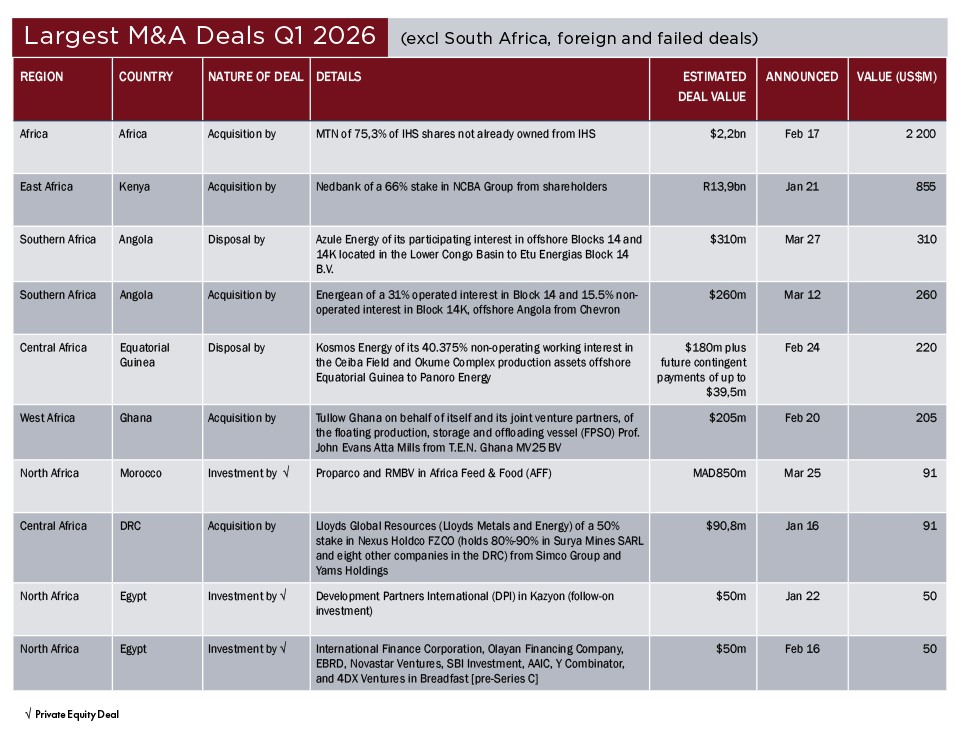

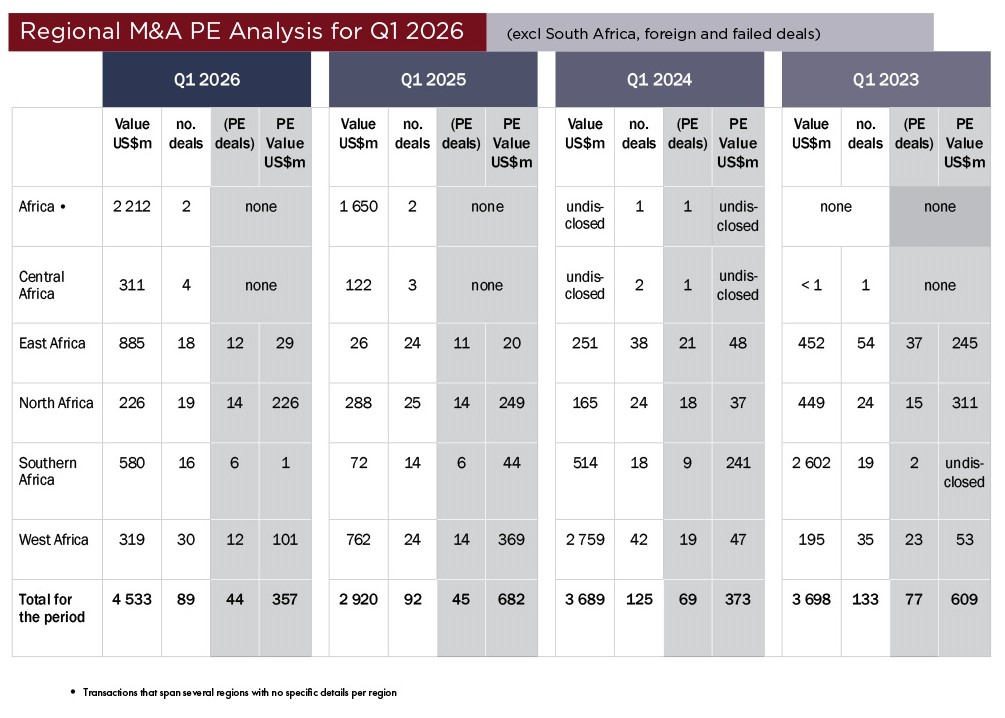

Africa’s M&A market entered 2026 with strong momentum in deal value, even as overall transaction volumes softened. In the three months to March 2026, announced deals across the continent (excluding South Africa and failed deals) reached an aggregate value of US$4,53 billion from 89 deals, compared with 92 deals valued at $2,92 billion over the corresponding period in 2025. Private equity continued to play a significant role, accounting for half of all transactions recorded during the quarter.

At a regional level, West Africa was, by far, the most active market, accounting for 30 deals, or 34% of total reported activity during the period. North Africa followed with 19 deals, and East Africa with 18. Within these regions, Nigeria (22 deals), Morocco (10 deals) and Kenya (13 deals) emerged as the key drivers of activity.

Energy and fintech remained the sectors of choice for investors across the continent. Of the top 10 deals by value announced during the quarter, four were energy transactions – two deals in Angola and one each in Equatorial Guinea and Ghana – with a combined value of $995 million. Topping the table was MTN’s acquisition of the remaining 75.3% shareholding in IHS, valued at $2,2 billion, followed by Nedbank’s acquisition of a 66% stake in NCBA, valued at $855 million.

According to Africa: The Big Deal, Africa’s start-up funding ecosystem continues to show resilience. In the 12 months to March 2026, African start-ups raised $3,3 billion (excluding exits), comprising $1,8 billion in equity funding and $1,4 billion in debt funding. However, a closer look at the data points to an evolving funding landscape, where overall growth has increasingly been driven by a surge in debt funding, offsetting a decline in equity capital raised.

While debt and equity investors each play distinct, but equally important roles in the development of a maturing start-up ecosystem, concerns remain around the decline in smaller early-stage equity deals. According to the publication, these transactions are critical for building the next generation of companies capable of attracting larger funding rounds in future. The slowdown in early-stage activity may not immediately affect aggregate funding totals – particularly while larger equity rounds and debt transactions continue to come through – but its longer-term implications for the pipeline of scalable African businesses are worth watching.

DealMakers AFRICA is Africa’s corporate finance magazine