In this edition of Ghost Bites:

- What is VCP planning at Bytes Technology?

- Hyprop is tapping the market for R500 million in fresh equity capital

What is VCP planning at Bytes Technology? (JSE: BYI)

This 5% stake is very interesting

Here’s an interesting one: Value Capital Partners (VCP) has taken a stake in Bytes Technology of just over 5%.

The way it works in the market is that each increment of 5% must be publicly announced. We won’t hear anything further unless VCP either drops below a 5% stake, or moves above a 10% stake.

VCP is generally not a passive investor, so it’s going to be interesting to see whether this is part of a broader plan to become more involved at Bytes.

The Bytes share price has been struggling. In 2024, the market had to get to grips with a scandal around undisclosed trades by the ex-CEO. Then, in mid-2025, there was a nasty profit warning that took the shine off a stock that used to enjoy a premium valuation.

Since then, it’s been a story of AI disruption concerns and a squeeze on margins related to Microsoft products, with little in the way of bullish sentiment to offset these issues:

Ghost Bite: Generally speaking, an institutional investor moving through a 5% threshold can be safely ignored. An exception is when that investor is known for playing a more activist role, or “constructivist” as the term sometimes goes. I look forward to seeing what happens here.

Hyprop is tapping the market for R500 million in fresh equity capital (JSE: HYP)

If market history is anything to go by, the REIT will increase the raise based on demand

When REITs announce an accelerated bookbuild, the end result is what it says on the tin: a book of investors is built very quickly.

By the time you read this, Hyprop will already know where the R500 million in capital will be coming from. There’s also a good chance of them upsizing the raise if demand is strong enough in the market.

There are very deep capital pools on the JSE thanks to the presence of institutional investors. These investors have a particular affinity for property funds, as they are strong dividend payers for the income-focused investors (the ultimate beneficiaries of these funds). Inflation protection is also very important, with many REITs doing a great job of delivering returns in excess of prevailing inflation levels.

Such is the demand in the market for REITs that these companies can often raise capital without even being specific around what the money will be used for. Hyprop has thankfully given us more information than that. They’ve provided a list of local and European projects that require capital.

On the local front, they’ve highlighted solar and battery energy storage system (BESS) projects at Canal Walk and Somerset Mall. There’s also an extension at Somerset Mall that needs money.

In Europe, Hyprop has flagged an extension at a property in Croatia. They are also looking more generically at “new acquisition and expansion opportunities” in Eastern Europe, other than the previously announced acquisition of Galleria Burgas in Bulgaria.

If there’s one thing that listed companies love, it’s a bit of flexibility around what to do with their money. I’m not surprised at all to see a generic comment like the one provided by Hyprop regarding Europe. In fact, I’m impressed that they’ve at least limited the acquisition targets to Europe, instead of just noting general acquisition opportunities across the markets of operation (i.e. including South Africa).

The guided growth in distributable income per share of between 10% and 12% for the year ended June 2026 is unaffected by this raise. That would make sense, as the raise is happening after that period! More importantly, it’s just Hyprop’s way of saying that they hit their growth target for the financial year. This comment is designed to encourage institutional investors to feel good about the management track record.

We will have to wait and see what the pricing on the raise looks like. They cannot issue shares at more than a 5% discount to the 30-day volume-weighted average price (VWAP).

Ghost Bite: Given the recent support of capital raises by REITs on the JSE, I doubt there will be much of a discount at all.

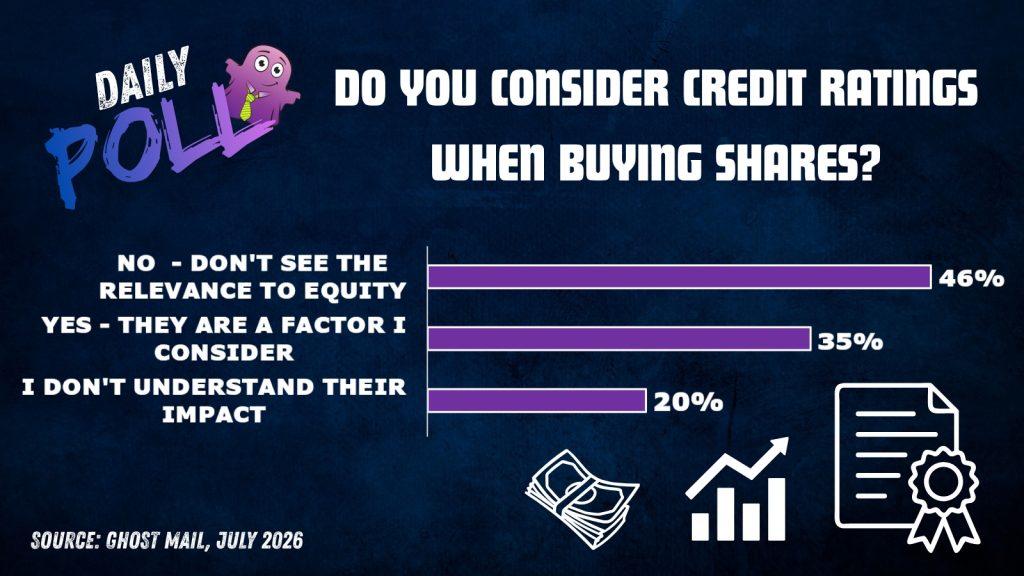

Results of previous poll:

Nibbles:

- Director dealings:

- A entity related to the founder of Capitec (JSE: CPI), Michiel le Roux, entered into a hedge over shares worth a whopping R6.6 billion at current prices. This is a funded put option transaction, which means that the shares have been pledged as collateral for a loan and then protected with put options to manage the downside risk. The strike price on the put option is R2,700 – way down from the current price of R4,795. The options have an expiry date of 1.16 years on average. It’s hard to imagine a market scenario in which this strike price becomes relevant, but a crisis can always happen.

- A non-executive director of Famous Brands (JSE: FBR), who also happens to be a member of the founding family, sold shares worth over R1.2 million.

- A director of Mr Price (JSE: MRP) bought shares worth R242k.

- Datatec (JSE: DTC) shareholders should be aware that the company has announced the ratio applicable to the scrip distribution. In case you aren’t familiar with how these work, they give shareholders the option to receive new shares in the company in lieu of a cash dividend.

- SAB Zenzeli Kabili (JSE: SZK) is in the process of getting approval for a special dividend of 57 cents per share from the SARB. It’s incredible how often the SARB approval for special dividends causes delays. The company now needs to revise the timing of the dividend,as the approval has not been obtained in time.