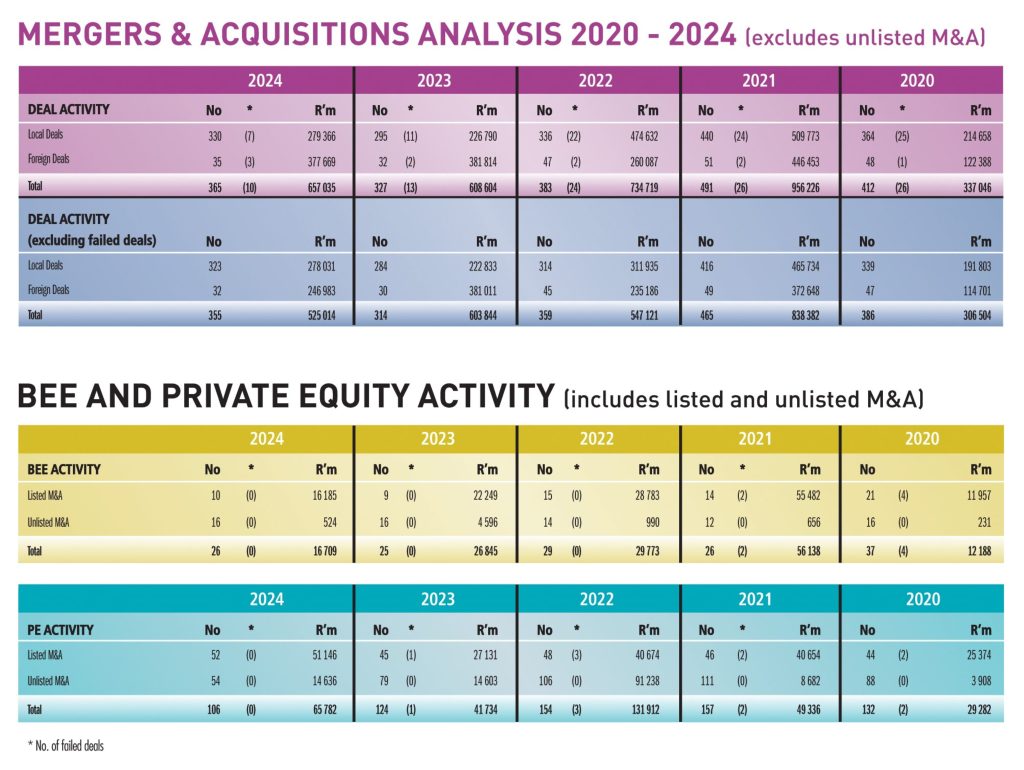

South African M&A activity in 2024 showed an improvement when compared with the previous year, with a favourable re-rating of equity prices due to a combination of economic and political stabilisation and sectoral growth, which in turn increased investor confidence.

Deals announced during the year increased 12% to 365 deals valued at R657 billion (2023: 327 deals valued at R608,6 billion). R377,7 billion of this total value represented deals by foreign companies with secondary listings on the JSE. 10 deals failed – the largest by value being Mondi’s proposed acquisition of DS Smith valued at c. R123 billion. The real estate sector remained buoyant, accounting for 34% of M&A activity in South Africa during 2024. This trend underscores ongoing investor confidence in the country’s property market, with significant transactions contributing to the sector’s dynamism.

High profile deals during the year included Groupe Canal+’s acquisition of MultiChoice – which won the award for Deal of the Year – Barloworld’s take private, and the sale by Telkom of Swiftnet, its telecom tower portfolio. The JSE welcomed WeBuyCars and Boxer Retail to the bourse, in addition to three inward secondary listings by Powerfleet Inc, Assura plc and Supermarket Income REIT plc, with a combined market capitalisation of c. R100 billion.

Behind the scenes, in what DealMakers categorises as general corporate finance activity, 275 transactions were recorded, amounting to R532 billion. Share repurchases of R217 billion accounted for the lion’s share of the total value, with the repurchase programmes of Prosus and Naspers dominating. The local listing of Boxer Retail in November was a significant event in the capital markets, with a market capitalisation at the time of listing of R29,05 billion. There were 15 listings on South Africa’s exchanges during 2024 – eight on the JSE (including three inward listings), six on A2x (with two inward listings), and one on the Cape Town Stock Exchange.

M&A activity in 2025 presents potential challenges, including global economic uncertainties and possible shifts in U.S. trade and investment policies under a new Trump administration. However, if South Africa continues to implement pro-investment reforms and stabilise key industries, the pipeline of deals could become a reality, and M&A momentum sustained.

The winners of the gold medal subjective awards are as follows:

Ince Individual DealMaker of the Year – Sally Hutton

(L-R) Andile Khumalo (Ince), Sally Hutton (Webber Wentzel), Zoe Smith (Ansarada), Laban Nyachikanda (Ince), Justin Smith (Ansarada) and Marylou Greig (DealMakers)

Brunswick Deal of the Year – Groupe Canal+ acquisition of MultiChoice

(L_R) Steven Budlender (MultiChoice), Diana Munro (Brunswick Group), Zoe Smith (Ansarada), Justin Smith (Ansarada), Marylou Greig (DealMakers)

Exxaro BEE Deal of the Year – Coronation Fund Managers

(L-R) Richard Lilleike (Exxaro Resources), Mary-Anne Musekiwa (Coronation), Anton Pillay (Coronation), Sonwabise Mzinyathi (Exxaro Resources), Zoe Smith (Ansarada), Justin Smith (Ansarada)

Catalyst Private Equity Deal of the Year – Harith InfraCo’s acquisition of assets from the Pan African Infrastructure Devlopment Fund

(L-R) Emile du Toit (Harith General Partners), Zoe Smith (Ansarada), Sandile Zungu (Zungu), Justin Smith (Ansarada) Marylou Greig (DealMakers)

Business Rescue Transaction of the Year – West Pack Lifestyle

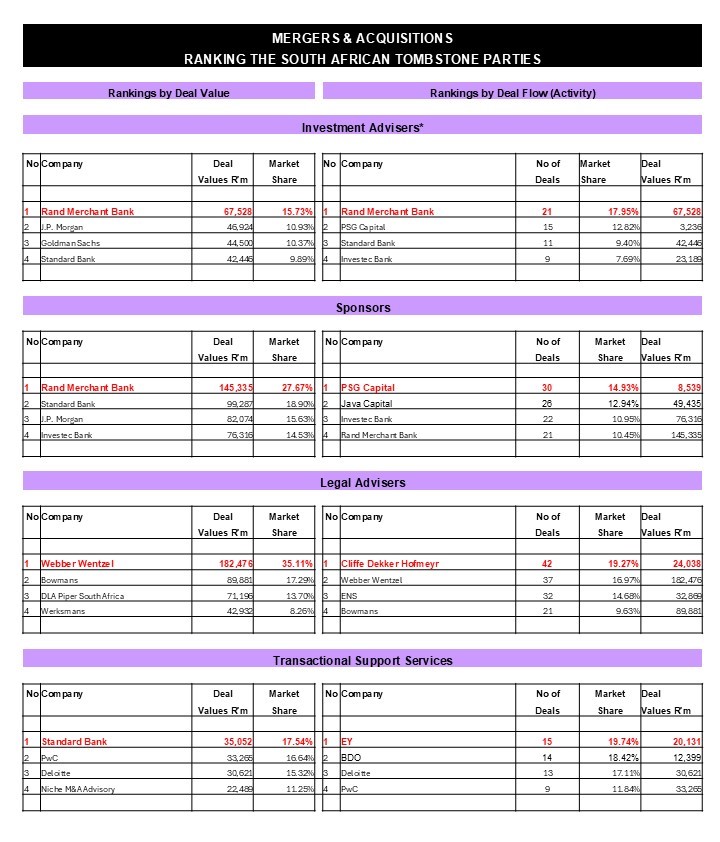

The category of Investment Adviser (by deal value) was won by Rand Merchant Bank. (L-R) Krishna Nagar (RMB), Zoe Smith (Ansarada), Justin Smith (Ansarada) and Marylou Greig (DealMakers)The category of Investment Adviser (by deal flow) was won by Rand Merchant Bank. (L-R) Krishna Nagar (RMB), Zoe Smith (Ansarada), Justin Smith (Ansarada) and Marylou Greig (DealMakers)

SPONSORS

The category of Sponsors (by deal value) was won by Rand Merchant Bank. (L-R) Valdene Reddy (JSE) and Masechaba Makhura.The category of Sponsor (by deal flow) was won by PSG Capital. (L-R) Valdene Reddy (JSE) and Mmakobela Mathabe (PSG Capital).

LEGAL ADVISERS

The category of Legal Adviser (by deal value) was won by Webber Wentzel. (L-R) Simla Ramdayal (WTW) and Christo Els (Webber Wentzel).The category of Legal Adviser (by deal flow) was won by Cliffe Dekker Hofmeyr. (L-R) Simla Ramdayal (WTW) and Roxanna Valayathum.

TRANSACTIONAL SUPPORT SERVICES

The award for Transactional Support Services Adviser (by deal value) was presented to Standard Bank. Khutso Manthata received the award from Marylou Greig (DealMakers).Femcke du Plessis received, on behalf of EY, the award for the Top Transactional Support Services Adviser (by deal flow) from Marylou Greig (DealMakers).

Winners of other awards presented on the night were:

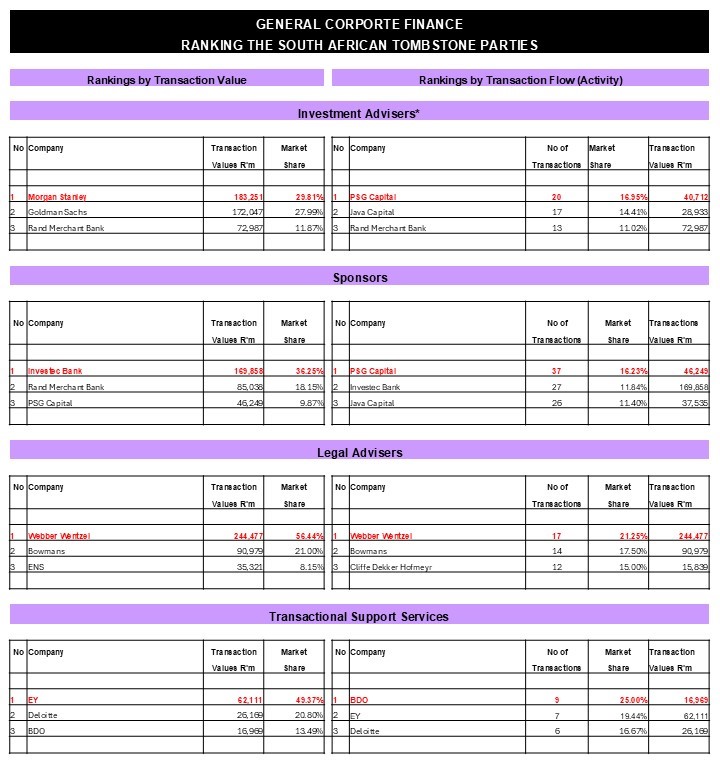

In the category of General Corporate Finance:

Investment Adviser (by transaction value): Morgan Stanley Investment Adviser (by transaction flow): PSG Capital Sponsor (by transaction value): Investec Bank Sponsor (by transaction flow): PSG Capital Legal Adviser (by transaction value): Webber Wentzel Legal Adviser (by transaction flow): Webber Wentzel Transactional Support Services (by transaction value): EY Transactional Support Services (by transaction flow): BDO

Anglo American plc has announced the signing of a memorandum of understanding between its 50.1% owned subsidiary Anglo American Sur SA and the Chilean state-owned mining company Codelco for a framework to implement a joint mine plan for the two companies’ respective, adjacent copper mines of Los Bronces and Andina in Chile. A new operating company will be jointly owned and controlled with the resulting copper production and value generated, as well as any costs and liabilities from the joint mine plan, shared equally. They will retain full ownership rights of their respective assets and will continue to exploit their respective concessions separately.

In addition, Anglo American plc has entered into an agreement to sell its nickel business in Brazil to MMG Singapore Resources Pte for a cash consideration of up to US$500 million. The nickel business comprises two ferronickel operations and two high quality greenfield growth projects. The agreed cash consideration comprises an upfront cash consideration of $350 million at completion, the potential for up to $100 million in a price-linked earnout and contingent cash consideration of $50 million linked to the Final Investment Decision for the development projects.

Vunani’s subsidiary Vunani Capital has concluded and agreement with Old Mutual Corporate Ventures (Old Mutual) to dispose of a 30% stake in each of Fairheads Benefit Services and Fairheads Financial Services businesses for R70 million. The deal will give FBS and FFS to grow activities within their core focus areas and to expand into new areas, leveraging off the skill available that comes with the strategic partnership with Old Mutual. The deal is a category 2 transaction.

CA Sales has entered into an agreement to acquire a 35% stake in Tradco Group, a market solutions business based in Kenya. Tradco offers logistics, warehousing and distribution solutions across the continent. The company has the option to increase its shareholding in Tradco by a further 20% which it is entitled to exercise at its sole discretion in the future. Financial details were undisclosed.

The proposed acquisition of a 30% interest in the newly formed entity Maziv, announced by Remgro and Vodacom in November 2021, which was prohibited by the Competition Tribunal in October 2024 and taken on appeal, have advised shareholders that long stop date has been extended once again to 14 March 2025.

The Assura board has considered the unsolicited approach from Kohlberg Kravis Roberts & Co Partners and USS Investment Management and has rejected proposal concluding that it materially undervalues the company and its prospects. No further proposal from KKR has been received.

Tongaat Hulett, which remains in business rescue, has advised shareholders that the High Court has dismissed the urgent interdict by RGS Group to have the adopted BR plan set aside. The plan involved the sale of the group’s assets and business to the Vision Parties. The High Court has, however, given RGS leave to deliver further affidavits on the matter.

Labat Africa has issued 147,349,826 new shares for cash. The shares were issued at a price ranging from 8 to 12 cents per share, representing a 50% premium to the current trading price of Labat. The funds will be applied to settle outstanding creditors.

Anglo American Platinum has declared an additional cash payout of R15.7 billion (US$852 million) to shareholders in preparation for an exit by parent Anglo American plc. Anglo intending to retain a shareholding of c. 19.9% in Amplats.

The JSE has approved the transfer of the listing of Trellidor to the General Segment of Main Board with effect from 18 February 2025. The listing requirements in this segment are less onerous for the smaller and mid-cap firms.

The JSE has notified shareholders of aReit Prop that the company has failed to submit its REIT Compliance Declaration within the four-month period stipulated by the JSE Listings Requirements. Accordingly, the company’s REIT status is under threat of removal.

This week the following companies repurchased shares:

On 19 February 2025, the Glencore plc announced the commencement of a new US$1 billion share buyback programme, with the intended completion by the time of the Group’s interim results announcement in August 2025. This week the company repurchased 10 million shares at an average price per share of £3.31. In line with the Company’s policy to maintain its number of treasury shares below 10% of total issued share capital from time to time, the Company announces the cancellation of 100,000,000 treasury shares.

Schroder European Real Estate Trust plc acquired a further 84,200 shares this week at a price of 66 pence per share for an aggregate £55,572. The shares will be held in Treasury.

In October 2024, Anheuser-Busch InBev announced a US$2 billion share buy-back programme to be executed within the next 12 months which will result in the repurchase of c.31,7 million shares. The shares acquired will be kept as treasury shares to fulfil future share delivery commitments under the group’s stock ownership plans. During the period 10 – 15 February 2025, the group repurchased 794,630 shares for €39,08 million.

Hammerson plc continued with its programme to purchase its ordinary shares up to a maximum consideration of £140 million. The sole purpose of the buyback programme is to reduce the company’s share capital. This week the company repurchased 313,533 shares at an average price per share of 290 pence.

In line with its share buyback programme announced in March 2024, British American Tobacco plc this week repurchased a further 496,450 shares at an average price of £30.65 per share for an aggregate £15,22 million.

During the period February 10 – 14 2025, Prosus repurchased a further 5,875,465 Prosus shares for an aggregate €240,92 million and Naspers, a further 418,550 Naspers shares for a total consideration of R1,8 billion.

Five companies issued a profit warning this week: Aveng, Metair, Metrofile, Mpact and AECI.

During the week, one company issued a cautionary notice: Vuani.

The International Monetary Fund (IMF) projects that between 2024 and 2028, the gross domestic product (GDP) of African frontier markets will grow at an average rate of 4.2% per annum. Notably, countries such as Mozambique, Rwanda and Senegal are poised for substantial growth, with projected annual increases of 7.8%, 7.2% and 6.8% respectively.1 Whilst Africa is well poised for growth, investors looking to invest in these markets are often confronted by challenges, especially when considering valuations and investment decisions.

A central component in valuations and investment decisions is the risk-free rate (RFR) – typically represented by government bonds – which implies a return on investments devoid of financial loss. In current financial climates, the importance of the RFR has intensified due to increased economic volatility and geopolitical uncertainty, including significant fluctuations in inflation and interest rates. This heightened relevance of the RFR stems from its role in helping investors gauge the baseline returns on their investments against a backdrop of unpredictable market conditions. By understanding the RFR, investors can better assess the additional risks and potential returns associated with various investment opportunities.

Accordingly, it is crucial to identify the specific challenges faced in determining the RFR in African frontier markets, particularly those with less developed financial infrastructures. These markets often grapple with issues such as limited bond market liquidity and inconsistent economic data, which can complicate the accurate assessment of the RFR. By understanding these unique challenges, investors can better evaluate and account for the inherent risks when making investment decisions in these regions.

Challenges with the RFR in Africa

Reliability of government bonds: Globally, government bond yields are often used as a proxy for RFR as, in principle, governments do not default on their debt because they can print more money to pay the bond, if required to. However, in frontier markets, government bonds may be an unreliable proxy for a “risk-free” rate, due to economic instability, political unrest and market illiquidity. The low liquidity in these bond markets can lead to broad yield spreads that do not accurately reflect market conditions, and make them difficult to price. Added to this is the limited availability of data on these bonds.

Currency volatility: High currency volatility adds another layer of complexity in some African markets, especially for foreign investors. Fluctuating exchange rates can significantly impact the real value of returns due to the added forex risk, which, again, makes it difficult to price accurately.

The impact of such challenges when determining the weighted average cost of capital (WACC)

The RFR is a key building block when calculating the WACC and, ultimately, value. It encapsulates the required rate of return from all sources of capital and is intended to reflect the aggregate risk that the valuation subject is exposed to, including country risk.

The RFR anchors the calculation of the cost of equity through the Capital Asset Pricing Model (CAPM), which is integral to the WACC. The RFR serves as the baseline return required for an equity investment, before making adjustments for correlated and uncorrelated risks associated with the valuation subject in question, to adequately compensate investors for the risk assumed.

Similarly, the cost of debt, which forms the other part of the WACC, is also intrinsically linked to the RFR. The cost of debt can be described as the credit spread, which indicates the extra yield needed above the RFR, taking into account the lender’s creditworthiness and the economic environment in which the lender operates. This is typically the rate at which a bank is willing to lend to a business after taking into account the risks associated with that business.

Given the typically higher RFR in Africa, the resultant WACC is also higher, indicating a perception of greater investment risk and the higher return required to compensate for this risk, which drives valuations down. This scenario poses a significant challenge to capital inflow, as investors require higher returns to justify the increased risk associated with investing in Africa and, in some instances, are not willing to assume such elevated risks (perceived or otherwise) to achieve higher returns.

Potential solutions worth considering

Leveraging local sovereign bonds: While U.S. Treasury Bonds are often used as a base for calculating the RFR due to their stability and liquidity, they do not fully capture the inherent risks present in African frontier markets. While adjustments can be made to recalibrate U.S.Treasury yields for country and currency-specific risks, this method can oversimplify the complexities of the African market.

A more suitable approach may be to use local sovereign bonds, if available and sufficiently liquid, to provide a closer approximation of the risks specific to the region. Often, this also more accurately reflects the risk of one country relative to another, where the one may have more reliable data available on it.

Composite indices for illiquid bonds: In cases where local bonds are illiquid, a composite index that factors in country risk premiums, inflation volatility and currency risk could offer a more accurate reflection of a RFR in these markets.

Strengthening local financial markets: In the long term, developing more robust financial systems in Africa is crucial for driving liquidity and providing reliable data for benchmarking and risk assessments. This should assist in attracting investment and laying the groundwork for improved capital markets and sustained economic growth.

To accurately value companies within the current constraints of African financial markets, it is crucial to leverage existing resources effectively. A more suitable approach may be to use local sovereign bonds, if available and sufficiently liquid, to provide a closer approximation of the risks specific to the region. If these bonds are illiquid, a composite index that factors in country risk premiums, inflation volatility and currency risk — calibrated against more stable regional/local markets – could offer a more accurate reflection of risk-free capital in these environments.

In the meantime, it is essential to recognise and adapt to the limitations of the current financial infrastructure. By refining how we use these existing tools (local sovereign bonds and region-specific indices), we can better understand and navigate the complexities of African markets. This strategy not only supports more accurate company valuations, but also contributes to enhancing financial stability and fostering investor confidence, which is vital for ongoing economic development across the continent.

International Monetary Fund, 2024. World Economic Outlook, April 2024: Steady but Slow: Resilience amid Divergence. [online] Available at: https://www.imf.org/en/Publications/WEO

Sibongakonke Kheswa is a Corporate Financier | PSG Capital

This article first appeared in DealMakers AFRICA, the continent’s quarterly M&A publication.

AngloGold reminded us why the saying “it’s a gold mine” can be appropriate (JSE: ANG)

How does an almost 9x increase in free cash flow sound to you?

AngloGold Ashanti delivered a set of numbers in 2024 that are quite magnificent really. With cash costs up just 4% for the year, the company was in the perfect position to generate immense profits from the much higher gold price (up 24% on average for the year).

Free cash flow increased from $109 million in 2023 to $942 million in 2024. That’s truly insane. The swing in HEPS is equally breathtaking, from a loss of 11 US cents per share in 2023 to a profit of 221 US cents per share in 2024. It’s also worth noting that headline earnings came in at $954 million, so free cash flow conversion was excellent.

There’s a new dividend policy in place at the company. The base dividend is $0.50 per annum, payable in quarterly payments. The total dividend will be 50% of free cash flow, provided that adjusted net debt to adjusted EBITDA remains below 1x. Considering that they are currently at 0.21x on that metric, the lowest level since 2011, I think the payout ratio is pretty safe.

The total dividend for 2024 was 91 US cents per share.

In terms of outlook, guidance for 2025 is production of between 2,900Moz and 3,225Moz. That’s way up from 2,661Moz in 2024, with the acquisition of Sukari helping to boost the outlook. AISC is expected to be between $1,580/oz and $1,705/oz. That’s a perfectly acceptable range vs. $1,611/oz in 2024. Provided that the gold price behaves itself, AngloGold is setting itself up for another massive year.

Despite this, the share price fell 6%. The gold price wasn’t the issue on the day, so it seems that the market was expecting more here. I guess in the context of a 62% return in the share price over the past 12 months (net of this sell-off), there’s always risk of profit-taking.

Some good news at Aveng (JSE: AEG)

Yet the share price still hasn’t found any support

Aveng fell another 8.3% on Wednesday, taking the year-to-date drop to a hideous 37%. Currently at R8.15 per share, I must point out that the 52-week low is R5.48. This thing can drop a lot further if the narrative doesn’t improve.

There aren’t many highlights in McConnell Dowell right now, the business segment focused on Australasia and Southeast Asia. As you may recall, Aveng recently flagged ugly losses there. Much closer to home, Moolmans (the segment focused on mining industry opportunities) put in a solid recent performance and has now locked in a large new contract.

The contract in question is worth R10.6 billion and is with Black Mountain Mining’s Gamsberg mine, a zinc mine in the Northern Cape. This is jointly owned by Vedanta and Exxaro Resources. The parties know each other well, as Moolmans delivered on an existing mining contract over the past 7 years.

The project requires capex of R1.3 billion over the life of the contract. As Aveng is busy losing money elsewhere in the world, they’ve had to get creative with how to fund this. One of the strategies is to rely on equipment OEMs for payment terms, while also designing the contract in such a way that the fleet renewal program is over the life of the contract rather than upfront.

The contract creates 342 new jobs in the Northern Cape, which is a pretty big deal.

City Lodge’s recovery story has stalled (JSE: CLH)

The dividend is flat

City Lodge Hotels has released results for the six months to December 2024. I’m afraid that they aren’t great, with revenue up just 2%. Although the average room rate increased by 10%, this had an impact on volumes with average group occupancy down 400 basis points to 57%.

Although HEPS climbed 15% without adjustments, it actually fell 2% on an adjusted basis. If you’re not quite sure what to make of this difference between the metrics, then always have a look at the dividend. Cash tells the real story and with the dividend staying flat at 6 cents per share, that story isn’t one of growth.

Interestingly, the company narrative suggests that the demand pressure on rooms was there anyway, so they pushed up rates in response to try and make up for it. Forgive me for relying on everything we know in this world about supply and demand, but that sounds odd. I’m not suggesting that they didn’t maximise things as best they could. It just seems strange to suggest that they responded to a weak demand environment by becoming more expensive!

Despite the lower occupancies, food and beverage revenue grew 6% and is now 20% of revenue. Gross margin improved from 59% to 61%. Management has done a great job in that space and this segment is the post-pandemic success story at City Lodge.

Another area where management deserves credit is cost management, particularly thanks to investment in areas like solar power.

This has been a period of extensive refurbishment projects to several key hotels in the group, so they will need to show growth in 2025 off the back of that investment. Occupancies are encouraging in January and February, up 200 basis points and 380 basis points respectively.

The share price is down 13% over 12 months and has taken a nasty knock of 17% year-to-date as the market has dumped many consumer-facing local stocks.

The strong momentum continues at Discovery (JSE: DSY)

They can get more than a free smoothie as the reward for these numbers

Discovery has released a trading statement dealing with the six months to 31 December. They expect normalised headline earnings to jump by between 30% and 35%. Before you worry too much about the “normalised” part of that, headline earnings without adjustments grew by a similar amount.

This was driven by a lovely performance in normalised profit from operations of an increase of between 25% and 30%. Discovery notes that Discovery South Africa and Vitality achieved similar growth rates.

Full details will be available on 4th March. In the meantime, the market celebrated with a 7.6% rally, taking the 12-month move to a juicy 54%.

Gemfields can breathe again: the stupidity of a Zambian export duty on gemstones is over (JSE: GML)

Well, for now at least

At a time when Gemfields is looking increasingly vulnerable, the very last thing they needed was the Zambian government trying to put a 15% export duty on precious gemstones and metals. As our very own government just showed us in the budget-speech-that-didn’t-happen, emerging and especially frontier market governments are always keen to shake the tree in search of more tax.

Thankfully, some degree of sanity has prevailed in Zambia and the export duty has been suspended. Make no mistake, this isn’t a forever solution. The word “suspended” is important here, as government might lift the suspension in future.

Gemfields finally caught a bid off the back of this news, closing 11.6% higher. Alas, it’s still down 45% over 6 months.

Glencore focused on cash generation in 2024 (JSE: GLN)

Lower energy coal prices were mainly to blame here

Glencore has released preliminary results for the year ended December 2024. Although revenue increased by 6%, they unfortunately saw adjusted EBITDA drop by 16%. That’s nothing compared to the net loss of $1.6 billion, which was driven by huge impairments.

Funds from operations is the metric that Glencore would far prefer you to focus on, not least of all because it increased by 11% despite bright red movements elsewhere on the income statement. Impairments are a non-cash expenses and Glencore also achieved net working capital inflows, hence the positive move in cash.

This is why Glencore has the confidence to announce top-up share buybacks in addition to the base dividend. This is despite net debt to adjusted EBITDA increasing from 0.29x to 0.78x off the back of the $7 billion EBR acquisition during the year.

Some relief to the net debt ratio will come from the disposal of Viterra, with $1 billion expected in cash proceeds (along with 15% in equity in the purchaser, Bunge).

The share price closed 5.7% lower on the day and is down 17% over 12 months.

Another Metrofile earnings release, another day of head scratching for the few remaining bulls (JSE: MFL)

Petition to change the ticker from MFL to FML

I will never understand the appeal of Metrofile. While writing the above headline, I initially mistyped the ticker as FML instead of MFL. Honestly, it feels more apt, particularly when you see a share price chart with a drop of 38% in the past year.

Buying low or no growth companies for the sake of a dividend yield is a fool’s errand in my opinion. Equities are for growth. If what you want is fixed income, then go buy bonds. When a share price falls by these sorts of numbers, the dividend won’t make up for it.

With HEPS down by between 23% and 46%, and normalised HEPS down by between 15% and 31% for the six months to December, it’s pretty woeful out there for Metrofile. Although there are pockets of growth in the group, they expect the “current challenges” to persist into the second half of the year.

Mpact’s margins are under pressure (JSE: MPT)

Operating margins have contracted off a high base

Mpact has released a trading statement dealing with the year ended December 2024. I’m afraid that this isn’t the kind of trading statement that you want to see, as the direction of travel for earnings is down. HEPS from continuing operations will fall by between 23.3% and 30%. Discontinued operations are much worse, with HEPS down by between 72.6% and 81.2%. Versapak was thankfully sold in November, so its challenges won’t be in the numbers again.

The share price is flat over 12 months, but this announcement came out at close of play on Wednesday. The market will only have time to trade on it on Thursday morning, so it could be a wild ride.

The issue wasn’t revenue growth, as revenue from continuing operations increased by 4%. Paper was up 3% and Plastics 8%. Despite this, EBITDA fell by 14% and operating profit by 24%. Clearly, the revenue growth wasn’t nearly enough to offset cost pressures.

Net debt at the end of the year was around R2.37 billion, well down from R2.7 billion at the end of 2023. The proceeds from the sale of Versapak helped here. Despite the lower overall debt, net finance costs came in at R300 million vs. R284 million the year before, which suggests that average balances over the year were higher.

Look out for the release of results on 10 March.

Sibanye-Stillwater expects a slight uptick in HEPS (JSE: SSW)

And you need toread this if you’re a Merafe (JSE: MRF) shareholder

Sibanye-Stillwater released a trading statement for the year ended December 2024. It may come as a surprise to you that HEPS is expected to increase by between 0% and 7%, despite all the negativity around the company in the past year. Even in HEPS though, there were a number of once-offs to help offset underlying pressure in PGM basket prices.

As for earnings per share (EPS), which includes the effect of impairments, there was another loss per share. It’s admittedly a lot better than the prior year loss of 1,334 ZAR cents, as the 2024 loss is expected to be between 245 and 271 ZAR cents.

It seems as though the second half of the year was the highlight, with the group also managing to achieve production within 2024 guidance for all but the US PGM operations. They also benefitted from the acquisition of Reldan (effective in March 2024), as Reldan’s focus is primarily on recycling industrial waste and achieving an output of gold as the primary commodity. It was a good year to be turning rubbish into gold!

The Sibanye share price remains a sad and sorry situation, down a whopping 73% over three years.

Separately, Sibanye announced an “enhancement” to the deal with the Glencore – Merafe venture. The change will lead to an accelerated completion of delivery of the required chrome volumes, which then leads into a new chrome management agreement that gives Sibanye more exposure to chrome prices than under the legacy agreement.

In a separate announcement, Merafe echoed Sibanye’s view that this is beneficial for all parties involved. Although there might be a change in exposure to chrome prices, there’s also an expectation of an increased feed and improved recoveries.

And in another separate announcement, Sibanye released its mineral resources and mineral reserves declaration as at December 2024. As they mine resources like PGMs and gold, these reduce over time. It isn’t so great to see things like geological changes and lower basket price assumptions. The only highlight really is the 36.6% increase in the attributable lithium mineral reserves, as well as a massive 116% increase to copper.

Revenue and margins down at Transpaco (JSE: TPC)

Here’s another SA Inc stock that is struggling

Transpaco’s share price fell 5% in response to the release of results for the six months to December 2024. With revenue down 3.1% and HEPS falling 9.8%, that dip isn’t a surprise.

When revenue decreases like that, it’s very hard to maintain margins. Inflationary pressures on costs are a reality, which is why operating profit fell by 13.7% and operating margin contracted by 100 basis points to 8.2%.

The HEPS impact was somewhat mitigated by share buybacks, shielding investors against some of the pain. The dividend displayed the most modest drop of all, down by 6.3% to 75 cents per share.

With pressure on profits seen across both major operating divisions, Transpaco needs a strong second half to the year. There isn’t much in the outlook section to suggest that anything is going to change in the near-term. The share price is up 22% over 12 months and trades on pretty thin volumes, so you could see some major percentage changes here.

Vodacom has laid out its five-year bull case (JSE: VOD)

The investor day presentation is well worth a read

Vodacom hosted an investor day themed around the concept of Vision 2030. The title is pretty self-explanatory, I think. It includes some absolute gems like this chart:

The story is firmly one of African growth, with Vodacom expecting South Africa to become a smaller part of its business over time. Although South Africa will still contribute the bulk of operating profit in 2030 (an expectation of 59%), that’s way down from 71% in FY20.

Key drivers of the growth story include population growth, smartphone penetration (with associated fintech benefits) and urbanisation. You can immediately see that these trends are stronger in the rest of Africa rather than South Africa, as they talk to frontier market rather than emerging market metrics.

Frontier markets unfortunately come with macro risks, particularly around their currencies. One of the ways to mitigate the risk is through localised costs, for example in Egypt where over 90% of operating expenses are denominated in local currency.

Of course, this doesn’t solve the issue of translating earnings into rands and ending up with large forex losses. These are the risks of chasing growth in frontier markets.

Still, it’s an enjoyable presentation to flick through. You’ll find it here.

Vunani is selling 30% of Fairheads to Old Mutual (JSE: VUN | JSE: OMU)

Now we know why they were trading under cautionary

The cautionary at Vunani has been lifted and we now know exactly what they were up to. Vunani has decided to sell 30% in Fairheads to Old Mutual for R70 million. For context, the Vunani market cap is R290 million. This is about as close as you can get to a Category 1 deal (and shareholder approval) without actually triggering one.

Fairheads is an important business for many reasons, not least of all because it does the financial administration for over 100,000 children who are dependents of deceased members of retirement funds. You can see why there is synergy with Old Mutual here.

If this deal manages to genuinely unlock synergies, then it could be pretty lucrative for Vunani thanks to the 70% stake being retained. Fairheads generated profit of R21 million in the interim period. If we double that to R42 million as a quick and dirty, then 30% of that is R12.6 million and Old Mutual has paid an annualised P/E of 5.6x for the stake.

WBHO has flagged a decent increase in earnings (JSE: WBO)

The share price is looking vulnerable though after a strong rally

Construction group WBHO is up roughly 50% in the past year. That’s a really strong performance, although this chart shows you that the share price has been battling to retain those gains for the past 6 months or so:

Is it forming a new base here, or will it crash through support and experience a nasty correction? While acknowledging that it was a wild afternoon in South Africa with the cancellation of the budget speech, it’s also worth noting that WBHO closed 2% lower after releasing a trading statement at 3:15pm that flagged a solid uptick in earnings. That’s a further worry for the share price, as momentum has waned.

Was the market perhaps hoping for more? Or was everyone just distracted? We will find out in days to come, as the market properly digests an expected jump in HEPS of between 15% and 25% for the six months to December 2024.

Focusing on HEPS from continuing operations, this means interim HEPS of between R10.42 and R11.32. Even if you double these numbers to annualise them, an incredibly risky approach to take in the construction industry, WBHO is on a forward P/E of 9x. Given the challenges that can easily take place in this industry (just look at the latest numbers from Aveng), that’s not a bargain in my books.

Nibbles:

Director dealings:

A non-executive director of BHP (JSE: BHG) bought shares worth roughly R12 million.

Things are finally happening at Labat Africa (JSE: LAB). Under new management and with a totally new strategy, they announced that the acquisition of Classic International will impact earnings at Labat by positive 7 cents per share. For context, the current share price at Labat is also 7 cents per share! The company has also made another non-executive director appointment with a focus on experience in the IT industry. It’s all about IT going forwards, which means a change of name is surely due at some point.

Northam Platinum (JSE: NPH) has finalised a power purchase agreement with an independent power producer in respect of a 140MW wind farm to provide energy to the group’s operations. The wind farm is close to Sutherland and will deliver power over the Eskom grid to Northam Platinum’s three operations. I always love the thought of the existing Eskom infrastructure being used like this. Deals like these have a number of benefits, ranging from energy security through to cost savings over time.

Super Group (JSE: SPG) announced that one of the conditions for the disposal of SG Fleet Group in Australia has been met. Noteholders gave a resounding approval to the deal, with the next critical milestone being Super Group shareholder approval that will be sought at the meeting on 25th February.

Salungano Group (JSE: SLG) announced that CFO Kabela Moroga has resigned from the company. Jannie Muller has been appointed as interim CFO. The process to appoint a suitable replacement CFO has commenced.

BHP (JSE: BHG) has indicated to the market that they are looking to add more debt to the balance sheet, so it’s not a surprise to see them pricing $3 billion worth of bonds in the US market. Here’s what the curve looks like: 5-year bonds at 5.000%, 7-year bonds at 5.125% and 10-year bonds at 5.300%. So, in case you didn’t already know this, the usual shape of a curve is that longer-term funding carries a higher cost. BHP will use the debt proceeds for general corporate purposes.

Redefine (JSE: RDF) announced that Moody’s has affirmed its long-term issuer ratings with a stable outlook. These credit ratings are particularly important in the listed property space due to the extensive use of debt.

Alexander Forbes (JSE: AFH) announced that is has repurchased all the shares held by the Isilulu Trust, an employee share scheme implemented in April 2015. The total guaranteed pay of affected employees will be adjusted to place them in the same position.

Tongaat Hulett (JSE: TON) announced that the High Court dismissed an application seeking to interdict the implementation of the adopted business rescue plan. It’s not over yet, as the applicant (RGS Group) is also seeking to have the business rescue plan set aside. The urgent interdict was thrown out, but further affidavits can be delivered in the broader matter. Separately, the board and business rescue practitioners have made some key executive appointments to the board.

The global exchange traded fund (ETF) market continues to expand rapidly, reaching US$14.85 trillion in assets under management (AUM) in 2024. This reflects a 10-year compound annual growth rate (CAGR) of 17.1%. South Africa is mirroring this global trend, led by Satrix, dominating the local market with 72.5%* of all ETF flows in 2024. When combined with its indexed unit trust flows, Satrix accounted for 50.5%* of all South Africa’s indexation flows. Fikile Mbhokota, Satrix** CEO, notes that the leading investment house saw ETF inflows grow by a staggering 127% year-on-year from 2023 to 2024.

Mbhokota further highlights that Satrix’s 2024 inflows exceeded that of 2023 by close to R5 billion, taking the Satrix AUM to in excess of R240 billion^ as of 31 December 2024. She attributes Satrix’s robust ETF growth to investors’ appetite for transparent, cost-effective investment solutions. She anticipates that this trend will continue into 2025 and beyond as South Africa follows the global trend of indexation adoption.

If we look at total flows across the local industry, it paints an interesting picture. The proportion of total industry flows into active strategies vs. indexed or rules-based alternatives (which include non-commodity ETFs and unit trusts) has changed dramatically. Over five years, the actively managed share of net flows was 64.3%, with the three-year number dropping to 43.5% compared to indexed alternatives. The past 12 months saw index strategies account for 87.8% of net inflows – clearly showing that the market has realised the value of index strategies in their portfolios.

Key Trends Shaping the Global ETF Market:

Increased Adoption: ETFs are gaining traction globally due to their transparency, liquidity, and cost-effectiveness, spreading beyond the US to Europe, the Middle East and Africa (EMEA) and Asia-Pacific (APAC).

ETF Savings Plans: In Europe, ETF savings plans are growing rapidly, with the number of plans set to quadruple over the next five years, according to BlackRock.

Innovation: The global ETF industry set a record in 2024, with 1,787 new products launched in the first 11 months – a net increase of 1,234 after 553 closures. This surpasses the previous record of 1,619 launches over the same period in 2021. Cryptocurrency ETFs have dominated asset accumulation among new launches, led by iShares Bitcoin Trust (US$48.43 billion).

Active ETFs: Active ETFs have outpaced mutual funds, particularly in the US, with a significant $3 trillion flow gap. This trend is gaining momentum in Europe.

Institutional Adoption: Institutional investors are shifting to ETFs for their cost-efficiency, transparency and multiple use cases.

European-Specific Drivers: Regulatory frameworks are impacting ETF adoption in Europe, supported by increased transparency and digitalisation.

South African ETF Industry Stats

As of December 2024, the South African Exchange Traded Product (ETP) market capitalisation reached R225.4 billion, reflecting a significant 36.2% growth compared to the previous year. This expansion was driven by R29.6 billion in capital raised through the listing of additional ETP securities on the JSE during the year, alongside the increase in market valuations year-to-date.

Kingsley Williams, Chief Investment Officer at Satrix, adds, “As a market leader in the ETF sector, Satrix will continue to drive local adoption by ensuring our local and offshore offerings meet the needs of our investors. With an ETF market capitalisation of R64.8 billion at the end of December 2024, our product offerings, such as the MSCI World, S&P 500, and Nasdaq 100 ETFs, have seen strong demand, particularly as South African investors look to diversify their portfolios globally.

“Investors are also increasingly using our other global ETFs, such as Global Bond, MSCI India and Global Infrastructure to better manage the diversification of their offshore exposure. In 2025, we’ll maintain our emphasis on offering cost-effective access while amplifying innovation as we explore new opportunities.”

Mbhokota concludes, “We believe South Africa will see continued growth in both equity and fixed-income ETFs, with an increasing share of investments flowing into internationally diversified funds. This growth is anticipated to be driven by both retail and institutional investors seeking cost-effective and transparent investment options that offer exposure to global markets. Investors are recognising the role ETFs can play in achieving a well-balanced, diversified investment portfolio, positioning ETFs as a core component of South Africa’s evolving financial ecosystem.”

*Source: Satrix and Morningstar, 31 December 2024

^Source: Satrix, 31 December 2024, AUM represents all assets managed in CIS vehicles (Satrix ETFs, Unit Trusts and UCITS), life pooled portfolios, assets managed via segregated mandates by Satrix as a division of Sanlam Investment Management and Satrix branded endowment funds managed by Sanlam Structured Solutions.

**Satrix is a division of Sanlam Investment Management

Other sources used:

ETFGI

Morningstar

etfSA.co.za

Introduction to ETFs: by State Street Global Advisers SPDR

Goldman Sachs ETF Accelerator: The Growth of ETFs in Europe

Satrix Managers (RF) (Pty) Ltd (Satrix) is a registered and approved Manager in Collective Investment Schemes in Securities and an authorised financial services provider in terms of the FAIS. Collective investment schemes are generally medium- to long-term investments. With Unit Trusts and ETFs, the investor essentially owns a “proportionate share” (in proportion to the participatory interest held in the fund) of the underlying investments held by the fund. With Unit Trusts, the investor holds participatory units issued by the fund while in the case of an ETF, the participatory interest, while issued by the fund, comprises a listed security traded on the stock exchange. ETFs are index tracking funds, registered as a Collective Investment and can be traded by any stockbroker on the stock exchange or via Investment Plans and online trading platforms. ETFs may incur additional costs due to being listed on the JSE. Past performance is not necessarily a guide to future performance and the value of investments / units may go up or down. A schedule of fees and charges, and maximum commissions are available on the Minimum Disclosure Document or upon request from the Manager. Collective investments are traded at ruling prices and can engage in borrowing and scrip lending. Should the respective portfolio engage in scrip lending, the utility percentage and related counterparties can be viewed on the ETF Minimum Disclosure Document.International investments or investments in foreign securities could be accompanied by additional risks such as potential constraints on liquidity and repatriation of funds, macroeconomic risk, political risk, foreign exchange risk, tax risk, settlement risk as well as potential limitations on the availability of market information. For more information, visit www.satrix.co.za.

Anglo American is getting many nickels for its nickel (JSE: AGL)

Here’s another major step in the simplification of the group

Anglo American is making solid progress with its plans to become a more focused group. Hot on the heels of the news that it will be stripping Anglo American Platinum of a fat dividend before cutting that controlling stake loose, we now also know that Anglo American will be selling its nickel business for up to $500 million.

These nickel operations are in Brazil, with two operating businesses and two greenfield growth projects. The buyer is MMG Singapore Resources and they already have a presence in Latin America.

The deal structure is a cash consideration of up to $500 million, with an up-front cash payment of $350 million as the deal is completed. There is then a price-linked earnout of up to $100 million (calculated over four years and with reference to the nickel price) and contingent consideration of $50 million subject to a final investment decision for the development projects.

Along with the steelmaking coal disposal announced in November 2024, Anglo American expects to generate up to $5.3 billion in gross cash proceeds. Although the words “up to” can work hard in these circumstances, it’s clear that Anglo is making a lot of progress on its stated strategy.

Local volumes are still light in Assura Plc, but the recent news got it some attention (JSE: AHR)

For now though, the board is rejecting the approaches from KKR and USS Investment Management

Assura Plc is a large UK-based property group focused on the healthcare space. Without much fanfare, the group added a JSE listing to its corporate structure in late 2024. Such listings can quickly diminish into obscurity, with little in the way of interest on the local market. That seemed to be the case for a while, although bidders circling the company could well have put it on the map.

Kohlberg Kravis Roberts & Co LP (or KKR for our collective sanity) put a proposal through to the board for a cash offer of 48 pence per share. That’s a 2.8% discount to the most recently disclosed tangible net asset value and a 30.1% premium to the 30-day VWAP. Talk about closing the gap to NAV! The board said thanks but no thanks, believing that this offer undervalues the company.

Separately, USS Investment Management Limited confirmed that it does not intend to make an offer for Assura, either as part of a KKR consortium or otherwise. So, that’s another potential bidder off the table.

The net result is that Assura is trading 13.9% higher on the day, still at light volumes though. Perhaps more investors will now pay attention to the company going forward? It certainly has no shortage of attention in the UK, considering the market cap is well north of R30 billion.

Earnings up, but dividends down at BHP (JSE: BHG)

Mining isn’t always a cash cow

BHP has released results for the six months to December 2024. At the halfway mark in the financial year, things are looking promising in key metrics like copper production (up 10% year-on-year). The group is on track to hit production guidance at all assets and they’ve made strong progress on unit costs as well.

From a revenue base of $25.2 billion, BHP generated attributable profit of $5.1 billion and will pay dividends of $2.5 billion. Or, put differently, the business generated $1 in dividends for every $10 in revenue.

HEPS has increased by 28.8% to 86.3 US cents. Despite this, the dividend per share has dropped by 31% from 72 US cents to 50 US cents. The market didn’t love this at all, with the share price down another 1.4% to take the drop in the past 12 months to 15.7%. When payout ratios are being decreased, it’s usually a sign that either management is worried or that the underlying business will need far more capital expenditure going forwards.

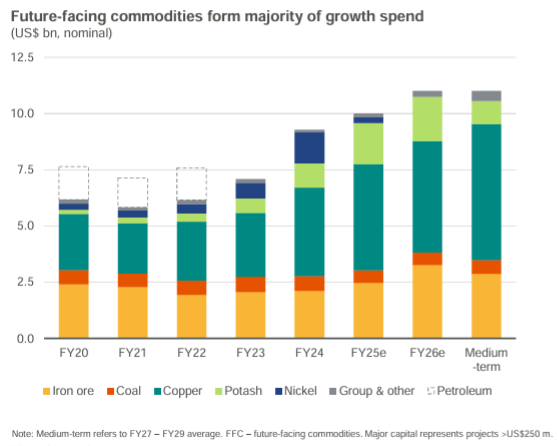

The balance sheet is fairly conservative by sector standards, with BHP expecting net debt to increase to the top end of the target range by the end of the financial year. Remember, debt isn’t inherently a bad thing. When correctly managed, it can boost equity returns. It’s also an important part of the capital structure in terms of funding capital spending, beautifully reflected in this chart from BHP that shows how copper has become such a big focus area:

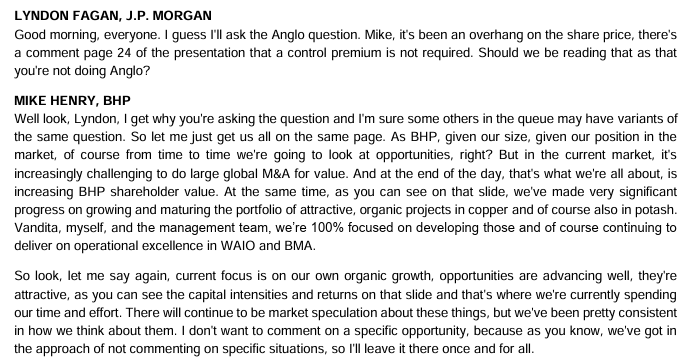

If you’re wondering about whether BHP is still eyeing out Anglo American for another takeover attempt, especially now that Anglo has already done much of the cleaning up of its group, you certainly aren’t alone. Here’s an excerpt from the earnings transcript and I wanted to include it here to show you how analysts ask questions and how executives respond to them:

It’s actually very rare to see locally listed companies making a full Q&A transcript available. I recommend you give it a read to see how institutions approach equity research. Here’s part 1 and here’s part 2.

DRDGOLD celebrates the gold price (JSE: DRD)

Adelicious jump in earnings is the reward for gold punters

DRDGOLD has released earnings for the six months to December 2024. With the gold price making headlines for such great recent performance, you probably already know that these earnings are shining brightly. Sure enough, HEPS jumped by 65% and the interim dividend was good for a 50% increase.

The driver of this result is a 28% increase in revenue, paired with an inflationary increase in costs. Operating leverage (the presence of fixed costs that go up with inflation rather than revenue) is a beautiful thing when it works in your favour.

With only a 1% increase in gold sold, this period clearly wasn’t driven by production volumes. In fact, were it not for the great gold price performance, they would’ve struggled to maintain margins. Luckily, the average gold price received was up 26% in ZAR, so all was well in the end.

Of course, there’s no guarantee of the gold price continuing to go up, so underlying metrics like a sharp decrease in yield at Ergo Mining are worth thinking about. Although the company will obviously seek out as many cost efficiencies as possible, having to process more volume to get the same amount of gold can only put pressure on costs over the long term.

The highlight at Kumba Iron Ore is definitely free cash flow (JSE: KIO)

As for revenue and HEPS, the trajectory is firmly in the red

Kumba Iron Ore has released results for the year ended December 2024. Most of the metrics look pretty rough, like a 21% drop in revenue and a 45% decrease in HEPS. The final dividend was 18% lower, similar to the drop seen in the interim dividend. TL;DR: it’s not good.

Return on capital employed halved from 82% to 41%. I must point out that 41% is still a great return on capital. 82% as the comparable number was just a tad on the ridiculous side.

This drop comes despite only a 2% decrease in export sales. Thy also achieved a significant decrease in cash costs per tonne, with Sishen and Kolomela improving by 10% and 16% respectively on that metric.

With sales only slightly down and costs improving by such a great extent, it’s clear that the metric that explains the negative performance is the average realised export price. That price fell by 21%, so it would’ve been very hard for Kumba to achieve much against that backdrop. Frustratingly, their ability to produce iron ore is limited by Transnet’s ability to transport the stuff, so Kumba can’t offset weak prices by ramping production.

Speaking of production, they expect 2025 production of 35 – 37 Mt (guidance unchanged). In 2026, production is expected to fall to 31 – 33 Mt based on planned activity at the manufacturing plant. My understanding is that they expect to make up the shortfall in sales using finished stock at Sishen. In 2027, production is expected to once again be 35 – 37 Mt.

The focus is therefore on cost efficiencies, with the hope of course that iron ore prices will increase.

Nibbles:

Director dealings:

Acting through Titan Premier Investments, Christo Wiese has bought another R793k worth of shares in Brait (JSE: BAT).

For Spear REIT (JSE: SEA) to have gotten its acquisition of the Western Cape portfolio from Emira Property Fund (JSE: EMI) across the line, the Competition Commission needed to give their approval. Of course, as we’ve come to expect, they used this as great opportunity for some regulatory overreach by forcing an increase in the Black Ownership percentage. Your guess is as good as mine in terms of how this addresses competition concerns. This means that an associate of a non-executive director of Spear has bought roughly R35 million worth of shares, funded to the extent of R30 million by a Nedbank loan that is guaranteed by Spear. In other words, all the shareholders of Spear (including existing Black shareholders who hold listed shares) are carrying more risk so that one specific shareholder can enjoy a great risk/return opportunity that wouldn’t be available without the corporate guarantee. This is a really old school approach to Black Ownership and it isn’t a net positive for the country vs. other ways of doing things, particularly when the situation is being forced by a competition regulator!

Keep an eye on Alphamin (JSE:APH), as the risks of doing business in Africa seem to be creeping up to its door. Insurgents in the Democratic Republic of Congo (DRC) have seized the city of Bakavu, which is the second largest city in the east. This follows the seizure of Goma in late January. Alphamin operates in a remote area and for now at least, there are no disruptions. Clearly, operations risks are now running red hot and any further escalation in the conflict could lead to disruptions.

Vunani (JSE: VUN) has renewed its cautionary announcement related to the disposal of a minority interest in a subsidiary. Negotiations are still underway and there’s no guarantee at this stage of a deal being announced.

Dipula Income Fund (JSE: DIB) doesn’t have any listed debt and doesn’t intend to have any, so they’ve decided to cancel the GCR credit ratings.

Afrimat has reminded the market that this is a tough year (JSE: AFT)

The market’s love for Afrimat is reflected in the share price

If you read the tone of Afrimat’s business update, they really couldn’t make it more obvious that this won’t be a great financial year. In the interim period (the six months to August), HEPS was down by a rather spectacular 79.9%. Although the announcement suggests that the second half was better, it still feels impossible that they could’ve clawed back an interim period like that.

Despite this, the share price is essentially flat over 12 months. It’s unusual to see such a disconnect between the price and the earnings, even for a stock that is a market darling.

In the Construction Materials business, the integration of Lafarge South Africa has been completed and cement operations are at acceptable levels. Overall, this segment is poised for growth. This is obviously one of the things boosting the share price.

The Industrial Minerals side also has a positive story to tell, with Afrimat describing a significant recovery in that business.

In Bulk Commodities, Nkomati returned to profitability in January 2025. All eyes are on the new financial year, with commitments for 80% of the new year’s export volume. Of course, this doesn’t make up for all the issues in the financial year ending February 2025. Afrimat continues to face problems with rail performance, with the company focusing on the silver lining of “volumes have not deteriorated” rather than any kind of improvement coming through. Local iron ore volumes remain a challenge, with the ArcelorMittal disaster having been a huge drag on performance at the start of the year. Although things have improved since then, there’s much uncertainty around the position going forward.

The Future Materials and Metals part of the group is small for now, with design work at Glenover and ramp-up in the phosphate plant.

Afrimat has confirmed that earnings for the year will be lower than the previous year. After the interim performance, nobody is surprised to hear that. The debate of course is around just how much lower the full-year numbers will be. The share price feels too optimistic to me.

If you’re keen to hear directly from management, Unlock the Stock will host Afrimat as its first event of 2025. As always, you can attend the live webinar and ask your questions. The event is scheduled for 27th February, a few days after the pre-close briefing session that management is hosting. Our efforts at Unlock the Stock are designed to give you as much management access as possible, levelling the playing field for retail investors vs. institutional investors. Best of all, attendance is free! You just need to register here>>>

Anglo American has given more details on the Anglo Platinum demerger (JSE: AGL)

They will receive a meaty dividend before the time

On the same day that Anglo American Platinum released results and announced its dividend (see further down), Anglo American reminded the market of its plans for the demerger. The goal is to get it done by June, with Anglo retaining a stake of 19.9% that they will “exit responsibly” over time i.e. sell into the market in such a way as to avoid crashing the market price. For context, the current stake is a 67% shareholding.

Anglo American will ask its shareholders to vote on the demerger at the AGM at the end of April. This means that Anglo American will bank a dividend of around $0.6 billion before the demerger. Read on to properly understand this…

Anglo American Platinum declares a huge special dividend (JSE: AMS)

The PR spin is that this is to have a more efficient capital structure

Here’s a bit of fun for you. Anglo American Platinum (Amplats) has released its 2024 results. They are ugly, with headline earnings down 40% despite a 4% increase in sales volumes and a reduction in all-in sustaining cost per ounce of 13%. PGM prices remain a huge headache and Amplats obviously can’t do anything to control that.

That’s not the fun part. We are getting to the fun part.

Despite the pressure in the business, Amplats has declared a final dividend of R3 per share, which is a 40% payout. This shows that although earnings are down, they are still able to stick to their usual capital allocation plans.

In addition to this (and here’s the fun), they’ve declared a special dividend of R59 per share. That is absolutely huge, with R15.7 billion about to flow out of the company. Does this sound like the kind of thing a company in an uncertain environment should be doing? Wouldn’t it be better to retain that cash and possibly pick up some great bottom-of-the-cycle acquisitions?

Of course it would.

Now, the official story is that Amplats wants to “set its independent capital structure in the most efficient manner” – something you would normally see from a company making more money than they possibly know what to do with. That’s the kind of narrative I saw recently at JPMorgan in the US, for example. Amplats is not even remotely in that category.

Take the PR spin off it and it’s really quite simple: the mothership Anglo American wants to extract as much cash as possible before they demerge Amplats. Although Amplats will be cut loose with an acceptable balance sheet, they certainly aren’t being given an acquisition war chest to move forward with.

Aveng released results – and the share price still can’t find the bottom (JSE: AEG)

It dropped by another 4% on the day

After breaking hearts on Valentine’s Day with news of the group slipping into a loss-making position, the release of detailed results did nothing to improve the relationship with the market. Aveng’s share price is now down 28% over 7 days. Ouch.

This is what happens when your interim revenue for the six months to December drops by R2 billion and operating profit swings from positive R192 million to a loss of R356 million. Included in this number are losses from J108 and Kidston, the disastrous projects, of R885 million.

At headline level, this means a headline loss per share of R3.09 vs. positive HEPS of R1.06 in the comparable period. Keep in mind that the share price is only R8.61!

Although cash on hand has increased from R2.8 billion to R3.0 billion, don’t get too excited about that number. They’ve recognised losses in this period that will only see a cash outflow in months to come. The income statement is telling you a lot about what is likely to happen to the balance sheet.

Can they claw some of this back in the second half of the year? Well, it’s not great to see that work in hand is down sharply from R37.2 billion to R30.1 billion. There’s a reduction in state government spending in Australia that is impacting the infrastructure segment in the business and more than offsetting the improved order book elsewhere.

The projects causing all the pain were awarded before Covid. Aveng makes the point that newly awarded projects are profitable. The issue in construction is that every contract looks profitable initially, otherwise why would the company agree to do it? It’s what happens in the years thereafter that counts.

Aveng still intends to separate its group into Moolmans (South African mining sector focus) and McConnell Dowell (infrastructure etc. in Australia, New Zealand and Southeast Asia). It remains to be seen how exactly they will structure this. Naturally, such a shocking period for McConnell Dowell isn’t helpful to this strategy.

CA Sales Holdings locks in another bolt-on acquisition (JSE: CAA)

This time, it’s in Kenya

After a truly spectacular run in the share price, even CA Sales Holdings took a breather in the market recently. With a return of 36% in the past year and a year-to-date dip of 4%, the market still has plenty of love for the company. Just look at the sell-off suffered by most of the other consumer facing businesses listed on the JSE. CA Sales may not sell directly to consumers, but the underlying exposure via the retailers is similar.

The strategy has been a combination of organic growth and bolt-on acquisitions, with the group following a smart approach of buying significant minority stakes and obtaining a pathway to control. I far prefer this strategy to 100% buyouts, as it ensures that the sellers are still incentivised to keep growing the business. There’s a big difference between partnering with entrepreneurs and allowing them to pass you the baton of whatever they’ve built.

The latest such example is the acquisition of 35% of Tradco, a route to market solutions business in Kenya. It has reach into other East African countries. This is firmly in the wheelhouse of CA Sales Holdings in terms of business model, although it does represent a tilt towards a different region in Africa to most of the existing exposure.

Importantly, CA Sales has the potential to acquire another 20% in the company. This is the pathway to control that I spoke about.

Emira has released the DL Invest circular (JSE: EMI)

This is a Category 1 transaction

Emira already holds a 25% interest in DL Invest. At the time of investing in that stake in 2024, Emira was granted an option to increase the stake to 45%. The aggregation rules on the JSE mean that the combined deal is a Category 1 transaction. If we didn’t have aggregation rules, it would make it very easy to circumvent categorisation of deals (and thus shareholder approvals and extensive disclosures) by breaking deals up into smaller tranches.

Emira has decided that international exposure is the gap in its story. The company has a direct property portfolio in South Africa that represents 69.7% of gross assets. They have 17.6% exposure to the US market and the rest in Poland, represented by the existing DL Invest stake. This deal is therefore designed to increase the exposure to Poland.

If all goes ahead, DL Invest will be 20.8% of Emira’s total investments and will contribute 12% of net income. There’s a long story in the circular about how Emira can get the stake at a discount to net asset value thanks to all the good stuff that Emira will bring to the relationship. In reality, property deals are done at discounts to net asset value all the time, all over the world. There’s nothing unusual about that.

Castleview Property Fund (JSE: CVW) holds 59.15% of Emira and has given an irrevocable undertaking to vote in favour of the deal. As these are ordinary resolutions, the shareholder meeting is thus a dead rubber as Castleview can simply approve the transaction.

Emira will fund the deal through a combination of existing cash reserves and space in revolving credit facilities that was unlocked through the disposal of the Western Cape portfolio to Spear REIT. Should property funds be swapping Western Cape exposure for Poland exposure? That doesn’t really seem to be in line with current trends, does it?

Quantum Foods has a positive story to tell (JSE: QFH)

Well, aside from the chicken looting in Mozambique!

I haven’t seen any headlines in a while about all the fighting between the board of Quantum Foods and certain shareholders. The board also had a fight with one of the non-executive directors. TL;DR: there’s been a lot of fighting.

Luckily, there hasn’t been a lot of pain in the business in the four months to January 2025. Egg sales are up, load shedding has basically disappeared and there were no HPAI outbreaks. That’s clucking excellent in comparison to what came before.

Although egg selling prices were down 13% on average (fellow Eggs Benedict fans rejoice), Quantum was able to offset this impact by enjoying a 70% increase in egg supply. With all poultry producers in South Africa enjoying a recovery in their flocks, egg prices are expected to keep dropping. Of course, there is the ever-present risk of an HPAI outbreak, so nothing is certain.

The other segments (broiler farming and the feed business) were described as having a “satisfactory” performance, so that looks positive alongside the layer farming business.

The negative news in this period was in the rest of Africa, specifically Zambia (where load shedding is an issue) and in Mozambique. The latter is quite a story, with a crowd attacking the layer farm on 26 December 2024 and stealing 16% of the layer birds! You can’t make this stuff up.

Spicy chicken action in Mozambique aside, the share price is up 34% in the past 12 months.

Nibbles:

Old Mutual (JSE: OMU) CEO Iain Williamson has opted to take early retirement. He will step down on 31 August 2025 after an impressive 32 years with the company and 5 years as CEO. That’s quite an innings!

Transaction Capital (JSE: TCP) announced that the commitment agreement in relation to the Road Cover disposal has become unconditional in accordance with its terms. That deal should now be final, which means Road Cover will sit in Mobalyz (SA Taxi) as part of Transaction Capital’s contribution to that business to try and keep it alive.

Depending on how things go from here, Assura plc (JSE: AHR) might disappear from our market as suddenly as it arrived. The company has confirmed media speculation that it has received a preliminary, unsolicited approach from major institutional investors KKR and USS Investment Management. Although nothing is certain right now and it could all fizzle out, those companies have confirmed that they are considering a cash offer of 48 pence per share – a 28.2% premium to the share price on the London exchange on 13 February. The board keeps rejecting the proposals from the bidders, so this could end up going hostile with an offer directly to shareholders. Of course, things could just fizzle out as well. There’s very little liquidity in the stock on the JSE, as the market hasn’t had much of a chance to get to know Assura. It’s a large company, with a market cap of nearly R29 billion.

The potential deal between Europa Metals (JSE: EUZ) and Viridian Metals is off the table. The idea behind the transaction was to reverse list Tynagh via Europa Metals, as Europa has disposed of the Toral Project. The clock is ticking for Europa, as they have only a few months to make a qualifying acquisition under AIM listing rules in the UK. Reverse takeovers are fun things where a listed company goes in search of an asset to be injected into the company, usually in exchange for shares. The worry is that although the Tynagh project had decent economics, Europa has noted that European conditions are not conducive to finding funding for a project like this. That’s going to make this acquisition search a lot harder.

Aveng shareholders are licking their wounds (JSE: AEG)

The construction industry just loves breaking hearts

I don’t like to use the word “never” unless I absolutely have to, but I am very confident that I will never invest in the construction industry. It always strikes me as gambling rather than investing, as there’s just so much that can go wrong. Aveng is the latest example, with a 25% drop in the share price on Friday in response to the release of a trading statement.

Why the long face in the market? It’s simple, really: Aveng is loss-making in the latest period. They expect a headline loss per share of between A$26.0 cents and A$27.0 cents for the six months to December 2024.

For all the effort to make McConnell Dowell the focus of investors (hence the reporting in Australian dollars), it was that part of the business that broke in this period. In New Zealand and Pacific Islands, they were pretty flat year-on-year. As for Australia and Southeast Asia, there are various legacy projects that have ruined profitability.

It takes just two bad apples in the basket of projects to contribute losses of A$77 million, more than offsetting the rest of the projects that made profit of A$50 million in aggregate. I don’t like businesses that are this lumpy and carry these kinds of risks.

Aveng has recognised the forecast costs to complete these projects, so the pain is theoretically captured in these numbers. The same can’t be said for the cash outflows that are expected to materialise over the next 18 months. Aveng reckons that the current cash balance along with expected profitability in other projects will cover the outflows. I must of course remind you that if these forecasts were super reliable, there would be no such thing as loss-making projects in construction.

As for Moolmans, the South African mining-focused business, there are positive earnings for the period and they are close to finalising a new 60 month contract. It’s therefore purely the offshore business letting the team down, a story that is far too common for South African listed companies.

You won’t often see a chart nosedive like this:

Jubilee’s copper catch-up at Roan is underway (JSE: JBL)

The feed materialis double the grade of material previously processed

After having suffered issues with the power supply to the Roan facilities in Zambia, Jubilee Metals needs to make up lost production. They are firmly in the process of doing exactly that, with the new high-grade copper feed material now being processed at Roan.

Jubilee recently announced that they had secured the rights to an initial 200,000 tonnes of this material, with the ability to get their hands on more of the stuff as well. Roan’s processing capacity is 45,000 tonnes per month, so this will keep them busy for a few months. The major benefit is that the high-grade material is roughly double the grade of the material that they previously processed, so this is part of an accelerated production plan to recoup lost production.

The share price is down 34% in the past six months and it doesn’t look like the momentum has turned just yet:

Metair is making a strategic shift (JSE: MTA)

I think they are tired of client concentration risks

If Metair didn’t have bad luck, they would have no luck at all. From hyperinflation in Turkey to floods at a key customer in South Africa, the world has dished up many a challenge for Metair in recent times.

The Turkish business really became a completely nightmare, with Metair eventually walking away with just $1 million in cash and a loss on sale of a breathtaking R4 billion. I will say it for the hundredth time: the track record in offshore investments for South African corporates is truly awful.

Thankfully, Metair seems to have recognised this, although they aren’t shy of taking on more risk in executing a strategy to be more focused on South Africa and to reduce customer concentration risks. The recently announced acquisition of Autozone comes at a time when group net debt is at R4 billion, most of which is short-term in nature. With a net debt to EBITDA ratio of between 3.4x and 3.6x, they are reliant on the lenders playing nicely with a refinancing package. There is a non-trivial chance of an equity capital raise being needed here, so tread carefully.

Moving on from these major strategic changes at the group, we find a set of results from continuing operations that don’t tell a promising story. For example, local vehicle production fell by 5%, with pressure at Toyota South Africa as a major drag on results. Although automotive battery volumes were higher in the Energy Storage business, Metair’s revenue from continuing operations fell by roughly 2.5% and EBIT is down by 21% at the midpoint of guidance. This included some once-off restructuring costs, without which the drop was 14.5% at the midpoint of guidance.

The net impact is a drop in HEPS from continuing operations of between 0% and 20%. This isn’t a position of strength for negotiations with banks. Even if there’s no rights issue coming, it’s likely that the cost of debt will be ratcheted in such a way that Metair spends the next few years working hard for the banks rather than shareholders.

The share price fell another 3.3% on the day, taking the one-year drop to a very ugly 48%.

Nibbles:

Director dealings:

There’s been some significant selling of shares by Richemont (JSE: CFR) executives. A member of the board sold shares worth R635k (with no indication that this was linked to stock compensation) and another board member sold shares worth R1.1 million (in this case linked to compensation, but it’s not clear whether it was the taxable portion or not).

The spouse of the CEO of Huge Group (JSE: HUG) bought shares worth R185k.

An associate of a director of Mantengu Mining (JSE: MTU) bought shares worth R133k.

The spouse of the CEO of Purple Group (JSE: PPE) bought shares worth R63k.

Labat Africa (JSE: LAB) has issued a sizable chunk of shares at a premium to the current traded price. The number of shares in issue has increased by 18.8% based on this share issue and the issue price was 12 cents per share, which is 50% more than the current traded price. The rand value is R17.7 million and the funds will be used to settle creditors and claims against the company.

Texton (JSE: TEX) announced that the aggregate holding of Heriot REIT (JSE: HET) and its subsidiary has ticked up to 22.77%.

Richemont (JSE: CFR) has done some juggling of its board and Senior Executive Committee, with three new appointments to that committee including the CEOs of two of the Maisons (one of which is Cartier). Not all of the Maison CEOs are automatically appointed to the committee. For example, one of the existing committee members is stepping down to become the CEO of Jaeger-LeCoultre.

Vodacom (JSE: VOD) and Remgro (JSE: REM) are still hoping for a positive outcome in the ongoing negotiations around the Maziv fibre deal. They’ve once again extended the transaction long stop date, this time to 14 March.

There is yet another delay to AYO Technology’s (JSE: AYO) financial results for the year ended August 2024. The auditor hasn’t yet finished the engagement quality control review, with AYO’s results now expected to be released by 28 February.

Delta Property Fund (JSE: DLT) announced that Brett Copans has resigned from the board as he is taking a role at a bank that has a business relationship with Delta and hence there would be a conflict of interest. You might remember his name from 2022 when he was appointed as Cell C’s chief restructuring officer. Some people really do enjoy turnarounds!