In this edition of Ghost Bites:

- Anglo American will sell the steelmaking coal business for up to $3.875 billion

- Astral Foods had a spectacular year

- Calgro M3 has been in an infrastructure investment phase

- enX’s remaining businesses look tough

- Famous Brands is a mixed bag

- Harmony Gold is on track to meet full-year guidance

- Nutun is reducing losses far too slowly

- Pick n Pay is eating the golden goose

- Santam’s prior period was the eye of the storm(s)

- SPAR doesn’t have to pay anyone to drag the South-West England business away

- Spear REIT remains bullish as ever on the Western Cape

- WeBuyCars – but can they sell more of those cars this year?

Anglo American will sell the steelmaking coal business for up to $3.875 billion (JSE: AGL)

Much of the purchase price is structured as an earn-out

Anglo American has found a buyer for the steelmaking coal mines in Australia. Dhilmar Limited (a UK-based private company) is willing to pay up to $3.875 billion in cash for the mines, with $1.575 billion in an up-front payment and $2.3 billion as an earn-out.

Together with the prior sale of the Jellinbah mine, this means Anglo American has exited its overall steelmaking coal operations for up to $4.9 billion in cash.

And in case you’re wondering, Anglo American is still fighting with Peabody about the latter’s decision to walk away from a deal for these assets based on an alleged material adverse change.

Ghost Bite: As we saw with Peabody, a deal is never a deal until the regulatory conditions are met. There’s also a big earn-out here to worry about, running for five years with quarterly payments. Still, this is a step in the right direction for Anglo’s strategy. Now if only they could find a buyer for De Beers…

Astral Foods had a spectacular year (JSE: ARL)

Yet the share price remains under pressure

When poultry businesses do well, they do really well. Astral Foods has proven this with their interims for the six months to March, reflecting a rather outrageous jump in HEPS of 467% despite a revenue increase of just 11%!

Welcome to the world of operating leverage, something that the chicken industry is famous for. With structurally low margins and a high proportion of fixed vs. variable costs, profits can do wild things in response to modest moves in revenue. In case you need more convincing, net operating profit margin has jumped from 2.5% to 10.2%. You won’t see that kind of move in many industries.

Despite a significant increase in working capital in response to revenue, the group still improved its net cash balance by 13.7% to R1.15 billion.

The Feed division isn’t where you’ll find the major jump in profits. Despite volumes being up 9.8%, revenue was flat due to lower selling prices. But with operating profit up by 23.2% to R366 million, the benefit of solid cost control is visible here. Margins improved from 5.6% to 6.9%.

The Poultry division is the wild child in the group. Revenue increased by 14% thanks to an uplift in margins and selling prices. Here’s the real kicker though: they swung from an operating loss of R26 million to an operating profit of R848 million! This took operating margin from -0.3% to 8.4%.

The outlook statement is sobering after such exciting numbers. Management has correctly flagged inflation risks in this environment of high oil prices. They’ve also pointed to an expected drought in the 2026/2027 summer growing season, as well as the ever-present risk of bird flu.

Ghost Bite: This is a tough industry that can turn paupers into kings – and back into paupers just as quickly. The share price usually isn’t as volatile as the earnings, as the market knows that earnings will average out to something more reasonable over time. The share price is up 29% over 12 months, but dipped almost 3% after the release of these results. Technical traders may want to check out the chart as it drops towards an interesting support level.

Calgro M3 has been in an infrastructure investment phase (JSE: CGR)

This significantly impacts the cash flow story

Calgro M3’s latest period (the year ended February 2026) has been defined by the commencement of infrastructure installation at Bankenveld District City. This is one of the main reasons why net cash from operations has swung from positive R34 million to negative R99 million. During a heavy investment period, they absorb cash that is subsequently released when the units are sold.

This is just one of the things that makes the property development model tricky to operate. Bulls would argue that this is also what contributes to the company having a moat!

The Bankenveld project is described as a landmark project. Just the initial infrastructure phase will unlock a pathway to 6,000 serviced opportunities over the next five years, rolled out in phases. They’ve taken on a huge project in an unforgiving time in the world, so execution will have to be perfect.

Gross profit margin for the segment contracted from 27% to 24%. Management has been warning the market that gross margin was running at unsustainable levels.

The Memorial Parks business is designed to smooth out the cash flows and bring them a capex-light source of income. Revenue increased from R68 million to R86 million. For context, revenue in the property segment was R942 million. Memorial Parks may be a lot smaller, but the division runs at a gross profit margin of 54.9%! The goal is for cash collections in Memorial Parks to be at a level that covers group overheads.

If we look at the overall numbers, we find that HEPS fell by 8.4%. The final dividend was flat in an effort to cushion the blow to investors. Net debt to equity has increased from 0.64x to 0.74x. Periods of major infrastructure development don’t look great in the financials.

Ghost Bite: Property development is one of the most challenging games out there. I have plenty of questions planned for management on Unlock the Stock this week. Be part of the discussion by registering here to attend.

enX’s remaining businesses look tough (JSE: ENX)

Be cautious of the long tail of businesses in listed groups

enX has been a typical value unlock story, with disposals of businesses and subsequent returns of capital to shareholders. What often happens in these scenarios is that groups are left with the least appealing businesses at the end. This makes sense, as they would be the hardest to sell. Squeezing out that last bit of value is very important.

In the six months to February 2026, enX has demonstrated exactly how hard this can be. Revenue is down 37% and they’ve swung from a profit of R16 million to a loss of R6 million. They were actually already in an operating loss position of R12 million in the prior period – it was just shielded by the R29 million return on large cash balances in the group that took them to a net profit. With cash returned to shareholders, there’s nothing to mitigate the losses.

One of the sources of revenue decline is the lumpiness that is inherent in project-based work on data centres. This makes it really difficult for investors to forecast earnings. They have other headaches as well, like a business that sells generators – a less lucrative space now that Eskom is working.

Ghost Bite: These continuing operations sound like a tough scenario to manage. With the imminent release of escrow funds from the West African International sale, enX still has value to return to shareholders. I just wouldn’t underestimate how difficult the remaining stuff will be.

A mixed bag at Famous Brands (JSE: FBR)

The supply chain is driving their performance

The Famous Brands share price has been under pressure and is currently sitting close to 52-week lows. The market is becoming increasingly scared of consumer businesses as we head into an inflationary period, so it will take special numbers to inject some positive momentum into the share price.

The results for the year ended February 2026 aren’t going to do it. There are some positives, but there are also big question marks around the scrappy performance in the operating segments outside of supply chain.

As group context, revenue growth was 5.6% and HEPS jumped by 12.1%. The dividend per share increased by 10.7%. The shape of this income statement wasn’t thanks to operating leverage, as operating profit margin dipped from 11.0% to 10.9%. Operating profit only increased by 4.5%. Instead, it was all about the financial leverage, with a 13.3% decrease in borrowing costs that drove the jump in HEPS.

Notably, free cash flow has dropped by 9.1% to R662 million. You have to really dig to figure out why, as capital expenditure was actually flat at R214 million. The culprit is tax payments, so that’s probably more of a timing thing than an indication of deteriorating return on capital over time.

Net debt has declined by 5.4%, so net debt to EBITDA has improved from 0.89x to 0.82x. This gave them the balance sheet flexibility to introduce a share buyback programme in January 2026. With R54 million invested thus far, this is a positive signal around capital allocation discipline in the group. Being able to accelerate this programme into a weakening market would make a big difference!

We now move to the segmental information, where it becomes clear that Famous Brands is fighting every day to keep things moving in the right direction.

Leading Brands (the typical takeaway brands that you’ll find everywhere) achieved revenue growth of 6% in South Africa. Like-for-like growth was just 2.8%, so most of the growth is coming from an expanding footprint. Operating profit increased by 5% to R516 million.

The SADC region saw a decline in revenue of 6% and a nasty drop in operating profit from R51 million to R29 million. The decrease in profit in SADC offset most of the incremental operating profit gain in South Africa.

In Africa and the Middle East, revenue fell by 17%. Despite this, the operating loss somehow improved from R43 million to R35 million.

It’s the oldest story in the world: why don’t they just focus on Leading Brands in South Africa, instead of trying to operate in multiple regions?

The scrappy set of numbers in Leading Brands is joined by a poor performance in Signature Brands. They are blaming consumer pressure, but I personally think they are just getting smoked by Spur Corporation (JSE: SUR) and their excellent businesses like Hussar Grill.

The Famous Brands portfolio is extremely uninspiring by comparison, with only a small uptick in revenue and an increase in the operating loss from R9 million to R11 million. Famous Brands should stick to takeaways instead of trying to beat Spur (and others) at their own game.

In the UK, revenue fell by 10% and the operating loss was R10 million vs. an operating profit of R7 million. My prior comments about different regions are still relevant.

By now, you must be wondering where Famous Brands actually makes any money!

The answer lies further back in the value chain. Supply chain – SA increased revenue by 7% to R6.2 billion. Operating profit improved by 14% from R444 million to R504 million. This is where they make up for the challenging performance in the franchising side of the business.

The truth is that these things go hand-in-hand. They can’t really operate one segment without the other. By controlling more of the value chain, they can make decisions like not passing coffee and beef cost pressures onto the underlying franchisees. They’ve used other initiatives to drive growth as well, like bringing Coca-Cola and frozen retail product distribution in-house.

Ghost Bite: Like so many other relics of the Lost Decade in South Africa, Famous Brands would do a lot of good for its valuation by simplifying its exposure and focusing on its home market instead of random international operations.

Harmony Gold is on track to meet full-year guidance (JSE: HAR)

If they do, it will be the 11th consecutive year of doing so

Harmony Gold’s operational update for the nine months to March 2026 was met with smiles from investors. The company is on track to meet full-year guidance across key metrics for both gold and copper.

As always, “meeting guidance” and “increasing production” are two different things. Sometimes, mining companies guide for flat production, or even a decrease, depending on underlying operational needs. Sure enough, gold production was up 5% in the third quarter, but still down by 3% year-to-date in line with the plan.

The average gold price has shot up by 39%, so that’s doing a great job of offsetting the dip in production. The other pressure point that needed to be overcome is the 14% increase in all-in sustaining cost (AISC) in gold. Free cash flow in the gold business jumped by 87% year-on-year!

The balance sheet has been quite the story. They’ve moved from net debt of R5.6 billion to net cash of R1.3 billion over a period of just three months. With a critical 24-month programme ahead (including the Eva Copper project in Australia), they need a strong balance sheet and no execution missteps.

In case you’re wondering, the company explicitly notes that labour and electricity are its major input costs. Although they are monitoring higher oil prices, they don’t expect any risks to guidance from the spike in energy prices. Of course, if oil prices stay higher for longer, then the inflationary pressures will come through indirectly.

Harmony’s share price is only slightly in the green over 12 months. It’s down 21% year-to-date due to the correction in the gold price.

Ghost Bite: If volatility bothers you, then the mining sector probably isn’t where you should be investing your money.

Nutun is reducing its losses far too slowly (JSE: NTU)

How did such a successful part of Transaction Capital end up in this position?

We know what happened to SA Taxi. We know that WeBuyCars (JSE: WBC) ended up separately listed. But what I struggle to understand is how the remaining business in Transaction Capital, now called Nutun, has ended up being such a difficult story.

Years ago, Transaction Capital Risk Services (the division that became Nutun) was a very good business. They made proper money by collecting debt books either on a principal basis (they buy the book for cents in the rand and collect it) or on behalf of clients on an agency basis.

Looking in from the outside, the business model hasn’t changed. But the results sure have, as despite a revenue increase of 10% and an EBITDA increase of 36% in the South African business, Nutun has still ended up in a loss-making position. The amortisation of the underlying book plus the interest costs in the group add up to more than the EBITDA generated by the collection business.

Instead of focusing exclusively on delivering improvements to that business, Nutun has been building out a business process outsourcing operation that targets international clients. Revenue dipped by 1% in that segment and EBITDA fell by 15%. EBITDA was just R80 million vs. R710 million in Nutun South Africa. Although this segment is more profitable right now than the South African business, it’s much too small to make up for the decline in the core operations.

Bring it all together and you’ll find a headline loss from continuing operations of R63 million vs. a headline loss of R122 in the prior period. They also report a metric called continuing core loss, which was R63 million in this period and R71 million in the prior period. If we use management’s metric, this tells us that the losses are being reduced far too slowly.

There’s a lot of talk in the outlook statement about the use of AI. This has positive and negative elements. Although AI might improve Nutun’s internal operations, it’s also putting pressure on margins due to a negative impact on contact centre demand.

Ghost Bite: It’s very hard to remain patient with this particular stock. The price is down 44% over 12 months.

Pick n Pay is eating the golden goose (JSE: PIK)

As I suspected, the “value unlock” trade is really hard to catalyse

I’ve been having a number of debates on social media and in investment circles around Pick n Pay. The bull case is simple: Pick n Pay currently trades at a vast discount to the underlying look-through exposure to Boxer (JSE: BOX). The bear case requires more analysis, including an allowance for marketability discounts and potential tax on disposal of Boxer, as well as a look at the balance sheet to see how enormous the lease obligations at Pick n Pay are.

The big win for shareholders would be an offeror swooping in and buying the entire Pick n Pay group. The problems are that (1) this is unlikely to happen while Pick n Pay is still going backwards and (2) the Competition Commission would probably add so many conditions to the deal that it would destroy the economic appeal.

So where does this leave Pick n Pay? They have little choice but to reduce the Boxer stake by selling it at the favourable current market price. The latest update is that they will sell 11.5% of Boxer, leaving them with a controlling stake of 54%. There isn’t much room left for them to keep dripping shares into the market without losing control of Boxer.

If the turnaround was going well, they could use the proceeds of up to R4.7 billion (subject to bookbuild pricing) for share buybacks at Pick n Pay level, a genuine catalyst for a major positive move in the price. Alas, things are still going badly based on the most recent trading update, so they need to eat these proceeds by investing them in the turnaround.

According to management, the entire Pick n Pay store estate has been upgraded and they’ve improved in-store execution. I must be honest that I haven’t heard positive feedback from even a single person in my friend group. Even if the corporate stores are doing better, Pick n Pay has a large franchise estate that has been performing poorly (and irritating customers along the way).

If there’s a successful turnaround happening, it’s hidden under a lot of ugly numbers.

Ghost Bite: Thus far, I haven’t been proven wrong about Pick n Pay’s performance in recent years and how they are being crushed to death by much stronger competitors. I look forward to being wrong, as we need a competitive grocery market that provides jobs.

Santam’s prior period really was the eye of the storm(s) (JSE: SNT)

Underwriting margins have come back down to earth

Santam’s latest numbers for the three months to March 2026 are a great reminder of the risks that insurers carry in their business. Underwriting margins can spike higher in a lucky period of only a few major disasters. But when mother nature strikes, these insurers quickly see their margins return to targeted levels (or worse).

Notably, this update doesn’t include the recent flooding in the Western Cape. Will will only see that come through in the quarter ending June.

The conventional insurance business achieved 9% growth in gross written premium. Within that performance, there are fast growing parts of the business (like Miway and Santam Direct) and areas that had a slow start to the year (like Santam Re).

The underwriting performance is where you’ll see the impact of flooding in the northern part of South Africa and the wildfires in the Western Cape. This led to a loss (net of reinsurance that offsets some of the pain) of R430 million. Despite this, underwriting margin was still above the mid-point of the 5% to 10% target range. This shows you just how fat the margins can be in a period of no major disasters.

The other critical source of value for shareholders is the return earned on insurance funds. The market wasn’t particularly kind to them in this quarter, with a return on insurance funds of 2% of net earned premium. Similarly, the group’s own capital experienced underperformance in investment returns. It won’t surprise you that the Alternative Risk Transfer business was also impacted, with the investment returns offsetting some of the progress made in the operating results of that segment.

The market is particularly interested in the Lloyd’s insurance syndicate that Santam has put together in London. They started writing business on 1 January 2026. They expect a strong contribution to premium growth over the rest of this year, although an operating loss of R300 million is expected in the first year.

The group is also developing its business in India, with a licence to establish a reinsurance brand in India’s GIFT City, the first operational greenfield smart city in India and an International Financial Services Centre.

Aside from market pressures this year and the impact of Western Cape flooding (which is still to be quantified), Santam has flagged the oil price as a source of inflation and thus upside risk to the cost of claims.

Ghost Bite: The share price is down 12% year-to-date, so the market is already aware of at least some of the issues. I wouldn’t underestimate the impact of the Western Cape storm – it’s a densely populated area with valuable property that has suffered considerable damages.

SPAR doesn’t have to pay anyone to drag the South-West England business away (JSE: SPP)

That’s good news, if you can believe it

After the horrors of SPAR’s disposal of the business in Poland, the market learnt that equity actually can go below zero if a balance sheet is bad enough. SPAR literally had to pay someone to take Poland away. They were thankfully more proactive with the Swiss business to avoid a similar disaster.

Now there’s another disposal on the table: the South-West England business with 71 company-owned stores and the associated infrastructure.

The price? £13 million. The expected proceeds after costs? Zippo. Nothing.

On the plus side, they are also in talks to sell 63 stores to third-party operators, with the hope being that they will complete the deals by September 2026. If shareholders are really lucky, perhaps there will even be some cash!

Ghost Bite: There’s all to play for in this turnaround story. To learn more about the strategy, check out this recent podcast that I did with SPAR CEO Reeza Isaacs.

Spear REIT remains bullish as ever on the Western Cape (JSE: SEA)

They are looking to do more acquisitions in the province

Spear REIT is a rare example of a focused REIT on the local market. Where so many funds have gone offshore in search of growth, Spear is like one of those kids from the southern suburbs who hasn’t ever left the Western Cape!

Jokes aside, they need to be cautious of making statements like “the Western Cape from a real estate perspective will continue to outperform the rest of South Africa”. Market cycles have a way of humbling those who use the word “will” – especially as governance changes in Gauteng could be the catalyst to stem capital flows from Gauteng to the Western Cape.

The reality is that Cape Town is at breaking point in terms of property prices, access to schools and traffic on busy routes. At some point, semigration will slow down to a crawl – just like the morning traffic on the N1. I don’t think Joburg will claw back all of the lost ground in my lifetime, but investments are forward-looking in nature. We could reach a point where Gauteng outperforms the Western Cape in terms of year-on-year growth.

Nonetheless, Spear is eyeing a number of acquisitions in the Western Cape. They expect to do deals worth between R500 million and R1.5 billion during FY27.

With 6% growth in the distribution per share for the year ended February 2026 and a 5.8% uplift in tangible net asset value (NAV) per share, I’m not surprised that they are confident enough to keep building the portfolio. A loan-to-value ratio of just 22.9% also helps!

If we dig into the portfolio, we find that the industrial portfolio is 43.7% of the group’s asset value. It boasts occupancy levels of 98.7% and lease escalations of 7.1%, so this is an excellent underpin to the growth story.

The retail portfolio has been boosted by the acquisition of Maynard Mall. It’s hardly a shiny and exciting centre, but they got it on a yield of 9.54%. The centre is in a busy commuter-focused area and gives them more exposure to national tenants, so they are excited about this recent addition to the story. The retail portfolio’s occupancy rate of 97.56% is solid, with in-force escalations of 6.61% and negative reversions of only 0.71%

The commercial portfolio has 92.55% occupancy, a rate that many office funds can only dream of. The in-force average escalations of 7.23% are high relative to the market though, leading to negative rental reversions of 6.05% on new leases.

The outlook for FY27 is growth in distributable income per share of between 6% and 8%. That’s the kind of real growth (i.e. in excess of inflation) that investors are looking for.

Ghost Bite: Spear REIT is seen as one of the safe bets in the local property sector, with an excellent total return in recent years. The big question is whether the Western Cape can maintain the level of outperformance that is now baked into this share price.

WeBuyCars – but can they sell them quickly enough? (JSE: WBC)

A market in a state of flux has driven some tough numbers

Let me begin by confirming that I remain a shareholder in WeBuyCars. I still believe in the long-term power of this business. If the biggest, most efficient used car player in South Africa is struggling right now, then what do you think is happening to the marginal names? In long-term plays, you need to be willing to ride the volatility.

Unless you’ve been living under a rock, you would’ve noticed that the brands on the road around you have changed. Instead of only Japanese and European cars, we are seeing plenty of Chinese and Indian names. This has filtered through into the used market, where prices have been hurt by how compelling the new car alternatives are. This is why we’ve seen an uptick in new car sales.

This transition in the market needed to churn through the WeBuyCars inventory base. The market hasn’t exactly been patient with this, as the share price has lost a quarter of its value year-to-date. It didn’t help that the founders reduced a big chunk of their holdings to go off and do the RMB Holdings (JSE: RMH) deal alongside Atterbury. Then again, I can’t blame them for diversifying their wealth into something as different as property!

Looking at the performance for the six months to March 2026, units bought increased by 3.2% and units sold only increased by 2.3%. They are living up to their name around buying cars, but the market doesn’t enjoy seeing this differential and a build up of stock – even if it happened during a period of expansion of trading space!

Revenue increased by 7.8% though, so this must mean that the average price per vehicle sold has increased. The official corporate speak is that they are following a “more disciplined percentile-based buying strategy” in more affordable inventory, which they correctly identify as their core competitive position. But with underlying mix effects and other factors at play, this doesn’t mean that they are chasing more expensive vehicles. It’s actually quite the opposite, as they are looking to stick to their range that works well.

This revenue uplift wasn’t enough to protect HEPS, which dipped by 1.7%. The 10% increase in the dividend sends a positive message to the market, but that message is watered down by the HEPS story.

The first and most obvious source of pressure on profits has been the impact on gross margin of the inventory needing to decrease in price to offer value vs. new car alternatives. Those Chinese brands will be entering the used market at an increasing rate though, so part of my investment thesis is that this issue will be worked through the system soon.

A source of pressure on HEPS has been the roll-out of three new supermarkets. It takes a while for the new facilities to become profitable.

Momentum into the end of the period is one of the reasons why the share price found some support on the day of these results. The group achieved an all-time sales record in March 2026, having bought more cars during January 2026 than ever before.

With the national parking bay footprint up by 23.6%, there’s plenty of space for growth here. The market will be looking for a meaningful upswing in sales in the next period. They are also open to smaller new facilities where this makes sense, like a 380 bay property in Bloemfontein (vs. 1,300-bay facilities recently opened in Cape Town and Pretoria).

Bolt-on acquisitions are also part of the story, with the deal for a 49% equity stake in GoBid being concluded in this period. Importantly, the deal comes with a pathway to control and even full ownership over time. This supports the strategy of operating in more areas of the used vehicle market, with GoBid focusing on damaged vehicles that cannot be sold through the usual channels.

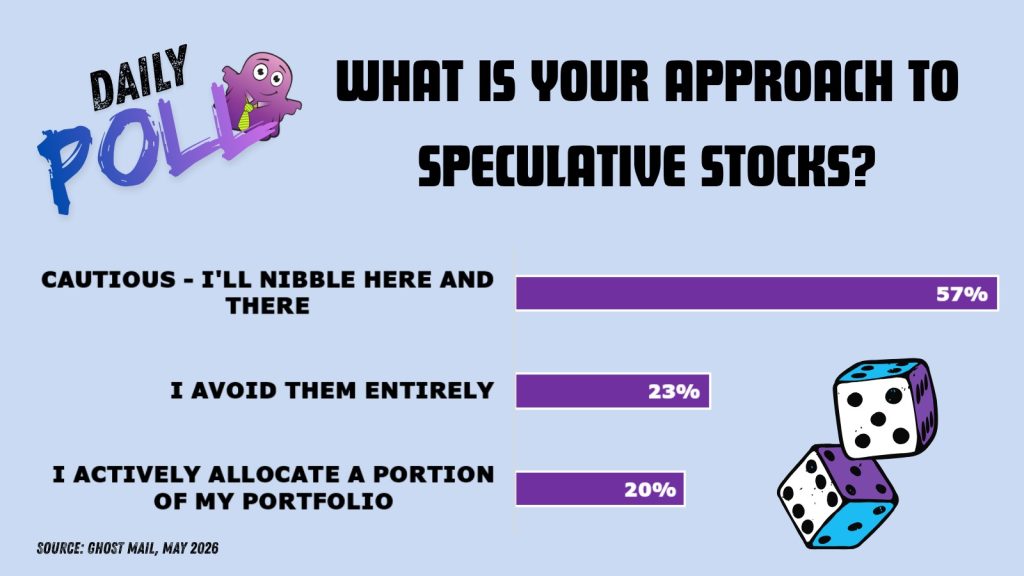

How do you feel about these numbers and the share price?

Results of previous poll:

Nibbles:

- Director dealings:

- The CEO of Choppies (JSE: CHP) and a senior management member sold shares worth a collective R2.8 million.

- A top executive at British American Tobacco (JSE: BTI) sold shares worth around R860k.

- A director of Labat Africa (JSE: LAB) acquired shares worth R285k in off-market transactions.

- Glencore (JSE: GLN) and Anglo American (JSE: AGL) have a headache at Collahuasi, the important copper mine in Chile that they each have a 44% stake in. A tribunal in the country has set aside the Environmental Authorisation that was granted in December 2021. It specifically relates to a project to develop a water desalination plant and its effects on the local community and the marine environment. Although there’s no immediate impact on production, the plant is nearly complete and so this is a potentially serious issue. Collahuasi seems to have been blindsided by this, as they are seeking clarification from regulators on the specific aspects of the ruling.

- Lesaka Technologies (JSE: LSK) found an error in its headline earnings calculation. This relates to the treatment of fair value movements on equity securities. It looks scarier in percentage terms than in absolute terms. Headline earnings for the three months to March 31 2026 is 15% lower than first reported, but that’s a difference of $378k in the real world. The comparable period is a much bigger change, with a headline loss of $22.3 million instead of $5.4 million. Although it hits the comparable period far more than the recent period, investors still don’t enjoy seeing stuff like this.

- Nu-World (JSE: NWL), a consumer products company with a market cap of around R660 million, wants shareholders to give the board a general authority to issue shares. Although many companies have such an authority in place, investors tend to be nervous of giving management the right to dilute them over time. For maximum flexibility, the company is also asking shareholders for a general repurchase authority as well! Sometimes, you just want to have all options available to you. A circular has been sent to shareholders for the meeting scheduled for 17 June.

- RMB Holdings (JSE: RMH) has given an update on acceptances of the offer by AttBid. Thus far, holders of 4.11% of shares in issue have accepted the offer. Together with the existing holdings of Atterbury Property Fund and AttBid, this would take the concert parties to a holding of 47.88% in RMH. The closing date for acceptances is 29 May.

- ASP Isotopes (JSE: ISO) is running a bit late on the filing of its 10-Q form (its quarterly financials in the format required on the US market). They expect to get it done within five calendar days of the deadline, so hopefully they won’t irritate the SEC too much with this.

- Say what you will about Africa Bitcoin Corporation (JSE: BAC), but at least they are a persistent bunch. Despite having suffered many setbacks on the journey as a listed company, they are moving ahead with transferring their AltX listings to the General Segment of the Main Board of the JSE. This was made possible by a share sub-division that increased the number of shares in issue. With a market cap of just R170 million, this will be among the smallest names on the Main Board. Can they finally find some sustained positive momentum?

- Trustco (JSE: TTO) has renewed the cautionary announcement related to a potential delisting of the company. This has been going on for a while now.