Get the latest recap of JSE news in the Ghost Wrap podcast, brought to you by Mazars:

British American Tobacco flags a weak first half (JSE: BTI)

Delivering the full-year guidance will depend on the US market

The British American Tobacco share price is trading at the same levels as ten years ago. Sure, there’s been volatility along the way, but the direction of travel is sideways, This is despite so much rand depreciation over that period. I have always struggled to understand the investment case here. Even the current dividend yield of nearly 10% isn’t a good enough total return to justify exposure, with the company constantly on a price-volume treadmill as global tobacco industry volumes are expected to fall 3% this year.

I couldn’t help but notice that the illicit vapour trade is now a problem. Illicit cigarette trading has been around forever. It seems that the crooks have also hired ESG consultants now, focusing on the New Categories instead. This is a particularly problematic situation in the US market, but there are proposed enforcement bills in 20 states. Such bills have only been enacted in 3 states thus far.

This is one of the reasons why revenue for the first half will be down low-single digits, along with adjusted profit from operations. This is on a constant currency basis. They are hoping for a much better second half, driven in part by management initiatives in the US market. Encouragingly, they expect operating cash flow conversion of over 90% again in 2024.

Further cash flow came in from the completion of the sale of 3.5% in ITC, unlocking substantial funds for share buybacks to try and drive earnings per share and inject some upward momentum into the share price.

By 2026, the goal is 3% to 5% revenue growth, along with mid-single digit adjusted profit from operations growth.

Copper 360 is off to a pretty awful start as a listed company (JSE: CPR)

There’s a very big miss of earnings forecasts here

Copper 360 announced that its headline loss per share for the year ended February 2024 will be between -10.5 cents and -12.0 cents. Compared to the previously published forecast HEPS of 2.9 cents for the same period, this is a very ugly miss.

They attribute this to inadequate crushing capacity, poor recoveries due to low acid solubility and delays in regulatory approval of funding for the acquisition of Nama Copper, which means that processing could only commence in March 2024 vs. the original plan to commence production in December 2023.

This is the same company that reported suspected market manipulation to the FSCA in April, believing that uncommercial trades led to a drop in the traded price. I haven’t seen the outcome of that complaint, but perhaps they should be focusing on their operations rather than obsessing over the share price.

Hopefully things will improve going forward. The market doesn’t appreciate a start like this.

Momentum Metropolitan’s growth has slowed in the latest quarter, but still looks good (JSE: MTM)

IFRS 17 does impact the comparability of these numbers, though

Momentum Metropolitan has released numbers for the nine months to March 2024. They reflect very strong growth in new business, but there’s a major change here. The present value of new business premiums (PVNBP) is now calculated using a risk-free discount rate rather than a discount rate that includes a risk premium. This is due to changes under IFRS 17. This has the impact of inflating the growth rate, showing 20% growth in new business. I didn’t see any disclosure of what the growth would be without that change.

This is a complicated group that ends up being a mixed bag when you look at the various operations, but management sounds pretty happy with the numbers. It does seem as though they have some struggles with costs at the moment, negatively impacting the value of new business.

Assets under management in Momentum Investments improved by 15% to R602.6 billion, but the acquisition of Crown Agents Investment Management added R57 billion of the total increase of nearly R79 billion.

One of the other highlights was an improvement in the claims ratio at Momentum Insure, improving the underwriting performance significantly.

Performance on a per-share basis will be boosted by significant share buybacks, which the group is managing to do at a substantial discount to the embedded value per share thanks to where the market is trading.

The group will share more information about the medium- and long-term strategy in July 2024.

The MultiChoice circular for the Canal+ offer has been released (JSE: MCG)

This deal has been going on for months now

The real action in the Canal+ activity around MultiChoice started in February, although the parties had already been in discussions for well over a year. Clearly, Canal+ sees MultiChoice as a juicy strategic opportunity, in line with the broader consolidation plays we are seeing in the media industry in response to the strength of global giants like Netflix.

After some initial tough negotiations around a price of R105 per share, the parties eventually agreed to cooperate at a price of R125 per share. Although structured as a mandatory offer, this is a price well above the R105 mandatory offer that the MultiChoice board would’ve advised shareholders not to accept. In other words, they’ve effectively accelerated the process by being willing to pay up. As I said, Canal+ sees this as a great opportunity.

Canal+ is headquartered in France and has 26.4 million subscribers, including 17 million outside France. The Africa subscriber base has nearly doubled in five years, with Canal+ having operated on the continent for over 30 years, starting in Senegal in 1991. They are now present in more than 25 African countries. The group has bigger global ambitions, having acquired a minority stake in a group called Viu that offers streaming in Southeast Asia and the Middle East. They are also the largest shareholder in Scandinavian operator Viaplay.

This is a massive opportunity for the South African film and media industry, where MultiChoice is already entrenched. Stories can be created here and taken to a global audience, not unlike Netflix has done with some of its regional hits. Purely wearing my South African hat here, I would love for this deal to go through.

Considering that MultiChoice was trading at R75 before the initial non-binding discussions in February, the price of R125 is a major premium. I struggle to see a reason why shareholders should not accept this, unless some are trying to be too cute and hoping for a bigger take-out premium down the line if Canal+ lists on the JSE as part of parent company Vivendi potentially splitting its group into several listed entities. Even if that happens, there’s no guarantee of a meaningful premium coming through at that stage. R125 is a good offer, as confirmed by the independent expert declaring it to be fair and reasonable, with valuation work suggesting a range of R113 to R129 per share, with a likely value of R120 per share.

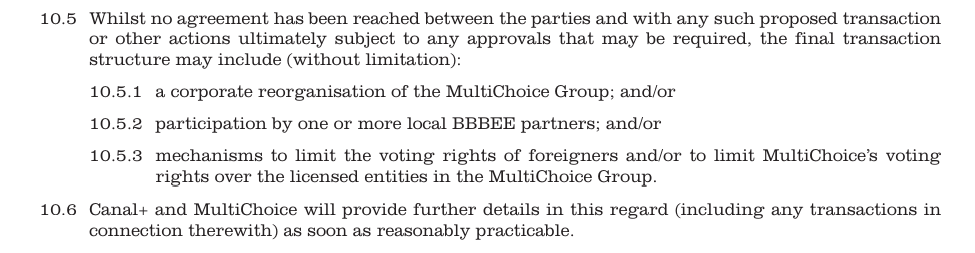

Before we get too carried away here, there are various regulatory approvals required to make this happen. The decision doesn’t lie solely with shareholders. The good news is that the Phuthuma Nathi B-BBEE structure sits at South African subsidiary level, so it is unaffected by this offer. This is yet another excellent reason to structure B-BBEE deals in subsidiaries rather than listed holding companies.

The limitations on control of foreign broadcasting services are less simple. They haven’t quite figured out how this will work yet. Here are the options put forward in the circular:

Those who don’t accept the offer will remain MultiChoice shareholders, but be aware that a 90% acceptance could lead to a squeeze-out scenario that will force remaining shareholders to accept the offer.

The offer is in cash and the bank guarantee of R34.4 billion has been provided by JPMorgan Chase Bank in South Africa. Canal+ already holds 45.2% in MultiChoice, so this amount covers the acquisition of the rest.

In an unusual element of this offer, no irrevocable undertakings have been sought from MultiChoice shareholders.

Perhaps I’m just blind, but I didn’t see a table of costs in the circular. With major international banks on the deal, the fees must be eye-watering. Standard Bank was paid R5 million purely to act as independent expert, which we only know because they disclosed this in their report.

Pan African Resources has agreed a five-year wage deal with NUM (JSE: PAN)

This deal is for employees at Barberton Mines

Pan African Resources has injected some certainty into its expense forecasts through a five-year wage agreement with the National Union of Mineworkers, the representative union for certain categories of employees at Barberton Mines. The deal lasts until 2029 and works out to an average annual increase of 5.3% per annum.

The current deal with UASA (the other union at Barberton Mines) runs until June 2026, providing for increases of between 5% and 6% depending on CPI. If CPI moves lower than 4% or higher than 7.5%, the parties have a once-off opportunity to renegotiate the increase.

The employee share ownership scheme at Barberton Mines was due to mature at the end of June 2024, but early settlement was agreed in March 2024. Over 2,200 employees received final maturity payments, with over R40 million in dividends having been paid to employees during the lifetime of the scheme.

The chickens are flying the coop at RCL Foods (JSE: RCL)

The proposed separate listing of Rainbow Chicken has been announced

This has been a long time coming. RCL Foods has been positioning itself for years to let Rainbow Chicken spread its wings, leaving behind a food business that allows shareholders to choose a risky option (the chicken group) or a safer option (the rest).

Unlike some of the recent activity we’ve seen in which a broken group tries to sell off a good company and list the remaining shares (Transaction Capital – WeBuyCars and the upcoming PicknPay – Boxer deal), this is just a standard unbundling of Rainbow Chicken. The shares will be declared as a dividend in specie to shareholders and will be separately listed. There’s no approval required by shareholders as their exposure to Rainbow Chicken doesn’t change. They simply hold it directly.

Look out for an abridged pre-listing statement on 10 June that will give all the required information about the business ahead of the unbundling on 1 July.

Little Bites:

- Director dealings:

- An associate of a director of Collins Property Group (JSE: CPP) bought shares in the company worth R379k.

- This is a useful signal, so I’m putting it right at the top of this section: a director of a major subsidiary of Stefanutti Stocks (JSE: SSK) bought shares in the company worth R153.7k.

- The CEO of Sirius Real Estate (JSE: SRE) bought shares in the company worth £9.9k in a self-invested pension. A person closely associated to him also bought shares worth £5k. But then, in a trade going the other way, a senior executive of the company sold shares worth £216k.

- The company secretary of Tiger Brands (JSE: TBS) received R234k worth of shares in the company under the share incentive scheme and sold the whole lot.

- The spouse of a director of Astral Foods (JSE: ARL) bought shares in the company worth R73k.

- Inexplicably, a director of a major subsidiary of PBT Group (JSE: PBG) bought 61 shares in the company at a total amount of R450, without getting clearance from the company. Perhaps he was checking if the button works. Or something.

- Although Sibanye-Stillwater (JSE: SSW) didn’t release a SENS announcement, there were widespread media reports of an illegal sit-in underground at the Kroondal mine as part of protest action around annual payments under the employee share option scheme. They are not entitled to any such payments, according to the company.

- Chris Seabrooke is retiring as an independent non-executive director of Transaction Capital (JSE: TCP). He will still be involved in the Mobalyz debt restructure until December 2024.

- Putprop (JSE: PPR) will move forward with its odd-lot offer at a price of R3.2718040 per share. As there are only 100 shares being repurchased from each shareholder, there’s really no arbitrage opportunity here despite the current market price being R3.20.