Inflation is at 3%. The Reserve Bank wants to lock it there. Interest rates are edging down. But the bigger picture is far from settled:

Growth is stuck below 1%

US tariffs threaten trade and jobs

The rand’s strength rests on fragile global sentiment

Consumers are squeezed and government finances remain stretched

In this episode of No Ordinary Wednesday, Jeremy Maggs speaks to Investec Chief Economist Annabel Bishop about the shifting sands of macroeconomic policy, and what it means for business, households and markets.

Hosted by seasoned broadcaster, Jeremy Maggs, the No Ordinary Wednesday podcast unpacks the latest economic, business and political news in South Africa, with an all-star cast of investment and wealth managers, economists and financial planners from Investec. Listen in every second Wednesday for an in-depth look at what’s moving markets, shaping the economy, and changing the game for your wallet and your business.

Anglo American laughs off the sale of the steelmaking coal business to Peabody (JSE: AGL)

This avoids a long and expensive legal fight around the MAC terms

A MAC clause in a transaction is an important thing. It stands for Material Adverse Change and is a critical protection for the buyer, as it is effectively an escape clause if something goes wrong with the target asset during the time between the agreement and implementation of the deal. It’s rare to see it invoked in practice, but it does happen.

A perfect example is Anglo American’s attempted sale of its steelmaking coal business in Australia, which Peabody Energy agreed to buy in late 2024. An underground fire at the mine in March 2025 spooked Peabody and they invoked the MAC clause, arguing that this event gave them the ability to walk away from the deal. Based on the lack of damage to the mine and all the progress made in restarting the mine, Anglo American argued that this isn’t in fact a MAC. An AC perhaps, but not a MAC.

Sadly the arguments over the “M” (Material) can become really burdensome, particularly in vague legal agreements. Remember, the more vague the definition of a MAC, the more wriggle room the buyer of the asset has.

I suspect that the state of the coal market this year is also part of the decision. If Peabody really wanted the asset, they would’ve surely negotiated with Anglo and gone ahead with a deal. Instead, it’s a convenient escape clause that allows Peabody to be more cautious with its capital.

Rather than becoming embroiled in a long and expensive legal battle in which only the lawyers are the ultimate winners, Anglo American is giving up on the deal and focusing on the safe restart of the mine and the performance of the broader steelmaking coal portfolio. Having said that, they will be initiating an arbitration process to seek damages for wrongful termination, so that could get pretty interesting.

Anglo claims that they have received unsolicited inbound interest for the asset in recent months, which suggests that an alternative sales process could be on the table soon. Of course, the price is what really counts, with the coal market in a rough place this year and unlikely to support a strong price.

BHP’s headline earnings dipped in 2025 and remain well off 2023 levels (JSE: BHG)

If you want consistent growth, the mining industry isn’t for you

BHP’s share price is up 4% in the past 12 months, which is probably a fair reflection of the mixed bag that the commodities sector has been in the past year. This is the benefit of buying one of the diversified mining houses as opposed to one of the specialists that can have great years and awful years. The diversified names tend to have a smoother experience.

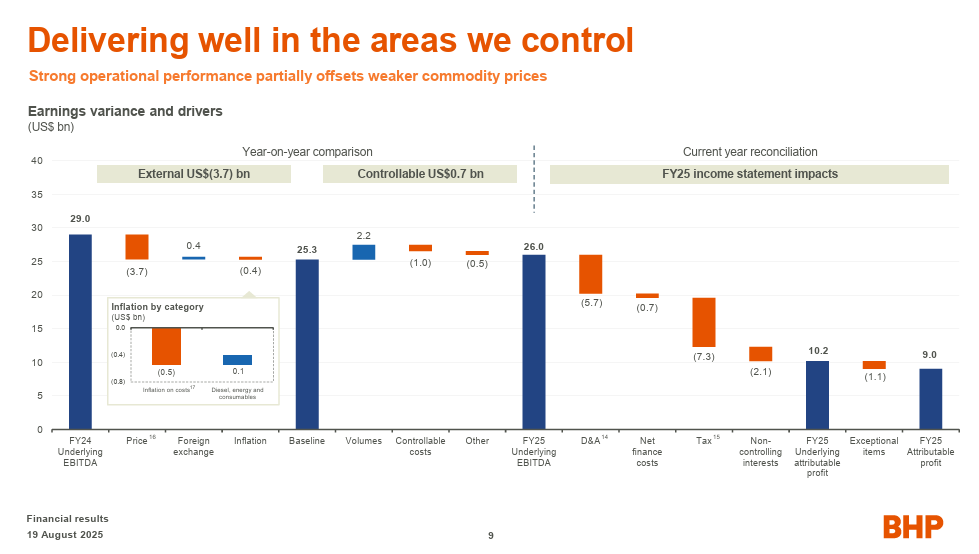

This doesn’t mean that earnings are smooth, though. In the year ended June 2025, HEPS fell by 6.9% (reported in USD). This puts HEPS at 182.4 US cents, which is way off the 2023 levels of 256.1 US cents. Even in the diversified names, you’ll see the cyclicality in the sector coming through.

I quite enjoyed this waterfall chart in the earnings presentation, which shows the split between “external” factors (like commodity prices and forex) and “controllable” factors (like production and operating costs):

The EBITDA margins vary substantially across the different commodities. For example, iron ore (with record production) was the star performer in this period, with EBITDA margin of 63%. Copper (another record) wasn’t far behind at 59%. Steelmaking coal was then some way off at 17% and energy coal firmly brought up the rear at 10%.

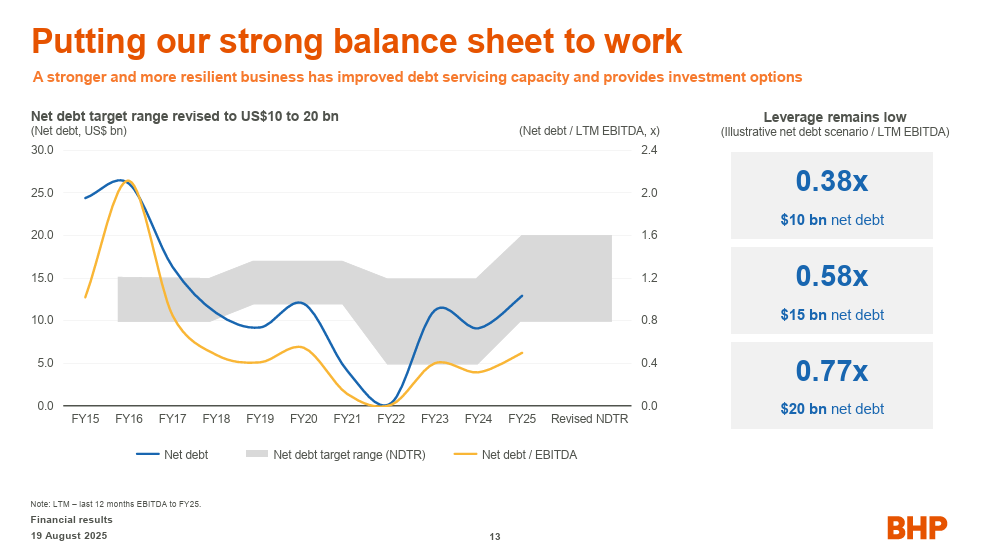

Here’s another great chart from the presentation that I think is helpful in understanding how the capital cycles work in mining, showing how the levels of debt change over time based on the extent of capex plans vs. the earnings in the business:

Aside from the obvious focus on copper, what BHP would really love to see is an uptick in global activity that would support higher iron ore prices. BHP is the world’s lowest-cost major iron ore producer, so they can literally print money when things go their way.

Deneb remains committed to selling properties (JSE: DNB)

Mobeni Industrial Park is on its way out – hopefully

Unless there is an exceptionally good reason for doing so, operating companies shouldn’t own properties. This is because property doesn’t have the same return profile (or risk) as commercial operations, so it’s better to separate the two and allow property investment companies to hold property and lease it to companies.

That’s the theory, anyway. There are many examples on the JSE of non-property companies holding large property portfolios, not all of which are for financially sound reasons.

The broader Hosken Consolidated Investments (JSE: HCI) group has been offloading property recently, which is good to see. Deneb is part of that, with a recent attempt to sell 195 Leicester Road in Durban in a deal that unfortunately fell through. Thankfully, they aren’t giving up.

The latest attempted sale is for Mobeni Industrial Park for R170 million, which makes it much bigger than the 195 Leicester Road deal which was only R48.5 million. I guess if only one of the two goes through, the bigger one is better!

Mobeni Industrial Park was valued at R170 million as at March 2025 and generated profit after tax of R11.5 million for that financial year. That’s a yield of just 6.8%, which shows you exactly why Deneb is much better off having R170 million on the corporate balance sheet and ready for investment in its own operations.

This is a Category 2 transaction, so shareholders won’t be asked to vote on it. Now we wait and see if the money actually materialises and the buyer completes the sale!

Dipula is buying Protea Gardens Mall in Soweto (JSE: DIB)

And a few other properties as well

There aren’t many pockets of growth in South Africa at the moment, but one of them is in township-adjacent and commuter-focused retail properties. Dipula Properties knows this, which is why they are happy to spend R478.1 million buying Protea Gardens Mall in Soweto.

Importantly, the mall boasts 70% occupancy by national tenants (i.e. large retail chains), so that’s a strong income underpin.

Instead of just giving us the latest financial performance of the mall, the announcement includes a forecast for the 9 months to August 2026 and then the 12 months to August 2027, as they assume that it will transfer during November 2025. This is frustrating disclosure.

Given the seasonality inherent in retail, I can’t see much use for the 9 month forecast. Using the 2027 12-month forecast, net property income is estimated to be R56.2 million. If we discount that for two years at 10% per year, that’s roughly R45.5 million in 2025 terms. This would be an acquisition yield of 9.5%, which feels a bit expensive to me. By the time you allow for debt, it’s likely that the distributable income of the mall will be below the dividend yield that Dipula’s shares are trading at (currently 8.7%).

Of course, if they actually disclosed the current level of net property income, I wouldn’t have to guess.

Dipula has hinted in its announcement that they may need to issue new shares to help fund the deal, although nothing is finalised at this stage. That’s perhaps something for retail shareholders to keep in mind, as such capital raising activity is usually in the form of an accelerated bookbuild that focuses only on institutional investors. Perhaps the company will surprise us here and give everyone a chance. Just to be clear on this – there’s no guarantee that any issue of shares for cash will take place.

But that’s not all folks – Dipula has also concluded a further R215.6 million in acquisitions that get a casual mention near the bottom of the announcement. The biggest individual one is Abland DC for R134.4 million, accompanied by the acquisition of Airborne Industrial Park for R63 million and marking a significant investment in logistics property around the airport in Joburg. They’ve also announced the acquisition of the Woolworths Gezina building for R16.2 million, along with land adjacent to the Tower Mall in Jouberton for R2 million.

Dipula has clearly been very busy. As the fund’s market cap is over R5 billion, the size of these acquisitions means that shareholder approval won’t be needed for any of them.

Harmony Gold can finalise the Mac Copper deal (JSE: HAR)

Harmony Cold? Harmony Gopper? Perhaps a better name is needed

Harmony Gold has ambitions to grow beyond what the name suggests. The allure of copper is so strong at the moment than even gold companies are keen to get in on the action, with Harmony acquiring MAC Copper in Australia in a deal that was announced back in May. The relevant update is that the Australian Foreign Investment Review Board (FIRB) has given the green light for the deal.

I can only assume that one of the conditions was to let them win a game of rugby. The timing is too suspicious.

There are a few remaining conditions to be met, not least of all shareholder approval 29 August.

Nibbles:

Director dealings:

After suffering a massive sell-off, the Bytes Technology (JSE: BYI) share price has recovered by 11% over the past 30 days and can now boast significant insider buying by various directors as part of the bullish thesis. The on-market purchases come to roughly R6.6 million in total.

An associate of the CEO of Acsion (JSE: ACS) bought shares worth R604k.

Des de Beer has bought R454k worth of shares in Lighthouse (JSE: LTE).

A director of Orion Minerals (JSE: ORN) participated in the company’s Share Purchase Plan to the value of A$6k (almost R70k).

The CEO of Vunani (JSE: VUN) bought shares worth R11.5k.

The chairman of Assura (JSE: AHR), Ed Smith, has notified the board that he is resigning as a director. As Assura might remain listed depending on the level of acceptances achieved in the Primary Health Properties (JSE: PHP) offer, the company has appointed senior non-executive director Jonathan Davies to take his place.

CAFCA (JSE: CAC) has almost zero liquidity in the stock. The cable manufacturing company operates in Zimbabwe and saw a 14% drop in sales volumes year-on-year. It looks like the mining sector was the culprit, with the construction and manufacturing sectors achieving growth to offset some of that pain. With three quarters out of the way, revenue is down 5% year-to-date and margins have also fallen.

Note: Ghost Bites is my journal of each day’s news on SENS. It reflects my own opinions and analysis and should only be one part of your research process. Nothing you read here is financial advice. E&OE.Disclaimer.

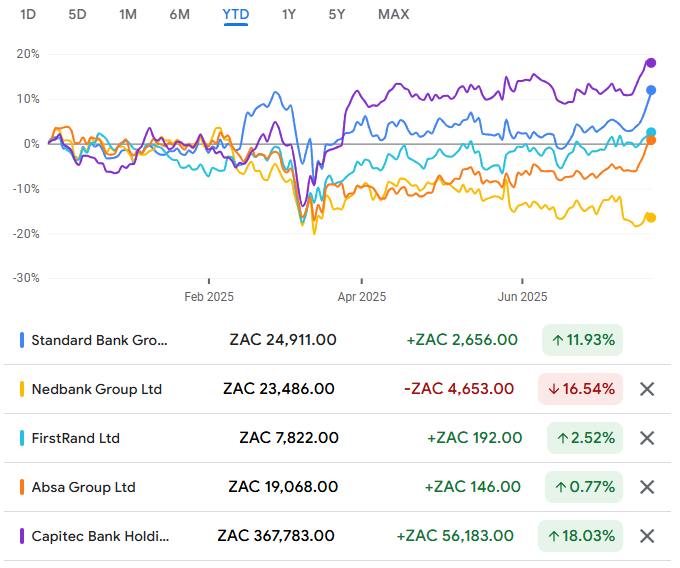

A much better credit loss ratio drove higher earnings at Absa (JSE: ABG)

This is how modest income growth led to 16.5% growth in HEPS

Absa’s results for the six months to June 2025 offer a fascinating way to learn about the drivers of banking earnings. The overall story looks great for investors, with the dividend up 14.6% thanks to a 16.5% jump in HEPS. Return on Equity – a key driver of bank valuations – increased from 14.0% to 14.5%.

And yet, net interest income (the core source of income for banks) increased by just 3%. What happened here?

Firstly, you need to understand that Absa finds itself in a situation where the decline in interest rates hasn’t driven a substantial increase in economic activity. Total loans and advances increased by 8%, but net interest margin contracted from 4.69% to 4.58%. That was enough to blunt the growth in net interest income to just 3%, as mentioned.

Then, you need to understand that although net interest income is the biggest source of income (R36.3 billion), they also have non-interest income at R20.2 billion. Thankfully, that was up 10% thanks to juicy underlying numbers like a 36% increase in net trading income. As non-interest income is far less capital hungry than net interest income, growth in this area is great news for return on equity.

The next critical point is that net interest income is measured before credit provisions. Absa’s credit loss ratio has improved sharply from 1.23% to 1.00%, which means the impairments charge in this period was 14% lower than in the prior year.

What does this mean in practice? Well, pre-provision income (including all sources of income) was up just 5.2%, whereas operating profit (after impairments) was up 8.6%. When you compare this to operating expenses growth of 6%, it shows you that the much-improved credit loss ratio helped Absa get on the right side of margin growth.

This tells us that although shareholders have something to smile about here, the reality is that Absa’s numbers were boosted by an increase in the credit loss ratio that won’t happen every year. Once the ratio is back within target range, impairments tend to move by a similar percentage to the overall book. Absa is less of a growth story right now and more of a recovery story, which is why the share price is actually flat year-to-date.

Another way to look at this is to take the segmental earnings, where there are wild swings in headline earnings that reflect how difficult things are in some of the underlying businesses. Focusing on the client-facing segments, Personal and Private Banking was up 23%, Business Banking fell 12%, Absa Regional Operations (rest of Africa) grew by a lovely 35% and Corporate and Investment Banking was up 10%. The rest of Africa did the heavy lifting in this period.

Aveng may need the Avengers at this rate (JSE: AEG)

And I’m talking about the superheroes, not the Covid-era shareholders they had

The pandemic delivered some pretty incredible cultural moments in the market, not least of all the self-styled “Avengers” on X (then Twitter) who were punting at Aveng. This was in the pre-share consolidation days, when Aveng was trading at literally a few cents a share – a genuine penny stock.

Sadly, after an 18.6% drop on Monday to take the year-to-date performance to a drop of 62%, the Aveng share price seems to miss its penny stock days and wants to get back down there as quickly as possible. It is now at R4.80 per share, way off the near-R30 levels it traded at after the consolidation.

This is unfortunately what happens when you swing from HEPS of R3.64 to a headline loss per share of -R7.44 for the year ended June, driven by huge losses in major projects like J108 and Kidston. This is precisely why I avoid the construction industry completely: just one or two projects need to go wrong and earnings get obliterated.

Silver linings? Well, there was still a free cash inflow of R257 million, so there’s that. The net cash position actually improved from R2.1 billion to R2.5 billion. They’ve also come into the new financial year with higher work in hand of R37.5 billion (up slightly from R37.2 billion).

In case you’re wondering, it’s the Australian Infrastructure business that is breaking the income statement. I wish someone had the time to do the research on just how many South African listed companies have been given an Ellis Park-level drubbing by the Australian market. For whatever reason, the business environment there is even more frightening than the spiders.

The other two major segments (Built Environs and Mining) both reported improved operating earnings. Before you get too excited, there’s an “Aveng Legacy” book of problematic non-core assets that contributed a significant operating loss.

Aveng’s corporate strategy is to split the group in two, which means the sale of Moolmans (the local Mining segment). They have made “significant progress with a preferred party” on that sale. This would leave them with the businesses in Australasia and Southeast Asia, which is like being left with your least favourite family member on a three-day hiking trip with no access to cellphones. You may survive, but it won’t be fun.

CA Sales flags high-teens growth (JSE: CAA)

The impressive growth story continues

Although there are some worries in the market around the risks to the Botswana economy from the collapse in the diamond market and what this might mean for the likes of CA Sales Holdings with significant exposure to that country, there’s no indication at this stage that growth is suffering. Quite the opposite, in fact, with the company releasing an encouraging trading statement.

For the six months to June 2025, CA Sales expects HEPS to increase by between 14% and 19%. As is the norm for the group, the growth is coming from a mix of organic sources (i.e. existing businesses they already owned) and the integration of new businesses that they’ve acquired (bolt-on acquisitions are core to the growth plan).

Detailed results are due for release on 1 September.

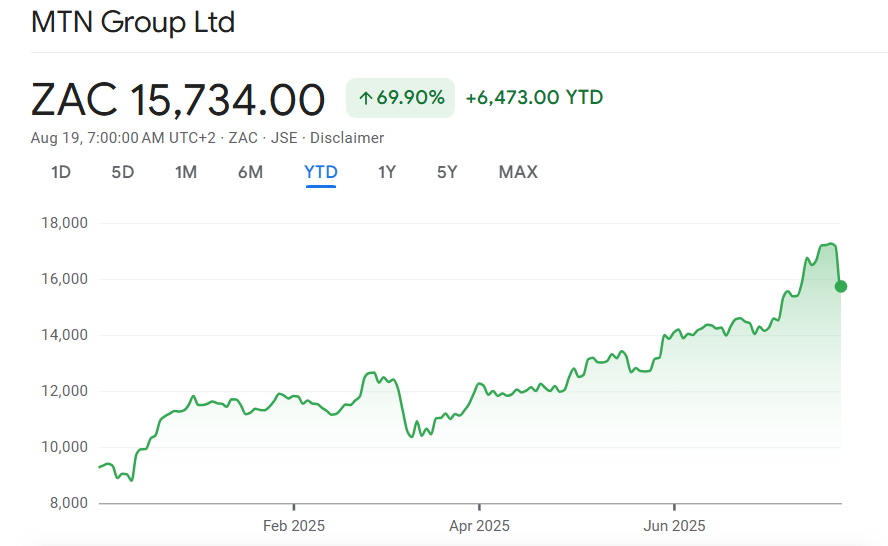

MTN released incredible overall numbers – yet the share price closed over 8% lower (JSE: MTN)

The likely reason for this is very close to home

MTN saw a monumental improvement in its overall business in the six months to June 2025. Driven by the results in the rest of Africa, group service revenue was up 23.2% as reported, or 22.4% in constant currency – and it’s lovely to see such a small difference between those numbers, as currencies in Africa stabilised recently thanks to dollar weakness and other factors.

When it comes to EBITDA, the jump was 60.6% as reported or 42.3% in constant currency. The gap is much larger there, but both those growth rates are fantastic. EBITDA margin was 42.7% as reported or 44.2% in constant currency.

The growth rate in HEPS was a bit daft really, up 352%. It’s easier to understand this as a swing from negative to positive, with a headline loss per share of -256 cents in the prior period and positive HEPS of 645 cents in this period.

As the icing on the cake, MTN upgraded its medium-term guidance to reflect group service revenue growth of “at least high-teens” vs. the previous level that reflected mid-teens.

It’s almost easy to forget a time when MTN was focusing on its balance sheet metrics rather than revenue growth, with huge challenges in getting the cash from the African subsidiaries to the mothership. Thankfully, those problems are largely behind them, with Holdco net debt to EBITDA at 1.5x (stable vs. 1.4x as at December 2024) and group net debt to EBITDA at just 0.5x. Non-rand debt at Holdco level was 17%, well below their upper limit of 40%.

Free cash flow conversion remains a challenge in this sector, as the large companies need to invest a fortune in their networks. Although reported EBITDA was a meaty R46.6 billion, free cash flow was just R6.7 billion. Aside from interest and tax payments, R22 billion in capex is the major reason for that gap.

In South Africa, service revenue growth was just 2.3%. It won’t surprise you that voice was down 2.2%, while data was up 4.3%. Despite a substantial drop in cost of sales, the South African business saw EBITDA fall by 3.6%. This could be why the market reacted negatively to the news, as South Africa is meant to be the steady anchor for the group. There’s also surely an element of profit-taking in the market here, as MTN has been on an incredible run and investors often get jittery in the search for a reason to exit.

In a separate announcement, MTN noted a restructuring of its group into three platforms: Connectivity, Fintech and Digital Infrastructure. There is plenty of reshuffling of chairs at Exco level to make this happen, including a new CEO in South Africa.

Here’s what Monday’s profit-taking exercise looks like on the chart:

For traders, this chart needs to come down and test moving averages that haven’t had a chance yet to catch up to the recent rally. I suspect that MTN is therefore firmly on the watchlist for punters!

Northam Platinum’s recent numbers reflect how rough things got in the PGM space (JSE: NPH)

The rally in share prices in the sector this year has been firmly forward-looking

Although the PGM sector has dished up some massive share price returns in 2025, you certainly won’t find the reason for this in the earnings over the past year or so. Across the board, earnings in the sector have been rough, with everyone looking ahead to hopefully better times thanks to higher PGM basket prices.

Northam Platinum is another perfect example of this, with a 6.9% increase in sales revenue for the year ended June 2025 and an 8.1% increase in the cash cost per ounce. The revenue increase thus wasn’t enough to offset mining inflation, leading to a 25.5% decrease in operating profit.

By the time we reach HEPS, Northam Platinum expects a drop of between 9.4% and 19.4%.

If we dig a bit deeper, the Eland mine is clearly the culprit. The cash cost per ounce jumped by 17.2%. To make matters worse, it was already the least efficient mine in the group, so the cash cost per 4E ounce is now up at R40,562. Compare this to Zondereinde (R26,758) and especially Booysendal (R18,502) and you can see the problem. For reference, the revenue per refined 4E ounce was R32,690, so Eland must have been heavily loss making in this period.

Importantly, Northam expects costs at Eland to normalise over the next two years, with the performance in this period attributed to safety interventions that limited production (even though total production was still up). Either way, the numbers are disappointing for shareholders.

For all the exuberance in the sector, Northam’s outlook statement includes plenty of sobering commentary and a reminder of how cyclical this market is. The share price is up 122% year-to-date, with the market piling into the sector regardless of the risks.

Orion Minerals raised roughly half of the planned amount under the Share Purchase Plan (JSE: ORN)

Under the circumstances, that’s pretty good

Sadly, when companies need to raise equity capital, the default setting is to work through brokers and advisors who bring large institutional investors to the table. This leads to a quick capital raising process that achieves the objectives of the company, but that also tends to shut out retail investors who aren’t given the opportunity to participate.

Full credit goes to Orion Minerals here: they are one of the few companies that give retail investors a fair chance to get involved. The share price has had a rough time this year (down 28% year-to-date), so I was curious to see how the latest Share Purchase Plan would turn out in terms of investor appetite. This was especially the case after the recent Unlock the Stock event with the company, in which retail investors peppered the management team with questions. Getting a wide range of investors onto the shareholder register can be a double-edged sword!

It looks like there’s still strong support from investors, with Orion managing to raise R22.2 million under this initiative. They initially targeted up to R46 million, but that was always going to be a long shot. Encouragingly, they raised R20.6 million from South African investors, so the overwhelming majority of the support came from investors who are close to where the assets are: right here in SA.

Thungela’s profits plummeted, but they’ve maintained the dividend (JSE: TGA)

In fact, the payout ratio for the period is more than 100%!

Things haven’t been pretty in the coal market. Thungela’s revenue fell by 12% for the six months to June 2024, which was enough to drive a rather hideous 80% drop in HEPS. Welcome to cyclical mining companies, particularly those with single-commodity exposure rather than a diversified basket.

Despite HEPS dropping from 952 to 192 cents, Thungela has maintained the dividend at 200 cents per share. This means that they are now paying out more than they earned for this interim period, which is an unusual situation. They would sooner sell their first-born children at Thungela than cut the dividend.

Tempting as it may be to point to the 21% drop in capital expenditure as the reason for the maintenance of the dividend, the reality is that adjusted operating free cash flow fell by 48%. Sure, the capital expenditure decrease helped blunt some of the impact of lower earnings, but there’s still a huge year-on-year drop here that isn’t reflected in the dividend.

The outlook for the second half of the year isn’t exactly bullish, with Thungela referencing risks to the coal price from global economic growth. Much will depend on the restocking activities in the Northern Hemisphere, along with levels of global production and how the supply – demand dynamic plays out.

Not only has Thungela maintained the dividend, but they’ve also approved another share buyback programme. With the share price down 35% year-to-date, that’s probably a sensible allocation of capital.

Nibbles:

Director dealings:

A prescribed officer of Standard Bank (JSE: SBK) sold shares worth R5.1 million.

Des de Beer is back on the bid for Lighthouse (JSE: LTE) shares, picking up another R2.14 million in the company.

The CEO of Crookes Brothers (JSE: CKS) sold share awards worth R191k (not just the taxable portion from what I can see).

With Hulamin (JSE: HMN) having previously flagged that the poor performance of the extrusions business has led to a strategic review, they’ve now released a cautionary announcement noting that they have entered into negotiations for a potential disposal of that asset. No other details are available yet.

Although it is very likely that a deal gets approval from the Competition Tribunal when it has been recommended by the Competition Commission, it’s not a guarantee. It’s therefore an important milestone for Barloworld (JSE: BAW) that the consortium’s offer to shareholders has now been given the green light by the Tribunal. The parties are working towards getting the remainder of the conditions precedent ticked off the list.

Omnia (JSE: OMN) announced that its credit rating has been affirmed by GCR Ratings. Although a credit rating isn’t an indication of equity returns, an affirmed rating does mean that the cost of borrowing should be steady (assuming constant rates in the market as well), which helps the company plan for growth and ultimately benefits shareholders as well.

Introducing Rabia Ghoor, founder of swiitchbeauty®:

Rabia Ghoor, founder of swiitchbeauty® and winner of multiple awards, is one of South Africa’s most celebrated young entrepreneurs thanks to her fascinating backstory of starting the business at the age of 14 and dropping out of high school shortly thereafter.

But in the decade or so since then, Rabia has built a powerhouse of an eCommerce business – a business that deserves the limelight beyond its founder.

On episode 2 of The Finance Ghost plugged in with Capitec, we gave the business lessons from the journey building swiitchbeauty® just as much attention as Rabia’s story.

Episode 2 covers:

The biggest mistake made along the way.

The entrepreneurial DNA in Rabia’s family and how an upbringing surrounded by the hustle contributed to her brave and unusual decision in high school.

The initial innovation that sparked the business, namely the use of Instagram and other social media channels in a way that traditional competitors weren’t doing.

The value of building an authentic online community over a long period and using that as the foundation for a brand.

Curating a product range over time and developing key differentiators, with the importance of ‘just starting’ without necessarily knowing all the future answers.

Advice for businesses on how to get the most out of social media.

The Finance Ghost plugged in with Capitec is made possible by the support of Capitec Business. All the entrepreneurs featured on this podcast are clients of Capitec. Capitec is an authorised Financial Services Provider, FSP number 46669.

Listen to the podcast here:

Read the transcript:

Intro: From side hustles to success stories, this is The Finance Ghost plugged in with Capitec, where we explore what it really takes to build a business in South Africa. This podcast features Rabia Ghoor, who started swiitchbeauty when she was just 14 years old and built it into a household name.

The Finance Ghost: Welcome to the second episode of The Finance Ghost plugged in with Capitec – such an exciting one today because I get to speak to Rabia Ghoor, who founded swiitchbeauty, literally a household name in the South African beauty and cosmetics space. I’m so looking forward to tapping into these insights from not just her early journey as an entrepreneur, but of course, everything she’s achieved in the decade thereafter.

This includes winning a whole lot of awards that recognise young South African entrepreneurs. And I think “young” is a feature that just keeps following you around, Rabia. It’s such a core part of the story of swiitchbeauty, and yet you have the kind of business experience that most people are lucky to have by their 40s if ever.

And full credit to Rabia here – she’s been so busy this week doing pop ups pretty much across the country, she’s apparently been irritating shopping centre security with just the sheer number of people who have shown up for these pop ups. So there’s another sign of success. And Rabia, you still made time to do this podcast even though you’re not even feeling well. So thank you very, very much – it really means a lot, just for you to be able to come here and share your story and your insights with the audience and certainly the inspiration that I think we’re all going to take from this, me included. So thank you for doing this.

Rabia Ghoor: Thank you so much for having me and for all of the grace with the rescheduling, etc. and so on and so forth. I am very, very honoured to have the opportunity to share with you. Just thanks for having me.

The Finance Ghost: No, it’s a great pleasure. And I think as we talk more about the backstory of this business and what you’ve built today, I think it’ll become very clear to any listeners who maybe aren’t familiar with you yet, exactly why we’re doing this podcast. So let’s jump into it because I think the backstory of swiitchbeauty is incredible. And for those who want to Google it, by the way, it’s with two i’s in the middle – swiitchbeauty, one word.

People say you’re never too young to be an entrepreneur, you’re never too young to start something. But generally when people say stuff like that, I don’t think they have 14-year-olds in mind as people who start businesses. It really is fantastic. And I’m keen to understand more about that early start because my understanding is you then left school at age 16 to go into the business full time, which is really quite a remarkable story.

So Rabia, what is it like being the poster child for teenagers everywhere who are arguing with their parents and claiming that teenagers know better, because you did in fact know better, or perhaps your parents were supportive of it? I’m keen to understand, but maybe talk us through from your perspective at least, what drove you at that age, what led you to do this?

Rabia Ghoor: That is hilarious, Ghost. And I really would love to – I think I need to kidnap you to be on my PR and marketing team because, wow, you have presented me so well and made this all sound so, so elaborate and, and cool that maybe I should hire you.

The Finance Ghost: Maybe, hey! Maybe.

Rabia Ghoor: So yeah, I think there’s been a lot of focus over the years when I’ve been asked questions, been a lot of focus on the age and I always answer and people always think I’m telling a joke, but it’s really very true that Indian people sell anything, you know, and so growing up, the coolest thing you could do at school is sell something, like anything – stickers, or I remember back then these sharpeners were really cool, erasers. It’s just nature. It’s in the nature of an Indian person, I think, to trade. And so you really are selling virtually anything from any age. And so it wasn’t that big of a deal when I think I decided to take it a little bit more commercial or a little bit more seriously with the onset of social media and Instagram. I had historically been selling all kinds of stuff at school up until that point in time.

Also, family of five kids and last of five kids. And so I kind of grew up watching my siblings sell all kinds of stuff, like phones and earphones and all types of chargers and stuff – anything that was cool or hot or trending, chances are my brothers were selling it to someone, somehow, some way. I grew up in a really commercial environment.

My dad has been an entrepreneur his whole life, my mom as well. So my mom actually, funnily enough, her family owns a spice business, a spice shop at the Victoria Street Market here in Durban. And they’ve owned the business for many, many, many decades. And in her prime of her life, what she would do is she created a mail order system for the business, because there were many foreigners that came through the Victoria Street Market, it was a big tourist attraction, and they loved to purchase the spices. And they always asked my mom: how can we get it when we go back to our countries or to go back to our hometowns? And my mom would take down their details and then ship to them on almost like a subscription – which was really ahead of its time.

Then later on, as my dad had been through many different businesses in his life, ups and downs, my mom then started a catering business from the house to sort of help out where she could. And so I’ve just witnessed a lot of commerce all of my life. My grandmother, actually, who I’m named after, she was an absolute maestro and legend of note. She had 10 children and 10 boarders. So in those days, you would have boarders that would come to stay because there were very few institutions that allowed people of colour to study. And in Pretoria, there was obviously TUKS, and people of colour could study at TUKS. So people from outlying areas would send their children to live with my grandmother and obviously board there. And that was one of her businesses.

Another one of her businesses was she would buy in bulk all kinds of groceries and then create grocery packs for all of the people that lived in the surrounding areas. So because she had 10 kids, she would just send one kid to buy each thing. So the one kid would go and buy like, 30 butters, and the other kid would go and buy, like, 30 loaves of bread, and the other kid would go and buy 30 litres of milk. And so she contracted out the work to each child, and they all came back with the groceries. And then she got them to form an assembly line at home to create the grocery packs. And then each grocery pack would then get delivered by one kid to one household. And so she had this whole system going. And so obviously, if she ran this type of system, then whatever groceries she purchased for the house were free because she would add a small markup to each grocery pack for the labour, etc. You just come up with a plan. And a lot of the time that plan involves commerce. And so this is sort of my background where I come from, so it seems very natural to see where it has led.

The Finance Ghost: Yeah, I love that. I love the richness of culture, obviously, just coming through and all of those influences in your early life. It’s fantastic. The hustle started young with you, clearly. I had a similar experience, actually. I also – even in high school, I was busy buying and selling stuff because I actually really wanted a PlayStation and there was no way my parents could afford a PlayStation for me. This was back in like, sho, this was probably PS1 days, maybe, it must have been PS1. And there was no chance I was getting one any other way. And so I managed to figure out there was this particular way I could buy stuff and then sell it to the other kids at the school. And I got to a point where eventually I’d made enough to actually buy myself the PlayStation in like grade nine, I think it was, or whatever the case is. So, you know, whatever that motivation factor is, I think you either have it in you or you don’t.

I mean, my theory on this is always, if you give me a choice between someone who’s a natural entrepreneur and someone who’s got an MBA from the fanciest possible college, and you ask me which one I’d rather choose in a high stress situation of running a business, I will choose the natural entrepreneur every single time. Because I think that when you get the academic stuff on top, yes, it can supplement what’s inside you, but it cannot teach you to be an entrepreneur. It’s like if I took a course to become an Olympic sprinter, I could literally have Usain Bolt as my teacher – it would not make a difference, I’m not going to be an Olympic sprinter. And I think it’s much the same with being an entrepreneur. There’s an element of “it’s in you” and you’ve got these influences around you – and it’s not to say that you have to come from an entrepreneurial family. Actually, on this podcast series, my first guest was Makomborero Mutezo, who started TheHungryMute. And what’s really great with his story is his mom is a professor of risk in an academic environment. So you can imagine this poor woman stressing over her son going out there and starting a business.

And I wanted to ask you about how your parents responded to this because you’ve mentioned the Indian culture stuff there. A lot of the sort of memes and stuff we see online and from tech in the US and stuff is the jokes of how high the expectations are of Indian parents. Often – it’s just like this standard trope that you see online. And I’m curious what it was like for you going to your parents and saying, look, I’m actually done with school. I mean, much as they’re entrepreneurs and much as there’s that rich family history. Did they kind of support that view. Did they just jump at it or did they try and talk you out of it?

Rabia Ghoor: You know, it’s really funny when you ask me this question, my mind jumps back to a memory that I have of when – so I once got busted in school for selling these sticker packs or something like that. They sent me to the principal’s office and principal’s like, yo, do you know you’re not allowed to sell stuff in school? And I’m like, I didn’t know that, sorry, whatever the case is. And I then proceeded to bribe the principal with a commission on said sticker packs!

And there was a great affinity in school for chicken wings during lunchtime. And so I would get off, like, five minutes before break time. I would tell the teacher that I needed to go to go to the bathroom, and then I would go to the cafeteria and I would buy out all the chicken wings. And then the bell would ring and it would be break time. And then I would proceed to then sell said chicken wings, which I now have a monopoly over, back to the students. And so…

The Finance Ghost: …that’s incredible! Never mind big oil. It’s big chicken. You were literally big chicken.

Rabia Ghoor: It’s big chicken!

The Finance Ghost: I’m starting to wonder if you dropped out by choice or if they actually just said to you, Rabia, please, this isn’t working. You’re ruining our school. Can you just go, please?

Rabia Ghoor: So I’m just thinking about those two things that I’ve mentioned. I’m thinking about what my parents might have been witnessing at the time. See, I’m the last of five, right? And no last of five was planned. Any last of five is likely a mistake. And so I think by the time I was born, my father was 50. And so I think, they were just really, really exhausted.

The Finance Ghost: Sho, I’m tired, actually, just thinking about that. I’m 37 now, and my kids keep me nice and busy. I cannot imagine having a baby at 50.

Rabia Ghoor: Yeah. As I was saying, I think by the time I told my parents that I wanted to leave school, not only did I have this incredible track record of doing things that I said I was going to do, like if I said I wanted to start something, I would do it and see through the whole way. I had also been in business for two years already by that point in time. I’d been doing switch online for two years at that point. So I had something to show them. It wasn’t like, hey, I’m going to leave school to start this business. It was more like, I’ve started this business., it’s doing – it’s doing pretty decently, I’m going to leave school. I want to pursue it full time.

And something that I was very lucky – my parents had, at that point, full confidence in me. You know, there really wasn’t even a glimmer or like even a hint of doubt in them at that time. And it was a very crucial point, right? Because you’re 14 years old, you’ll believe anything that they say. So if they tell you that you can’t do it, or if they tell you that, you know, maybe just think about how easy it would have been for my father to be like, yo, just finish. Just finish high school and then you can start this and I’ll support you. Then I think about how easy it would have been for him to…

The Finance Ghost: …I think your dad was 64 and he was like, let me get this straight, Rabia. You want me to stop paying school fees and then you’re not going to go to varsity? He was like, great, this is wonderful for the pension plan!

Rabia Ghoor: Absolutely, absolutely.

The Finance Ghost: But, I mean, all jokes aside, obviously belief from the people around you is important, and it’s very hard to build a business where you don’t necessarily have that belief from your immediate support structure. That certainly makes it a lot harder. It’s definitely not impossible, but it helps tremendously – everything that is positive around the whole story, because it’s a hard thing to do. Aany wins you can get, you’ll take at the end of the day. And obviously family support is a big part of it. So it is a pretty great backstory. It really is.

I think – because you must be quite tired of actually talking about this backstory to basically everyone, because it’s such a feature of it – and I think it’s really a small part of the journey because all it is, is the start. And anyone who’s built a successful business and been at it for a number of years understands that the start is exactly that – it’s the start. A whole lot of things have to happen after that in order to make the thing work.

So I think let’s jump into more about the business that you have today and how you think it actually got here. You’ll have to forgive me here, because I’m not your target market. I’m not someone who wears makeup, personally, so it’s quite hard for me to look at the cosmetics markets and say, okay, I can see that swiitchbeauty’s competitive advantage is X, Y, Z. This is what makes you different, this is what you’re up against. So I’m very keen to understand from you what you think it is that has actually made swiitchbeauty a success and a standout and everything else. And I did obviously research the company, look on the website etc. and I wonder if that tagline: “makeup and skincare for lazy girls by even lazier girls since 2014” perhaps holds a clue here, because that really is a lovely bit of brand messaging and was very endearing. And I think it actually – it says a lot, right? Even for me, someone who doesn’t wear makeup, I can kind of see where this is going.

Rabia Ghoor: I think it’s important that we go back to the start to try and understand why things have shaped up the way they have over the years. And the way I started was literally on Instagram, talking to the people who supposed to buy my products, talking very informally and very sincerely, as opposed to trying to portray the image of like big brand, or like conglomerate or like institution. For the first time, a conversation was being had in beauty that wasn’t an aspirational thing. It wasn’t a brand telling a customer: you need to buy X and Y and Z in order to be X and Y and Z. For the first time. I think the streets were open both ways. Both lanes were open, right? Where historically, a lot of brands had not made it onto social media at that point in time. It was a very critical juncture. 2014, a lot of brands had not made it onto social media just as yet. People started hopping on in 2016, 2017, and there was an entire zeitgeist that had already developed in that time – ‘14, ‘15, ‘16. And so if you hopped out in ‘17, you were real late to the party.

Many of the brands only came around in 2020. Covid kind of forced them onto the platforms. And so this tiny, tiny, tiny community that started building – you know, these days the word community gets thrown around a lot in marketing. It’s sort of become a really hot marketing buzzword, but we’ve lost the essence of what it truly means. Community means being seen and being heard. Not just being listened to, but being truly heard in a space amongst other people. It doesn’t mean your likeness, so it doesn’t really mean that this person looks like me or they sound like me. It just means that they are looking at me and they are hearing me and I’m looking at them and I’m hearing them.

And so what starts off with just this tiny segment of people, say 50 people, then grows into 100, 150, 500, a thousand, etc. It’s a slow, slow, slow burn. But a slow burn means that you are scaling at a pace that is manageable. You are scaling at a pace in which it’s possible to still maintain the essence or the truth of the message or the brand or whatever it is that you’re trying to convey. And so these kind of things, I look back at them in hindsight and it’s very easy for me to assign these big words or social phenomenons to them. But at the time it just felt like, oh, this is cool, this is happening, let’s go. But at the time I didn’t really understand the impact of what was happening amongst this very, very small core group of people who today I am still very proud to say that they are with the brand, they’ve evolved with the brand, the brand has evolved with them. All things regarding the brand – things like development, things like activations, things like retail, all the ways in which the brand has been able to scale or grow or evolve – these people have been a part of that. Not in like a weird poll or weird survey way, but in a truthful sort of face-to-face way in which they – they don’t feel like they’re being heard because they are being heard. So they don’t need to feel like they’re being heard because they are being heard. They’re not being made to feel like they’re being heard. Do you understand?

The Finance Ghost: It’s the authenticity, right? It’s not just saying the thing, it’s doing the thing.

Rabia Ghoor: I wonder Ghost if that answers your question?

The Finance Ghost: Yeah, I think it does. Because what I’m hearing is that and just some context for listeners and you know, we forget – so Facebook IPO’d, which means it listed on a stock exchange, in 2012. Now it existed for a few years prior, it was only in 2012 that Facebook listed on the market. And at the time I was working in investment banking and I remember how people would say this is a joke, Facebook doesn’t even make money, it’s a free product. What is the business here? This is just going to fall over. What is this nonsense?

Well, today Meta is one of the biggest and most important companies in the world. People also forget that the first iPhone was in 2007. I remember because I was first year varsity and because I’ve referenced that stat before, because I still find it astonishing that 18-year-olds today were basically born when the first iPhone came out. That’s how old the iPhone is. You know, you could sell the iPhone a drink legally! So that’s just how much the world has changed in such a short space of time.

And I think it’s allowed for businesses like yours and like mine to actually work because suddenly you don’t have all this gatekeeping of these traditional distribution channels. Because what I’m hearing from you is that in the beginning, because of the focus on social media and because it was such an interesting story to have you involved at such a young age and living and breathing the brand, it almost sounds like it was an influencer model before people understood what that actually means. It was more of a distribution play in the beginning, building community, getting that authenticity, getting people to like you, which is not difficult. Then they come and they buy the product.

Or do you think that there were also key differentiators to the product right from the very beginning? Or do you think that’s actually been curated over time and you’ve rather built on the strength of the distribution that happened up front?

Rabia Ghoor: I think in the very beginning there was nothing really unique about the product or about the offering, just I think unique about the delivery. As I mentioned to you, our route to market was distinctly Instagram. As I mentioned earlier, there weren’t a lot of brands that were taking social media, let alone Instagram seriously.

Even things like Facebook, like in the beauty industry at that point in time, it was unheard of for big beauty houses to be even on Instagram, let alone having a conversation, a two-way conversation on Instagram. And so what that conversation allowed me to do was in real time do some of the most important market research. I didn’t know it was market research at the time because I was just chatting, right?

And so it allowed me to really get to know my customer on like a one-to-one level where it’s not this odd survey or this inauthentic questionnaire that they’re filling out, but this true and real conversation that is being had and that I’m able to then go back to the drawing board and modify my product and evolve and develop and morph it into something that this person truly, truly needs and wants. And the way that I know that they truly need it and want it is because I just asked them, because I was just chatting to them. You’re not throwing mud at a wall and like hoping that it sticks. These are informed development decisions that are rooted in literal conversations.

The Finance Ghost: So, Rabia, we’ve spoken a lot about how distribution was a big part of the early journey and Instagram and everything else. But of course today, it feels like everyone’s talking community and online and everything else. I imagine your product has now also developed to the point where it’s differentiated, or at least it has one or two key selling points that your audience really attaches to it. So what has been that key selling differentiator for you beyond just having an amazing Instagram profile, for example?

Rabia Ghoor: Wow. So basically, the philosophy of Switch is “for lazy girls by even lazier girls” – and that concept is really well and truly meant by each and every single one of the products. When I am developing something, my number one concern with it is how little time can this cost me. Like, in fact, can it save me time? Can it give me time back?

If I think about it, maybe I use five products in my makeup routine or three products in my skincare routine, if each product can just save me one minute, then I have gained five minutes in the morning. To give a woman five minutes in the morning – no one can claim to do that. Also, she’ll never forget it. It’s like lasting, it’s forever. It means that I had to wake up five minutes later. It means that these robots on the way to work are not going to take me out because the brand that I love so much gave me five minutes back.

It’s something that you don’t even notice. When something saves you time, you barely even notice it, but it makes a world of difference in how you feel. And nobody really remembers what you told them, but they just remember how you made them feel, right?

So, yeah, each product is designed with really big focus on function and ergonomics. I think a lot of the beauty products on the market these days are considered greatly in form and aesthetic. Not many of them are treated like tech products and have that attention to detail, in terms of function and ergonomics, how does this perform? How do we make it perform faster? How do we make it perform in a way that is more efficient to the user? Because most products that are made in the beauty market aren’t actually made by the user. They’re made by chemists or artists, not by users.

The Finance Ghost: I love that point around people remember how you made them feel. There is a huge amount of value in there from a marketing perspective for any business. So that is certainly well worth remembering.

So I want to bridge this concept now around your key differentiators when you started and your client value proposition now, and how people often feel when they sit down and they think about starting a business, sometimes people sit down and they say, oh, you know, I can’t think of what business to start. I just don’t know, like, what’s missing out there? What is my big idea? What is the incredible product that’s gonna change the world? You don’t need to do any of those things. You actually just need to innovate. And innovation is a very incremental concept. You didn’t invent makeup – definitely not. But what you did do was you said, hang on, there’s a gap here in terms of distribution, and distribution is an innovation at the end of the day.

Capitec, who are making this podcast possible, they didn’t invent banking. They didn’t invent business banking. They certainly didn’t invent retail banking, but they saw a way to do it differently, and they’ve built an absolute powerhouse as a result of that.

I think the same is true for you. I think the same is true in terms of my own business. I didn’t invent finance or financial media or writing about the markets or podcasts, but there’s a unique mix of skills there that makes Ghost Mail and The Finance Ghost and the whole ecosystem something that people look to for insights that they can’t necessarily get very easily anywhere else.

So that’s all that innovation actually is – and I wish more people would just think about it that way and say, okay, here’s my skill set, what can I do with it? And what can I do with it that is just different enough to what’s already there in a way that’s going to make it more economically lucrative? So well done to you for spotting that at the tender age of 14.

I guess what helps is that at the time, you and your friends would have all been checking out all the new social media stuff. Instagram’s new and exciting. And then because you’d already had such an entrepreneurial lens on the world and your daily life and your, you know, slightly dicey dealings at school, you kind of looked at this and said, hang on, there’s actually something that I can do here. And I remember reading a piece by an author named Seth Godin. So he’s like a marketing guy, and he writes these quite interesting books. A lot of his books are actually just a collection of ideas, it’s not really something you’ll easily read cover to cover. But I remember reading something he wrote, now it must be 10 years ago at least, and it left such an impression on me where he wrote about how the internet just is this great disintermediating factor. It takes away the gatekeepers and it helps people take what he calls their art to the world. And he writes about the concept of having 1,000 true fans. And if you can build a business around having 1,000 true fans, and I think that’s exactly what you’ve done, is you built this community, it was authentic, people really liked you, they trusted you. You had this army of true fans. And today you go and do a pop up and you have thousands of true fans in one city. But you don’t get that overnight, you know, you start by building 10 true fans and then 100 true fans. And now look at where you are. I mean, does that sound like a pretty decent summary of this journey for you?

Rabia Ghoor: I’ll say, I’ll say. Also, you know like how every time they have these interviews with entrepreneurs and then they ask if there’s one piece of advice, what would you give? And then the entrepreneur says the advice would be to just start. And then you get kind of annoyed because you’re like, okay, but can’t you just tell me how to start? Why are you telling me to just start? But you know, earlier you were asking all of those questions. The only way you get to asking those questions is by starting. Sometimes you don’t go out the gate knowing all of those answers. If you just start somewhere, the chances of that question coming up will be more likely and the chances of you needing to answer it then naturally are more likely. So the whole “just start” thing is cliché because it’s true.

The Finance Ghost: It is true. And I will also say that the benefit of starting is that you don’t actually know what it’s going to lead to next. So, I learned how to build a community-based business because I initially did it on something that had nothing to do with finance and had everything to do with my particular interest, especially more so at the time, today I’m a bit busy for it, sadly, but I had this big interest in classic cars. I was rebuilding a classic car and I thought, okay, there’s going to be other people out there who are doing this. I’m quite young for that, or I was at the time. Let me start something that’s kind of interesting around this and the motorsport that I was involved in. And then I realized that I could, if I was creating content around this and people were following it, there was an opportunity to sell advertising around this and that actually paid for my racing. So I had this beautiful circle where I was like, hang on, I can blog and create content about stuff I love, which then attracts advertisers, which then pays for the thing I love. This is fun!

And that taught me so much about how it works online, how websites really work, what sort of things people resonate with, etc. I basically just took those learnings and then said, okay, well, if I can scale that up to finance, which is a vastly bigger audience with much, much bigger advertisers, maybe I can have a really strong business. And here we are today.

So I think “just start” is good advice. I think start with a plan, definitely. And start in a way where you don’t risk everything that’s going to hurt you so much upfront. You know, as you say, you already were two years into the journey. You kind of had a brand, you could show that you had achieved some resonance with it, and that was what made it easier for you to say, okay, I’m going to go all in on this thing. From the sounds of it, I’m not sure you would have been focusing at school really anyway, because I can imagine how this was absolutely dominating every though, every bit of excitement. But you had the guts to do it. You had the guts to actually roll the dice and start. And you’re right – I think that is a big part of what people need to think about in the early stages of having a business.

And I imagine that you’ve had some pretty cool validations over the years, right? People who love your product, people who give you that feedback, people who spot you in the wild, maybe because you are the face of the business to a large extent, or at least you certainly are a publicly visible founder. So I imagine you have had that a couple of times, hey?

Rabia Ghoor: I’ll say. Yeah. But it’s a really, like, friendly thing that happens. It’s not like – very rarely will people even ask for a pic, because it’s not like that. It’s just like a – I see you and you see me, and we know we’re from the same place type of thing. And what’s really beautiful about it is that it spans ethnicities and genders, even religions, all types of socioeconomic statuses. It’s just like a, I know a switch girl when I see a switch girl and I know that she knows me look of recognition. And there’s even sometimes a smile or exchange which happens. It’s a really lovely thing that happens. I haven’t ever experienced it to be annoying. Do you know what I’m trying to say? An annoying thing, like celebrity type thing that happens.

The Finance Ghost: Yeah, it’s like a respectful recognition, which is great. That’s exactly, that’s exactly what you want, right? That’s the best. But I guess as well with building a business around a specific personality like you’ve done certainly in the initial stages, it’s a bit of a double-edged sword, right? I mean I face much the same issue where you kind of become the voice or the face of a business.

And you’re lucky in a way – well, not lucky. It’s by design, right? You’re not actually the product, people are buying makeup as the product. So that’s one up on mine, as me writing and speaking is the product. So that’s – I don’t know how to solve that problem. But I can imagine for you it was tough to actually start to bring people on board to actually start to get help. This is I think the biggest thing that entrepreneurs struggle with, successful entrepreneurs. So once they’re out the gate and they’ve got a business that works, they’ve got an idea that works, they’ve got product market fit, one of the hardest things then is to actually figure out, okay, how do I scale this thing? How do I bring people in? I mean, how have you handled that part of the journey?

Rabia Ghoor: I really am battling to think about how to answer this question because I think one of the luckier places I got in life is starting so early that even if you made like a really, really, really small amount of money to you, it was a really big amount of money because you were a kid.

And so at every given point in time the scaling of this business has changed, felt very natural and very much where it’s supposed to go. Simply because I really never expected – it’s not that I never expected it to become successful, it’s just that I never really needed it to because I always thought of myself as like a kid. Do you know what I mean? I feel like the older you get, the more you kind of get pressure. When you get to grade 10, people are like, what subjects are you taking? And then you get to matric and people are like, oh, how many A’s did you get? And then it’s like after matric, oh, what are you going to study? And then after you study it’s like, oh, where will you get your first job? And there are all these questions – and so I suppose now if I start to think about scaling from this point onwards, it can be more of an anxiety inducing thing because I wonder where to from here? But then I look back at the last 10 years and at any given point I could have wandered way too from here and it could have been a source of fear for me, a source of anxiety for me, but instead, I know this is going to sound so incredibly whimsical but bear with me: what if I just trust the process and go along with the journey and keep doing what I’m doing? There has to be a reason why it’s worked out until this point. So what’s the reason why it won’t continue working out in the future?

The Finance Ghost: I don’t think it’s whimsical at all. I think if you’ve got the track record, there’s no reason to believe that it won’t continue.

A lot of entrepreneurs do also find that there are different phases of the journey, right? So as you get bigger and bigger, then there’s another – you know, initially you scale some of the relatively basic things like admin processes and one or two of those sort of things. But as a business really matures, then you have to start outsourcing strategic decisions and giving people the ability to make product decisions on your behalf and marketing decisions on your behalf and eventually finance decisions on your behalf. And that’s how you eventually become a larger organization. And I think each of those scaling journeys is actually quite a scary and difficult thing to get right. It really isn’t easy.

I think you’ve touched on a point there which is also really helpful. And I often say this to people when they’re thinking of starting a business is: just take a proper look at your life right now, are you actually able to do this? Because if you are sitting with two very young kids in school and maybe your partner’s income is not going to necessarily cover everything if anything goes badly wrong for you and you won’t necessarily get another job quickly. Let’s not glamorise taking a risk. Taking a risk and saying, okay, that’s it, I can make this work. Yes, it’s an amazing thing to do when you’re 14, but you’ve got a massive safety net as well. You know, you’re not – your parents are not going to lose their house because you didn’t quite sell as much makeup that month as you thought. Whereas when you get into adult-level risk taking, the downside is very real and it gets very ugly very quickly. So I always give people a realistic view on this and just say, look, don’t romanticise the risk you’re taking. The reward can be wonderful, the journey can be great, but there is huge survivorship bias. For every Rabia who’s able to do this podcast, there are a lot of people where it hasn’t worked out. And that’s why entrepreneurship is so exciting, is because it’s a risk. So I always suggest to people: feel inspired, definitely, but don’t be silly. You know, take a realistic view and actually make those decisions in a – I think just a disciplined and just smart way. I don’t know if you’d agree with that?

Rabia Ghoor: You know, I think it’s difficult to tell someone to dream and to be realistic in the same breath. When I was growing up, my uncle would always say to me that if you’re going to play with a bomb, that you should take it outside of the house and play with it outside. And what he meant was that you look after the thing that is currently sustaining you, right? So whatever that thing is – at the time, for me, the thing that was currently sustaining me was school, right? And so you look after the thing that’s currently sustaining you. Meaning if that’s your job or if there’s something that is making you money somehow and it’s covering your day-to-day expenses, look after that. And when you would like to play with the bomb, go outside and play with it. So that’s after-hours, pre-hours, you wake up before your job and you work on your business, you work on your business after your job, but you are still working on your business. You’re still playing outside with the bomb, but you’re just playing with it outside of your house so that anything happens. So if it decides to go off, it’s not going to blow up your house.

The Finance Ghost: I think that’s a great analogy. So thank you. And I think that is an incredibly good point. It’s why I’m a big supporter of side hustle and businesses that start as side hustles because it lets you figure out stuff like product-market fit and whether or not you actually want to be doing this then long before you resign from your job and roll the dice. So that is lovely advice.

On the subject of advice, I’m going to hit you with three quickfire questions as we start to bring this to a close. So the first one is around just social media and businesses looking to really make it work on the socials, which is clearly something you’ve done extremely well. I think just the first kind of do’s and don’ts that come to mind for you, if people ask you for advice on this, what do you think works? What do you think absolutely doesn’t work?

Rabia Ghoor: The number one thing I would tell you to do is not outsource your social media to an agency because chances are you’re not going to get anything novel or unique, which is what ultimately does well on social media, is novelty. And even that one-off, like virality or whatever the case is, I would suggest hiring younger people, people even much, much, much younger people than you would think to hire. There’s an intangible zeitgeist, nuanced language digitally native language that is spoken on these platforms and more often than not they are spoken by the youth, which is now, mind you, escaping me as well. I can’t consult people my own age anymore. Every time there’s a family function and there are these gen alphas…

The Finance Ghost: You’re at that point, Rabia, where you have to say, back in my day, it’s coming.

Rabia Ghoor: Dude!

The Finance Ghost: I don’t think you’re there yet, but you’re almost at “back in my day” – it comes for us all.

Rabia Ghoor: I’m already meeting kids and telling them that I knew them when they were this big. And then you like signal how big they were.

The Finance Ghost: Oh, that’s great.

Rabia Ghoor: It’s like, yoh, dude.

The Finance Ghost: Yeah that does happen to us all.

Rabia Ghoor: But yeah, I – every time we have family functions and there are Gen A’s around, I bring them all together around the table and I start asking them questions about TikTok and I start asking them questions about their purchasing behaviour and what influences them. And obviously the older you get, the more informed these kind of questions become, the more you know exactly what you’re looking for. It’s one thing to listen to what they’re saying and go, okay, yes, but you’re just a kid. It’s another thing entirely to try and understand what sort of incentives or thinking patterns or mental phenomena are influencing these answers that this child is giving me. It’s a greater psychoanalysis that goes into this evaluation. It’s like a think tank but on steroids. And you also have to take them very, very, very seriously. The mistake that people make is by thinking that they’re smarter than the kids. That’s the big mistake.

The Finance Ghost: I love that point. So I’ll give you a very real example for me as well. I was one of the first financial analysts in South Africa who started writing properly about lab grown diamonds and how I thought it was going to fully disrupt the diamond market. And today De Beers is now loss-making, so it has happened. And it wasn’t because I sat around and thought, oh, you know, I can see this happening out there. No, it’s because my now fiancé, who is five years younger than me, said to me: I want a lab grown diamond. I said to really, you know, like, are you sure? I mean, I love you, you don’t have to get a lab grown diamond kind of thing, because I just didn’t understand. And then she kind of walked me through the way she thinks about it and the way she has this outlook on what it means that it’s a lab grown diamond versus having come out of the ground versus where money could be spent instead, etc. And this penny dropped for me of, hang on, it’s only a five-year age gap. But if this is how she’s thinking, then how are girls in their mid-20s thinking right now who are even more inclined to go down a route of sustainability, etc? And then I started doing the research and I was like, hang on, this whole mined diamond thing is in serious trouble. And it’s because I spoke to someone who is right there in the market saying, I don’t want that thing.

And that’s your exact point is it really doesn’t help you if you are outsourcing marketing functions and speaking to people who are not actually your target market or even remotely of their age because they don’t get it. They’ll try and sell you a story that they do, but they don’t get it. So I think that’s great advice, I really do.

Next quick question is just around supply chain and maybe biggest learning from that journey because now that your business is quite big, there must be a lot of plumbing around the back there keeping this thing working. What’s been your biggest learning from a supply chain perspective in this business?

Rabia Ghoor: Ooh my biggest learning is that a lot of the time people use acronyms to try and make it sound like it’s a lot more difficult than it actually is. But if you just learn the acronym or if you just ask the person what the acronym is, you don’t sound dumb. You’ll just be able to create more efficiency. So my biggest learning is just learn the acronyms!

The Finance Ghost: Yeah, that’s great. Actually. It’s amazing how similar that is to the world of finance. So it’s don’t fight the jargon, learn the jargon and then you won’t feel like you’re not involved in these things.

I think that’s a general thing that comes through from you, is get a deep understanding of all the stuff that your business is going to be made or broken on. Is that a fair statement?

Rabia Ghoor: Yeah, I think sometimes if you’re not qualified in something specifically, or maybe you don’t have experience in it, it’s very easy to feel as though you are on the back foot. But sometimes the very thing that you think to be your disadvantage turns out to be your greatest advantage. Because if you are not qualified in that thing or not learned in that specific thing, then you have the opportunity to look at it with a bird’s eye view instead and to innovate or to disrupt, right? So, yeah, don’t let the jargon intimidate you.

The Finance Ghost: Last question, Rabia, on this wonderful podcast. Your biggest mistake, because I’m sure there is one, there must be one that burns or that you will remember for the rest of time or something you’re obviously willing to share publicly – but what would that biggest mistake be?

Rabia Ghoor: Cool. So there was a point in time in which switch was really starting to take off and there were many opportunities for me to develop my personal brand. And I bit, I bit too quick and I bit too fast. If I could go back in time, I would probably have developed my personal brand a lot less and just worked on developing switch a bit more. But obviously I was young and you see any opportunity as an opportunity, right? To just kind of go along with it with the journey. But in retrospect, I think I would have done a lot less from a personal brand marketing perspective.

The Finance Ghost: So, Rabia, thanks. We’ve covered so much ground here. As usual, the podcast is longer than I planned. It always goes that way because I’m lucky enough to speak to such fascinating people who have amazing insights to share. Well done on building such a cool business and I think to do it at the age you did it – I know that’s all the focus that a lot of people put on this thing, but actually, as much as that’s impressive, I almost think it’s the follow-through that’s even more impressive, which is what’s happened in the decade after that to actually build this thing. Because it could so easily have just stayed a little side hustle and a little trading business, and instead you have an incredible brand that is widely followed. It’s just a great story. It’s a very inspiring South African business story, so congratulations to you.

Thank you for giving up your valuable time to be on this podcast. Luckily, you have a lot of valuable time because you use your own beauty products, so it saves you that five minutes a day. And all those minutes add up then into being able to come onto this podcast! So Rabia, thank you. Congrats and just carry on doing what you’re doing. I think it’s lovely.

Rabia Ghoor: Thank you so much. It’s really me who should thank you for having me and for honouring me in this way. I think it’s been a really lovely thought exercise for me as well and an amazing experience. So thank you. Thanks so much.

The Finance Ghost: Thanks Rabia. Ciao.

Real stories and real people. Yours could be next. Plugged in with Capitec. Capitec is an authorized financial services provider, FSP 46669.

African Rainbow Minerals increases its stake in Surge Copper (JSE: ARI)

They describe the stake as being for “investment purposes”

When listed companies acquire stakes in other listed companies, it’s usually because there’s a long-term plan at play. The market doesn’t reward companies for owning small random stakes in other listed companies, as shareholders can just as easily replicate that situation for themselves by going and buying the shares that they actually want. It becomes a different story when a listed company is either buying up shares as they are working towards a takeover, or at least significant influence in a company, as that’s not something that shareholders can go and do themselves.

So, what is African Rainbow Minerals’ plan in respect of Surge Copper? We don’t know at this stage, with the company merely describing the stake as being for “investment purposes” – but they seem to be investing a whole lot more in it, so could there be a bigger plan here? After the latest investment of around R57 million, African Rainbow Minerals will own 19.9% in Surge Copper. They previously had 13.44% before the latest tranche.

With copper as a hot asset at the moment, African Rainbow Minerals is clearly seeking diversification from its core business (iron ore and a few other commodities) and exposure to the copper growth story. Time will tell if they have ambitions to control this asset.

Aveng is indeed loss-making, and by a huge margin (JSE: AEG)

The initial trading statement gave little indication of just how rough the year was

In early June, Aveng released a trading statement that indicated that the company would swing from a profit to a loss in the year ended June 2025. Full marks to the company for giving this early warning and for not taking the easy way out, which would’ve been to say that profits will be more than 20% lower. But even then, the full extent of the loss is quite something to see.

Things got so bad that the headline loss is between A$83.8 million and A$87.2 million vs. a profit of A$38 million in the prior year. On a HEPS basis, that means a headline loss per share of between 63.3 and 67.2 A$ cents. With the share price currently on R5.90, you can therefore very quickly see why the price is down 53% on a year-to-date basis.

Construction is an incredibly risky sector, as projects that go wrong and generate losses are capable of producing huge losses. There are substantial problematic projects in Southeast Asia and Queensland. In fact, the only highlight seems to be New Zealand, where they are now paying tax, as assessed losses have been used up by that operation.

Detailed results are due for release on 19 August.