It was expected that the steady rise in foreign investments in Africa would result in an equally steady increase in tax revenue. As this has not been the case, African countries have embarked on reviews of their tax policies in an effort to get as much tax revenue in the net as possible. One type of fish, Capital Gains Tax (CGT) seems to have been avoided by both the African governments and the investors, yet it counts for a big percentage of the potential tax revenue collectable from the foreign investments. For instance, in 2020, an analysis by Oxfam highlighted that in just seven disputes emanating from CGT avoidance by multinationals, an amount of US$2,2 billion was in contention.

This article takes a deep dive into the specific steps taken by Kenya to ensure an increase in the amount of CGT collected from both onshore and offshore transactions. In light of this, it is imperative for potential investors to carefully review their activities, to ensure that they are not adversely affected by the changing laws in Kenya and the aggressive position taken by the Kenya Revenue Authority (KRA).

A look at Kenya

In Kenya, CGT has traditionally been levied on gains made from the transfer of property, whether or not acquired before 1 January 2015. The applicable rate went up from 5% to 15% of the net gain, beginning 1 January 2023.

The Finance Act, 2023 (the Act) ushered in a new regime for CGT in Kenya. Of relevance to this article is the fact that, effective 1 July 2023, gains from the sale of shares in foreign entities that derive more than 20% of their value directly or indirectly from immovable property situated in Kenya shall now be subject to CGT. Immovable property is defined within the Act to include land and things attached to the earth or permanently fastened to anything attached to the earth, an interest in a petroleum agreement, mining information or petroleum information. Please see the following illustration.

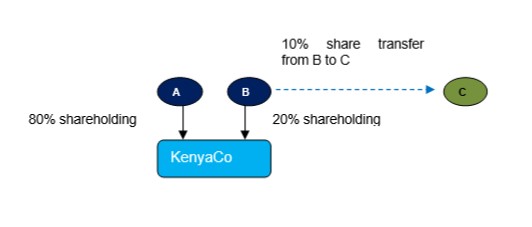

Figure 1: Before the Act

Figure 1 is an illustration of an onshore transfer of shares in a company situated in Kenya. A and B are individuals owning 80% and 20% respectively of the shareholding in KenyaCo. B is transferring half of his shares in KenyaCo (10%) to C. Before the Act came into force, only transfers of this nature (happening in Kenya) were subject to CGT.

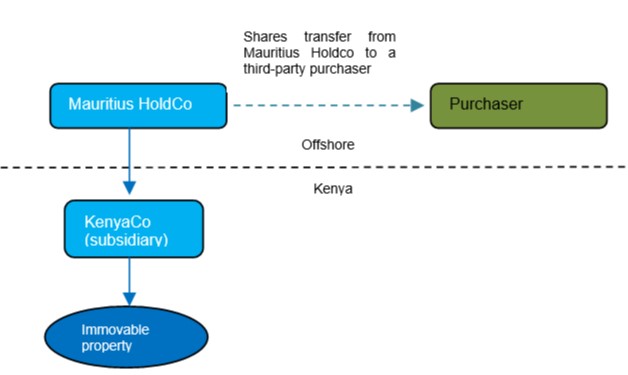

Figure 2: After the Act

Figure 2 is an example of an offshore indirect transfer now subject to CGT in Kenya. In the illustration, Mauritius Holdco indirectly derives more than 20% of its value from immovable property located in Kenya, owned by its subsidiary, KenyaCo. As such, it is liable to pay CGT in Kenya.

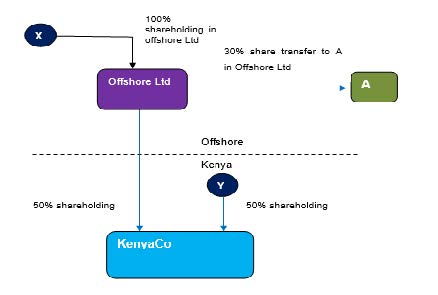

It is noteworthy that pursuant to the Act, non-residents holding more than 20% or more of the shareholding in a resident company, directly or indirectly, are subject to CGT on the disposal of their interest in the company. Please see the following illustration:

Figure 3: After the Act

In Figure 3, X is a non-resident who owns Offshore Limited. Offshore Limited and Y (a Kenyan individual) each own 50% of the shares in KenyaCo, a resident company. X is transferring 30% of the shares in Offshore Ltd to A, a non-resident. According to the Act, transactions of this nature by non-residents are now also subject to CGT in Kenya.

This recent development was not only effected in law, it has also been enforced by the judicial organs. More specifically, the Tax Appeals Tribunal, in the case of Naivas Kenya Limited v Commissioner of Domestic Taxes (2022) and ECP Kenya Limited v Commissioner of Domestic Taxes (2022), determined that the Kenya Revenue Authority (KRA) had not erred in taxing the gains from the sale of shares in Mauritius-based entities, for the reason that they were being managed and controlled from Kenya. It is notable that the assessment in both cases related to corporation tax and not CGT. This points to the aggressive position taken by the KRA not just to pursue 15% CGT, but corporation tax at 30% for an offshore indirect transfer that derives value in Kenya.

International best practice

Tax treaties are at the centre of international cooperation in tax matters, such as tackling international tax evasion. To prevent double taxation, they would typically award taxing rights to either the resident state or the state where the asset is located.

Kenya has aligned itself to International best practices, including the OECD Model Tax Convention and United Nations (UN) Article 13 (4). Both the UN and OECD Model Tax Convention stipulate that gains derived by a resident of a Contracting State from the alienation of shares or comparable interests, such as interests in a partnership or trust, may be taxed in the other Contracting State if, at any time during the 365 days preceding the alienation, these shares or comparable interests derived more than 50% of their value directly or indirectly from immovable property situated in that State.

Conclusion

For commercial reasons, Foreign Direct Investors may opt to invest through offshore entities. However, the recent developments in Kenya call for a review of this approach. Kenya and other countries have taken steps to implement concrete measures to effectively collect CGT from capital gains realised through such transactions, and the taxation of offshore indirect transfers is already a fully established international tax norm.

Investors with offshore operations should, therefore, consider taking a step back to ensure that their legal, operational and transactional structures adapt to the changing tax regulations. This calls for expert guidance to identify any potential weaknesses in the existing structures, as well as to advise on and implement the necessary adjustments to maintain tax compliance, minimise tax exposure, and guarantee sustainability.

It is important for global investors to carefully review the tax impact for investments that derive their value from Kenya, to ensure that the risk of CGT and Corporation Tax on offshore indirect transfers is addressed.

Alex Kanyi and Lena Onyango are Partners, and Judith Jepkorir a trainee Advocate | CDH Kenya

This article first appeared in DealMakers AFRICA, the continent’s quarterly M&A publication.

DealMakers AFRICA is a quarterly M&A publication

www.dealmakersafrica.com