Profits and cash flows look better at Aveng (JSE: AEG)

The order book has softened though

In construction, due to the immense pain that a bad contract can inflict, it’s possible to see profits improve substantially despite a drop in revenue. In fact, revenue can be a poor predictor of profitability, which is why I completely avoid investing in this sector.

We see this come through in Aveng’s results for the six months to December 2025. They reflect a drop in revenue from R16.6 billion to R14.2 billion, yet operating earnings swung beautifully from a loss of R356 million to profit of R107 million.

Even though infrastructure markets have softened in Australia and New Zealand, gross margin improved from 2.7% to 5.6% as the quality and implementation of projects improved. There’s also the substantial impact of the Jurong Region Line (J108) project in Southeast Asia and the Kidston Pumped Storage Hypro project in Australia, with combined losses of A$20.2 million in this period vs. A$76.7 million in the prior period.

Like I said – revenue is a poor predictor of profitability!

Aveng has recognised the forecast costs to complete those projects in this period, but the associated cash flows will be in the second half of FY26 and in FY27. It’s worth noting that cash on hand improved from R3.1 billion to R3.4 billion in this period.

Headline earnings came in at R4 million. That might not sound like much, but the comparable period was a loss of R399 million. At least they are back in the green, albeit only just.

There are other difficult contracts in the group as well, like the Tshipi project. Aveng is negotiating commercial settlements with various clients, with David Simpson appointed as the interim group CEO to focus on commercial resolution and delivery of underperforming projects. At the Moolmans business, Pieter van Greunen has been appointed as managing director, with the resolution of the Tshipi contract as one of the key focus areas.

The group heads into the second half of the financial year with work in hand of R38.6 billion, up from R37.5 billion in the first half. But it seems like success depends as much on resolving the legacy projects as it does on the new stuff.

And as a reminder, after a lot of work went into figuring out what to do with McConnell Dowell, Aveng has decided to keep that that business for now.

Clientèle’s numbers are complicated (JSE: CLI)

But they do seem to be heading in the right direction

Clientèle has released a trading statement for the six months to December 2025. Based on the JSE rules, the release of such an announcement immediately tells you that the numbers differ by at least 20% vs. the prior period. In this case, the percentage move is a lot bigger!

But we need to deal with some issues that are impacting the comparability of numbers.

One of the major distortions in the numbers is the bargain purchase gain of over R400 million related to the acquisition of 1Life. This is excluded from HEPS, which gives me a good opportunity to remind you that HEPS is the number that the market uses to actually judge performance.

Here comes another distortion that does impact HEPS though: a change to the application of IFRS 17 that led to a restatement of the interim results for the six months to December 2024. That may sound like a long time ago, but remember that this impacts the base period of comparison for the six months to December 2025.

But perhaps the biggest distortion of all is that Emerald Life has been consolidated for the first time in the latest numbers. This has resulted in HEPS increasing by between 92% and 112% vs. the previously reported numbers, a sizable jump that is essentially a doubling of HEPS at the midpoint of that range. After the base period was restated for IFRS 17, the expected increase in HEPS is between 43% and 63%.

There are a lot of adjustments to consider here, but the direction of travel is up.

Gemfields flags decent pricing for fine-quality rubies (JSE: GML)

But the lower-quality stuff is under pressure

Gemfields announced the results of a mixed-quality rough ruby auction held from 9th to 20th February. This is the auction that was deferred from December 2025. The auctions are always difficult to use to establish a trend, as the quality of the stones varies from one auction to the next.

In this case, they achieved auction revenue of $53 million, having sold 90% of the lots offered for sale and 88% of the carats offered for sale. The average price was $279 per carat.

Although fine-quality rubies attracted decent prices, management has indicated that other qualities were more “muted” due to the uptick in product on the market from illegal mining networks, along with weaker demand from China. The products may be beautiful, but it’s still a tough space to operate in.

Notably, this is the first auction that includes material from MRM’s second processing plant.

If we look at previous auctions over the past few years, the price per carat at this auction is the lowest that we’ve seen. Although Gemfields notes that this is because lower quality rubies weren’t offered at those auctions, the reality is that pressure on the average price per carat can’t be good news for shareholders. I doubt it’s much cheaper to extract a lower quality ruby vs. a high quality ruby, so the price per carat is still relevant to profitability.

Mr Price is ready to close the NKD deal (JSE: MRP)

Based on the lack of share price recovery, the market still doesn’t like it

A chart of the Mr Price share price makes it depressingly easy to see exactly when they announced the NKD acquisition. You’re looking for the precipitous drop in late 2025 that looks like someone threw the share price off the side of a cliff:

You may also note that the share price hasn’t really staged a recovery yet. Some efforts earlier this year to address the anger in the market stemmed the bleeding, at least, but there’s little doubt that the market is still angry about the deal.

Mr Price has gone ahead with the deal anyway, with the latest update being that all regulatory conditions have now been fulfilled. The deal is therefore subject only to the money actually changing hands. They are targeting a scheduled closing date of 31 March 2026.

In yet another effort to try to get the market on the same page as management here, there is an investor presentation scheduled for 17 March. I’m not sure how they will try to tell a better story that time around, but perhaps some pleasantly surprising nuggets will be shared.

Nedbank secures an important regulatory win in the NCBA deal (JSE: NED)

They have received an exemption from making a mandatory offer

In January this year, Nedbank announced an intention to acquire a 66% stake in NCBA Group, a major financial services operation in East Africa. Nedbank is well behind its peers when it comes to the African growth story, so this feels a bit like a game of catch-up.

To pay for the deal, Nedbank is using 20% cash and 80% new shares in Nedbank. The deal is worth a substantial R13.9 billion, so it’s not surprising that they can’t do a transaction of that size purely in cash.

An important component of the deal is that the remaining 34% of shares in NCBA will continue to trade on the Nairobi Securities Exchange. This makes the deal a manageable size for Nedbank, while giving them control via the 66% stake. Companies like to buy control, but not necessarily 100% of the earnings.

But in the event of needing to do a mandatory offer, Nedbank was prepared to switch the structure to an offer for 100% of the shares. This tells me that they want either 66% or 100%, but preferably nothing inbetween.

They don’t need to follow this route though, as the takeover law regulator in Kenya has provided the exemption from the mandatory offer, so 66% it shall be.

Another element to the transaction is that this is a pro-rata offer to shareholders, which also allows for excess applications for those who want to sell more than 66% of their shares to Nedbank (to make up for others who may not want to sell). Nedbank has received irrevocable undertakings to accept the offer from holders of 77.54% of NCBA shares in issue.

Octodec affirms guidance – but this portfolio sounds like hard work to manage (JSE: OCT)

Inner-city properties come with a host of challenges

Octodec might begin with a bullish narrative in its pre-close update for the interim period, but it quickly becomes clear that managing their property portfolio is anything but easy.

In an update that covers the five months from 1 September 2025 to 31 January 2026, the Johannesburg residential portfolio is one of the more obvious challenges. Octodec highlights the pressure on landlords to provide alternative solutions to failing council service delivery and infrastructure. Tenant affordability is another challenge. Nothing about this sounds particularly encouraging for rental yields.

On the plus side, at least the retail portfolio around Lilian Ngoyi Street has improved after the damage from the gas explosion was finally fixed. The Joburg CBD really is an example of how to play the property game on hard mode.

The overall retail shopping centre portfolio had a vacancy rate of just 0.2% as at the end of January 2026, which is better than the 0.5% reported for August 2025. The ugly duckling is Killarney Mall, currently held for sale with a vacancy rate of 17.7% at the end of January (in line with August). The launch of a Regus shared-office space at Killarney is expected to improve footfall.

The collection rate is largely okay, although they do highlight that one of their tenants is in business rescue.

Despite the portfolio being a tricky thing to manage, Octodec has plenty of experience in this space and the risks are well diversified. This has enabled them to raise debt at reasonable rates, with refinancing of maturing debt on improved commercial terms also being possible.

It also make a big difference that the loan-to-value ratio is on the right side of 40%, with disposals of nine non-core properties during the five months (for a total of R81.2 million at a 3.7% premium to book value) helping to achieve this outcome. Unutilised facilities increased from R675 million to R1 billion, so they have decent headroom on the balance sheet.

The goal is to get to 35% in the long term, achieved through further disposals of smaller properties in the portfolio. They also need to fund various capex projects of course, including the ongoing Gezina City project.

The weighted average cost of debt is down to 8.8% at the end of January 2026, an improvement from 9.1% in August 2025. This is thanks to the refinancing activity, as well as the lower overall interest rates.

Guidance for the year ending August 2026 has been affirmed, with expected growth in the distribution per share of between 0% and 4%. That’s not much, but at least it’s in the green.

Earnings fall at Sasol, but at least free cash flow is up (JSE: SOL)

Growth remains hard to come by

Sasol’s share price is up 62% in the past year. But for the six months to December, HEPS has fallen by 34%. Markets can be confusing things, especially for the likes of Sasol where the valuation is low and the the share price performance will depend on just how much bad news actually materialises.

With flat turnover (despite a 3% increase in volumes), Sasol’s adjusted EBITDA fell by 12%. Production volumes at Secunda Operations were up 10% and this no doubt informed some of the share price action, but the macro environment is still working against Sasol. The average rand price of oil fell 17%. Even the price of chemicals (in US dollar per ton) dropped, with the rand strength against the dollar putting further pressure on the translation of the international chemical results.

Capital expenditure fell by 43% to R8.5 billion, so free cash flow generation actually improved dramatically thanks to this. Free cash flow for the period was R0.8 billion vs. -R1.3 billion in the comparable period.

On a market cap of R89 billion though, R0.8 billion in free cash flow isn’t exactly an exciting yield (even if you annualise it).

Here’s the real kicker though: this is actually the first positive interim free cash flow for four years. When you’re used to dry bread, a piece of toast with butter can feel gourmet. I just wish that the butter was coming from improved cash flow from operations, rather than a drop in capex.

With net debt to adjusted EBITDA of 1.6x, the balance sheet is in reasonable shape. EBITDA can change quickly though, so this ratio is always at risk. Debt was brought down from R103.3 billion to R93.5 billion, so that’s an encouraging sign.

In terms of updated guidance, the dip in capex is expected to stick. They reckon that capex for the year will be R2 billion lower than previous guidance of R24 billion – R26 billion. Alas, the International Chemicals adjusted EBITDA is revised lower to between $375 million and $450 million, well off the previous level of $450 million to $550 million. This is a decrease in adjusted EBITDA margin, to between 8% and 10% vs. previous guidance of 10% to 13%.

There are no easy wins at Sasol, that’s for sure.

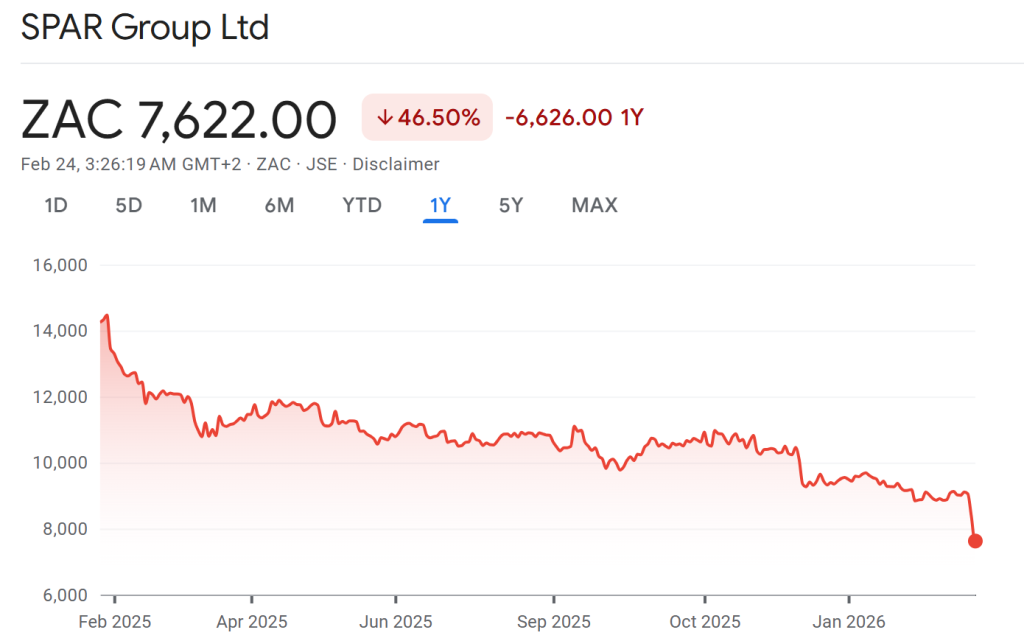

SPAR’s share price obliteration continues (JSE: SPP)

Will they ever recover from the catastrophic SAP implementation?

SPAR is such a good example of how the success of your local franchisee can be a terrible indication of the health of the franchisor. We’ve all shopped at a SPAR that we know and love, with a great deli and a product assortment that makes it unique in the local community. Yet for all the effort that goes into making that happen by the franchisee, we have a scenario where the holding company performance looks like something revolting that got cleaned out of a grimy corner of the storeroom.

Part of the problem is that the franchisees aren’t required to buy everything from the franchisor. In other words, SPAR as a wholesaler must compete with other suppliers to the stores. You would imagine that this is a no-brainer, as SPAR is surely the most efficient and obvious supplier to the stores. After all, they send one truck from the distribution centre that has everything on it.

Right? Well…

What happens when the distribution centre implements a new system in a way that is disastrous even by oh-no-this-retailer-is-going-with-SAP standards? And what happens when they do it in their traditionally-strongest regional market?

Also, what happens if that same company runs around in Europe dealing with problems elsewhere, instead of focusing on the home market?

Here’s what happens:

I actually have a small speculative position here, based on a thesis around believing that it would be difficult to fully destroy a brand that is part of the fabric of community retail in South Africa. I’m now wondering about whether it is so difficult after all.

CEO Angelo Swartz has decided to throw in the towel. He’s only 43 years old based on the SPAR website, yet this turnaround managed to burn him (and his family) out. That tells you something about how bad it actually is.

Reeza Isaacs is taking the top job, hopefully bringing some stability to the story. Megan Pydigadu moves from COO to CFO to replace Isaacs. And based on the latest trading update at the company, they have a lot of work to do.

For the 18 weeks to 30 January 2026, SPAR’s wholesale turnover from continuing operations was up just 2.1%. To make it even worse, their gross margin fell, which means they could only achieve this number through highly promotional activity to drive sales.

SPAR Southern Africa? Growth of just 0.9% – a shocker. Within that, Grocery & Liquor was just 0.8% (exceptionally poor), Build it fell 2.4% (also poor, but a tricky business) and SPAR Health was up 23.0%. Perhaps all the accountants looking at these numbers were at least buying their headache tablets internally.

In Ireland, growth was 3.1% in local currency and 6.1% in rand. This helps bring the group number up to the 2.1% noted above. Yay.

With internal selling price inflation of 2.6% in Grocery & Liquor, they suffered a negative move in volumes despite all the promotional activity. Although they try and make things sound better by referring to 2.3% overall growth in November to January (i.e. excluding a soft October that dragged them down to 0.8%), even the “better” number is actually very weak.

Another example of clutching at straws is to describe the high-income segment as showing a “modest recovery” with like-for-like growth of 1.6%. Modest, indeed. Compare this to Checkers and Woolworths Food, and you’ll quickly see just how bad SPAR is.

Retailer loyalty is the way they measure the extent to which franchisees procure from the wholesaler. Loyalty in KZN is at just 71.5% vs. 84% for the rest of South Africa, reflecting the immense hangover of the SAP implementation that left retailers stranded for stock. There’s even litigation around this, with claims related to the SAP implementation and how it affected the claimant. The initial claim was R5 million and the litigation “significantly exceeds” that amount. Other than the claimant and one other retailer, all KZN retailers have reached settlements with SPAR.

You can’t just stop a SAP process along the way. To get the full benefits, they need to finish the project. They talk about a risk-mitigated revised plan to finish the project.

My long-standing joke remains undefeated: Ernie Els is the only truly successful SAP implementation story.

The group has reiterated that they want to hire a Managing Director for the Grocery & Liquor business in South Africa. I’ll say it again: adding layers of management to the structure is not the answer.

And are they at least done with selling businesses in Europe? Not quite, with AWG in South-West England needing to be sold. I’m going to pull this pearler from the announcement, as it genuinely tells you everything you need to know about SPAR:

“Further, the Group does not anticipate needing to make a cash injection to effect the disposal.”

They are so accustomed to having to pay people to drag their rubbish away that they now need to specifically indicate to the market whether that will be happening again.

They talk about a transaction structure that has been “substantially agreed” for the AWG disposal. Let’s hope they can get it done quickly.

Somehow, against this backdrop, SPAR believes that they might be able to do share repurchases in the next financial year. Getting the authority from shareholders vs. actually being in a financial position to pull the trigger on share repurchases are two different things.

Overall, the company is now a steaming pile of you-know-what. I would’ve loved to buy the dip here, but I think it would be a safer bet to stick to the type that I’ll find in the chips aisle.

But what do you think? Do you believe they can restore SPAR to its former glory?

Nibbles:

- Director dealings:

- Despite all the positivity around Dis-Chem (JSE: DCP) (or perhaps because of it?), an associate of director Stanley Goetsch sold shares worth R11.2 million.

- An associate of a director of 4Sight Holdings (JSE: 4SI) bought shares worth R724k.

- Another day, another SENS announcement from ASP Isotopes (JSE: ISO) regarding US subsidiary Quantum Leap Energy. Except in this case, the update actually relates to a South African subsidiary of Quantum Leap Energy! Group structure aside, it relates to an agreement with the South African Nuclear Energy Corporation (Necsa) to collaborate, develop and produce High Assay Low Enriched Uranium (HALEU). This services contract builds on the previously announced memorandum of understanding between the parties. Necsa will provide facilities and infrastructure in Pelindaba, while Quantum Leap Energy will provide proprietary enrichment technology. The world’s energy needs are going through the roof right now thanks to AI data centre infrastructure and general industrial electrification, so ASP Isotopes and its subsidiaries are fully focused on addressing that opportunity.

- Telemasters (JSE: TLM) released a trading statement for the six months to December 2025. They have flagged a increase of 94% in HEPS, taking it from 0.35 cents to 0.68 cents. Note: I said 0.68 cents, not R0.68. So although the share price is under R2, it’s still trading on an enormous Price/Earnings (P/E) multiple.

- Louis Raubenheimer, son of Raubex (JSE: RBX) founder Koos Raubenheimer, has been appointed to the board of that company as an independent non-executive director. He has plenty of prior experience with the company, having held various roles from 1992 until 2022. His most recent role was running the Roads and Earthworks Division.