A festive staple with a surprisingly cutthroat backstory, the poinsettia’s rise to Christmas royalty is tangled up with colonial meddling, corporate monopolies, and a global plant arms race. This is the unlikely tale of how a fragile Mexican shrub became one of the most powerful products in the modern holiday economy.

Every year, just after November, it emerges. In great crimson waves, it stakes its claim, conquering territory at nurseries, grocery stores, and reception desks around the country.

Christmas is nigh, because the poinsettia has arrived.

With roughly 200 million plants sold worldwide annually and a retail haul well over the $1 billion mark, the poinsettia is, without exaggeration, one of the most commercially successful plants on Earth. Not bad for a humble Mexican shrub with a name that sounds like something you’d see a podiatrist for.

But those showy red leaves (yes, those are technically leaves, not flowers) are concealing a story absolutely heaving with geopolitics, patent wars, botanical espionage, dethroned monopolies, and a global supply chain so tangled it makes Christmas lights look organised.

So how did cuetlaxochitl – a plant once used to dye cloth and treat fevers – become the undisputed queen of Christmas décor?

A shrub with divine connections

Long before Woolies flooded their checkout displays with them, the poinsettia lived quietly in its native habitat of Southern Mexico. To the local Nahua people of the 14th century, it was less of a festive decoration and more of a practical aid; they mostly used it for dye and medicine.

Everything changed when the Spanish arrived and, in a rare moment of colonial subtlety, didn’t rename it something horrendous like “Royal Scarlet Colonial Flower of His Majesty”.

Instead, Franciscan monks in the 1600s christened it “flor de Nochebuena” – aka “Flower of the Blessed Night”. They incorporated it into Christmas celebrations, drawn to its star-shaped leaf pattern (which they said symbolised the Star of Bethlehem) and its vivid red bracts (representing Christ’s sacrificial blood). The white variants suggested purity. Hence, the plant’s connection with Christmas, one of the most important holidays on the Christian calendar, was firmly established.

For a few centuries, the plant was a local superstar, beloved in Mexico but virtually unknown everywhere else. Then Joel Roberts Poinsett walked onto the scene like the main character and turned everything upside down.

The diplomat who couldn’t stay out of trouble

Poinsett, a wealthy Southern Unionist, slave owner, and America’s very first diplomat to Mexico, had what you might politely call a talent for making himself unwelcome. During his tenure in the late 1820s, he managed to irritate just about everyone – partly because he tried to buy Texas (unsuccessfully), and partly because he simply couldn’t resist meddling.

But in 1828, just before Mexico finally told him to please pack his bags and go home, Poinsett visited the town of Taxco. There, he spotted flor de Nochebuena and had what can only be described as a botanical epiphany. He immediately shipped cuttings of the plant back home to the US.

A few years later, the poinsettia – now renamed after its “inventor” – made its American debut at a flower show in Philadelphia. People lost their minds. No-one had ever seen anything like it. Demand skyrocketed, and supply raced to keep up.

There was just one problem: the early poinsettia was actually terrible at being a commercial product. It wilted after 2–3 days, it hated travel, and it dropped leaves the moment you looked at it funny. Basically, it was the houseplant equivalent of a Victorian child who took ill if the weather changed unexpectedly.

If the poinsettia was going to make it in the big leagues, it was going to need a miracle. Fortunately, it got the Ecke family.

The dynasty that turned poinsettias into Christmas royalty

In 1900, German immigrant Albert Ecke set off for Fiji to open a wellness spa, but never quite made it there. On the way, he stopped in Los Angeles, liked the sunshine, and simply… stayed. His detour would go on to change agricultural history.

Not one to sit on his hands, Ecke built a dairy, then a fruit orchard, then started selling cut flowers, including poinsettias. He therefore had his ear to the ground when the big poinsettia boom started to rumble. Wisely, Ecke diverted his attention and made poinsettias the centre of the business, earning a relatively good living as a result.

His son, Paul Ecke, took over the family flower farm in the 1920s and had two big insights: 1) poinsettias needed better genetics and 2) the public needed better marketing. He introduced a secret grafting technique (a closely guarded method learned from an amateur gardener in Germany) that produced poinsettias with fuller shapes, more branches, sturdier stems, and longer shelf lives. In other words: consumer-proof poinsettias.

Then came the Plant Patent Act of 1930. Ecke immediately registered dozens of his unique cultivars, shutting out copycat competitors faster than you can say “intellectual property rights”. But Paul’s son, Paul Jr., took it even further. Unlike his father, he understood the power of the media. He knew that in order to get people to buy something, you needed to put it where they could see it. He flooded women’s magazines and breakfast television shows with free poinsettia samples. He (and his plants) even appeared on The Tonight Show. In doing so, he transformed the poinsettia from a plant into a seasonal identity.

By the 1990s, the Ecke empire was moving 500 000+ potted plants and more than 25 million cuttings a year. Their market share was a staggering 90%. As one journalist at the time so succinctly put it: “The Eckes of Southern California are to poinsettias what De Beers is to diamonds.”

But just like diamonds, that dominance was about to crack.

The graduate student who broke the monopoly

In 1992, a graduate student named John Dole got his hands on an Ecke cutting and did what graduate students have always done best: he tinkered. Piece by piece, experiment by experiment, he worried at the problem until the industry’s most closely guarded secret finally gave way. Dole had reverse-engineered Ecke’s top-secret grafting method – and instead of locking it back up, he published it. The effect was immediate and explosive.

Once the technique was no longer proprietary, the mystique vanished overnight. Anyone could now grow poinsettias with the same full, lush form that had defined Ecke plants for decades. Competitors rushed in, and the 1990s turned into a kind of poinsettia renaissance. Breeders pushed boundaries, colours multiplied, sizes shifted, patterns grew bolder, and varieties emerged with names that sounded less like plants and more like 80s rock bands – think Premium Picasso, Monet Twilight, and the like.

Then the big-box retailers arrived, and the tone of the industry changed again. Home Depot, Lowe’s, and Walmart recognised poinsettias as the ideal holiday loss leader: seasonal, emotional, and disposable enough to sell by the million. Prices plunged, sometimes as low as 99 cents a plant. Margins collapsed. Growers were squeezed hard, small farms disappeared, consolidation accelerated, and production steadily migrated offshore.

By 2012, even the once-invincible Ecke empire could no longer stand apart. It was sold to Dutch giant Dümmen Orange, one of the largest plant breeders in the world. An era ended. In its place, a globalised supply chain took root.

A global empire with one major omission

Today, Dümmen Orange sells roughly 60 million poinsettias a year – more than half of the global supply – which means there’s a good chance the plant sitting on a table at your local nursery traces its lineage back to them. The poinsettia may feel ubiquitous and anonymous now, but behind that familiarity sits an industrial-scale operation quietly dominating a once-fragmented market.

There’s an irony threaded through this success. While the world buys millions of poinsettias every December, the country where the plant originated, Mexico, still struggles to sell its own potted versions in the United States. A century-old soil restriction means Mexican growers are allowed to export cuttings, but not fully grown plants. As a result, Mexico earns around $12 million a year supplying the raw genetic material, while the far more lucrative potted-plant market remains firmly out of reach.

For many growers, the resentment is palpable and understandable. This is, after all, their native plant. Yet the poinsettias filling homes and shopping centres around the world are overwhelmingly patented, branded, and controlled by foreign firms, their value captured far from the soil where the species first evolved.

In Mexico, the tension has even seeped into language. “Poinsettismo” has become a slang insult, used to describe someone arrogant or intrusive. A pointed jab, especially when you remember that the plant’s global fame began with one very intrusive American diplomat.

A holiday icon, no matter the politics

For all the geopolitics, the patents and supply chains, the monopolies and student-led disruptions, the rise of Dutch mega-breeders and the slow grind of global consolidation, one thing has remained stubbornly unchanged: nothing signals Christmas quite like a poinsettia.

What began as a Nahua medicinal dye has become a billion-dollar global holiday symbol – a star-shaped burst of colour that shows up, unfailingly, every December. It’s a reminder that history rarely moves in straight lines, and that the objects we take for granted often carry stories that are stranger, messier, and far more interconnected than we imagine.

About the author: Dominique Olivier

Dominique Olivier is the founder of human.writer, where she uses her love of storytelling and ideation to help brands solve problems.

She is a weekly columnist in Ghost Mail and collaborates with The Finance Ghost on Ghost Mail Weekender, a Sunday publication designed to help you be more interesting.She now also writes a regular column for Daily Maverick.

Introducing Market Kokoro franchisees Lu-ise Hattingh and Ruan Botha:

Lu-ise Hattingh and Ruan Botha are a great example of the power and value of travel. After spending time in Japan, they fell in love with the culture and food. As all great entrepreneurs do, they also took the opportunity to learn about the Japanese approach to consumer brands. That curiosity eventually sparked a business idea they brought back home.

Today, Lu-ise and Ruan are rolling out Market Kokoro franchise stores in South Africa and especially the Western Cape, tapping into the existing Market Kokoro infrastructure in South Africa and adding their particular flavour of experiential retail. If you love the thought of cooking your off-the-shelf noodles in the store, then Market Kokoro is for you.

In bringing miso to Mzansi, one of the biggest insights is about the importance of meeting customers where they are, both in terms of tastes and locations.

On episode 6 of The Finance Ghost Plugged in with Capitec, Lu-ise and Ruan share the journey behind building a cross-cultural brand.

Episode 6 covers:

How travelling sparked the idea for Market Kokoro – and how this married couple turned a dream to bring this culture and food back home into a working business

Why their unique mix of skills (Ruan as an attorney and Lu-ise with a background in film and hospitality) lead to success

The background to Market Kokoro in South Africa and their involvement with the business

What makes the retail landscape in Cape Town different from Johannesburg – and how they adapt to each

Why additional sources of income are crucial while getting a business off the ground

The benefit of tapping into governmental organisations to help launch in a specific city

The consumer licensing opportunity in South Africa and how Japan’s model inspired their approach

The Finance Ghost plugged in with Capitec is made possible by the support of Capitec Business. All the entrepreneurs featured on this podcast are clients of Capitec. Capitec is an authorised Financial Services Provider, FSP number 46669.

Listen to the podcast here:

Read the transcript:

The Finance Ghost: Welcome to this episode of TheFinance Ghost plugged in with Capitec. We are deep in November at the time of recording and by the time you hear this, it will probably already be December. So we are in ‘silly season’ and people are busy, trying to finish things off before the end of the year.

Speaking of finishing things off, my guests today have been out there in the wild, building out their new store today, as they have been doing for the past few days and will probably still be doing for the next few years. Well, not that one store. If you’re still building the same store in a few years time, something has gone horribly wrong. But they’ll certainly be building this business for a few years. I’m really looking forward to chatting to these two. I think it’s going to be a huge amount of fun.

So my guests today are Ruan Botha and Lu-ise Hattingh of Market Kokoro. We will discuss their exact involvement with the group later in the podcast, along with that wonderful name of Asian descent. Well, not Ruan and Lu-ise, you guys definitely are not of Asian descent. You are both firmly South African, athough at this stage I’m actually starting to wonder if you might have honourary citizenship in Japan or Korea or wherever else, never mind South Africa, because you are doing so much work in this space to bring these cultures to South Africa.

Welcome to the show. It’s going to be a lot of fun.

Lu-ise Hattingh: Thank you. Thank you so much for having us.

Ruan Botha: Yeah, it’s great to be here.

The Finance Ghost: So, I think let’s jump straight into the word ‘kokoro’, which is so interesting. And, as you described it to me before we started recording this podcast, it effectively refers to the heart and the spirit (and hopefully I got that right). I think it’s such a lovely term, and it speaks directly to the way you’re actually building this business.

So, the backstory. There’s a lot for us to unpack here in terms of your relationship with Market Kokoro overseas and in South Africa, because it is an overseas brand that was then started here some years ago. And then you’ve been involved in developing it within the country and certainly in the Western Cape in particular, although you do have some business interests in it in Gauteng as well. Even your own podcast on some of this cultural-type stuff, Ruan, which we’ll get to later. But let’s start right at the beginning – that’s enough of a tease of what’s to come.

You’re a husband-and-wife team. You’re both young entrepreneurs. How did you get here? What was the backstory of the travels, and how this culture just grabbed you and inspired you to spend your day sweating it out, building out new stores?

Ruan Botha: Yeah, so I grew up in a small town in the Western Cape. And basically, it was pre-internet, so the library was the only means of connecting to the outside world. There was this one particular book that really stuck with me. It was a book on the Edo period or the Shogun period in Japan, and it had these beautiful illustrations of Japanese armour and just a completely different culture to anything that I’ve experienced up until that point. In South Africa, we knew China fairly well back then, but Japan was a little bit of a mystery. And so from a young age, I’ve had my eye on Japan.

Obviously, as a teenager, I got introduced to Japanese pop culture, anime and the like. So, Japan has been in the background for a big part of my life. And that’s kind of how I managed to pull Lu-ise into the realm of Japan.

Lu-ise Hattingh: I, on the other hand, had zero interest in Japan. I had my eye more on Europe. But, fast-forward a couple of years from Ruan’s teenage self watching anime, we ended up visiting Japan in 2016, just as a fun trip for two weeks. And when we came back, we were obsessed. We were like, “We just… We need more. More, please.”

And we just realised that it is such a culture with so much depth and so much to learn from. Fast-forward another couple of years to 2018, and we found ourselves engaged, ready to get married, and looking for an exciting honeymoon adventure!

Ruan Botha: We got an opportunity to go and work in Japan. A couple of months after getting married, we joke and said that we left on ‘an extended honeymoon’. And yeah, for three years, we lived in Japan where we immersed ourselves in the food, the culture – the retail obviously, by extension. We kept on reminding ourselves, “There’s so much that we want to take back to South Africa.”

We didn’t take this opportunity to live in Japan to escape South Africa. We are, as you mentioned at the start, very much South African. The idea was just to have a little bit of a ‘walkabout’, as they would say, and to go and experience a different country. But while we were there, we just wanted to come back and bring a lot of our experience that we enjoyed in Japan back to South Africa.

Lu-ise Hattingh: And of course, Japan – and especially the city where we lived, Miyazaki – was quite close to Korea. So we got to experience Korea a bit as well. And, same thing – the food got us. The food definitely got to us in Korea, and I think the retail, the experiences and the culture got to us in Japan.

The Finance Ghost: Well done on rather choosing to bring back South Korea because I think, if you brought back learnings from North Korea, that would be quite problematic. I’m not sure we’d be doing this podcast, for example. At least, not with my consent. No, I’m just kidding.

So when you were working in Japan, was that like the classic ‘teach English offshore’ kind of vibe, or what were you doing? It was that, right?

Lu-ise Hattingh: Yes, that’s why we went over. And then I eventually started working as an operations specialist for a US-based company. So I was working remotely. And then that’s also where Ruan got involved with JETRO.

Ruan Botha: Yeah, so we’ll get into the consumer product licensing side of things. And in our preparation, I spoke about how Japan is next level with that. But there, I got a lot of experience working with a local municipality as well and then, from there, got introduced to an organisation called JETRO.

The Finance Ghost: Okay, interesting. And I do want to take one step back before we get into some of that, because it really is just such a cool story.

How old were you guys when you met? Because it almost sounds like Ruan, you kidnapped her to Japan the first time, or basically just force-fed her anime and then eventually she was like, “Oh my gosh. If this guy is the one, I’m going to have to just stomach this and get over it. It’s Dragon Ball Z or nothing.”

Lu-ise Hattingh: That’s exactly how it happened. He captured me when I was still a teenager. We met when I was 19, and Ruan was 20 – the night of his birthday, actually, we met – and the rest is history. We’ve been together for 14 years now.

The Finance Ghost: Amazing. Very cool story.

Ruan Botha: In my defence, I just mentioned Japan and Lu said, “Okay, let’s go check it out.” And then, Asia did the rest.

The Finance Ghost: Were you wearing shogun armour and had one of those really big samurai swords when you mentioned Japan? And she said, “Oh, you know, let’s go have a look. You know, still deciding.” But I mean, she seems to have embraced it now, which is quite exciting. So whatever your tactics were, they clearly worked.

So, let’s move on to understanding more about this JETRO thing that you mentioned and then let’s get into some of your background. Just walk us through what that is and how that shaped the rest of your journey.

Ruan Botha: Cool. So I am an attorney by profession – Attorney of the South African High Court. But, going into law, I knew that was not necessarily what I wanted to do with my life. I knew it was a means to an end – which sounds kind of rude, I guess.

But for me, a legal background (unless you specialise, obviously that’s great), as an introduction to everything in South Africa, is quite broad. And it touches on a lot of different subjects.

The Finance Ghost: Look, it’s the same reason that I studied accounting, so I completely get it. Like, 100%.

Ruan Botha: Yeah, it opens a lot of different doors, right? I think accounting is maybe even more useful, because you get down to the nuts and bolts of a lot of things.

With a legal background, you get to sample bits of different companies. They say, “A clever person learns from their mistakes, but a wise man learns from other people’s mistakes.” And I think, in the legal profession, you get to see a lot of mistakes made by different businesses or organisations, and taking the little lessons from there has been very useful and helpful.

But then, after that, coming back from Japan, I got an opportunity to work for the Japanese External Trade Organisation, which is a Japanese government-related organisation that promotes trade from Japan to South Africa.

They identify various local South African partners, whom they then recommend to Japanese corporates or small businesses to kind of foster export-import relationships. And they’re based out of Sandton in Johannesburg. So, they work really hard to help SMEs in South Africa connect to Japan and, at the same time, help Japanese companies connect with South Africa.

The Finance Ghost: And that’s JETRO, right? The Japanese External Trade Organisation.

Ruan Botha: Yeah, that’s right.

The Finance Ghost: Yeah, got it. And then Lu-ise, your stuff is so interesting because, as far as I know, you have this film and hospitality background, right? You worked in some startups there. You kind of mentioned it’s such a diverse set of skills, which I guess is probably why this team works so well.

But before we even talk about the combination of those skills – just your own background, what you bring to this thing, how that journey was shaped – it’s so interesting to see how you got to where you are now. What have been some of the learnings and interesting nuggets along the way from that?

Lu-ise Hattingh: Yeah, I think hospitality and film sets you up for a really high-paced environment. If there’s anything that puts you through the wringer, I think it’s those two industries specifically.

It really teaches you about thinking on your feet, planning meticulously, executing on those plans to the T, and then just being really versatile. If you’re hired on a set for holding a boom, you’re probably going to do multiple other things, like wipe sweat off actors’ faces and run around for their specific dietary requirements.

So, that’s kind of where I started – behind the camera. I studied acting, but then realised I’m too short, fat and ugly to be an actress, so I had to go behind the scenes. And that’s just really where I started to get interested in operations and what goes on behind the ‘behind the scenes’.

So, I got really into the inner workings of what makes a business work because I think that every set, every production, is a small business in itself. You have your finances, you have your planning, you have your strategies. So, that’s where I started my journey into business. I worked with small businesses, startups from there and with founders growing their businesses.

And I think the main lesson, or what I bring into the retail space, is I think that every day in a retail store is almost like a show or a performance or a film set. Before opening, before the curtain goes up, you have your prepping, your cleaning of the store. You’re making sure that everything’s on track and everyone’s there. All the actors (AKA your chefs and your cashiers), they’re ready, they’re prepped, they’re hyped up for the day.

And then, when the doors open, that’s when the curtain goes up, and it’s showtime. And you have to smile and wave. Even if a customer comes in and you know they’re a little bit upset about something, or there are some challenges, you have to just keep the show going.

Ruan Botha: Yeah, there might not be applause all the time or a standing ovation, but you’ve got to keep the energy. And also, inevitably, you can plan and rehearse as much as you can…

Lu-ise Hattingh: …But someone’s going to forget their words!

Ruan Botha: Along the line, the light’s going to fall out of the attic, or someone’s going to slip and fall, or forget their lines. And you just have to roll with those punches.

Lu-ise Hattingh: Yeah. And I think a big thing for me is keeping the team together, keeping that motivation going. When you’re on set, the days are long and the months are long, and they all roll into each other. It becomes really challenging to keep that energy up.

And the same happens in retail. You have to keep those guys going, and you have to really try your best to keep the smiles up, keep the energy up and keep the motivation there.

Ruan Botha: What Lu-ise taught me about all of that is that, especially in theatre, when it’s your opening weekend, the energy is high. Things are going well, and you’re running on this adrenaline rush.

But the first performance can’t be different from the last performance. The people who paid the same price for the ticket go to the closing performance, and that still has to deliver the same excitement to the audience that the opening show did.

And it’s exactly the same with retail, right? You need to…

Lu-ise Hattingh: …A Monday, Tuesday and Saturday have to be the same quality of experience, especially since we’re in experiential retail and not just, you know, your standard.

The Finance Ghost: So Lu-ise, I won’t comment on that self-deprecation there and your chances of being an actress. You’re lucky that we don’t use the video, or everyone would know you’re lying, which I’m sure people would agree with. Certainly Ruan would, definitely!

But what I will comment on is that it’s just such an interesting combination of skills, which is really cool. And I guess that starts to tell us a little bit about how you split what you actually do in the business, what you each focus on.

And that leads into the next thing I wanted to ask you, which is: any tips you might have for these husband-and-wife teams out there (or romantic partners, obviously)?

Before you answer that, one of the podcasts in this series was with Hugh Cunningham. He’s got a pharmacy, The Local Choice – a franchise that he runs with his wife, Yolandi. It was only Hugh on that particular podcast, but he had some really interesting advice there. So, I’m keen to hear your advice and then compare what it’s like versus his, for example.

And anyone in that position, go and listen to the Hugh Cunningham podcast as well. You’ll get two different perspectives, two very different generational views as well. They are quite a lot older than the two of you, so it’s interesting to get their opinions versus yours.

So, hit us with the husband and wife pro tips for being in business together and thriving, not just in the business, but also in your relationship, because that is obviously very important.

Lu-ise Hattingh: I think communication. That’s a boring answer, but communication is just so important. You have to choose your lane, as well, and choose your kind of department. Stick to that, but then also bring each other on the journey. So, communicate with each other across departments, don’t silo yourself into just what you’re busy with. Because if you’re just both going to be on your own journey, you might end up in completely different places.

Ruan Botha: Yeah, I think that’s a very good answer – well. I should think that’s a good answer…

Lu-ise Hattingh: That’s our answer! [laughing]

Ruan Botha: …I should think it’s a good answer. [laughing]

The Finance Ghost: Very diplomatic, Ruan. Very well done. I see no disagreement here.

Ruan Botha: But to echo what Lu mentioned – play to your strengths. I know that what Lu can do, I can’t perform on that level. And hopefully there are a few things that Lu feels like, “Okay, let me rather leave that to Ruan to do.”

She mentioned bringing each other on the journey because the one hand needs to know what the other hand is doing. And that sounds maybe a little bit obvious, but I think the benefit of starting a business or running a business with your life partner is that there’s no one you trust more. So it’s easy to kind of just go, “Listen, I know what Lu’s doing. She’s making decisions that are the best for us as a whole and for the business.” But then, unfortunately, what could happen is that at some point, you might feel a little bit out of the loop and then start doing double work instead of really dividing the tasks and…

Lu-ise Hattingh: Divide and conquer!

Ruan Botha: …divide and conquer, yeah! So I think that’s very important. And it’s very difficult to, after a long day, come home and switch off and be husband and wife, but also, at the same time, you’ve got the business that you’re worried about and thinking about and that you need to problem-solve.

So I think it’s also important to set aside time to be like, “Okay, no shop talk here. We just relax and chat about whatever we feel passionate about.”

Lu-ise Hattingh: But also, that said, we love what we do so much, so it’s really hard to leave it at the door and go, “This is date night, only.” Because we’re just so excited about the projects that we’re doing, and we want to talk about it. It’s what’s going on in our lives at the moment.

So, I wish I could say that we’re really strict about it and we have these rules, “no shop talk at date night”, but it’s hard. And we’ve kind of decided not to be too hard on ourselves if that does spill over, because we just enjoy it. It lights us up. And we enjoy riffing on each other and going like, “Yes, that’s a good idea. Oh, you know, we should do this, we should do that.”

At the moment, it’s what excites us, so we go with the flow.

Ruan Botha: Yeah, I think that’s quite unique to our case specifically. Because Lu and I are optimists, and we’re both dreamers. So I think that dreaming part, and thinking about how we can improve or what new ventures or opportunities await – that’s also what drew us together from the start. It’s that we share that passion, and we infect each other with that excitement.

The Finance Ghost: Look, you have to be an optimist. You absolutely have to be an optimist. It’s such a cool thing to have brought up because you have to be a dreamer, you have to be so bonkers, to believe in what you’re building.

And we’ll get to that shortly, but one of my favourite concepts – and people have said this to me before – it basically goes along the lines of, “Pessimists sound really clever. They can point out all the stuff that could go wrong. But optimists build the world around them and figure it out as they go.” And somewhere in the middle is probably a sensible way to go through life. I guess that would be a realist? I don’t know.

But if you’re not more on the optimistic side of things, then you are definitely not going to build a business. So, I think the fact that you guys share that is such a big part of it. You’ve both got to believe, all the time. You just have to!

Perseverance is the first moat in any business. If you stop believing, everyone stops believing. That’s just how this game works.

Lu-ise Hattingh: I want to just quickly share a really cute story on something that happened today. So, today was a big day for setting up the shelves in the shop (and that is really freaking complicated – someone should make shelves that aren’t so complicated to set up!). And we were figuring this out and building the shelves, and one moment, Ruan was just really over it.

He looked at me and he was like, “Honestly, they should really put something on the box or say like, ‘This is not recommended to set up with anyone other than the person you’re preparing to spend your life with.’” I was like, “That is so true!” And also, the same goes for setting up four shops in one year.

The Finance Ghost: Yeah, 100%. You may as well go through it together, right? So let’s talk about these shops. Let’s talk about the business. You’ve given us some wonderful insights into who you are as people. Such an interesting couple, loads of passion. You’ve done a lot of cool stuff, you’ve travelled.

It’s amazing how often travel creates a lot of thinking around businesses. I always encourage people – if you can travel in your early life, do it. You don’t have to stay in fancy places, you just need to go and immerse yourself in cultures that are so different to yours. You’ll learn a ton and you’ll come back with ideas you never dreamed that you would have.

And that idea, for you guys at least, is to be involved with Market Kokoro. So let’s understand what that thing is really. If I go onto the Market Kokoro website, it talks about being ‘South Africa’s online Asian grocery store’. You talked about getting your hands very dirty today, fighting with shelving, so clearly it’s an omnichannel model.

And I think that talks to your specific involvement with this business in South Africa, because you didn’t start Market Kokoro in South Africa. It’s more that you’ve spotted an opportunity to build out a franchise footprint of these stores, and to really work with the broader group in actually developing the business at the end of the day – in the Western Cape specifically, although you do have a store in Joburg as well. I actually saw in the press today that there’s a nice deal with Pick n Pay now from a head-office perspective at Market Kokoro. So, very interesting stuff is happening there.

If you could just walk us through firstly, Market Kokoro South Africa (which is not you guys specifically), and then the franchise strategy (the piece that you are building) and how you got involved with this thing.

Ruan Botha: Basically, Market Kokoro Corporate was started by a Korean family in the late ’80s, early ’90s, I believe. They grew to five or six corporate-owned shops and then identified franchising as a viable way of growing their footprint. And that’s where we came in.

We, through our professional network, knew the franchisor quite well, and we’d worked with them in different capacities. Then, when this franchise opportunity presented itself, we said, “You know what? Let’s give it a shot.” Because it’s something that we feel passionate about, and the brand is such a vibrant brand that, again, we got excited about it.

And I think so many other people get excited about Market Kokoro. It’s not just a stale offering. It’s a surprising offering. Customers who visit us walk into a shop or a store and they’re like, “Wow, I want to come back here.” They want to spend time there. And that’s quite unique, right?

Usually for South Africans, the retail experience is, “I’m in and I’m out. I hope the queue is not too long. Where’s the cashier that’s available? Can I pay for 20 items at the money market without anyone complaining? Can I just get out?” Where Market Kokoro as a brand has created an environment that’s way more experiential. Obviously, it’s not just built on experience, but the experience part adds to what we do.

Lu-ise Hattingh: And, just to add to that, that’s what we brought to it. The experience part, and applying what we learned from our travels into how to change it from being a store to an experience. And adding selfie opportunities, adding touchpoints for customers to do more in the shop than just buy a couple of groceries.

Ruan Botha: So our first store, we opened a year ago – Market Kokoro Linden. And the big thing that we introduced there is instant ramen cookers. So basically, you can buy your instant ramen, and then we’ve got these noodle cookers that you can prepare it and make it yourself. And that just blew up massively. Because it brings that experience to it, it’s something – in today’s age, most consumers have got a gateway to the world through their phones. They might never have been to Asia, they might never set foot in Asia, but at least they can see what’s going on in Asia. And if they see something cool going on there, they want to experience it.

Now, not many people are going to get on a plane and fly to Korea or Japan to go and cook instant noodles, so I think it’s a unique opportunity for us to bring that little bit of Asia to South Africa.

So, we opened the store in Linden in August 2024, and then Sea Point, December 2024. Then we’ve got a store in Worcester, and now we’re building the Western Cape flagship in Belleville. And the franchise – there’s a different franchisee in Durban, and then there’s about seven or so corporate-owned stores in Gauteng.

I think the focus for us in this whole experience, as you mentioned – it’s omnichannel. You can buy a lot of things online, but because there’s such a big experience part tied to it as well, people still do want to experience the in-store experience. And that, at the end of the day, is also something very important to us.

Obviously, Asian food has been popping off tremendously over the last couple of years. I think if you go back ten years and you try to sell miso to someone, they’d be like, “What the hell is miso?” Now, the consumer is a little bit more educated. But at the same time, we’ve got to meet the consumer where they are. And that’s also why our footprint is so important. It’s blowing up, but it’s still very much a niche, I would say.

And also, people still have the perception that if they buy Asian ingredients, they’ve got to cook Asian food, whereas there are a lot of Asian ingredients you can easily incorporate into your South African cooking and just add that little kick. Not necessarily spicy, but just putting it on another level.

I think a low-hanging-fruit example is Kewpie mayonnaise versus a regular mayonnaise. If you’ve tried Kewpie or sushi mayonnaise…

Lu-ise Hattingh: You’ll never go back.

Ruan Botha: …it’ll be very difficult to go back to regular mayonnaise.

The Finance Ghost: As a sushi fan, I’ve got to say that makes absolute sense.

Ruan Botha: Yeah, so I think the thing in Japan, and Korea as well, they’ve got a big convenience-store culture where they meet the consumer, where the consumers are. Now, even though we’re not on a convenience store level, we need to think, “Okay, where can we position ourselves that’s easily accessible to different consumer bases, so to speak?”

And then, yeah, working with Pick n Pay and working with head office, I think Market Kokoro as a brand is firmly behind the idea that ‘a rising tide raises all ships’. And that’s something that also resonates deeply with Lu and me because, like we said, we’re optimists and we want to believe that a blue ocean strategy can be applied to the benefit of multiple stakeholders.

So that’s kind of the approach that we have. We’ve got the corporate-owned stores, we’ve got the number of franchises that we run. And, because we’re a new franchise, it’s an exciting dynamic between tried-and-tested knowledge, and a lot of product knowledge and experience, and then…

Lu-ise Hattingh: Unknown waters!

Ruan Botha: …and then the unknown waters, but also a fresh energy and the experience of living in Japan and in Asia for a bit, that we can also bring back and say, “Hey, how about we present it in this way that can make it interesting and maybe more accessible to local consumers?”

Because also, just to end that off real quick, the majority of our consumers are South African. We’re not targeting the Asian community in South Africa. We are very much backed by South African consumers who love our brand and who support us on a daily basis.

The Finance Ghost: I had a look at the Google reviews, by the way, for your Sea Point store, and it certainly suggests that people are very stoked to go and buy their noodles, cook them on site. So if you’ve got one of these stores near you, if you live in Joburg or Cape Town or even Worcester – I was mildly surprised to learn that, pretty exciting for the humble town of Worcester – go and check this stuff out. Go give it a try. It does sound pretty good.

It’s also quite a rapid expansion, so I guess my business brain immediately wonders. Is this something that the two of you are doing full-time? Are you having to side hustle to actually make it work, or is it able to support you at the moment? Because obviously that’s one of the big challenges for entrepreneurs, especially in the early stages.

Lu-ise Hattingh: So we both are consultants in our own capacity. I still consult with businesses, small businesses, founders growing their businesses, mostly based in the UK. I spend 80% of my time on my consulting and only 20% on Market Kokoro. But that 20% doesn’t include the weekends and the after-work 6pm to 10pm.

The Finance Ghost: Yeah, I was going to say there’s no way it’s 20%. It’s impossible. I refuse to believe it. Ruan, what’s your split – your real split? This is like that David Beckham meme from Netflix where he pokes his head in at Posh Spice and just says, “Be honest, Victoria, be honest.” So, give us the real number here, Ruan, not this 20% nonsense.

Ruan Botha: I think, yeah, I spend the majority of my time. So, as you mentioned, I also consult. My consulting portfolio is much smaller, so I don’t have to spend as much time, fortunately. I would say I’m the opposite of Lu. I spend about 80% of my time on Market Kokoro and maybe 20% consulting. But yeah, these are our babies, so we need to nurse them and give them the attention they are due.

But I think also, not to just shamelessly plug Capitec, but that’s also where they’ve been very supportive in their offering and being able to work with them. And then the business, obviously expanding very rapidly. But at the same time, I do also want to give a shout-out to our customers and our loyal clients who pull up to our opening events and stay the course in supporting us.

The Finance Ghost: Yeah, absolutely. I don’t know if you guys have read Shoe Dog, the story of Nike. If you haven’t, then you should. You’re both nodding, so you have read it.

So what I love most about it… Because I hate the whole ‘success-porn’ movement. It’s like, “Oh, I’m here on a yacht, and I worked three hours today, and now I’m unbelievably wealthy. And you can do it too, just buy my course.” It’s the absolute worst. Anyone who has built anything of actual substance knows this is a lie.

And I honestly recommend that if you are starting a business, then lock in other sources of income if you can. If it’s a bit of consulting, it really helps. You’re dreaming if you think you’re going to start a business, work 8 to 5, and pay your salary month one guaranteed. Unless you have very low overheads, that is a huge, huge risk. So I would not recommend doing that.

I mean, I’m five years deep in my business. I can tell you I’m still doing 80-hour weeks. It’s no better than my investment banking days, to be honest. It’s probably at least as bad. It just is what it is. The weekends mesh into weekdays and evenings, and it is simply just a tough thing.

And it gets much harder when you have kids, and you have to really try and then make time for everything. Kids are the ultimate startup. They definitely take a lot more than 20% of your time, that much I can tell you.

But I think the way the two of you are doing it is great, which is to build out this thing and then make sure that you can actually allow the business to stand on its feet without having to necessarily rely on it too soon, because too many businesses die that way.

And that brings me back to Shoe Dog, because Phil Knight, who started Nike, continued to work as an accountant, I think it was, for quite some time while he was literally selling shoes out the back of his car. That part of the story is amazing for me, and it’s true. And the one thing I love about that book is he’s just so honest, where he says that if he hadn’t done it that way around, it would probably have failed.

So in America today, that startup culture is very much around raising money, doing it with someone else’s money, writing some cool blogs about failure and success. We don’t have that startup culture in South Africa. It just doesn’t exist. You’re probably going to have to bootstrap. If you’re lucky, a bank like Capitec (and they are very good with this) will support what you’re doing. They might give you some of the finance to roll this thing out. But generally speaking, it’s quite hard to get that in South Africa. So you’ve got to hustle and you’ve got to give yourself some runway.

Ruan Botha: 100%. Just to echo what you were saying earlier, we kind of, especially with social media, right, we get quite enamoured or blindsided by the overnight success that’s been 10 years in the making. It just looks nice. “Oh, start your own business, and then you can work three hours and just chill.” But friends of ours mentioned that as soon as you start your own business, you switch your 9 to 6 (or 9 to 5, or whatever it is) to a 24/7. It’s just continuous.

The Finance Ghost: The plus side, of course, is that you get control over your time. So I will say, if anyone’s listening to this and going, “Oh, my goodness, I’m not going to start a business now.” What is amazing is the amount of control you do actually have over your time. It’s a big win. You’re choosing when you work as opposed to someone else choosing for you, which, for me at least, makes a really big difference.

Not everyone cares about it as much as I do. And that’s why not everyone should be an entrepreneur. I genuinely don’t believe entrepreneurship can be taught. It’s not for everyone. I think you can learn some underlying skills that you can apply to a business, and the two of you have proof of that – film and hospitality meets legal. But bring those skills together and, if you define those skills properly and broadly enough, then you understand how they actually relate to a business and what you really learned along the way, which I think is just fantastic.

So, something I wanted to ask you, given that you’ve now got stores in both Cape Town and Joburg, what are some of the differences that you’ve observed between the two cities? Other than the quality of the pavement outside and how often the grass gets cut, obviously. But what are some of the other differences in the retail environment for Cape Town vs Joburg?

Lu-ise Hattingh: It’s quite a different consumer. We’ve kind of established or spoken about this quite a lot and realised that it’s more the older consumer that’s so different, and then the younger consumer (because they have access through their phone to similar things), they tend to kind of ‘magnet’ towards the same kind of things.

So, some differences that we’ve noticed are that in Cape Town, you compete with not only other restaurants or other retail opportunities, but you compete with tourist attractions. Because a lot of our customers, in Sea Point especially, are tourists.

The Finance Ghost: Yeah, I was about to joke and say, “You’re competing with the ocean.” And then I thought, “No,maybe I shouldn’t say that.” But actually, it’s right. You are. You’re competing with the mountain and the penguins.

Ruan Botha: Yeah, 100%. There’s a whole host of things that you can go and enjoy, experiences that you can go on, that are on your doorstep. Why go to a retail store in Sea Point, you know? So, you are not necessarily competing with other Asian grocery stores or small restaurants or anything. You’re competing with, like you said, the ocean. The mountain.

Lu-ise Hattingh: Something that is also interesting between Joburg and Cape Town is that Joburg has a more captive audience. So they also don’t mind driving a little bit to get to your shop. Just like Capetonians don’t mind driving to a wine farm over the weekend, Joburgers don’t mind driving 40, 50 minutes, maybe even an hour to a retail shop for that experience. So, you have more of a captive audience.

The Finance Ghost: Yeah, this just blows the minds of Capetonians. So I grew up in Joburg, I lived there for 27 years or whatever it was, and in Cape Town for the past decade. And it’s just mind-blowing how different these cities are. And that is one of the single biggest differences. You’re absolutely right.

And I think it’s because of the road network. You can get from one side of Joburg to the other in like 30 minutes. In Cape Town, you could barely get from Milnerton into the city in 30 minutes, because there’s an ocean and a mountain and not enough roads and too many people. So, it really is a factor. It’s actually a big, big factor.

Lu-ise Hattingh: In Joburg it’s almost like a ‘build it and they will come’. Whereas in Cape Town, it’s…you have to take it to the people. And that’s especially what we realised with our Sea Point store. Someone from Durbanville does not want to drive all the way to Sea Point, especially not when there’s a rugby game on at Green Point.

The Finance Ghost: And vice versa. Half the people in Sea Point think that Durbanville is in KZN because they’ve never driven any further than Newlands. It’s just a fact about the city. It blows my mind, but these really are the facts. Honestly.

Ruan Botha: Like you said, you take Joburg, you’ve got people commuting from Pretoria to Joburg on a daily basis. It’s a 40-minute or an hour’s drive. An hour out of Cape Town ,that’s on the other side of the mountain!

So yeah, I think the other thing where Cape Town is quite different to Joburg is that there’s quite a significant tourist contingent to Cape Town as opposed to Joburg. I think you’ve got a lot more digital nomads living in Cape Town than you do in Joburg.

Someone coming from a New York, or a Los Angeles, or a London, where you’ve been exposed to Asian products for a lot longer. They come and they live in South Africa or in Cape Town for six months or three months – they still want to buy those products. And that’s kind of where they figure into your store as well.

Where Joburg, you don’t necessarily get… Listen, I think Joburg as a tourist destination has got a lot to offer, or a lot to develop that they can offer. But the reality of the fact is people touch down, head to Kruger National or head to Cape Town from OR Tambo. So we don’t necessarily see a lot of tourist customers shopping in Joburg.

The Finance Ghost: As a retail business, you just have to recognise this stuff. That’s absolutely right. There’s no point in beating around the bush with it, it’s just the reality of the two cities. They are two different places, they attract very different clientele, and if you don’t adapt from one to the other, it’s almost guaranteed that you will fail.

It was very interesting in this podcast season. I also got to speak to Ricky Ruthenberg. He’s the co-founder and CEO of Bootlegger, obviously now a national brand in the coffee shop restaurant space. They actually started in Sea Point, then eventually built out in the Western Cape, and then went to Joburg. Then they had to deal with COVID – big disaster. They’ve gone back to Joburg subsequently, and they’ve made it a success. Big lessons learned along the way.

And it’s almost a different world, the two cities. He talks about how when they went to Joburg, they practically had to restart with the brand. They thought they’d go there and people would know it. And actually, everyone thought Bootlegger was a bottle store with the ‘S’ on the end. So they’ve got to teach people there’s no ‘S’ on the end, it’s a coffee shop.

It was a fascinating podcast episode. If anyone listening to this is really enjoying this concept of these consumer-facing retail businesses, go and check out that Bootlegger podcast as well, because I think you will really enjoy it.

Just one other thing around your regional focus. So I think you mentioned to me when we were chatting before this podcast that Wesgro has been quite a useful pillar of support for your ambitions down here in the Western Cape, which I found very interesting. Not super surprising because I have had engagement with Wesgro years ago, I must be honest.

And I’m keen to hear more details on that. What was your experience? Because other entrepreneurs listening to this might be keen to understand how Wesgro and similar organisations, if they can find them, might actually help them.

Lu-ise Hattingh: So as first-time business owners, we didn’t know what to do or where to go to be legal and do what we need to do. Of course, the franchise offers some guidance and some things that we need to do. But Wesgro – and the GGDA in Joburg – they were tremendously helpful in supporting us.

To provide us with what we needed to do, just guide us with all the compliance that we needed to have, all the certificates we needed to have. They’ve even helped us with advice on advertising and research. And they have a whole network of really kind and helpful people who have come across our path just because we connected with them and we reached out to them and asked them for help.

Ruan Botha: I think we were quite lucky. I met the Wesgro team through past endeavours, and same with the GGDA, we met them for a delegation we hosted in the past. But the crazy thing is, these guys are a significant resource that you can use. Not just a network that you can tap into, but they have good relations with the City of Cape Town, so they can get you answers to your questions real quick. They are very efficient and super helpful. They’re just a bunch of really helpful, very friendly people.

Lu-ise Hattingh: They helped us to expedite a lot of things that we needed. And it’s free!

Ruan Botha: Yeah, that’s the thing. The help that they provide is free. They might ask you a few things for their stats, like how many people you employ and things like that, to kind of gauge the economic impact.

But yeah, they’ve really helped to also just make us feel, it’s going to sound weird, but to kind of feel that we are surrounded by people who care about us without having any stake in the business. They just really want to see us succeed as well and have made their resources available to us. I think, when you’re starting a business, any help that you can get from a semi-government-related organisation is fantastic.

The Finance Ghost: Absolutely. And it’s their whole mandate, right? To promote growth in Cape Town. My engagement with them was over 10 years ago. It was actually really interesting. I approached them because I was quite keen to potentially go work there. It was right near the end of my investment banking days. I was looking for something that was more based in Cape Town and it just wasn’t the right fit for everyone involved, but I was super impressed with the engagement with them. Solid people. And it’s nice to hear stories like these. It really is very cool. So, well done.

And it just shows – the lesson is: if you reach out to people and you ask the question, the worst they can say is ‘no’. And the best that can happen is a whole lot of great stuff! So your upside versus your downside, that’s a great trade. The finance geek in me would take that trade every day, and I do suggest business owners do the same. Just ask the question, you’ve got nothing to lose, literally.

So we’ve talked a bit about experiential retail and how you’re building that out and how this thing is so different, and you’ve gotten involved in it, which is great. How your skills have come together, and the differences between these two big cities in South Africa, Cape Town and Joburg, and your experiences there. It’s been fascinating.

There is one other big trend underneath all this, which we haven’t gotten to yet. And it’s a nice place to start to bring this podcast home, because this is the concept of consumer product licensing. It’s something they do so well in Asia. And this Korean movement, this ‘K-wave’, as I’ve seen it described, it’s a big thing.

So it’s KPop Demon Hunters. It’s Squid Game. That was kind of the start of it for a lot of Western consumers. Netflix started bringing this Korean show to the world, and then they did KPop Demon Hunters, and everything just exploded. It became memes, all this stuff. It’s just gone from strength to strength.

There’s a lot of other stuff as well. There are tons of Japanese IPs that people have been familiar with for decades now. Loads of anime, Pokémon, Dragon Ball Z, etcetera. It’s a whole different world. People do enjoy that culture and everything it means.

So, what do you think the opportunity is in South Africa to then expose consumers to this? What can we learn from this consumer product licensing culture that they’ve built in Asia? This behemoth of an industry, where you’ll see products that sometimes make no sense to Western eyes.

Stuff like Crocs with all the funny little things on them – those are massive in Asia. And here it’s like, “Ooh, Crocs. It’s a bit weird that people wear them.” Sorry if I’m offending anyone, but, you know, they are Crocs. The number one way to not be offended about wearing Crocs is to not wear Crocs. Just kidding, let me stop there.

Let me let you talk about consumer product licensing and what you think that could actually look like in South Africa.

Lu-ise Hattingh: I’ll leave that to Ruan, because he’s the expert.

The Finance Ghost: And by ‘expert’, you mean geek. I know that you mean geek, here. [laughing]

Lu-ise Hattingh: [laughing]

Ruan Botha: That’s where everything starts, right? I think the interesting thing about consumer product licensing is it’s a win-win situation. If you do your homework on what brands could resonate well with your target consumer, you get to introduce or sell your product using someone else’s IP, right?

So, internationally known, let’s take Pokémon or KPop Demon Hunters. Everyone knows that. I’ve got a manufacturing plant manufacturing T-shirts in South Africa. I license that IP, I put it on my T-shirt, or I design some clothes, and then I sell it to a consumer. So, I get to leverage that global brand in a South African context. And that resonates quite strongly with me – supporting local manufacturing. So, how do you differentiate your white T-shirt from someone else’s white T-shirt imported from wherever? That could be a really strong differentiation point.

The thing that I think Asia does really well when it comes to consumer product licensing is that they recognise that the human experience is vast and diverse, and people interact with a variety of products and things on a daily basis. And if I’m a fan of a specific IP, I might want to buy that Croc Jibbitz or whatever it’s called, right? I want to have the opportunity to buy that, at the end of the day.

The Finance Ghost: Look at this guy pretending that he’s ‘not quite sure what it’s called’. You know, “Oh, whatever it’s called.” Meanwhile, back at the ranch, this man has a wall of Crocs and Jibbitz and KPop Demon Hunters and little Market Kokoro things that he puts on them. Come now, be honest. I’m gonna quote ol’ David Beckham back in here again.

Ruan Botha: [laughing] Yeah, so the thing is that at the same time they also know that, even though I’m wearing Crocs and those Jibbitz, I want to go out to eat somewhere. So why not then have some noodles with the brand on? Because that’s a way that they’re going to get my attention, and I’m going to buy that brand of noodles. Also just to be part of the craze for a bit, but if I’m a fan, you know, that’ll be something – and the product is good of course, that’s vital – I’ll return to it.

I think in the South African context, what’s been challenging for businesses – and that’s kind of where I find myself spending that 20% of my time that I’m not spending at Market Kokoro. I’m spending it on trying to develop the resources that businesses can use to make better decisions when it comes to (and better understanding) the anime consumer or the pop-culture consumer in South Africa.

The demand is there. If you go to Comic Con Africa or Comic Con Cape Town, your mind will be blown. Your eyes will open to the vibrant communities that support these different IPs that are asking for these products. But the industry has been quite disorganised for the longest time. You have someone doing something, you have someone else doing something else. Simba brought out the Tazos, back in the 2000s or whatever, with Dragon Ball Z and Pokémon…

The Finance Ghost: … Yeah, I remember that. Wow, that was a whack of nostalgia across the head.

Ruan Botha: Yeah, you’re welcome.

The Finance Ghost: Thank you. Yes, no, absolutely. Thank you.

Ruan Botha: You’re going to go dig through your flip file to see if you find any of…

The Finance Ghost: … I think my Tazos are long dead, but I certainly had them. I absolutely did have them.

Ruan Botha: Yeah. But the thing is – and this is where the blue ocean side of things comes into play as well – no information was ever shared, necessarily, on how well that promotion did for PepsiCo or Simba or whoever brought it in. But, as we go deeper and deeper into the information age, those resources become available, even though you need to go and dig for them a little bit.

But I had an interview with Burger King for Comic Con Africa earlier this year, and they did a promotion with Naruto and the whole executive marketing team said, “No way. Naruto? Do South Africans watch anime? I’ve got no idea what this thing is. Let’s be conservative.” They ordered 300,000 units for a month-long promotion – so that’s 300,000 toys, essentially. They sold out within the first two weeks of that promotion. In their whole team, there were only two people who said, “Listen, I’ll resign if you don’t bring this promotion to South Africa.” So, you know, that information is vital to prove a point to Burger King. To say, “Okay, listen. We need to bring something similar next year.”

But then, if you look at the box office in South Africa, everyone thinks cinemas are struggling; it’s a dying industry. Then we’ve got a release of Demon Slayer: Infinity Castle, which globally was a massive phenomenon. From my understanding, the local distributor thought they weren’t going to do too well. The movie grossed 9 million at the South African box office – $9 million, I believe. That’s the highest-grossing movie in South Africa. It out-grossed Superman, it out-grossed Fantastic Four – quite big names.

So I think that shows that there’s a focus on these Asian brands, and they’ve got a lot of marketing power behind them. So, why not use those brands to promote your products and to promote your offering? I think, like you said earlier, it’s kind of a no-brainer, right? If there’s some information that backs it up, it’s really worthwhile to try and explore that.

The Finance Ghost: And the stuff is big. The one thing that I found so interesting is when that AI model came out that was copying that Studio Ghibli-style animation, people were furious. They were not just slightly angry. I think a lot of creatives have obviously been jilted by AI, and a lot of creative people are quite into a lot of this anime-type stuff and that style of Eastern storytelling, I suppose. But wow, people were angry about that Studio Ghibli thing. Frankly, as they should be. It really is beyond me why so much investment in AI is about going after art, as opposed to actually genuinely making people more efficient. But that’s a discussion for an entirely separate podcast, which we certainly won’t get distracted by now.

So, Ruan, there’s obviously a lot of passion for this stuff. Lu-ise, you’ve been kind of dragged along into it, but I think there’s some passion there as well for it, which is very cool. I think that’s great. And the lesson in there is how important it is to be passionate about the thing you’re building, because you are going to throw so much time and energy and everything else at it.

I’ve got a couple more questions. We don’t have much time left at all. It’s been a nice long and juicy podcast. First one, you did mention Capitec earlier, but let’s just chat a little bit more about that. I think you’ve used them for franchise financing and a few other services, and to just help you grow the business. Been a bit of a lifeline, right? I’m not sure you would have been able to do it without them.

Lu-ise Hattingh: Absolutely. And they’ve been incredibly helpful, honestly. We’re not just saying this, but they have really been so helpful. We moved over to them quite recently actually, but they’ve really been helpful in setting up our…

Ruan Botha: Accounts.

Lu-ise Hattingh: …accounts, setting up our…

Ruan Botha: POS system.

Lu-ise Hattingh: Yes, and… You take over. [laughing]

Ruan Botha: I think the key thing from Capitec’s side is obviously they’ve got a very strong focus, especially Capitec Business. They’ve got a strong focus on the SME sector, and I think it’s no secret that the small-medium-micro-enterprise industry in a country plays a big role in the backbone of that country. If it’s strong and vibrant, the country is all the better for it, you know? It creates a lot of opportunities.

Lu-ise Hattingh: I think philosophically, we just really align with Capitec.

Ruan Botha: We’re really aligned, yeah. Which is maybe a la-di-da answer, but at the same time on a practical level, as bankers, they don’t feel like people sitting in an ivory tower, locked away, that you’ve got to phone a call centre. I think their target is to answer a call within like 5 seconds…?

Lu-ise Hattingh: 30 seconds, yeah.

Ruan Botha: …or 30 seconds? Like, It’s insane. And it’s just because they are so consumer-focused. And for a business where we need to be consumer-focused – where we need to focus on going to the customer and giving them what they want, when they want it – it’s great to…

Lu-ise Hattingh: That’s exactly what they’ve done for us.

Ruan Botha: It’s refreshing to have a bank provide that service to us. Helping us…like, I don’t have time to sit on a phone call waiting for hours to chat to someone to give me an answer. So, they feel part of the team, as opposed to just this grudge that I’ve got to go deal with someone at the nearest branch or whatever.

The Finance Ghost: So, I think that’s exactly why they resonate with entrepreneurs. Because they do obsess over their customers, honestly. The fact that they made this podcast possible really shows it.

And honestly, every single guest I’ve asked on this podcast series gives roughly the same answer, which kind of goes like this. “I’m on a Capitec podcast so I know it sounds like I’m going to say something that I kind of have to say right now,” but it actually comes across so sincerely, from every single one of them. Everyone says Capitec has been a great partner, and so it really is lovely to hear that.

Ruan, last question, and I’m aiming this at you because, as far as I know, it’s only you doing this (although if Lu-ise was in the background of these podcasts, she should tell me). But, such is your passion for a lot of these cultural elements and this content that you also have your own podcast.

What is it all about? Where can people find it? And perhaps most importantly, do you wear Crocs while you are recording it? That is a very important additional question.

Lu-ise Hattingh: He definitely wears Crocs while doing it! [laughing]

The Finance Ghost: Oh, no! Is it? I hope there’s no video then. I’m hoping it’s just audio.

Ruan Botha: No, luckily it’s just static imagery.

The Finance Ghost: There we go.

Ruan Botha: Listen, I wouldn’t be much of a fan if I didn’t wear the Crocs. I need to drink the Kool-Aid. Lu’s been a tremendous support because, you know, sometimes it’s like, “What are you doing?”

Yeah. The podcast is called the Not Just Anime Podcast. It started this year with eight episodes available. Half of the season is consumer-focused, and then the second half is more business-focused. And the idea is just to illuminate Japanese and Asian pop culture in South Africa, and to kind of provide people and potentially other businesses with some insights into how the fandom works, but also how the business side of things works when it comes to consumer product licensing and the pop culture content.

And Lu’s background in film has helped me, actually quite tremendously, because the podcast is hard, man. The Finance Ghost is wild. What you’ve achieved is very impressive, and a ton of respect for doing what you’re doing.

The Finance Ghost: Yeah, that’s very kind. Look, it is my business, and that’s the difference. I think for you, it’s adjacent to your business, but it’s also a passion project. So, I actually almost have more respect for that, because you’ve got to find the time, in and amongst everything else. Whereas my podcasting literally pays the bills, so in some respects it’s easier. My motivation is not just that I enjoy it, but also because I need to pay school fees. Whereas on your side, it is a bit different. Although I do really, really love what I do. I’m very lucky in that regard.

Ruan, Lu-ise, this has been such a fun chat. Thank you so much. I would certainly encourage listeners to go and check out Market Kokoro online. I’ve got to tell you, I’m pretty keen to go and have some noodles, either in Durbanville at this new store, or maybe in Sea Point. Or maybe you should just come and open one in Milnerton, then it’s nice and close to me at home. We can consult on locations, because I’ve lived in the area for about 10 years now. That would be quite fun.

But thank you so much for your time. Thank you to Capitec for making this podcast possible. And if you’ve got a craving for some Asian culture, especially Japanese, Korean, maybe some stuff you’ve never experienced before – go and check it out. Expand your horizons and your taste buds, because that is what being alive is all about, at the end of the day.

Ruan, Lu-ise, thank you so much for your time. It really has been lovely having you on the show.

Lu-ise Hattingh: Thank you so much. This has been so much fun.

Ruan Botha: Thank you, thank you! It was an awesome conversation. Thank you so much.

Fairvest invests deeper in township fibre (JSE: FTA)

This may sound very random for a REIT, but there’s a yield and an upliftment of areas in which Fairvest has properties

Fairvest has previously invested around R477 million in Onepath, a subsidiary of Fairvest that acquires fibre network infrastructure in townships and leases it to Fibertime Networks (US spelling for some reason). The claim to fame is that households can be connected on a pay-as-you-go model for just R5 a day, which is fantastic.

But why would a REIT do this? Well, there are two main reasons.

The first is that the investment actually generates returns, in this case an annualised yield of 14.9% from November 2024 to September 2025. There’s certainly nothing wrong with that, particularly as these are triple-net leases that put all the insurance and maintenance costs on Fibertime.

The second is that it gives Fairvest useful information about these communities, which in turn informs their decisions around township-adjacent retail properties. This is an important growth area in South Africa.

To further the strategy, they’ve committed to invest up to R1 billion in aggregate in Onepath i.e. they are roughly halfway there.

Personally, I think anything that brings connectivity to marginalised communities should be celebrated, especially if the financial returns also stack up.

Mantengu has commissioned Langpan’s second chrome processing plant (JSE: MTU)

This is good news to cap off the year

Mantengu’s share price hasn’t yet recovered from the nasty drop in response to the recent set of financials. The company has lots of work to do, but there’s some good news around Langpan to help improve the financial prospects of the company.

Mantengu has successfully commissioned the second chrome processing plant at Langpan Mining. Langpan has 300,000 tonnes of tailings that will be fed into the new plant, giving them roughly 10 months of feed to work with. It looks like the proceeds from processing this feed will then be used to ramp up mining operations, as they need to get to 60,000 tonnes per month of chrome ore feed in order to sustain two processing plants.

There’s a PGM strategy in here as well, as the tailings contain PGMs that haven’t been recognised on the balance sheet as of yet. The company has promised to give a subsequent update to the market regarding the PGM strategy.

Premier Group and RFG Holdings shareholders approve their deal (JSE: PMR | JSE: RFG)

Approval at both meetings was unanimous

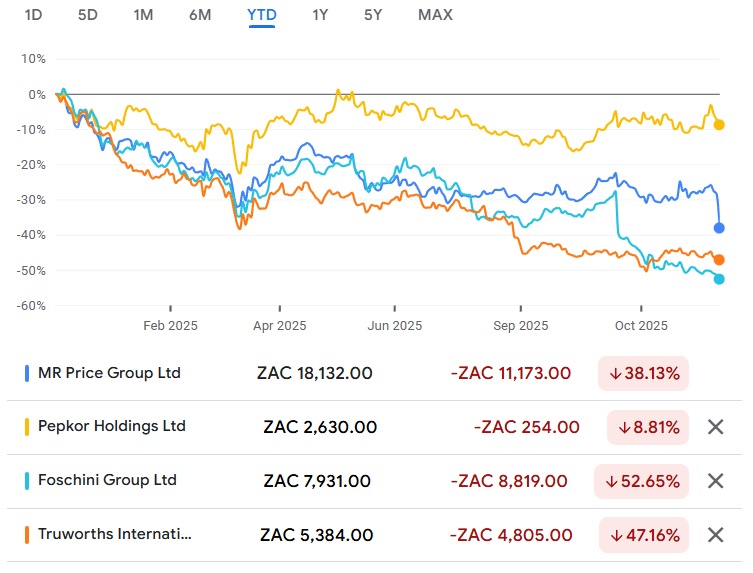

In a week in which Mr Price (JSE: MRP) showed us what a truly daft deal looks like, it’s worth reflecting on whether Premier Group and RFG Holdings are doing the right thing with their deal. As a reminder, Premier is acquiring RFG, but in reality it’s closer in spirit to a merger.

The market is comfortable with the transaction, as shown by the two share prices over the past few months:

For the sheer contrast of it, here’s what it looks like when the market is angry at a deal:

So, people aren’t overly worried about Premier’s acquisition of RFG Holdings. In fact, there’s bullish sentiment around it. I remain skeptical, as it’s not obvious to me that this deal is based on sensible underlying reasons for the companies to belong together. We have a private equity seller on one side and an acquirer on the other who can take advantage of relative earnings multiples to achieve an accretive deal. Accretive HEPS in the near-term doesn’t necessarily mean that the strategic fit over the next few years will work out as well as they hope.

Time will tell. The FMCG market is notorious for questionable deals. I hope we won’t see a situation where the combined group trades at a structurally lower multiple than before due to more erratic earnings and the difficulties investors will face in forecasting earnings. JSE investors are rewarding simplicity at the moment, not complexity.

Nibbles:

Director dealings:

A2 Investment Partners bought another R55 million worth of shares in Nampak (JSE: NPK). It comes through as a director dealing because they have representation on the board.

Adrian Gore sold Discovery (JSE: DSY) shares worth R50 million. He also entered into a put-call hedging structure, with puts at R229.28 and calls at R374.87. The current spot price is R227, so he’s protecting downside risk from these levels. The value of the hedge based on the put strike is a meaty R365 million.

Here’s a big disposal: a prescribed officer of Dis-Chem (JSE: DCP) – specifically Christopher Williams on the wholesale CJ Distribution side – sold shares worth R35 million. I’m glad they didn’t try to soften the messaging by talking about some kind of rebalancing.

The CFO of Lewis Group (JSE: LEW) sold shares worth over R1.3 million. The ol’ “portfolio rebalancing” rationale has struck again. A sale is a sale!

Acting through Titan Premier Investments, Christo Wiese bought shares in Brait (JSE: BAT) worth R608k.

The company secretary of Bidvest (JSE: BVT) sold shares worth R323k. Although the sale relates to a share price appreciation rights plan, the announcement isn’t explicit on whether this is only a taxable portion. I therefore assume that it isn’t.

Two directors of Spear REIT (JSE: SEA) bought shares worth R254k in aggregate.

A director of Afrimat (JSE: AFT) bought shares worth R84k.

The CEO of Vunani (JSE: VUN) bought shares worth R43k.

Astral Foods (JSE: ARL) announced the appointment of Johan Geel as CFO with effect from 1 March 2026. He will replace Dries Ferreira who has resigned as CFO. Johan’s most recent role was CFO at AFGRI Limited, so he has plenty of experience in the agriculture sector.

KAP (JSE: KAP) has implemented the category 2 disposal of Unitrans Swazi Holdings with an effective date of 1 December.

Supermarket Income REIT (JSE: SRI) confirmed that Fitch has reaffirmed the company’s existing investment grade rating on the debt (BBB+ with a stable outlook). For property companies, debt is part of their business model and so these ratings are critical.

The Conduit Capital (JSE: CND) mess is finally coming to an end, at least in the listed space. Having been suspended from trading for three years and with no meaningful ability to rectify the situation while they pursue various court processes, it’s time for this one to go. The JSE will delist the company on 19 December. If you’re unlucky enough to be stuck with shares in this thing, they will now be in an unlisted company.

Mr Price has entered into a transaction agreement to acquire 100% of European value retailer NKD from private equity parties Fliegendes Pferd Midco, a UK company holding 98.22% and Fliegendes Pferd MEP, a German general partner holding 1.78%. Mr Price will pay a base purchase price of €415 million (R8,23 billion) subject to a maximum of €487 million (R9,66 billion), which will be settled by way of cash and debt. The deal, a category 2 transaction, is expected to close during Q2 2026.

Capitec Bank is to acquire 100% of Walletdoc, a local fintech providing scalable, innovative payment gateway solutions for merchants, including online and in-app payments, digital wallets, Instant EFT, payment links and real-time payouts. For Capitec, the acquisition is strategic, reinforcing its ongoing commitment to lower the cost of payments, broaden access to digital financial services, and promote local financial inclusion. Capitec will pay up to R400 million for the business.

Aligned with the Group’s strategic direction to simplify its portfolio by sharpening its focus on priority categories with sustainable growth potential, Libstar has sold its fresh mushroom operations. It has however retained the Denny brand which it has licensed to the purchaser for the use in the fresh mushroom category and will continue to produce and market its value-added Denny branded products. Libstar expects to report a loss on sale before tax of its mushroom operations in the annual financial results for the year ended 31 December 2025 of between R45 million and R55 million.