AECI found a nasty whoopsie in its numbers (JSE: AFE)

It’s not a crisis, but nobody wants to see a “change statement”

A change statement is a rare thing on the market. It means that something was found between the release of reviewed and audited results. In this case, AECI discovered unsubstantiated supplier payments in the DRC, leading to an adjustment to tax payable of R32 million.

What does this mean in practice? HEPS will be R10.68 for the year ended December 2025, instead of R10.98 as previously indicated. That’s a 2.7% difference.

It’s not going to break the bank, but it’s annoying for shareholders and raises bigger questions around risk in the underlying operations, particularly in the rest of Africa.

BHP: aiming for the upper half of copper guidance and on track for iron ore (JSE: BHG)

They need to a strong finish to the year

Brandon Craig will take the role of CEO at mining giant BHP from 1 July 2026. He will inherit a company that is performing well, with an exciting portfolio across copper, iron ore and coal.

The production update for the quarter and nine months ended March 2026 is a reminder of the volatility in mining.

In copper, the metal that everyone is talking about, they are expecting to hit the upper half of production guidance. This is despite a 3% decrease in copper production for the nine months, mainly due to a 19% drop at Pampa Norte caused by various ongoing challenges around ore complexity and variation. Copper South Australia was up 3% and Antamina increased by 19%. Escondida, by far the largest mine, dipped 3%.

They highlight record production at Western Australia Iron Ore (WAIO), although the production increase is only 2% for the nine months. Technically, even the smallest possible percentage increase on a previous record would be a new record! More importantly, they are on track for FY26 guidance in iron ore.

Steelmaking coal production is up 1% year-to-date, with guidance for the full year unchanged. They only expect to be in the lower half of the guided range, which means unit costs will be at the top end of the guided range.

Energy coal is up 11%, with BHP expecting to reach the upper half of the guided range.

The production performance will always be impacted by the specific period that you’re looking at. The year-to-date numbers are much smoother than the quarterly numbers, as you might expect. The Q3 numbers indicate just how much pressure there is at Pampa Norte in copper, with a 34% drop for the quarter. With Escondida down 9% for the quarter, copper had a poor quarter with a drop of 7%.

There’s all to play for in Q4, the final quarter of Mike Henry’s tenure as CEO.

Capitec looks unstoppable (JSE: CPI)

These numbers are insane

The best business story of South Africa’s democracy has done it again. Capitec reported excellent numbers for the year ended February 2026, boasting over 25 million personal banking clients and a ridiculous 54% market share among young adults (18 to 35).

I’m going to remind you that there are multiple banks in our market. It’s almost unbelievable that just one of them has over half of the market in the segment that will drive earnings in decades to come.

Another surprising element to Capitec’s business model is the success they are finding among high earners. Clients earning more than R50k per month are up 21%.

This is translating beautifully into the financial performance, with headline earnings up 23%. Return on Equity has reached 31%, up from 29%. That’s double what some of Capitec’s competitors are achieving.

The contribution at the top of the income statement is also well worth touching on. Net interest income after credit impairments increased 18%, while non-interest income increased by 19%. Although operating expenses increased by 12% to fund growth, that excellent revenue performance was more than enough to drive earnings higher.

The Business Banking operations are now contributing 5% of group headline earnings. This is an exciting growth driver going forwards. I’ve obviously been working with Capitec on The Finance Ghost plugged in with Capitec and I’ve been extremely impressed with the quality of the clients I’ve been introduced to.

Here are two other data points that may surprise you: Fintech contributed 26% of headline earnings, while Insurance contributed 27%. Personal Banking is still the largest at 41%. AvaFin is the smallest at 1%.

I could fill five editions of Ghost Bites with news about Capitec. I need to keep it brief on a busy day of company updates. I’ll therefore mention just one more innovation that shows how powerful this group is: they are introducing free calling between Capitec Connect customers. Just contemplate what this means to the Capitec client base and stickiness of those clients.

The share price is up 32% in the past year.

Based on this update, what is your current view on the share price?

Record net inflows at Quilter (JSE: QLT)

Solid momentum at the end of 2025 has continued into 2026

Quilter has released a trading statement for the first quarter of 2026. With core net inflows up 35% year-on-year and representing 9% of opening assets under management and administration (on an annualised basis), they are telling a bullish story about their business.

The inflows were offset by market movements around quarter end, but the solid market recovery in recent weeks has given them an excellent base for the second quarter and beyond.

Importantly, they enjoyed net inflows across both the Affluent and High Net Worth segments. The UK market struggled with uncertainty last year and a general exodus of wealth. The final quarter of 2025 marked a recovery that seems to have continued into 2026.

And with strong inflows, it’s not surprising to see that productivity (measured as Quilter channel gross sales per Quilter Adviser) has increased substantially from £3.4 million to £3.9 million.

The share price is up 27% in the past year.

Spear REIT to raise R1 billion in fresh capital (JSE: SEA)

And if demand is strong, they might increase the raise

After market close on Wednesday, Spear REIT announced the launch of an equity raise of R1 billion through a bookbuild process. As usual, this means that the advisors will reach for their little black books and phone institutional investors with deep pockets.

Given the success of Spear’s strategy and how focused they are on the Western Cape, I doubt it will be terribly difficult to raise the money. Spear has noted that they might increase the raise if demand is strong. I wouldn’t be surprised to see that happen.

The group must have a strong acquisition pipeline that goes well beyond the recently announced deal in Mitchells Plain. Other than new deals, they are also looking to develop bulk within the industrial property portfolio.

The thing to look out for is the price at which the book will close. Ideally, you want to see the smallest possible gap between the existing traded price and the issue price for the new shares. The size of the gap indicates the incentive demanded by institutions to support the raise.

South32’s production is on track (JSE: S32)

At the nine-month mark, most commodities are at or above 75% of full-year targets

There are numerous unpredictable factors in the mining industry, not least of all the impact of weather and heavy rainfall in particular. Mining production reports tend to isolate these problems to help investors distinguish between weather issues and other underlying problems.

South32’s report for the three months to March reflects some encouraging signs, like a record quarterly dividend at Sierra Gorda and record year-to-date production at Brazil Alumina. But there was also an adverse weather impact in Australia Manganese, where FY26 production guidance has been revised lower by 6%.

Overall, with nine months of the financial year behind them, South32’s various commodities have achieved between 74% and 79% of full-year guidance. This means they are well on track.

The one exception is Mozal Aluminium, which sits at 103% of full-year guidance as the facility has now been transitioned to care and maintenance and won’t operate in the fourth quarter. It exceeded its production guidance in its closing stages. Talk about a farewell kiss!

Net cash increased by $121 million in the quarter, putting them in a positive net cash position of $96 million.

To give you context to how South32 allocates capital, they invested $239 million in capex (excluding equity accounted investments and Hermosa) over nine months. Hermosa is a substantial standalone project, requiring $496 million in growth capital over the period.

Share buybacks over the same period were $35 million. The dividend for the first half of the year was $175 million. As you can see, South32 is having to reinvest far more capital than it can distribute at the moment. They are playing the long game in key metals.

Double-digit growth at Standard Bank (JSE: SBK)

The first quarter of 2026 went well

Standard Bank announces financial information each quarter. This is because the high-level numbers are provided to ICBC in China, the investor that has a significant minority stake in Standard Bank. ICBC equity accounts for the stake and needs to do so each quarter. The happy outcome is that the market gets a very basic update on Standard Bank every three months.

For the three months ended March 2026, Standard Bank enjoyed a 12% increase in earnings attributable to ordinary shareholders. They guide that headline earnings growth is similar.

That’s a strong follow-up to the recent capital markets day. Guidance for the year ending December 2026 remains unchanged despite the recent energy shock.

Stor-Age makes an acquisition in KZN (JSE: SSS)

It’s a small deal, but a strategically sensible one

Stor-Age has a market cap of R9.2 billion. It’s not easy to move the dial with a single transaction once you’ve reached that size. But then again, that’s a dangerous goal to have, because it’s far better to build through a combination of organic growth and bolt-on deals than to roll the dice on a megadeal.

The latest transaction is a great example of a modest deal that simply adds to the company’s ecosystem. Stor-Age is acquiring Execustore in Ballito for R59 million, giving them a trading property that has strong access to the region’s dominant retail hub and important residential and commercial areas.

The current GLA is 5,700 sqm. There’s plenty of room to expand, with 6,600 sqm of land available.

The effective date of the acquisition was 1 April 2026. They clearly aren’t superstitious about April Fool’s Day!

The deal is too small to require any additional disclosure. It’s good to see the company at least including the purchase price in the voluntary announcement.

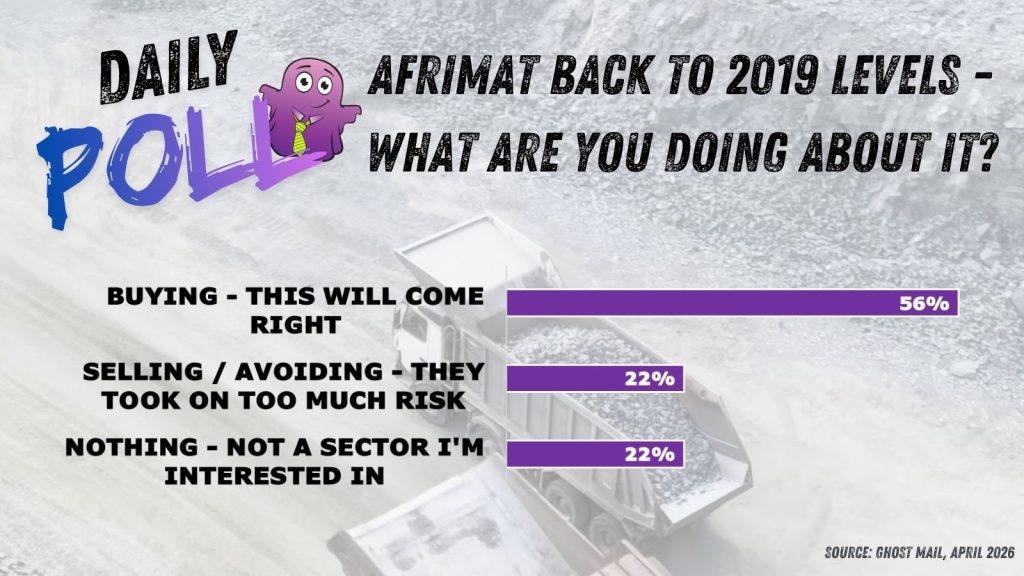

Results of yesterday’s poll:

Nibbles:

- Here’s an interesting one: Apex Partners Holdings, founded by Chris Seabrooke (of Sabvest (JSE: SBP) fame) and Charles Pettit, has taken a 5.82% stake in Stefanutti Stocks (JSE: SSK). The Stefanutti Stocks share price is up 43% year-to-date.

- enX (JSE: ENX) has been in the process of selling the remaining 75% interest in West African International (WAI) to Trichem SA. The only remaining step is the receipt of a TRP compliance certificate. The deal is expected to be implemented with effect from 24 April 2026.

- Remgro (JSE: REM) has disposed of its remaining FirstRand (JSE: FSR) shares for R3.6 billion. I would love to see this cash be used for share buybacks. But it probably won’t be.

- There’s a shuffling of chairs in the mining industry. Jacques Breytenbach has resigned as an independent non-executive director of Afrimat (JSE: AFT). He’s popped up immediately as CFO-designate of Tharisa (JSE: THA), with an expected appointment date of 1 May 2026. He brings tons of mining experience to the role.

- OUTsurance (JSE: OUT) announced that group CFO, Jan Hofmeyr, has resigned after more than 18 years with the group. He’s moving to an unnamed fintech venture (clearly a well-funded one). Francois van Rooyen has been named as his replacement at the age of just 39, having joined the group in 2018.

- Numeral Limited (JSE: XII) has cautioned the market regarding an intended restatement of results for the year ended February 2025. This relates to the technical accounting considerations around the recovery of the 50% interest in Cryo-Save South Africa. The company notes that the restatements are more to do with the presentation of financials than the underlying economic substance of the group.