugar industry levy in the base period is responsible for 5.6 cents of the “at least” 27.4 cents drop in HEPS. Kudos to the company for giving helpful and detailed disclosure here!

The remaining 21.8 cents is thanks to the performance in the sugar business itself, with the challenge being an influx of imports that led to local production being sold in the less lucrative export market.

This tells us that sugar is more expensive locally than it would be without tariffs. The importance of the growers and millers in the South African industry leads to government being willing to protect them, with RCL pushing for amendments to the tariffs to do something about these deep sea imports that have hurt the local industry.

Thankfully, the Groceries and Baking units are achieving higher profits despite pressure on volumes. It’s just not enough to offset the pain in Sugar as the largest individual segment from an EBITDA perspective.

Well, Sugar probably isn’t the largest segment anymore, as Baking has been hot on its heels and this update suggests that there might be a new pecking order within RCL.

Southern Sun will take a 50% stake in key properties in Sandton (JSE: SPG)

Liberty will be selling to Southern Sun and Pareto

Southern Sun currently operates the Sandton Sun, Sandton Towers, Garden Court Sandton City and Sandton Convention Centre under long-term contracts with Liberty and Pareto. Those two companies have stakes of 75% and 25% in the properties respectively.

Liberty is a wholly owned subsidiary of Standard Bank (JSE: SBK) and Pareto is owned by the Government Employee’s Pension Fund, managed by the PIC.

Liberty is going to sell its stake in Sandton Towers, Garden Court Sandton City, Sandton Convention Centre and the Virgin Active Sandton (but note: not Sandton Sun). Pareto will increase its stake from 25% to 50%, while Southern Sun will take the other 50%.

Strategically, this makes sense for Southern Sun. They own the majority of their hotel portfolio, giving them far more control than if they were purely an operator on behalf of others. Being able to take a 50% stake in these properties creates more strategic alignment with the rest of the portfolio.

Southern Sun’s 50% stake will cost them R735 million, payable from available debt facilities. This is in line with the independent valuation that was done as at December 2024.

This seems like a strong deal for Southern Sun, with the share price closing 4.3% higher in appreciation.

Super Group’s continuing operations live up to the name (JSE: SPG)

The same can’t be said for the automotive business in the UK

Super Group has released a trading statement for the six months to December 2025. HEPS is expected to be between 23.6% and 31.8% higher, which means a range of between 150 cents and 160 cents. To add to that good news, the balance sheet is in good shape and net debt ratios are healthy.

Great, but what about the discontinued operations?

If you include those operations and therefore look at the group total, then HEPS is between 134 cents and 145 cents. The year-on-year move is less relevant, as the disposal of SG Fleet in the prior year impacts comparability. The part that is relevant is that the UK automotive segment is in trouble.

The Hyundai and Suzuki dealerships in the UK have been closed. The UK KIA dealerships remain in discontinued operations. The automotive logistics segment has deteriorated thanks to a cyberattack on Jaguar Land Rover that led to a two-month shut down of production. If there are no cars being produced, there’s nothing to move around in the logistics business. This drove a trading loss in AMCO of R25.5 million for the six months. Overall, the UK is an unhappy place in the automotive space right now.

Super Group clearly believes in the mantra of your first loss being your best loss. They’ve decided to exit AMCO and they are looking for a buyer. This is why the business has landed in discontinued operations in this update. But with no guarantee of a buyer emerging quickly (or at a reasonable price), I don’t think it would be right to focus only on the continuing operations in this update.

The release of results on 24 February will have full details for investors.

Zeder finally has a buyer for Zaad (JSE: ZED)

The share price closed 18% higher on the day

Zeder has been a value unlock play for as long as anyone can remember. They’ve been selling off smaller assets in the group, but Zaad has always been the big fish that needed to find the right line to be hooked onto.

That line has come in the form of a consortium of WIPHOLD, the PIC, the IDC and Phatisa Food. This gives enough balance sheet muscle for Zeder and the minorities in Zaad to be able to sell their shares and claims for up to R1.42 billion. Zeder will receive R1.39 billion of that amount.

In case you aren’t familiar with the business, Zaad operates in the agri-inputs industry with a focus on emerging markets in Africa, the Middle East and Eastern Europe.

Nothing is ever quite this simple. As a precursor to this deal, excluded assets worth R801 million need to be sold separately or restructured out of Zaad Holdings. This means that Zeder will continue to own May Seed and various other assets. The assets other than May Seed are in the process of being disposed of.

Zeder intends to distribute a “significant portion” of the deal value to shareholders. They will give further information in the circular when it is released to shareholders (around 23 March 2026), as this is a Category 1 transaction.

The value of the shares and claims in the latest financials was R2 billion, but this included May Seed and the other “excluded assets” and isn’t directly comparable. This implies that they’ve sold roughly R1.2 billion worth of assets for R1.42 billion. Importantly, the share price was trading at a discount to the valuation anyway, so this price is significantly higher than the market cap was implying.

That’s how a value unlock is supposed to work!

Nibbles:

Director dealings:

Saul Saltzman, son of the founders of Dis-Chem (JSE: DCP), sold shares in the company worth R12.7 million.

A prescribed officer of Life Healthcare (JSE: LHC) sold shares worth R9 million.

A director of a subsidiary of RFG Holdings (JSE: RFG) bought shares worth R119k.

A director of a major subsidiary of Insimbi Holdings (JSE: ISB) sold shares worth R71.5k.

Bowler Metcalf (JSE: BCF) has a market cap of just over R1 billion, making it a small cap on the JSE and thus a company with limited liquidity in the stock. Recent results seem to be solid though, with revenue up 8% for the six months to December and HEPS up by 16%. The cash has followed suit, with the interim dividend up 16%. Nice!

Tharisa (JSE: THA) is looking for a new CFO after the resignation of Michael Jones with effect from 31 July 2026. That’s a solid handover period that reflects an innings of 14 years as CFO. It will be interesting to see whether they have an internal replacement lined up vs. bringing in external ideas.

Stefanutti Stocks (JSE: SSK) has made another repayment of R50 million to Standard Bank. The outstanding facility has been reduced from R300 million to R250 million.

Sirius Real Estate (JSE: SRE) announced the results of the dividend reinvestment programme. Holders of 0.46% of issued shares in the UK and 3.0% of issued shares in South Africa opted to receive shares instead of cash. But here’s the nuance: settlement is through the purchase of shares in the market rather than the issuance of new shares. This is therefore non-dilutive to other shareholders.

Between 26 November 2025 and 22 January 2026, Argent Industrial (JSE: ART) repurchased R11.4 million worth of shares at an average price of R33.34. The current price is R32.50. This only represents 0.63% of shares in issue and they have the authority to do far more.

MTN Zakhele Futhi (JSE: MTNZF) shareholders will receive an “agterskot” payment thanks to the costs of unwinding the scheme being less than anticipated. The final payment is 23 cents per share, of which 8 cents is the agterskot and 15 cents is the scheme consideration.

DRDGOLD inks a wage deal with NUM and AMCU (JSE: DRD)

This brings certainty, but also above-inflation increases for five years

DRDGOLDhad a tricky end to 2025. Despite gold prices doing wonderful things for the share price, the company received notice of a protected strike action from NUM and AMCU. The strike was suspended to allow the parties to sit around the negotiating table.

It looks like the unions came out with a strong deal here. They’ve secured increases of between 6% and 7.5% per year for the next five years. There’s a new 2% performance-based incentive based on key metrics, as well as various other improvements to allowances and support schemes. Backpay is payable from 1 July 2025. And as the cherry on top, there’s a payment of R5k to each employee!

DRDGOLD better hope that the gold price keeps doing well.

MC Mining takes drastic action with Uitkomst Colliery (JSE: MCZ)

This comes after the quarterly update that revealed the difficulties

MC Mining has attracted international investment based on the exciting Makhado hard coking and thermal coal project. The problem is that the group also owns Uitkomst Colliery, where the financial performance is going from bad to worse. In business as in life, you cannot allow a tumour to go untreated.

This is why MC Mining has taken the decision to temporarily suspend mining and processing operations at Uitkomst with an intended effective date of 1 March 2026. They have a lot of hoops to jump through to achieve this, not least of all from a labour and retrenchment perspective.

It’s always very sad to see stuff like this, but businesses are run for a profit and sometimes need to make tough decisions. Uitkomst is suffering cash losses at the moment, something that a mining company with an important development project just cannot (and shouldn’t) stomach.

The reference to this being a temporary closure is just an effort to retain long-term optionality. I can’t see them magically reopening in a couple of months.

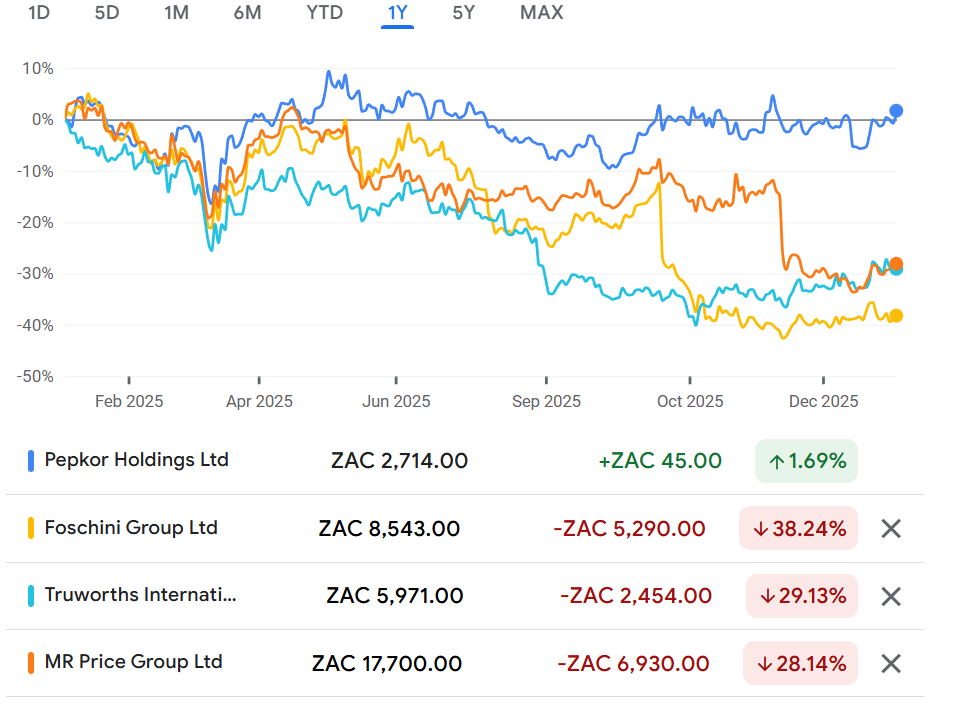

Pepkor had a solid finish to 2025 despite the tough base (JSE: PPH)

This is why the share price suffered much less than clothing peers over the past year

We know that the clothing sector has been a hideous place to invest in the past year. Even Pepkor, by far the best of a bad bunch, is only flat over 12 months. That’s considerable outperformance in this context though:

Yikes!

Pepkor’s defensive share price performance has been well earned. For the three months to December 2025, a really tough period vs. the two-pot withdrawal base period at the end of 2024, revenue was up by 8.3% if you split out the acquisitions. If you include them, then revenue was up 12.9%. Impressively, the two-year CAGR without acquisitions is 10.3%. Double-digit revenue growth in this market is excellent.

Sales in Southern Africa were up 2.0% on a like-for-like basis. In PEP Africa and Avenida, like-for-like sales were up 12.7% in constant currency, as those businesses didn’t have the two-pot withdrawal distortion that we had in South Africa. In rand terms, they were up 16.7%.

In case you’re wondering, PEP Africa and Avenida contributed 4% and 5% of group sales respectively.

Another important lens is to compare cash sales (up 7.4%) to credit sales (up 26.9%). Credit sales contributed 18% of total sales.

Group online sales increased by 27.9%, an exceptional performance that shows how important digital adoption is across the LSM curve. Mr Price (JSE: MRP) should pay attention here, as their online sales are only growing in line with in-store sales.

Looking at the retail segments, the Clothing and General Merchandise (CGM) segment grew 5.8% excluding acquisitions and 7.5% on a two-year CAGR basis. Furniture, Appliances and Electronics (FAE) grew 4.6% excluding acquisitions and 6.5% on a two-year CAGR basis. I must note that CGM is over 5x the size of FAE, so these segments are far from being of equal importance.

Speaking of importance, PEP and Ackermans contributed a combined 63% of group sales. It’s therefore critical that these parts of the business perform well. Ackermans struggled with a 0.6% decline in like-for-like sales, but PEP managed a strong 2.8%. Back-to-school is a critical period for Ackermans, so the current quarter likely matters even more than the festive quarter.

Retailers often have to make tough decisions in their footprints. For example, Pepkor has closed Shoe City – that’s a significant closure of 113 stores. Making these tough decisions is key in driving the group forwards.

You might be wondering how those segmental performances reconcile with the much stronger group revenue performance. The answer lies in the Fintech segment, where revenue was up by a wonderful 25.4%. This includes financial services, insurance, cellular and other revenue opportunities.

In the first three weeks of January 2026, they’ve carried on where they left off. Group sales were up 8.3% excluding acquisitions.

Shoprite piles the pressure on competitors (JSE: SHP)

They achieved above-inflation earnings growth despite being very aggressive on price

Shoprite isn’t trying to win a competition based on who can release the best quarterly results. They are playing a long game, acting as the python that is continuously squeezing the impala until it devours the whole thing. Retail is a game of tiny incremental changes and improvements, particularly in grocery retail where consumers are so price sensitive.