With over two-thirds of the energy drink market in a vice grip, Red Bull isn’t just a beverage – it’s the undisputed overlord of its category. But what does any of this have to do with death-defying stunts, football teams and the youngest Formula 1 driver in history? Welcome to perhaps the best example of lifestyle marketing in the world.

As of 2024, Red Bull was estimated to have a 37% share of the energy drink market, making it the most popular energy drink on the planet and the third most valuable soft drink brand behind Coca-Cola and Pepsi. Not bad for something that tastes like fizzy cough syrup and ambition!

Since crash-landing into the world in 1987, Red Bull has sold over 100 billion cans globally. 12.7 billion of those were sold in 2024 alone. That’s a lot of people hoping to sprout some wings.

The original formula came in exactly one flavour, but these days, there’s a rainbow of spin-offs and even a sugar-free option. But the core product remains a sort of carbonated rite of passage for students, startup founders, and anyone whose sleep schedule is a suggestion, not a rule.

The now-iconic slogan, “Red Bull gives you wings”, has been imprinted on the cultural psyche with the same permanence as “Just Do It” or “I’m Lovin’ It.” But Red Bull didn’t climb to the top by playing it safe. Instead, it built a high-octane mythology around itself, sponsoring death-defying stunts, adrenaline-fuelled sports, and events that blur the line between brand and belief system.

Forget jingles and TV spots – this is how Red Bull built an empire by selling a lifestyle disguised as an energy drink.

From jet lag to jet fuel

Before Red Bull was fuelling snowboarders, DJs, and sleep-deprived students in the West, it was keeping truck drivers and factory workers upright in the sweltering heat of Thailand. Its origin story takes us to the backstreets of Bangkok, where a duck-farmer-turned-pharmaceutical-entrepreneur named Chaleo Yoovidhya was tinkering with a solution for exhaustion.

Chaleo, the son of Chinese immigrants, founded T.C. Pharmaceutical Industries in the 1970s, selling over-the-counter syrups and medicines to Thailand’s working class. Inspired by Japan’s growing market of functional tonics, he created Krating Daeng in 1976 – a thick, non-carbonated, caffeine-and-taurine cocktail served in squat little glass bottles. It didn’t fizz, it didn’t come in a designer can, and no one called it a “lifestyle choice.” It was made for people who worked long, hard hours and needed to stay awake to finish them.

And that might’ve been the whole story if an Austrian toothpaste marketer hadn’t been battling jet lag in the early 1980s.

Enter Dietrich Mateschitz. On a business trip to Asia, running on fumes and frustration, he was handed a bottle of Krating Daeng by a local colleague. One sip and his circadian rhythm snapped back like a rubber band. More importantly, he saw something others didn’t: a business opportunity with wings.

By 1984, Mateschitz and Chaleo had struck a deal. They co-founded Red Bull GmbH, each owning 49%, with 2% set aside for Chaleo’s son, Chalerm. Chaleo brought the formula. Mateschitz brought the vision, and the rest, as they say, is history.

But bringing Krating Daeng to the West wasn’t a copy-paste job. Western palates weren’t ready for the syrupy, medicinal original. So Mateschitz carbonated it, tweaked the sweetness, and ditched the humble glass bottle for a slim, futuristic can that looked more at home in a nightclub than a 7-Eleven. From the packaging to the flavour, it was a complete identity overhaul – but the masterstroke would be the positioning. In Thailand, Krating Daeng was a blue-collar tool. In Europe, Red Bull would be an elite accessory. A drink not for the tired, but for the tireless.

An empire of experiences

Instead of sticking to traditional ads or celebrity endorsements, Red Bull built its identity around experiences – specifically, the kinds of experiences that involve risk, speed, or gravity-defying stunts.

Its strategy is rooted in experiential marketing. The idea is that people remember what they feel, not just what they see. By sponsoring extreme sports events and athletes, Red Bull has created a strong association with adrenaline, ambition, and adventure. To keep that storytelling in its own hands, Red Bull created Red Bull Media House, an in-house content studio responsible for everything from YouTube videos and Instagram reels to documentaries and podcasts. By keeping production close to the brand, it ensures consistency in tone and message, something that’s helped Red Bull stay culturally relevant across platforms.

One of the clearest examples of this strategy in action is the Felix Baumgartner stratosphere jump, a moment that blurred the lines between science, sport, and spectacle. On October 14, 2012, Austrian skydiver Felix Baumgartner ascended to an altitude of approximately 39 kilometers above Earth, lifted by a helium balloon from Roswell, New Mexico. From this height, he executed a free fall that lasted about 4 minutes and 20 seconds, during which he reached a top speed of 1,358 km/h, becoming the first person to break the sound barrier without vehicular power.

The mission, known as Red Bull Stratos, aimed to transcend human limits and gather valuable data for aerospace medicine and engineering. The project involved a team of experts in various fields, including aerospace medicine, engineering, and pressure suit development. The event was broadcast live and captivated millions worldwide, setting a record for the most concurrent views on a live stream at the time.

The brand’s investment in sport extends well beyond sponsorship. Red Bull owns several major teams, including Red Bull Racing in Formula 1, and football clubs like RB Leipzig, Red Bull Salzburg, and the New York Red Bulls. Beyond traditional sports, Red Bull has backed niche pursuits like the Cliff Diving World Series, and has even entered the music industry through Red Bull Records, an independent label launched in 2007 to support emerging talent. A year later, the brand added a publishing arm to represent songwriters and producers.

Market like you mean it

It might seem unconventional for an energy drink company to own Formula 1 teams, football clubs, music labels, and a global media house. But for Red Bull, these are more than side hustles. They’re the scaffolding of its entire brand strategy.

Red Bull allocates an estimated 25–30% of its annual revenue – that was around $2 billion in 2023 – to marketing. But instead of traditional ad campaigns, it channels this investment into building a self-reinforcing ecosystem. Red Bull doesn’t just place its logo on sports teams; it owns them. It doesn’t just sponsor content; it produces it. This ownership model gives the brand full control over the fan experience, on the track, on screen, and online, allowing it to orchestrate every touchpoint with precision.

This integrated approach creates a powerful synergy. Fans of Red Bull Racing, for example, are more likely to tune into Red Bull TV documentaries, share extreme sports clips on social media, or attend a cliff-diving event, all of which amplify brand engagement. Each part of the ecosystem promotes the others, unlocking economies of scale and deepening consumer loyalty. By aligning every element of its brand universe, Red Bull has built a marketing machine where the lines between content, commerce, and culture blur.

As the company looks to the future, Red Bull is well-positioned to expand its existing presence in emerging areas like esports, where its high-octane identity aligns naturally with digital-native audiences. At the same time, its growing media output allows it to diversify revenue streams and capitalise on the demand for premium branded content. The challenge will be balancing its aggressive spending with sustained returns, especially in markets with tight sponsorship regulations.

Still, Red Bull’s playbook shows what’s possible when a brand doesn’t just sell the experience, but becomes the experience.

Finally, here’s a fun fact for us South Africans: Red Bull’s biggest competitor, Monster, was launched by South African-born Rodney Sacks and Hilton Schlosberg in 2002 after they acquired Hansen Natural Corporation in the US in the early 90s. And as a great example of how you really don’t know where the pursuit of opportunity will take you, Sacks studied law and was a partner at Werksmans before he left for the US and made the acquisition.

Clearly, we should all be travelling more.

About the author: Dominique Olivier

Dominique Olivier is the founder of human.writer, where she uses her love of storytelling and ideation to help brands solve problems.

She is a weekly columnist in Ghost Mail and collaborates with The Finance Ghost on Ghost Mail Weekender, a Sunday publication designed to help you be more interesting.She now also writes a regular column for Daily Maverick.

Adcorp has released results for the year ended February 2025. Revenue increased by 2% and gross profit was up 3.5%, with the fireworks happening below those lines – operating profit jumped by 33.3% and HEPS was substantially higher at 134.5 cents, a 61.6% increase. Nice!

With the final dividend more than doubling to just over 50 cents, there’s solid cash quality of earnings and management is clearly feeling more confident.

This isn’t an easy business to run, with the workforce solutions provider industry under pressure. Achieving any revenue growth at all is commendable, with Adcorp having to focus on cutting costs and seeking out the highest margin opportunities.

The balance sheet is now in a strong position, with a net cash balance of R442.1 million. The market cap is R665 million, which means that approximately one-third of the market cap is attributable to the operations. The Price/Earnings multiple of Adcorp is thus very misleading, as the truth is that roughly two-thirds of the share price of R6.50 is attributed to cash. The remaining ~R2.20 per share can be compared to HEPS of 134.5 cents, which means the P/E is more like 1.6x!

And yes, I have a small long position here.

There’s renewed optimism at African Media Entertainment (JSE: AME)

The radio assets remain the highlight

After such a rough time during COVID for radio assets, it’s great to see that African Media Entertainment has continued to recover. A huge part of the revenue in this space comes from events organised by radio stations, hence why COVID was such a problem.

For the year ended March 2025, revenue increased by 9%. Although operating profit was higher, there were impairment reversals at play in both periods. As always, I therefore prefer to look at headline earnings per share, particularly as this also considers financing costs that moved higher in this period. The revenue growth wasn’t sufficient for HEPS to head in the right direction, with a 4.9% drop in HEPS. The total dividend for the year was steady at 450 cents per share.

Algoa FM did particularly well, with the aforementioned initiatives like events coming in as a positive contributor. I was also very pleased to see that Moneyweb achieved growth in revenue. I’ve been partnering with Moneyweb for roughly a year now on a podcast called Supernatural Stocks and it really has been a joy to work with the team there.

The group is now stable and has a reasonable foundation off which to build.

AYO Technology’s loss has worsened (JSE: AYO)

As a reminder, Sekunjalo is looking to take the company private

AYO Technology has released results for the six months to February 2025. They expect the headline loss per share to further deteriorate to 45.09 cents.

Because maths (and apparently proofreading) is hard, they go on to suggest that this is a difference of between 26% and 46% vs. the comparable period. Obviously, they meant to give a range for the headline loss instead of a point estimate. 45.09 cents is smack in the middle of that guided range, so someone wasn’t concentrating.

Much as they like to blame the media and everyone else for their issues, perhaps they should consider whether the share price drop is at least partially due to their headline losses and general lack of care?

Delta Property Fund is still just treading water (JSE: DLT)

The loan-to-value ratio just will not budge

Delta Property Fund has a portfolio of 83 properties across South Africa. This is very much a polony portfolio, consisting of a mish-mash of undesirable things that roll up into something that is barely edible and unlikely to be good for you.

Last year, they had 89 properties. The fund is doing its best by trying to sell off what it can, making tiny dents in the debt along the way. The problem is that the loan-to-value ratio has actually ticked up slightly from 59.4% to 59.5%, so these efforts are proving to be futile at the moment.

There are some green shoots. Although rental income fell 1.9%, net operating income increased by 10.3% thanks to cost optimisation and selling off some of the really bad properties. Although there’s a net loss of R104.2 million for the year, this was due to non-cash fair value losses of R222.5 million. This is also why the loan-to-value remains stubbornly high, as the value is going the wrong way. Funds from operations per share did come under pressure though, decreasing by 19.3%.

The vacancy rate improved from 33.4% to 31.9%, helped by the disposal of six properties that had few or no tenants. Getting the tenants who are in place to pay is another problem, with a collection rate of only 95.1% of billings.

The good news is that major bankers have renewed the group’s facilities out to April 2026 and in same cases to June 2027. The banks are enjoying themselves at this carcass, helping to keep it alive and earnings juicy interest payments along the way.

This patient is still in ICU, but has been stabilised at least. It’s now about the recovery process and avoiding any major setbacks.

Deneb needs to get out of its property portfolio (JSE: DNB)

The otherwise decent operating results are being obscured

Deneb Investments, part of the HCI stable (you’ll see that a lot in Ghost Bites today), grew revenue by 6.3% and improved gross margin by 50 basis points. To add to the happiness of gross profit growth of 8.5%, they kept operating costs to an increase of just 5.9%. But underneath all this, it gets a lot more interesting.

The property segment saw revenue fall by 11% and operating profit by 24%. They refer to this as a “little disappointing” but I think we can all agree that it’s a lot worse than that. Although one of the factors here is the disposal of properties, they also have a major vacancy to contend with and a provision for bad debts.

The question that springs to mind is: why? Why do they own a property portfolio in the first place, which is a completely different risk/reward setup to the operating businesses?

Speaking of the operating businesses, the branded product distribution segment was good for revenue growth of 4.4% and impressive operating profit growth of 21%. The manufacturing segment grew revenue by 8.4% and operating profit by 21.1%.

Deneb has owner-occupied property worth R302 million and investment property worth R957 million. This balance sheet is screaming for a restructure and value unlock. Mothership HCI isn’t scared of property exposure though, so one wonders if Deneb would be allowed to get out of that space even if they wanted to.

eMedia laments the local “advertising cake” (JSE: EMH)

But at least they enjoyed a largest slice of it

eMedia, part of the HCI group and the owner of the various e.tv (and other) businesses, grew revenue by 3% in the year ended March 2025. This is despite national television advertising revenue decreasing for the year, which means that eMedia increased its market share of the “advertising cake” that they refer to.

They have the highest market share in local prime-time audience viewing at 34.4%, above DStv at 30.5% and SABC at 26%. You can only show Anaconda so many times (yes, even you e.tv), so they have to spend a fortune on local content to maintain a prime-time audience that wants to enjoy South African storytelling. This pressure on content costs led to a drop in profits, as there just isn’t enough advertising growth to support the underlying increase in content spend.

So, with all said and done, HEPS fell by 10% to 45.63 cents. They make it clear that the dividend is important (HCI is very focused on upstreaming cash at the moment), so the dividend was only 6.3% lower at 15.00 cents. The low payout ratio is an indication of how capex-intensive this business is.

Frontier Transport is also part of the HCI stable. This is a solid business with a strong reputation for being an excellent operator of bus companies. This makes it quite a capex-intensive business though, particularly during a period of heavy investment in the fleet. They commissioned 19 electric buses into active service in the year ended March 2025 and those don’t come cheap.

The underlying business is doing well, with revenue up 16.5%. Operating costs increased by even more though, leading to EBITDA being only 10.9% higher – still a decent outcome.

The problem is that debt levels have shot up, leading to much higher net finance costs. This results in HEPS being down 3.5% for the period.

Despite the levels of debt and the pressure on earnings, the total dividend for the year was 30.4% higher. It’s hard to believe that this is the best thing for Frontier’s balance sheet as opposed to the best thing for HCI’s balance sheet further up. HCI holds roughly 82% in Frontier.

HCI’s hotel investment is the highlight (JSE: HCI)

And smaller oil and gas losses, if you can call that a highlight

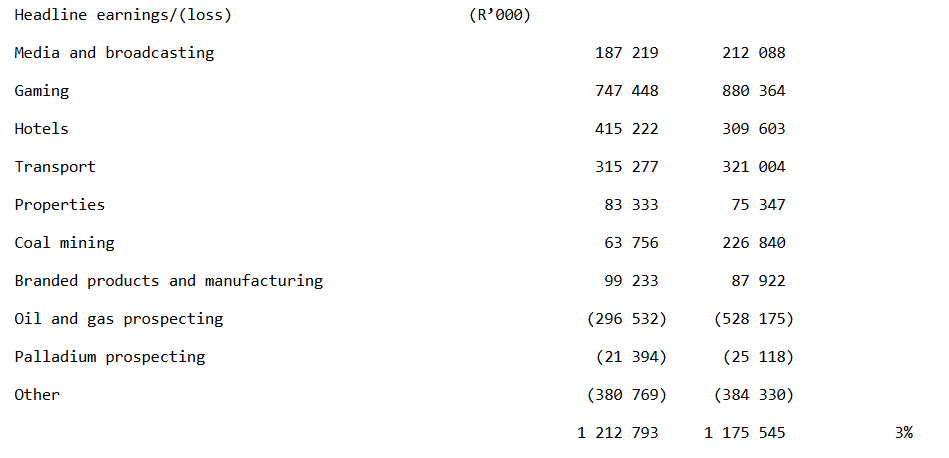

As you’ve probably noticed by now, Hosken Consolidated Investments (HCI) holds a number of listed and unlisted investments. The best way to reflect this is to just show you the numbers from the horse’s mouth. You can’t see it on the screenshot, but the numbers on the left are for the year ended March 2025 and are therefore the latest numbers:

As you can see, earnings were down in media and broadcasting, gaming (a major worry), transport (only slightly though) and coal mining (another major worry). The hotel investments were without a doubt the highlight, along with a much smaller loss in oil and gas.

The listed companies of relevance here are Tsogo Sun, Southern Sun, eMedia, Deneb and Frontier Transport Holdings, all of which have separately reported. Montauk Renewables is also a small contributor, along with Platinum Group Metals Limited and African Energy Corp. I’m not going to rehash each of those here.

Essentially, HCI finds itself in a situation where the gaming revenue (casinos) is at serious risk. The trajectory in that sector is a problem, evidenced by large impairments recognised on the underlying assets. Although the hotels offset most of that drop in this period, I would argue that gaming has further to fall than the hotels have to gain. Once you add on cyclical exposures like advertising (in media and broadcasting) and especially coal mining, you have a less-than-ideal base off which to be funding risky investments in oil and gas prospecting.

Head office non-current borrowings have jumped from R778 million to R2.6 billion. Combined with the pressure being put on the underlying businesses to maintain or increase their dividends, you would therefore expect to see the dividend at HCI being flat at best. But despite HEPS being just 3% higher, the HCI dividend for the year is up 70%. Yes, they have a very low payout ratio, but is this really the best use of capital when the share price is down almost 20% over 12 months?

These Lewis numbers are spectacular (JSE: LEW)

Is this a fluke or are they really a growth stock now?

For the longest time, Lewis has been a value investor favourite. They’ve done all the right things in terms of capital allocation, using share buybacks as a way to juice up returns to shareholders from otherwise modest revenue growth.

But now, as the results for the year ended March 2025 show us, Lewis is looking more like a growth stock. Revenue increased by 13.5%, gross profit margin was up 30 basis points to 43.4% and operating profit jumped by 66.9%. HEPS was up 60.3% to R14.83 per share, capping off a wonderful year. As icing on the cake, cash quality of earnings is evidenced by a 60% increase in the dividend.

Interestingly, return on equity is now at 15.4% vs. 9.3% in the prior period. This shows you that the group was previously earning sub-economic returns, which would’ve been the major reason for the subdued valuation. Even at 15.4%, I think they are still below their true risk-weighted cost of equity. Their medium-term target is 15%, which in my view is too low given the cyclical nature of the underlying business and the risks that it faces.

Credit sales were the growth driver here, up 12.1% vs. cash sales up 3.4%. Although some have pointed to the two-pot system to try and explain the recent Lewis numbers, the credit sales growth puts this argument to bed once and for all. Two-pot withdrawals would’ve boosted cash sales, not credit sales.

The debtors book looks healthy, with satisfactory paying customers at record levels as a percentage of the total book.

It really is a sign of the times at Lewis that there were no share repurchases in the second half of the year. But despite the share price being up more than 80% over 12 months, they are still only on a P/E of 5.6x!

Still no sparks at Old Mutual (JSE: OMU)

If you’relooking for excitement, you won’t find it here

Old Mutual released a quarterly update for the three months to March. As is usually the case, they are light on growth.

For example, Life APE sales dipped by 2%, in some respects due to the timing of lumpy corporate sales. On the plus side, gross flows were up 6% thanks to inflows in areas like wealth management and private clients.

Here’s the really ugly number though: net client cash outflow came in at R4.8 billion, a massive negative swing vs. positive inflow of R166 million in the comparable quarter. There was a R6.4 billion outflow from a large offshore investor. Although this is a low-margin indexation flow, it’s still a big number in the wrong direction. They also note R3.6 billion in outflows from the exit of unprofitable business in Old Mutual Corporate. There might be some cleaning of house here, but that’s still a really worrying net number.

Loans and advances were flat year-on-year, with Old Mutual’s cautious approach continuing.

And finally, gross written premiums grew 7%, with Old Mutual Insure as the star of the show with growth of 12% in premiums and an underwriting margin well above their 4% to 6% target range. The African business unfortunately dragged down the overall performance for this metric.

Old Mutual expects to launch its bank publicly later this year. I’m still not sure that South African needs another bank, but perhaps the group will surprise us with something interesting.

Sea Harvest’s earnings are up (JSE: SHG)

It’s anyone’s guess by how much

The rule for a trading statement is that a company must notify the market when they expect earnings to differ by at least 20% to the comparable period. Of course, most companies try and give a much tighter range than that. From time to time though, you see companies give the bare minimum disclosure i.e. that earnings will differ by at least 20%.

The trick here is that Sea Harvest is giving this guidance for the six months ending June. In other words, they are already so far ahead of the comparable period that they feel that they need to give this guidance to the market. As they conclude the period, they will give tighter guidance.

They have attributed this improvement to better catch rates, efficiency gains and sales price increases in the South African fishing business. These are all high quality reasons for growth in earnings, which is why the share price jumped 4% on this news.

SPAR is scaling back and trying to focus (JSE: SPP)

Two of the European businesses are up for sale

It’s been a long and painful post-COVID journey for SPAR. The share price is 36% lower than it was 5 years ago. I must remind you that this means it’s lost more than a third of its value since May 2020, back when the world was rather insane.

Poland was the worst part of the story, sure, but there have been other issues. SPAR has lost ground to the likes of Checkers locally, with Shoprite’s Sixty60 offering posing some serious questions about the relevance of SPAR’s convenience model. I still shop at my local SPAR because it’s quite brilliant really (shout out to the owners of SPAR at The Paddocks in Milnerton). The group level numbers tell a different story though.

To help clean up the group, they’ve decided to sell SPAR Switzerland (I’m not surprised at all) and Appleby Westward Group (AWG) in South-West England. The latter comes as a surprise, but perhaps SPAR has learnt from previous experiences and would rather sell a business that isn’t in dire straits.

This means that the continuing operations consist of SPAR Southern Africa and SPAR Ireland. For the 26 weeks to 28 March 2025, diluted HEPS from these businesses is expected to be between 0% and -15% lower than the previous year. You could also look at comparable earnings from continuing operations, which makes adjustments for the reporting calendar, in which case the expected diluted HEPS range is -5% to 5%. A further read suggests that both the Southern Africa and Ireland businesses saw improved margins and decent top-line performance in this period, with the translation of the Irish earnings into rand as one of the drags. We will have to wait for detailed earnings before jumping to any conclusions.

As for the discontinued operations, they’ve recognised R4.2 billion in impairments in anticipation of selling these businesses. This comes after the loss on disposal of R531 million in Poland. SPAR is essentially drawing a line in the sand here, cementing itself as a great example of disastrous offshore expansion by a local retailer (an ever-growing club) and giving itself a base off which to recover.

If you include the discontinued operations, diluted HEPS fell by between -34% and -24%. There’s no way that they could release numbers like this without it being accompanied by a plan to stop the bleeding.

Come home, SPAR.

Nibbles:

Director dealings:

The business development director of AVI (JSE: AVI) received share awards and sold the whole lot worth R6 million.

An associate of the CEO of Spear REIT (JSE: SEA) bought shares worth R71k.

After 10 years as CEO, Gary Chaplin has resigned as CEO of KAP (JSE: KAP). He certainly guided them through some pretty crazy times, not least of all the collapse of major shareholder Steinhoff. There’s always a mix of good news and bad news at KAP, so this wouldn’t have been an easy decade. CFO Frans Olivier is stepping up to the top job with effect from 1 November 2025. He’s been with KAP for 19 years, so there’s plenty of institutional knowledge there.

There is minimal liquidity in the stock of Afine Investments (JSE: ANI), a REIT focused primarily on owning forecourts. They have properties across four provinces. Although distributable earnings increased by 13.24% overall for the year ended February 2025, the thing that really counts (the dividend per share) was actually down 0.24% vs. the comparable period.

Clientèle (JSE: CLI) had to make some tweaks to its funding structure for the Emerald Life acquisition. This necessitated a shareholder vote. The resolutions achieved almost unanimous approval.

Stefanutti Stocks (JSE: SSK) is still in the process of disposing of SS-Construções (Moçambique) Limitada. As reported in the recent group financials, this is one of the key steps in the financial restructuring of the group. The parties are currently renegotiating fundamental aspects of the deal like the purchase price and payment terms, with the period for fulfilment or waiver of the conditions precedent being extended to 30 June 2025.

Altvest (JSE: ALV) has published the financials for the Altvest Credit Opportunities Fund, which is the reference asset for the C preference shares (JSE: ALVC). They funded over 30 SMEs and extended over R240 million in structured credit in the latest period. This is an early-stage venture, but I would say that it is the most scalable of all the Altvest projects at the moment. They did at least make a profit before impairments this time around, but they have to get a lot bigger to cover their operating expenses. If you’re interested in what they are doing, you’ll find the report here.

Cash shell Trencor (JSE: TRE) is finally proposing the resolution for the winding-up of the company and the distribution of value to shareholders. A special dividend of 90 cents per share in anticipation of the winding-up has been declared.

Supermarket Income REIT (JSE: SRI) has gone through the process of internalising its management company. As part of this, they want to transfer their listing in London from the closed-ended investment funds category to the equity shares (commercial companies) category of the Official List. This may sound like just pushing paper around, but it does impact things like which companies they are compared to and which funds might be willing to hold them. There will also be a genuine cost saving, as there’s an additional regulatory burden that comes with the closed-end investment funds categorisation.

Tony Phillips has resigned as chairman of Mpact (JSE: MPT) with immediate effect. Sbu Luthuli, currently an independent non-executive director, will be taking his place. This came as a surprise to the company and they have amended the resolutions for the upcoming AGM accordingly.

Brikor (JSE: BIK) announced that results for the year ended February 2025 will be delayed until mid-June due to circumstances “beyond the board and management’s control” – whatever those might be.

As part of fixing the sad and sorry state of its balance sheet, Deutsche Konsum (JSE: DKR) has agreed that VBL will swap existing debt exposure of EUR 86 million for the issue of additional shares. There are of course various nuances at play here. They aim to finalise the overall restructuring negotiations by August 2025, with the hope being to reduce the expected property sales until 2027.

Globe Trade Centre (JSE: GTC), which has close to zero liquidity in its shares on the JSE, released results for the three months to March. Rental revenue was up 9%, but funds from operations as well as profit dipped significantly year-on-year. The net loan-to-value ratio remains high at 52.1%. There’s also been a change in management, with the supervisory board resolving to replace the president of the management board. Corporate governance structures are quite different in Europe. With an upcoming bond repayment of €500 million in 2026, the board has also decided to suspend dividends at the fund. All is not well.

British American Tobacco unlocked a casual R25 billion in cash in one morning (JSE: BTI)

This is where capital markets shine

British American Tobacco confirmed on Tuesday that they would be selling down a small part of their stake in Indian group ITC. They did this in 2024 as well, raising plenty of cash in the process. History has repeated itself, with a successful block trade of 2.5% in ITC for £1.05 billion (around R25 billion) on Wednesday. This shows you just how deep capital markets can be.

Aside from reducing debt, they will also put an additional £200 million towards share buybacks, taking the total share buyback programme in 2025 to £1.1 billion.

This is a classic capital allocation shift, which isn’t a surprise given that British American Tobacco has to focus on maximising shareholder returns right now from sources other than meaningful revenue growth.

Burstone remains focused on driving fee revenue (JSE: BTN)

The decrease in distributable income per share is in line with guidance

Burstone Group is following a rather interesting strategy. Perhaps driven by their underlying DNA from the Investec days, they understand that return on capital is the ultimate driver of value. Increasing the returns without investing capital is therefore a desirable strategy, with the group putting together various investment platforms that they manage on behalf of co-investors. This earns fee revenue without requiring major balance sheet investments.

For the year ended March, fee revenue grew by 40%. It now contributes 10.7% of distributable earnings, up from 7.3% a year before. Third party assets under management increased 2.6x over the past year. This is the crux of the investment thesis at Burstone, with partnerships being put in place with massive global investors like Blackstone.

They are also putting together a South African fund with a cornerstone investor. Due diligence has been completed, with only investment approval processes remaining. Burstone will look to seed this platform with up to R5 billion of its South African assets.

As great as this all is, distributable income per share fell by 3%, in line with guidance. The group upped the payout ratio to 90%, which means that the cash dividend per share actually increased by 3.1%. They can’t increase the ratio every year of course, so earnings growth needs to come through. They expect growth of between 2% and 4% in the coming year.

The balance sheet is worth a nod, with the loan-to-value ratio down from 44% to 37%, or 36.3% if you allow for the proceeds on properties that are currently being transferred.

Due to substantial fair value and other adjustments, the NAV per share has dropped by 23.8% to R11.78. The current share price is R8.80.

Decent numbers and a new CEO at Emira Property Fund (JSE: EMI)

This is one of the more diversified funds you’ll find on the JSE

Emira Property Fund has exposure to South Africa, Poland and the US. They also hold a mix of office, retail, industrial and even residential properties. If you’re looking for a highly focused REIT, this isn’t the one for you.

The year ended March 2025 was one of asset disposals in the local portfolio, with R2.8 billion sold and transferred and another R628 million under contract for sale. This has helped to reduce debt, which is useful when rates are stubbornly high. Emira is also investing further in Poland.

The year saw a significant increase in NAV per share of 20.9%, driven by fair value gains on the Polish investment and higher property valuations. The dividend per share for the year is 5.9% higher.

And in case you’re wondering, the office sector is still struggling. Despite having mainly P- and A-grade offices, they suffered negative reversions of -9.3% (worse than -6.3% in the comparable period). At least vacancies came down from 10.9% to 8.4%.

I must point out that reversions were also negative in the retail and industrial portfolios, reflecting the level of diversification in the portfolio and the overall macroeconomic backdrop. To get positive reversions at the moment, you need to have a focused portfolio in the right places.

As part of the release of results, the company announced that non-executive director James Day will be appointed as CEO with effect from 1 July 2025.

They’ve struck gold at Goldrush (JSE: GRSP)

The company is part of the consortium that has been awarded the National Lottery Licence

Here’s some exciting news for Goldrush shareholders: the company is part of the consortium that has been awarded the licence to operate the Fourth National Lottery and Sports Pools for South Africa for 8 years. This is a big deal.

Goldrush as the listed company owns a 59.4% stake in Goldrush Group, which in turn is a 50% shareholder in Sizekhaya, the entity that has been awarded the licence. This interest in Sizekhaya will decrease to 40% once shares in the consortium have been issued to a government entity, as is the law.

The operator of the National Lottery promotes and sells tickets and makes payments to winners, while transferring the mandated portion of ticket sales to the National Lotteries Distribution Trust Fund.

This is obviously lucrative for Goldrush, with the share price up 46% year-to-date.

HCI expects a modest uptick in HEPS (JSE: HCI)

They are having a tough time at the moment

The Hosken Consolidated Investments (HCI) portfolio isn’t exactly a land of milk and honey right now. The share price is down 25% over the past year, reflecting problematic underlying exposures like the casino investments.

The oil and gas business is also still bleeding, with IOG and African Energy Corp incurring a loss of R262 million in the year ended March 2025. That’s better than R483 million in the prior year, but is still significant.

They expect HEPS to be in the range of -1.8% to +8.2% vs. the prior year.

HomeChoice to change its name to Weaver Fintech (JSE: HIL)

This is a sign of strategic intent and focus

What’s in a name? Shakespeare had his own views on these things. When it comes to markets though, some companies get really smart with this stuff (think of Ferrari and the stock ticker $RACE) and others don’t give it too much thought.

In the case of HomeChoice, the listed company name was past its sell-by date. HomeChoice is so much more than a catalog retailer these days, so I think it makes sense to shake off that moniker. Instead, they will be called Weaver Fintech Ltd going forward, adopting the name of the underlying financial services business that they have been busy building.

So, no prizes for guessing where their best growth opportunity is then!

Jubilee Metals gave a general update on Zambia (JSE: JBL)

They have plenty going on there

After extensive trials at Jubilee Metals’ Roan Concentrator, production commences this week under the long-term feedstock supply agreement. This seems to have inspired the company to give the market a broader update on the Zambian business.

They are proud of their technical outcome at Roan, as they are able to process material that the CEO notes is “deemed as waste or too complex by many operators” – and of course this gives them access to copper, which is the commodity that everyone is chasing at the moment.

The Munkoyo mining operation is targeting a step-up in output in coming months, with the run-of-mine (ROM) transported to Sable for refining. They are also planning an on-site processing plant.

The combined increase in copper production at Roan and Munkoyo means that they need to expand the Sable Refinery. They expect to be done with this expansion by the first quarter of 2026.

The Project G mine is much earlier in its journey. They are currently working on upgrading the resource (i.e. just getting a better understanding of what is there) and designing an open-pit expansion.

In terms of funding transactions, Jubilee previously announced that they’ve sold a portion of the resources at the surface of the Large Waste Project. The deal is worth $6.75 million, payable in tranches as the material is lifted. $600k has already been received. They are busy with negotiations with various potential funding parties regarding targeting modular processing units at the Large Waste Project, with such a structure preferred to the previous discussions with an Abu Dhabi investment firm.

As further capital raising activity, Jubilee sold one of its waste assets outside of its large copper tailings for $12.3 million, payable in tranches over 20 months. And although a much smaller source of funding, the issuance of £200k in shares to the former chairperson in lieu of cash fees (and as part of a performance bonus) also helps.

So, there’s plenty going on here. It’s incredible how Jubilee went from the talk of the town in 2022 to now trading at roughly a quarter of where it was in that period:

A bidding war is officially underway for MAS (JSE: MSP)

The offer from their joint venture partner has been improved

As I wrote at the time, the initial offer put on the table by MAS’ joint venture partner PK Investments was a bit daft. It was below the traded price of the shares and included the additional complicated of an inward listed preference share, which I can almost guarantee would have as much liquidity as the Sahara Desert.

In fact, the deal created the opportunity for Hyprop to have a sniff around MAS, while using it as an excuse to send their advisors off to raise some cash from the market in anticipation of a potential offer. Hmmm.

Now, with PK having been given a PK (I’m sorry, I can’t help myself) from the market in the form of nobody taking that offer seriously, they have increased the cash offer from EUR0.85 per share to EUR1.10 per share. The maximum cash amount has increased from EUR40 million to EUR80 million.

They are also working on “improvements” to the share instruments that would be inward listed. I just can’t see them finding much support for anything other than an all-cash deal.

Renergen has released the circular to regularise the ASP Isotopes loan (JSE: REN)

The Takeover Regulation Panel wasn’t happy with the terms

As a first step in getting the deal with ASP Isotopes across the line, Renergen needs to make some changes to the loan terms related to the amounts advanced by ASP Isotopes to keep the lights on at Renergen.

The original terms of the loan made reference to capital raising activities and the pending offer from ASP Isotopes. The Takeover Regulation Panel (TRP) sees this as coercive behaviour, with the worry being that shareholders of Renergen are essentially being forced into a corner to support the scheme. The parties disagree with the TRP’s assessment, but they also need to get a deal done here, so they’ve decided to rather amend the terms of the funding and move on.

This is why a circular has been sent to shareholders dealing with the resolutions required to amend the loan terms and ratify the funding arrangements. The actual scheme circular for the takeover will come further down the line, assuming they get over this first hurdle.

A flat dividend at Reunert (JSE: RLO)

And that’s the highlight of this story

Reunert released results for the six months to March 2025. Revenue fell 5%, operating profit was down 16% and HEPS decreased by 20%, so there’s little in the way of good news here. The only highlight is that the interim dividend stayed flat at 90 cents per share. This is really just a case of kicking the can down the road, as companies try hard to avoid cutting the dividend.

There were a number of reasons for the poor results. The battery storage market is right up there among the largest headaches, with the disappearance of load shedding leaving many energy businesses stranded. Reunert has decided to dispose of Blue Nova Energy. Deciding to sell something and actually selling it are two different things.

At least one of the issues sounds more like a timing thing than anything else, being the deferment of the fuze contract into the second half of the year. That’s encouraging, but it doesn’t offset the other issues like weak power cable sales.

Another notable point is that there was a COVID insurance claim in the comparable period, which impacts the year-on-year comparability of results as this is obviously a non-recurring item.

It’s all to play for in the second half of the year, with management giving a bullish outlook. This confidence is informing the decision to keep the interim dividend steady. The share price is down 20% year-to-date, so the market doesn’t seem to be feeling quite as positive.

Tiger’s roar grows louder (JSE: TBS)

The turnaround is being executed beautifully

Tiger Brands has enjoyed a ~70% increase in the share price over the past 12 months. The turnaround is clearly working, as further evidenced by results for the six months to March 2025.

Revenue growth of 2% may not sound like much, but it works when combined with all the efforts made in improving the efficiencies of the underlying portfolio. Tiger is a different business these days, boasting a 23% reduction in SKUs (the number of different products) and a jump in operating margin from 7.5% to 9.6%. This was good for a 30% increase in operating income and 34% in HEPS!

Efficiencies lead to better return on capital, with Tiger’s ROIC increasing from 13.8% to 15.7%.

As you dig into the underlying segments in the excellent results presentation, you find encouraging signs like higher operating margin of 7.8% in Milling and Baking (vs. 5.7% the year before). The jump in Grains is even more impressive, with operating margin improving dramatically from 0.8% to 6.4% despite flat revenue!

In many ways, the Grains business is reflective of the broader theme at Tiger Brands of this recovery: turning modest revenue growth into meaningful growth in profits.

As the cherry on top, there’s a special dividend of R12.16 per share. It’s interesting that they chose this route instead of a large share buyback programme. With Tiger trading at an elevated valuation based on the turnaround progress, is this perhaps a sign that things have gotten a bit too hot in the share price kitchen?

The clouds have covered Tsogo Sun (JSE: TSG)

Casino assets aren’t what you want right now

Tsogo Sun has released a pretty ugly set of results for the year ended March 2025. Income was down 3% and costs were up 1%, so adjusted EBITDA fell 11% and HEPS took a 16% knock. The final dividend per share was down 25%, showing that management doesn’t have tons of confidence right now.

And why should they? Tsogo Sun is stuck with a portfolio of assets that was fantastic many years ago when people were still enjoying casinos, but things have changed. Combined with a net debt to EBITDA ratio of 2.09x (not insignificant), they are sitting with plenty of risk here.

The business still makes money, as evidenced by an adjusted EBITDA margin of 31.1%. Margins are under pressure though and it’s quite difficult to see how that will improve. One of the potential catalysts for growth would be if Tsogo Sun can get the approvals for investment in casino assets in the Western Cape, as there’s just one casino serving the Cape Metropole.

Perhaps worst of all, Tsogo Sun is disappointed with its online division’s performance. This is the only growth area in the business and they are still only break-even on adjusted EBITDA level, having suffered a R27 million write-off based on cash management and reconciliation issues.

I quite enjoyed this comment at the end of the management report:

Look, when you have to cut your dividend in order to reduce debt, I’m really not sure how it can be seen as anything other than negative. If the business was performing well, they would be able to reduce debt AND pay higher dividends.

Nibbles:

Director dealings:

I see that Standard Bank (JSE: SBK) execs are hitting the sell button again. This time, two prescribed officers sold shares worth a total of R23.6 million.

The Chief People Officer (yes, that’s the official title) of AngloGold Ashanti (JSE: ANG) sold shares worth a substantial $1.2 million. Some of this was related to a share award, but the total amount is higher than even the full value of the award, let alone the taxable portion.

A prescribed officer of Barloworld (JSE: BAW) sold an entire share award worth R1.3 million,

A director of a major subsidiary of Altron (JSE: AEL) and the company secretary of the listed company bought shares worth a total of nearly R700k.

The executive chairman of Southern Palladium (JSE: SDL) bought shares worth around R225k.

An independent non-executive director of Stefanutti Stocks (JSE: SSK) bought shares worth R165k and a director bought shares worth R125.7k. Given how speculative this company is at the moment, that’s a positive signal.

Junior mining houses frequently give presentations at mining conferences, as they need to ensure that their projects are on the radar of potential investors. Southern Palladium (JSE: SDL) presented at the Junior Mining Indaba in Johannesburg and you’ll find the presentation here.

Altvest’s trading statement deals with each share class (JSE: ALV | JSE: ALVA | JSE: ALVB | JSE: ALVC)

The credit opportunities fund seems to be the pick of the litter

When you look at Altvest’s trading statement, you may feel overwhelmed by the number of different share classes. This is because the company’s model is to list a separate preference share instrument for each underlying investment, with the Altvest holding company’s ordinary shares being listed as well.

The trading statement for the year ended February 2024 deals with each share class separately. They base the disclosure on NAV per ordinary share, as is the market norm for an investment holding company. I do think that Altvest is somewhat of a hybrid though, as what they are doing (which is very startup in nature) is different to how I would view a standard investment holding company.

The net asset value per share for the ordinary shares will be between 44% and 64% higher, which is significant. Moving into the preference shares and starting with the A shares, which reference Umganu Lodge, the NAV per share will be between 3% lower and 17% higher. The B share references the Bambanani Family Group restaurants, where things are going wrong and restructuring is under way, evidenced by the NAV per share plummeting by between 50% and 70%. I remember that there were nasty losses in that business in the interim period. As for the C shares, which related to the credit opportunities fund, there’s a useful uptick of between 11% and 31% in the NAV per share.

Altvest is still early in its journey. The credit opportunities fund seems to be the best opportunity at the moment.

Bidcorp has grown off a demanding base (JSE: BID)

This really is one of our best exports

Regular readers will know that most management teams on the JSE have a pretty sketchy track record when it comes to offshore expansion. Bidcorp is an exception of note, with over 90% of revenue sourced outside of South Africa. Through a consistent strategy of bolt-on acquisitions rather than betting the farm on any one particular deal, they’ve grown beautifully.

The latest trading update reflects the year-to-date numbers for the 10 months to April 2025. They are up against a strong base, as the FY24 results were solid and there has been little in the way of food inflation this year to boost revenue. Despite this, trading profit growth is around 10% for the period under review and HEPS is also up by 10% on a constant currency basis.

The rand has been stronger recently, so that’s actually had a negative impact on Bidcorp of around 3.8% year-to-date. You win some and you lose some when it comes to currencies, so I agree with management’s view that constant currency numbers are the best choice for assessing performance.

Revenue is up 6.7% in constant currency, of which 4.6% is due to organic growth and 2.1% is from acquisitions. EBITDA margin improved by 20 basis points to 5.8%.

Bidvest has achieved these numbers against a backdrop of significant pressures on consumer budgets, resulting in a dangerous cocktail of weak demand from consumers and a need for ongoing inflationary increases for staff. This hurts margins, with Bidvest having to swallow this issue in some markets to protect volumes. This makes the group margin performance even more impressive.

It’s interesting to note that emerging markets have had a relatively stronger period than developed markets. The major exception to this is China, where they note that conditions remain challenging. Discretionary consumer spending in China has been a headache for so many companies in recent times. The major headache on the developed market side is Australasia, where Bidcorp is dealing with a market that is suffering from weak consumer demand and pressure on hospitality in New Zealand. I don’t think it helps that New Zealand is about 3 – 5 business days away from basically anywhere that isn’t Australia or China.

The group has invested a net R5.6 billion over the period, split equally between maintenance and expansion capex. They aren’t exactly slowing down with acquisitions either, with a total of 10 bolt-on deals year-to-date at a cost of R1.1 billion.

The share price is up 13% over the past year. Given the relative strength of the rand, that speaks volumes about the strength of the underlying business.

British American Tobacco is reducing its stake in ITC (JSE: BTI)

They already did something similar last year

In 2024, British American Tobacco sold part of its stake in Indian company ITC for around $2 billion, which Reuters notes was India’s third-largest block deal ever. These are serious numbers.

On Tuesday afternoon, the company responded to press speculation regarding another sell-down of the stake. A couple of hours later, full details were released.

Through its Indian subsidiary that holds the stake, British American Tobacco will sell a 2.3% stake in ITC via an accelerated bookbuild. This will help the group reach its target for net debt to adjusted EBITDA of between 2x and 2.5x. They will also use the proceeds to increase the current share buyback programme by £200 million to £1.1 billion.

After the sale, British American Tobacco will be left with a 23.1% stake in ITC, an investment that goes back to the early 1900s!

I would rather work at Coronation than own the shares over the long term (JSE: CML)

A 7% increase in operating costs isn’t “tight expense management”

Coronation is struggling to grow. Although they keep blaming the South African savings culture, I also see little evidence of them doing anything about their business model. If the assets aren’t coming to you, then shouldn’t you be going out there to find them?

At least this period saw a decent financial performance, with average AUM up 9% and revenue up 8%. Total operating expenses increased by 7%, which is below revenue but still above inflation. My worry is that they describe this as “tight expense management” based on underlying people costs. This immediately tells me that Coronation is a business with slow growth and expensive human capital, a combination that they seem quite happy to live with. There’s nothing tight about above-inflation cost increases.

If this sounds more like a fixed income investment profile than an equity investment to you, then you aren’t alone in that thinking. The market values Coronation in such a way that the dividend is usually the bulk of the return. The interim dividend increased by 8% to 200 cents per share and if we annualise that, then Coronation is trading on a forward yield of 10%.

Combined with the share price growth in the past year, it’s been a great return over 12 months. I just can’t help but wonder what they might achieve if they put in a serious focus on growing assets, particularly as they are so proud of their track record of fund performance. Over 5 years, the share price is slightly in the red and shareholders have been fully reliant on dividends for their returns.

Datatec had a pretty spectacular year (JSE: DTC)

Revenue growth is the last metric to look at here

Revenue growth is usually the right place to start when assessing company performance. At Datatec though, it doesn’t tell the right picture for the year ended February. A change in accounting policy has impacted the way that revenue and cost of sales are recognised, with no net impact on gross profit. Thus, gross profit is the metric that will help you understand the numbers.

It really was a great year for the group, with gross profit up 5.6% and EBITDA up 24.6% – both measured in US dollars. HEPS jumped by 79.6 cents! The dividend per share is measured in rand and increased by 53.8% to 200 cents. This is why the share price is up 60% in the past year.

There are several drivers of this growth, including the AI boom and how it is driving a need for “generational” change in infrastructure.

Looking at the underlying segments, Westcon International grew adjusted EBITDA by 24.7%, with particularly strong growth in Asia-Pacific. Logicalis International achieved adjusted EBITDA growth of 26.8%, while Logicalis Latin America saw a jump of 59.5% in adjusted EBITDA.

The trend in margins is expected to remain positive, with a greater proportion of revenue coming from software sales and annuity services. Along with the benefit of more cash sitting at the centre of the group, this has inspired management to increase the dividend payout ratio from 33.3% to 50% of underlying earnings.

Harmony makes a giant leap in copper (JSE: HAR)

Everyone wants a piece of this metal

When it comes to commodities, copper is firmly in vogue at the moment. Harmony Gold has already diversified into this metal and they certainly aren’t playing around, announcing the acquisition of MAC Copper for a meaty $1.03 billion (over R18 billion).

The underlying asset is the CSA Copper Mine in New South Wales, Australia. This mine is a high-grade copper asset and is obviously in a stable jurisdiction where the infrastructure works. The operating free cash flow margin is 36%, so this is a profitable and lucrative mine. With a reserve life of 12 years and exploration potential, the hope is that the cash will continue for a long time. This is a complementary asset for Harmony, as they have other assets in the region including Eva Copper in North-West Queensland.

Despite the size of the deal, Harmony’s net debt to EBITDA is expected to stay within the target range of below 1x. They will finance the transaction with a $1.25 billion bridge facility and existing cash reserves. They will refinance the bridge funding in due course.

MAC is listed on the New York Stock Exchange and the Australian Stock Exchange. The offer price is a 32.1% premium to the 30-day VWAP, so Harmony is paying up for the asset. This isn’t an unusual control premium, but the market does tend to get nervous of swashbuckling deals in the mining space. Harmony closed 4.6% lower on the day.

The MAC board is unanimously in favour of the deal and will propose it to shareholders as a scheme of arrangement. Holders of roughly 22.5% of shares outstanding (directors and key shareholders) have indicated that they will vote in favour of the scheme.

A number of large mining groups have positioned themselves around copper. I hope that the supply-demand dynamics will work out the way they expect them to.

Insimbi Industrial Holdings is having a tough time (JSE: ISB)

There are nasty losses and they seem to be in breach of covenants

Insimbi Industrial Holdings has released an updated trading statement for the year ended 28 February 2025. It tells a sad and sorry tale, with a headline loss for the period that could be as bad as -7.75 cents per share. That’s significant when the share price is R0.61 (having closed 11.6% lower in response to the news).

The loss per share (rather than the headline loss per share) is much worse than that, driven by impairments. This tells you that the underlying business is struggling. The far more worrying note in the update is around covenants, with Absa agreeing to relax covenants up to February 2027.

Although we will only know for sure when detailed results come out on 30 May, bankers don’t generally relax covenants unless a company is already in breach. It’s obviously great to see that the banks are giving them some breathing space, but that’s still an unpleasant situation to be in.

Novus has had a decent financial year (JSE: NVS)

Investors must be patient for a couple more weeks for detailed results

Novus released a trading statement for the year ended March 2025. HEPS is expected to be between 6.1% and 18.1% higher. That’s a wide range at the moment, as the group is still finalising the results for release on 13 June 2025.

The reason for the trading statement (which is triggered by a difference of at least 20%) is that Earnings Per Share (EPS) will be between 40.1% and 52.1%. This gets skewed by all kinds of once-off adjustments, hence the market generally focuses on HEPS.

Strong growth and margin expansion at Pepkor (JSE: PPH)

But keep an eye on Avenida

Pepkor has released interim results for the six months to March. At group level, they tell a great story – revenue growth was up 12.8% from continuing operations and gross margin expanded by 110 basis points to 39.2%. HEPS was good for 12.4% growth. If you adjust for the normalised tax rate, then HEPS was up 18.9% – a solid outcome indeed.

If you include discontinued operations and you don’t normalise for the tax impact, then HEPS was only up by 8.5%. I don’t like brushing over these things, but that’s not a great indication of how well the core business is performing.

Like-for-like sales growth is my preferred metric in the retail world. PEP was a highlight here, up 11.9%, with Ackermans putting in a solid 9.6% performance. Speciality was good for 4.2% and Lifestyle managed 6.3%. As for the non-SA businesses, PEP Africa was up 21.3% in constant currency, while Avenida was down 1.8% in constant currency. As you can see, Avenida is the only blemish on this period, with the Brazilian retailer slowing down its store expansion programme in order to refine the business model.

Credit sales growth continued to outpace cash sales growth, with the proportion of credit sales increasing from 13% to 15% of total revenue. This has driven a 67.3% increase in revenue from financial services, while Pepkor continues to beat the drum of its “credit interoperability” strategy. They also have cellular and insurance businesses that are helpful contributors. In the informal business, which rolls up into the broader fintech play, the Flash business achieved a 23.6% increase in throughput.

They aren’t sitting on their hands. Pepkor is looking for new areas of growth, like through the recent acquisition of Choice Clothing that gives them an off-price business. They are also looking forward to having Shoprite’s furniture business in the group, with that acquisition having been announced in September 2024. But most of all, Pepkor wants to improve its market share in adult wear categories, including a rebrand of Ackermans womenswear stores to the Ayana brand and of course the recently announced acquisition of Legit and other businesses from Retailability.

Aside from the headaches in Brazil, this was a great set of numbers that sets them up strongly for the rest of the year.

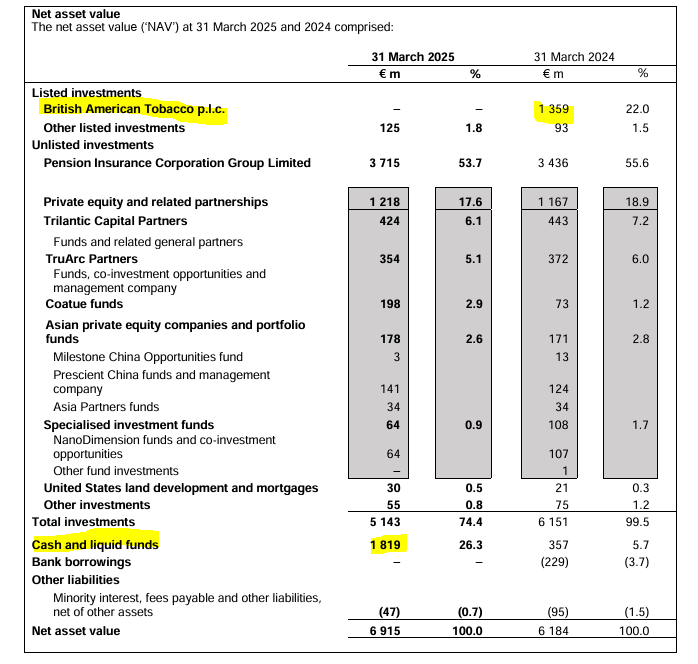

Reinet’s NAV and dividend have increased (JSE: RNI)

The group is firmly in a new era

In a major step, Reinet recently sold its entire stake in British American Tobacco. They held this asset since being spun-off from Richemont in 2009 and received a whopping €2 billion in dividends over the years before finally letting it go. By their calculations, the annualised return from this investment was in excess of 11%.

As was recently pointed out to me by a well-respected local investment professional, this means that British American Tobacco was a stronger performer than the rest of the Reinet portfolio. Since 2009, the total portfolio only grew its net asset value by 9% per year including dividends. In other words, with British American Tobacco no longer part of the Reinet story, they will need to improve their capital allocation in other assets.

The other major asset is Pension Corporation, which has had a strong year. This has been the primary driver of the 11.8% increase in Reinet’s net asset value from March 2024 to March 2025. It’s also worth noting that the Reinet dividend is 5.7% higher vs. last year.

The group has also been allocating capital to other institutional managers, with a variety of specialist offshore funds that have caught the eye of Reinet over the years. As the group inherited the British American Tobacco asset from a previous life, the management team’s track record will be measured based on what they achieve beyond that asset.

It’s worth looking at this net asset value summary, as it represents a new era in which the British American Tobacco stake was transformed into a huge cash pile instead:

Stefanutti Stocks remains speculative, but profits have moved much higher (JSE: SSK)

The balance sheet is still on a knife’s edge

Stefanutti Stocks is quite a wild thing. The share price is up nearly 300% in the past 12 months, which is a wonderful example of the potential rewards at play when you’re willing to gamble on an absolute basket case of a company. It looks better than it did a year ago, but remains a high-risk punt.

An 8% increase in contract revenue from continuing operations was good enough to drive a rather daft 700% increase in profit from continuing operations. There was an equally daft deterioration of 656% in the loss from discontinued operations, but thankfully the relative size of continued and discontinued operations means that profit from total operations jumped from R15.9 million to R131.5 million (up 727%, in case you were wondering).

HEPS improved from a loss of 55.73 cents to positive earnings of 109.36 cents, which explains why the share price rose so sharply from R1.15 a year ago to close at R4.27 on the day of these results.

To make this rollercoaster ride even more interesting, the group’s current liabilities exceed its current assets by R1.3 billion. This is why there’s a restructuring plan in place that includes various elements, one of which is a potential equity raise.

For now, lenders have extended the loan to June 2026. Priced at prime plus 5.1%, the bankers are making a delightful amount of money while watching this story play out. This has allowed the group to prepare its accounts on a going concern basis, with the bankers taking a juicy first bite of this partially rotten cherry and shareholders getting the rest.

As great as the return has been over the past 12 months, they aren’t out of the woods yet. The restructuring plan includes some difficult elements that aren’t all within the company’s control, ranging from the disposal of the Mozambique business through to legal disputes.

Zeda pulled a margin rabbit out of the hat (JSE: ZZD)

As a shareholder, I’m pretty happy with this

My local automotive sector exposure is a combination of WeBuyCars and Zeda. WeBuyCars gives me a focused play on car sales (only used, not new) and Zeda delivers exposure to the rental market, with used sales as part of their business but not their core focus.

I believe that WeBuyCars is the better quality business. When it comes to Zeda, a big part of the appeal for me is the low multiple that the share is trading on. Over the past year, Zeda has all the makings of a value trap vs. WeBuyCars which has been a wonderful position for me:

I’m pleased to say that WeBuyCars has been the higher conviction position for me and sized accordingly. It’s much bigger in my portfolio than it used to be, thanks to that share price performance!

“Cheap” stocks like Zeda can take a long time to blossom, as they need to achieve consistent enough results that the market takes notice. For the six months to March, a top-line performance of a 1.6% drop in revenue isn’t going to attract too many growth investors. Used vehicle sales were the source of the pressure, with Zeda managing to sustain performance in their rental business.

But here’s the good news: thanks to the changing mix and management’s overall efforts, gross profit margin improved by 200 basis points to 43% and gross profit was up 4.6%. Operating profit was up 5.4% and margin improved by 100 basis points to 16%. Sure, there are some iffy line items like a dip in EBITDA, but what I really care about is HEPS – and that was up by a lovely 11.2%.

This puts interim HEPS on 184.1 cents. Now, in a business as seasonal as car rental, you can’t just annualise the interim number. Instead, a last-twelve-months basis is appropriate, which you calculate by taking the second half of the previous year and adding it to this interim period. They made full-year HEPS of 312 cents last year and interim HEPS of 165.5 cents. This means that the second half of the year (which isn’t the peak tourist season) was a contribution of 146.5 cents.

Adding that to the latest interim number gives us HEPS over the last-twelve months of 330.6 cents. Zeda closed 3.7% higher on Tuesday to trade at R12, which puts it on a Price/Earnings multiple of 3.6x. Yes, multiples can stay “cheap” for a long time, but not if underlying HEPS growth continues. I’m also quite happy to bank an interim dividend of 55 cents per share along the way.

In the second half, I would like to see a normalisation of the balance sheet. They took on debt and increased the fleet size right near the end of the interim period, so the earnings related to that increased capacity haven’t come through yet. This spiked the net debt to EBITDA ratio to 1.9x (from 1.5x) and took return on equity down from 28.5% to 21.8%.

Nibbles:

Director dealings:

A2 Investment Partners, the activist shareholder and associate of Andre van der Veen who is the chairman of Nampak (JSE: NPK), bought shares worth almost R13 million in the company.

Gerrie Fourie (who is retiring as CEO) sold R8.9 million worth of shares in Capitec (JSE: CPI).

An associate of the COO of Afrimat (JSE: AFT) bought shares worth R74k.

Copper 360 (JSE: CPR) has appointed Graham Briggs as the new CEO, with effect from 1 June 2025. Controlling shareholder and current CEO Shirley Hayes appears to have spearheaded this appointment.

Wine in Focus is an Investec Focus Radio five-part vodcast series hosted by Lerato Motshologane, a dealmaker at Investec for Business and founder of Discover Wines.

To coincide with Investec’s sponsorship of the Trophy Wine Show, we recorded this from Grande Roche, in the stunning Paarl winelands.

Lerato chats to wine makers, investors, farmers and judges on everything from how to invest in wine, to innovations changing the way we farm, and South Africa’s growing prominence on the international fine wine market.

In Episode 1 of this series, you can listen to Johan Malan from Wine Cellar, Mike Ratcliffe (co-founder of Vilafonté) and Investec’s Roy van Eck as they discuss how to invest in fine wine. They cover how you tell the difference between a premium vintage and plonk, how to age wine, a wine bond, and their hopes for SA’s wine industry.

If you enjoy this, be sure to visit this page for more information and for upcoming episodes.

Lerato Motshologane works at the intersection of finance and fine wine. As a dealmaker at Investec for Business, when she isn’t shaping funding solutions for her commercial clients, she’s promoting and trading in South Africa’s finest wines. As founder of Discover Wine, she’s passionate about educating the local consumer about the value and quality of our wines and enjoys hosting international wine lovers in our beautiful winelands.

The African Rainbow Capital Investments offer found very few takers (JSE: AIL)

Many shareholders will move into unlisted territory

You may recall that when the offer to shareholders of ARC Investments was announced, I noted that it felt like a cheeky price. The mental gymnastics that were used to determine the offer price as being fair were even more impressive.

The rather pitiful take-up of the offer tells you that the price was low. The offer was accepted by holders of just 18.64% of shares eligible to accept the offer, or fewer than 1 in 5 shares. This works out to 6.31% of total shares, giving the offerors a stake of 55.13% as they move into the unlisted environment.

This means that a large number of shareholders will hold unlisted shares, presumably holding on for a big payout down the line from assets like Tyme. If liquidity discounts were a problem while the company was listed, then you can imagine what it will be like when unlisted.

Altron is focusing firmly on profits (JSE: AEL)

There might not be much revenue growth, but just look at HEPS

Altron has released results for the year ended February. If you exclude the sale of the ATM business, revenue was up just 3%. That doesn’t sound exciting at all, yet HEPS from continuing operations was up by a whopping 73%. This was driven by an increase in gross margin of 200 basis points and a 50% increase in operating profit thanks to solid cost control.

The percentages just get silly if you look at the group including discontinued operations, with HEPS swinging from a loss of 25 cents to positive 134 cents. Interestingly, the dividend is up by 52% though, so perhaps that’s the right measure to look at.

Within the group, Netstar grew EBITDA by 17% thanks to subscriber growth of 16%. With 91% of its revenue being of an annuitised nature, Netstar is a strong business. At Altron FinTech, they enjoyed EBITDA growth of 38% thanks to the SME customer base and the associated growth in transactions. Altron Document Solutions has now been reclassified as a continuing operation and that’s not the worst thing, with EBITDA swinging from a loss of R74 million to positive R84 million.

If you start digging deeper into individual businesses within these segments, then you get the typical mix of good news and bad news. This isn’t unusual for large companies. The important thing is that group profitability has improved and so has the balance sheet, with a notable 58% increase in net cash and cash equivalents.

The outlook statement does include a word of caution about growth in FY26 given the broader operating environment. They don’t give specifics on what the impact might be. Medium-term margin targets are still in play, as is the dividend policy of paying out at least 50% of HEPS.

Barloworld’s HEPS decline: from Russia, with no love (JSE: BAW)

At least EBITDA margin moved higher excluding VT in Russia

Barloworld has released results for the six months to March. Given the underlying offer to shareholders that still hasn’t reached enough acceptances for it to go ahead, these numbers are particularly important. Shareholders that haven’t accepted the offer need to decide whether there’s enough in here to justify hanging onto the shares in the hope of a better return down the line.

Including the Russian business tells a sorry tale. Group revenue is down 5.8%, EBITDA fell by 9.1% and HEPS took a nasty 20.5% drop. The ordinary dividend is down dramatically from 210 to 120 cents per share, a drop of 43%. It’s important to look through the noise though to assess how the group is doing excluding Russia, as that’s the best indication of whether the offer price is appealing.

Revenue excluding Russia fell by 2.2% and EBITDA was up 3.0%. This means that EBITDA margin expanded from 11.9% to 12.5%. Normalised HEPS excluding Russia was flat at 356 cents per share.

The Equipment Southern African business warrants its own discussion, as EBITDA fell by 6.9% to R1.3 billion. The EBITDA profit margin was down by 10 basis points to 11.5%. They attribute this to a change in sales mix.

The most important growth asset in the group is Equipment Mongolia, which saw EBITDA improve by 14.5% to R549 million. Still, EBITDA margin of 23.0% was below the prior period margin of 24.7%.

Ingrain also deserves a mention, with EBITDA up 10.1% to R411 million and margin expanding from 11.7% to 12.9% due to cost reduction measures.

This means that although group margin improved excluding Russia, this was due mainly to mix effects rather than stronger margins in the underlying businesses. Sure, Ingrain went in the right direction, but it’s also the smallest segment. Equipment Mongolia grew strongly and runs at a much higher margin than the other segments, hence it now contributes a higher percentage of group EBITDA and the change in mix drives a higher EBITDA margin.

There are of course some other businesses in the group, but they are too small to really feature in any decisions for shareholders here.

Annualising HEPS in such a cyclical business is dangerous at best, but the FY24 numbers were a surprisingly evenly split between H1 and H2. So, if we simply double this interim HEPS of 423.2 cents, it gives us indicative forward earnings for FY25 of 846.4 cents. The offer price is R120 per share, a forward earnings multiple of 14.2x. As I’ve written a few times now, if I was a Barloworld shareholder, I would take the offer and run. Each to their own.

As a further overhang from Russia, the deadline for the voluntary self-disclosure to the US Department of Commerce’s Bureau of Industry and Security (BIS) has been extended from 2 June to 2 September. I am no expert in this space, but I suspect that the word “voluntary” is working hard here.

Blue Label Telecoms highlights the Cell C business model (JSE: BLU)

The journey to a separate listing has begun

Blue Label Telecoms has started the process of getting the market used to Cell C as a standalone entity. They are looking to restructure and separately list the company, which means they need to drum up investor support for it.

Cell C has completely repositioned itself to be a capex-light buyer of network capacity. This feels at first blush like a market position that is ripe for disintermediation, but in practice I can imagine why it wouldn’t make sense for each partner (e.g. retailers selling cellphone products) to engage with each network. Cell C does all the hard work in the middle, creating an easy solution for companies with strong distribution channels who want to get a piece of the action here.

I will note that the “smarter” and more capex-light the business model, the greater the chance of attracting competitors. Cell C has over 90% MVNO network share, which is an extraordinary market share that will be hard to defend over time from disruptors.

Still, it’s great to see Cell C doing so well and it’s especially good to see the slick branding and the overall smell of success that the business gives off, a most welcome change from the stench of failure that followed it around for so many years.

I recommend that you at least flick through the presentation here.

A juicy jump in HEPS at Dis-Chem (JSE: DCP)

Full details will be availablelater this week