An historic day of fighting for the Blu Label bulls and bears (JSE: BLU)

There are few companies that have such vocal fans and critics

The Blu Bulls (of the non-frightening Loftus variety) are all over X, putting forward views on why the Blu Label share price remains undervalued. The bears are fewer in number (as usual – or perhaps just quieter), with a general feeling of “it’s too good to be true” in their arguments.

Personally, I’ve stayed out of this one completely, as the financial disclosure until this point has been too difficult to unravel. I’m not shy to put something in the “too hard” bucket and leave it for other people who have more time to dedicate to trying to understand a single stock. This approach suits investors who have highly concentrated portfolios, whereas I prefer a larger number of small stakes.

Having gotten that out the way, the latest news from Blu Label is the publication of the circular for the Cell C restructure and listing. They’ve also released a useful investor presentation showing the journey of the turnaround strategy and how they took Cell C to R11.1 billion in revenue in 2025 and R830 million in free cash flow.

Key to the thesis is the capex-light MVNO model, in which Cell C essentially provides the backbone technology that allows the likes of Capitec Connect (and many others) to use its distribution power to sell airtime and telecom services. This is where the bears tend to jump in, as they question the strength of the moat here and why others can’t win market share from Cell C.

One of the bullish responses is that the MVNO market is expected to expand by 2.3x to a share of total SIMs of 10.8%. This is according to Cell C of course, but it does strike me as plausible when you consider the distribution strength of the companies taking advantage of the MVNO opportunity. Even if Cell C has to fend off more competition, they are at least swimming downstream rather than upstream like most South African companies.

Even with Cell C becoming a separately listed group, Blu Label will remain a significant shareholder in the company. The good news is that all transactions will be on an arm’s length basis, which means that it will be much simpler to understand the financials of both companies. Importantly, the presentation notes that the Cell C listed company will be “largely self-funded” rather than reliant on the complex funding relationships currently within Blu Label.

The problem with a group that is so difficult to value is that one is never sure when the momentum is gone and it’s time to get off the bus. That’s why you can end up with a wild chart that looks like this:

Like with any company, the most sensible approach is to read the views of the staunch bulls and bears and then consider where you land on that spectrum. Personally, I would want to see this story play out for a while longer before I would even consider getting my own money involved. The telecoms sector has hurt many investors over the years and I’m cautious of it as a result.

Well done to those who have made money here!

Choppies is growing sales in Botswana (JSE: CHP)

If the Botswana economy is in trouble from diamonds, it’s not showing just yet

Choppies released results for the year ended June 2025 and they look good in terms of sales, with revenue from continuing operations up 14.6%. Things do go wonky further down the income statement, leading to HEPS from continuing operations dipping by 2.1%.

HEPS from continuing and discontinued operations increased by 19%, but that’s not a particularly useful measure here.

A far more important metric is like-for-like retail sales, which increased by 8.6% for Choppies. They also saw an uptick in gross profit margin in all segments except Liquorama, which faced more competition and the problem of illicit imports.

The major issue is actually in expenses, up 21.8% and therefore way in excess of total revenue growth. This does include the loss on sale of the Zimbabwe segment and impairment losses though. To try and give a more maintainable view of earnings, Choppies reports adjusted EBIT growth of 12.2%. This still suggests some margin pressure.

Free cash flow was up by 5.8%, so arguably the most important metric of all is in the green.

Overall, this is a useful read-through for the Botswana economy, with Choppies generating 80% of its EBITDA from that market. They do refer to an “increasingly challenging economic environment” though, so be cautious.

KAL Group is selling Agriplas (JSE: KAL)

KAL wants to focus on retail offerings, not manufacturing

KAL Group announced the disposal of its shares and claims in Agriplas and the property on which its manufacturing facility is situated in Stikland. The buyer is Sana Partners Fund 2, an en commandite private equity partnership.

Agriplas operates in the irrigation industry, manufacturing and selling equipment to local and export customers. The primary customer base is of course the agricultural sector, but they have clients in other areas like mining as well. KAL sees this as a non-core manufacturing offering, hence the disposal so that the group can rather focus on its core retail offerings.

The business is being sold for R155 million, with the usual adjustments for net working capital once the deal is completed. The property is being sold for R67.5 million.

KAL seems to have gotten a decent price here, with interim profit after tax for the business of R7.8 million (you would double this for an estimated P/E of around 10x) and a net asset value on the balance sheet for the property of R15.5 million (subject to adjustments and clearly no reflection of its fair value). KAL is trading on a P/E of 7.2x, so that selling price looks good to me.

The sellers are restricted from directly or indirectly engaging in any activity that competes with Agriplas for a period of 2 years. There’s also a non-solicitation regarding customers. This is pretty standard stuff.

Canal+ takes control of MultiChoice (JSE: MCG)

Now we wait and see how big their stake will be

After a long and difficult road to get to this point, MultiChoice announced that all the conditions for the Canal+ deal have been met and that Canal+ now has a 46% direct stake in the company, with a further 2.2% having been tendered in the offer. You may recall that Canal+ would very much like to own all the shares in MultiChoice, not just some of them, so they are almost halfway there.

Importantly, with the restructuring in South Africa now complete, the shares held by Canal+ in MultiChoice are no longer subject to any scale-back of voting rights due to foreign ownership restrictions. Although Canal+ hasn’t quite gone through the 50% controlling threshold yet, their stake gives them effective control as there’s no world in which every single shareholder arrives at a meeting and then votes against Canal+. The announcement calls this “effective control” and it’s an accurate description. In any event, it’s likely that more shares will be sold by MultiChoice shareholders to Canal+ now that the deal is unconditional, taking them beyond the 50% threshold.

This is the largest deal that Canal+ has ever done and it gives the combined group a subscriber base of 40 million people across nearly 70 countries. That’s certainly a scale player! I also think this deal saved the local film industry, as MultiChoice appeared to be on a path of financial self-destruction.

If we are really lucky, DStv might actually wake up and stop trying to fleece everyone for access to the Springboks! An affordable sports-only package is long overdue.

The Canal+ management team will be in ultimate control, with David Mignot as group CEO and Nicolas Dandoy as group CFO. The ex-CEO of MultiChoice Calvo Mawela will chair the operations on the African continent, while ex-CFO Timothy Jacobs will have a “senior position in the finance department” of the combined group. A further important change to note is that MultiChoice’s year-end will shift from March to December to align with Canal+.

As a consumer and a fan of anything that creates jobs in South Africa, I’m excited for where this might lead.

PPC is indeed “awakening the giant” (JSE: PPC)

If only the broader macro conditions would play ball as well

For PPC to do really well, they need South Africa to become a construction site. Sadly, this absolutely isn’t the case out there, so the management team needs to navigate an extremely tricky environment of low growth and stiff competition from imports and other local manufacturers. They are doing a very good job of it!

With the emotively named “Awaken the Giant” turnaround strategy in place, the four months to July 2025 reflect an increase of 4% in group revenue and a jump of over 20% in group EBITDA! EBITDA margin is up from 13.7% to 15.9%.

In South Africa and Botswana, sales volumes were up 2%. Combined with other management initiatives, that’s enough for the EBITDA margin to increase from 10.3% to 17.7%. Although you may be tempted to extrapolate this operating leverage, management has guided that the margin for this segment should settle at around 17%. In other words, you should see this as a recovery period towards steady-state economics.

In Zimbabwe, volumes were up by a juicy 22%, not least of all thanks to the introduction of a 30% tariff on imported cement. Due to plant shutdowns, the EBITDA margin has behaved in the opposite way you what you would expect here, dropping from 29.0% to 15.3%. Management has indicated that margins have returned to the levels seen in the comparable period in the months after the shutdown. The Zimbabwe business has declared dividends of $20 million during the interim period (i.e. the four months covered by this update and the subsequent two months), of which $8 million is expected to be received by the group holding company in October. Notably, the sale of the Arlington property for $30 million is still on track.

Interim results are due for release on 24 November 2025. The group is clearly going to bring a positive story to the market.

Renergen brings the Springbok Solar Power Plant battle to a close (JSE: REN)

There’s also a trading statement reflecting wider losses

As Renergen is in the process of merging with ASP Isotopes (JSE: ISO), I’ll rather focus here on the issue that would’ve been material going forwards: the Springbok Solar Power Plant dispute. As you might recall, Renergen was fighting with a company that was building solar infrastructure in a way that Renergen was very angry about.

After some legal disputes and pointed commentary by Renergen, the parties have settled. Importantly, Springbok Solar has acknowledged the lack of consultation under Section 53 of the MPRDA and that they “regret the circumstances” around this. Better to ask for forgiveness than permission?

Either way, the parties have now reached an agreement that allows Renergen’s Virginia Gas Project and the Springbok Solar Project to coexist. The Department of Mineral and Petroleum Resources was involved in the process of a settlement being reached.

This is certainly helpful for Renergen in terms of removing an irritating and expensive legal overhang, but it feels like it was Springbok Solar who got quite lucky with this outcome. Either way, it’s finally over.

Separately, Renergen released a trading statement that reflects an increase in the headline loss per share for the six months to August 2025 of at least 20%. This isn’t really a surprise given the backdrop of transaction costs and increased depreciation now that the plant has been commissioned. These numbers aren’t particularly relevant to the story going forwards, as the market will instead focus on the numbers once the group is part of ASP Isotopes.

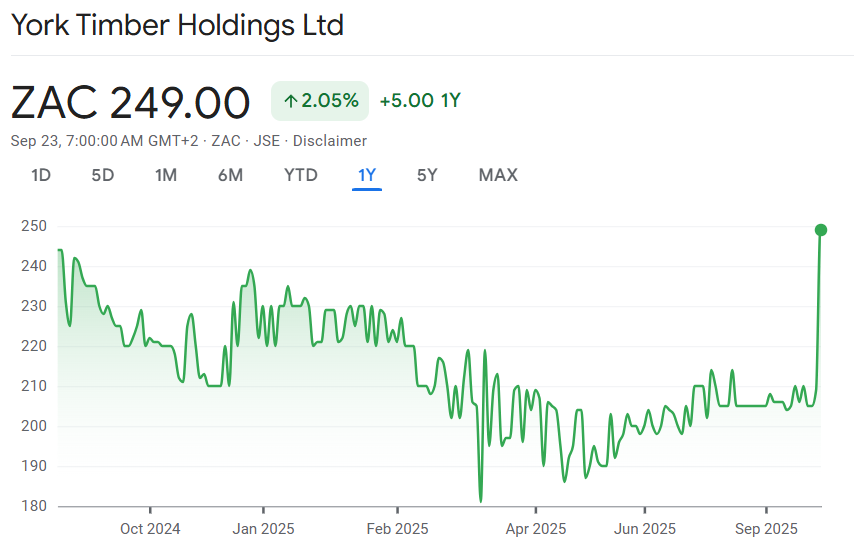

York Timber has had a much better period (JSE: YRK)

And the market liked it too, with the share price closing 19% higher

York Timber’s numbers are incredibly volatile thanks to the accounting requirement to value the biological assets each year and recognise the move in value in the profit or loss of the company. This adjustment isn’t reversed from HEPS, so even the market’s favourite indication of maintainable earnings isn’t much good here.

This is why York also reports core earnings per share excluding the biological assets adjustment, giving you an idea of how much money the business is making excluding the change in the value of the forests. The challenge is that you also can’t ignore the value of the trees entirely, so it’s a tough business to understand properly.

The market seemed to have no trouble in understanding enough about the latest announcement to get excited, taking the share price 19% higher on strong volumes (by York’s standards). This is because core earnings per share (excluding the biological asset movement) improved by between 94% and 99% from a loss per share of 10.74 cents – in other words, York was almost break-even on that metric!

But I think the real excitement was in cash from operations, which is expected to be between 418% and 423% higher than R28 million in the prior period. Even cash from operations is complicated though, as EBITDA in the prior period was R90.6 million (vs. cash from operations of R28 million) and you can thus see the gap between the two and the lack of reliable cash conversion.

In case you’re wondering, HEPS including the biological asset move is expected to jump from 13.74 cents to between 66.35 cents and 67.03 cents. To add to the complexity, the prior year number has been restated!

The share price chart does a good job of looking like the side profile of one of the plantations:

Nibbles:

- Director dealings:

- Des de Beer bought shares in Lighthouse Properties (JSE: LTE) worth R694k.

- Castleview (JSE: CVW) is busy building up some important stakes in other property funds. One such example is SA Corporate Real Estate (JSE: SAC), in which Castleview now holds a 21.133% stake.

- Shareholders of Primary Health Properties (JSE: PHP) who are planning to participate in the dividend reinvestment programme have until 5pm on 31 October to elect to do so.

- ArcelorMittal (JSE: ACL) has renewed its cautionary announcement without providing any further details on what is happening in the Longs business.

- Enthusiasts of the bond market will want to keep an eye on NEPI Rockcastle (JSE: NRP) and their planed issuance of €500 million in green bonds. They will use this to finance or refinance eligible “green” projects. The group has also launched a tender offer to repurchase bonds due in 2026 and 2027. For a group of this size and with such important debt, the liability side of the balance sheet is very actively managed.

- Capital Appreciation Limited (JSE: CTA) will change its name to Araxi Limited (JSE: AXX) with effect from 1 October.

Note: Ghost Bites is my journal of each day’s news on SENS. It reflects my own opinions and analysis and should only be one part of your research process. Nothing you read here is financial advice. E&OE. Disclaimer.