In this edition of Ghost Bites:

- Altron’s numbers look spectacular

- Exemplar REITail’s township mall strategy is working

- Netcare’s income statement is healthy

- A period of solid growth at Omnia

- Pick n Pay is still going backwards

- PPC’s giant keeps awakening

- RMB Holdings has impaired its NAV almost down to the AttBid offer price

Altron’s numbers look spectacular (JSE: AEL)

The share price jumped 14% on the day!

There aren’t many businesses on the JSE that describe themselves as being “platform” businesses. In practice, the application of this term has expanded way beyond the business models of the US tech firms that made it famous (and highly desirable).

Although we can debate the exact meaning of this word, there’s certainly no debate that Altron’s Platforms segment is making an absolute fortune at the moment.

The group numbers are excellent as you work down the income statement, but they start with revenue growth of just 1%. This is because the Platforms segment of the business grew by 12%, but the IT Services and Distribution segment was in the red.

Thankfully, due to the much better economic profile of the Platforms segment (recurring revenue and high margins), everything gets more exciting from here. In fact, the Platforms segment contributed 95% to operating profit despite contributing only 46% to revenue!

Operating profit just jumped by 25% to R1.2 billion, with operating profit margin up 250 basis points to 12.6%. A change in accounting policy at Netstar and a pension fund expense affected this growth rate. Excluding these distortions, operating profit was up 19% – still an excellent growth rate.

Return on invested capital (ROIC) increased by 390 basis points to 18.8%. HEPS increased by a casual 34%!

The business is spitting out cash at the moment, with cash generated from operations of R1.9 billion and no debt on the balance sheet. Group capex of R800 million is easily covered by the inherent cash flow in the business, with R739 million of that capex flowing into growth initiatives (mainly within the Platforms segment).

I must point out that R492 million of that capex number is going into Netstar rental devices, a business-as-usual requirement that is perhaps best seen as working capital rather than capex (regardless of the accounting rules).

The closing cash balance as at 28 February 2026 was R1.3 billion. It’s little wonder that they are paying a 120 cents special dividend per share in addition to a 44% increase in the final dividend to 72 cents. For context, the total ordinary dividend for the year was 120 cents, so the special dividend is doubling the payout to shareholders.

In the Platforms segment, which we now know makes almost all the profit, we find three pillars: Netstar, Altron Fintech and Altron HealthTech.

Netstar has exceeded R1 billion in EBITDA for the first time this year. Aside from cute milestones, the important point is that EBITDA was up 16% and margin jumped from 41% to 44%. If you can believe it, the Australian business has been a drag on the numbers vs. South Africa. Why is every single sector in Australia so difficult?!?

Altron Fintech was one of the stars of the show. Annuity revenue is 88% of total revenue and they are achieving operating margins of 37%. Operating profit climbed 33% year-on-year. Those metrics look great even by global standards.

Altron HealthTech only managed to grow revenue by 2%, yet operating profit was up by an impressive 19%. With 96% of revenue being annuity-based, this is a dependable business.

Within the IT Services segment, we find another three pillars: Altron Digital Business, Altron Security and Altron Document Solutions. This segment is far more of a struggle, with revenue down 5% and operating profit declining by 15%.

In Altron Digital Business, we find a revenue decline of 8% and operating profit of only R7 million – a near-miraculous turnaround from a loss of R42 million in the first half of the year. This is still the biggest headache in this segment.

Altron Document Solutions was the highlight. Although revenue was down 2%, operating profit was up 61% year-on-year to R98 million. This doesn’t tell the full story, as this business suffered an operating loss of R97 million two years ago!

Altron Security was a solid performer in this period, with revenue up 4% and operating profit up by 5%. The annuity business is 80% of revenue in this segment.

Altron’s capital markets day is scheduled for 9 June. They will talk to the market about how they are emerging from the “Accelerated Growth” phase and entering the “Transformative Growth” phase. It’s going to be incredibly interesting!

Ghost Bite: Turnarounds can be beautiful things. And this is one of the prettiest ones you’ll find on the local market.

Exemplar REITail’s township mall strategy is working (JSE: EXP)

Check out these growth rates…

Exemplar REITail’s numbers for the year ended February 2026 are impressive. The company is unusual on the JSE, as they are focused on owning township and rural shopping centres that tap into the trend of informal-to-formal retail shifts.

The 31 retail assets in the portfolio are working hard, with a 13.1% increase in net property income and a 15.3% increase in the total distribution per share for the year.

In an unusual display of congruency, the growth in the net asset value (NAV) per share is also 15.3%.

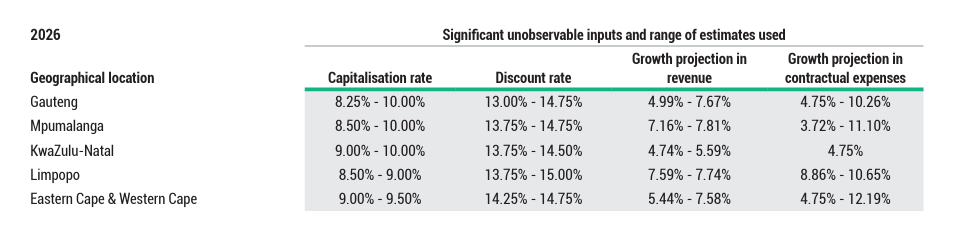

For the finance geeks among you who are interested in how properties are valued, this table is particularly interesting:

I didn’t expect Limpopo to have a capitalisation rate with the lowest midpoint! Check out the projected growth in revenue in that region as well.

Ghost Bite: This is a difficult business to run, but it’s also one of the more exciting growth engines in the South African economy. The shiny buildings with great views aren’t delivering growth in the mid-teens!

Netcare’s income statement is healthy (JSE: NTC)

This is a prime example of leverage

For businesses with extensive fixed costs (like a hospital group), operating leverage is a powerful thing. It only requires modest revenue growth for there to be a much stronger result by the time you reach the bottom of the income statement.

Netcare’s revenue for the six months to March 2026 was up 4.8%. EBITDA increased by 6.6%, operating profit was up 7.4% and HEPS jumped by 21.2% thanks to the share buyback programme. The interim dividend followed suit, up 22.2%.

The balance sheet is also in good shape, with net debt to EBITDA at 1.2x.

Return on invested capital (ROIC) increased from 11.9% to 12.4%. For a defensive business, that’s a solid return!

Guidance for the full year is for revenue growth of between 4.0% and 4.8%. That’s softer than the first half of the year, with changes made by medical schemes as one of the pressure points going into the second half.

Ghost Bite: Hospital groups aren’t exactly seen as growth assets, so this kind of earnings jump is really impressive. The share price jumped by 7% on the day of release, so the market quite rightly approved of the numbers.

A period of solid growth at Omnia (JSE: OMN)

The group achieved an acceleration in earnings in the second half

Omnia’s trading statement for the year ended March 2026 is highly encouraging. The group achieved HEPS growth of between 17% and 23% – a great outcome for investors. Perhaps most importantly, HEPS growth in the first half of the year was only 11%, so there’s plenty of positive momentum here.

Although they talk about strong cash generation in this period, the net cash position has actually dipped slightly vs. the prior year. We will have to wait for detailed results in early June to see why.

Ghost Bite: Omnia is up 28% year-to-date and 41% in the past year. There aren’t many companies with a share price chart that has literally shrugged off the macroeconomic volatility like this:

Pick n Pay is still going backwards (JSE: PIK)

There’s all to play for in the s189 process

Pick n Pay’s numbers require a careful read. In addition to the performance at store level, there are other important movements.

It’s also key to remember that this is a 53-week trading period, so that flatters numbers like turnover growth unless you use the comparable 52-week numbers.

We begin with the store-level performance, as that’s what makes or breaks the story. On a 52-week vs. 52-week basis, group turnover was up 3.4%. But underneath that number, you’ll find Boxer (JSE: BOX) up 12.3% and Pick n Pay down 1.6%.

The trading profit line is where that deviation really comes through. Boxer saw a R330 million increase in trading profit, while Pick n Pay saw a further R404 million deterioration in the trading loss to R953 million!

This is why I talk about Pick n Pay eating its golden goose by selling the Boxer shares and ploughing the money back into the Pick n Pay group.

Here’s another important point: Pick n Pay’s trading loss after leases is actually R2 billion. That’s the number to remember from these results.

It’s not all bad. For example, the Pick n Pay company-owned supermarkets achieved an acceleration in like-for-like sales momentum from 3.3% to 3.9%. The gross profit margin improved by 40 basis points.

Even the highlights wash away quickly though as you work through the numbers.

When you see things like a 6.7% increase in like-for-like trading expenses in Pick n Pay (vs. 3.9% sales growth), it’s not hard to see why the losses are getting worse. The increase in gross margin was more than offset by the pressure at store level. It’s little wonder that Pick n Pay will be pursuing a s189 process to try and right-size the store costs.

Moving on, the Pick n Pay franchise supermarkets could only grow by 0.9%, so the store owners are somehow doing a worse job than the corporate managers. This remains an absolute mystery to me.

Pick n Pay Clothing standalone stores had a shocking second half of the year, down 5.6% in that period and dragging down the full-year results to growth of just 0.7%. They blame an “exceptionally soft clothing market” in that period. Look, things are tough in South Africa, but to go backwards by 5.6% and then blame it on the economy is pretty wild.

What you’re hopefully taking from this is that Pick n Pay’s turnaround is far from guaranteed. This even comes through in the audit report, where the “matter of most significance to the current year’s audit” was the recoverability of deferred tax assets. In other words, the auditors had to do a lot of work in figuring out whether it’s a fair assumption that Pick n Pay will actually have any future taxable profits at all!

As a final point, Pick n Pay ate R2 billion in cash over the past year. This leaves them with R2.4 billion in cash before the proceeds of the latest sale of Boxer shares. They simply have to stem the bleeding in the next financial year.

Bear with me. There are two other complexities I want to cover.

The group increase in profit before tax and capital items of R597 million can be largely attributed to a R681 million improvement in net funding interest. Or, put simply, the fact that they raised equity and repaid debt means that the cost of capital isn’t on the income statement. There is no accounting charge for the cost of equity capital, even though investors certainly are demanding a return.

Another importance nuance in these numbers is that the increase in the Boxer non-controlling interest means that Pick n Pay shareholders are getting less of the Boxer goodness by the time we reach headline earnings level. They are consolidating all of Boxer (which means all the revenue growth as well), with the adjustment made right near the end for how much Pick n Pay actually owns. In a period where the Boxer stake has been reduced significantly, that creates a mismatch between the income statement and the HEPS number.

Ghost Bite: The schizophrenia of the market headlines around Pick n Pay tells me that very few people actually understand the numbers or know how to read the details. The share price is going to bounce around accordingly. The real story is that the s189 process at store level is going to be critical – can they get it right without affecting the experience for shoppers?

PPC’s giant keeps awakening (JSE: PPC)

The turnaround story continues

PPC has been one of the best turnaround stories in the JSE in recent years. The positive momentum has continued, with HEPS for the year ended March 2026 expected to increase by between 20% and 33%.

This puts it in a range of 48 cents to 53 cents. If you adjust for the foreign exchange losses on USD hedges, then HEPS would be between 54 and 60 cents. For further context, the share price is R6.85, so PPC’s turnaround has taken it into the double-digit P/E multiples.

The company has attributed the recent growth in HEPS to a number of factors across the business, most of which have a flavour of efficiencies and cost management rather than outright growth.

Ghost Bite: PPC’s “Awaken the Giant” strategy would go a lot faster if we had more infrastructure investment in this country. Any company playing in that value chain has had to look in the mirror to find earnings growth, with efficiencies as the focus instead of investment in growth. We can only dream.

RMB Holdings has impaired its NAV almost down to the AttBid offer price (JSE: RMH)

There are broader questions that need to be asked about sector NAVs

RMB Holdings kept SENS busy on Monday. One of the announcements gave an update on the level of acceptances by shareholders of the AttBid offer. With that offer due to close at the end of this week (29 May at noon), they’ve received acceptances by holders of 4.15% of shares in issue.

Together with the existing stakes and other shares bought in on-market trades, this takes the concert parties to a holding of 47.93%.

Separately, the company released financials for the six months to March 2026. Aside from the numbers, the release announced the resignation of CEO Brian Roberts with a one-month calendar notice period. The non-executives are also resigning once the offer closes, so there’s a complete change in the boardroom.

The key number in the results is the net asset value (NAV) per share, which has dropped by 27% from 68.5 cents to 50.3 cents due to a large impairment on the Atterbury stake from R770 million to R498 million.

The offer price is 47 cents per share, so the NAV is only slightly above that level. Those who are angry about the deal will say that this is far too convenient. Those in favour of the deal (along with many accountants) will point out that a market price is a strong indicator of value.

The challenge for RMB Holdings is that the Atterbury portfolio is by far the biggest part of the balance sheet. Monetising this stake was so difficult that it eventually led to this scenario where the Atterbury owners are buying RMB Holdings. The original intention was for it to be the other way around!

Ghost Bite: I think that NAV does a poor job of reflecting market realities. Auditors in the property sector should be paying far more attention to how realisable the NAV numbers actually are, especially where the holding structures in the underlying assets are complex.

Results of previous poll:

Nibbles:

- Director dealings:

- Nothing to report here today!

- Hosken Consolidated Investments (JSE: HCI) has released a trading statement for the year ended March 2026. HEPS is expected to jump by between 45% and 55%. Results are due this week and given the complexities of the HCI group, it will be important to drill down and find the drivers of this performance. We already know that one of the reasons for the positive swing is the substantial prior-year losses in the energy business.

- Trematon (JSE: TMT) is busy with a value unlock strategy of selling off their assets. The Club Mykonos Langebaan disposal is due for shareholder vote soon, while the potential disposal of the Generation Education group is in an early stage of negotiations. The latest trading statement reflects intrinsic NAV per share of between 145 and 155 cents. The current share price is R1.06. The movement in intrinsic NAV is irrelevant, as the company has paid major distributions to shareholders that have reduced the size of the balance sheet.

- enX (JSE: ENX) has announced a special dividend of R1.92 to be paid at the end of June (subject to SARB approval – a bit of a wildcard at the moment in terms of timing). This is based on the proceeds from the sale of Trichem SA. The current share price is R4.56.

- Mantengu (JSE: MTU) has suffered a substantial negative move in earnings. The headline loss per share for the year ended February was -82 cents vs. a loss of -23 cents in the prior period. The share price is just R0.40 per share, so they are now on a P/E of -2x. My bearishness wasn’t misplaced.

- In a trading statement for the year ended February, Mahube Infrastructure (JSE: MHB) confirmed that the headline loss per share will be between -35.53 cents and -40.38 cents. That’s a horrible swing from HEPS of 61.26 cents in the prior period. Aside from lower dividend income from one of the wind assets, the numbers have been impacted by negative fair value movements due to macroeconomic factors. Higher bond yields aren’t kind to renewable energy and infrastructure valuations, as these are long-duration cash flows.

- Copper 360 (JSE: CPR) released a trading statement for the year ended February 2026. The headline loss per share is expected to be between -26.91 cents and -29.75 cents. This is at least an improvement on the prior period of between 12% and 20%.

- For those interested in Nu-World (JSE: NWL), the company has released a circular giving more information on why the company is looking for a resolution from shareholders that gives them the authority to issue shares. I can only imagine that shareholders weren’t thrilled with the initial notice, as the company gave the market nothing to work with in terms of the intended use of capital.

- In a tragic reminder of the ongoing dangers in the mining sector, Harmony Gold (JSE: HAR) reported a loss-of-life incident at Mponeng Mine. Two employees didn’t make it home to their families thanks to a shaft engineering incident.