In this edition of Ghost Bites:

- DRDGOLD released a refreshingly conversational presentation on their capital projects

- Hudaco locked in the world’s strangest (or most efficient?) share repurchase

- Richemont’s blowout sales growth brings luxury back in vogue

- Supermarket Income REIT is raising £100 million (R2.2 billion) for acquisitions

DRDGOLD released a refreshingly conversational presentation on their capital projects (JSE: DRD)

They are in the peak of their capex cycle

DRDGOLD is busy executing its Vision 2028 strategy. This is an extensive capital programme designed to substantially increase throughput at the company’s underlying operations. Such is life in the mining sector – whether you operate underground or with surface tailings, you still need to spend money today if you want to make money down the line.

Full credit to the company for the language used in this presentation. They’ve done a good job of trying to simply complex concepts. For example, they explain that in 2023, they were “running out of room” at both Ergo and FWGR. The issue at Ergo related to tailings capacity and margin, whereas FWGR was lacking scale.

The net result of that issue? An infrastructure plan aimed at increasing throughput from 2.15 million tonnes per month (Mtpm) to 3Mtpm.

They began with an energy project at Ergo at a cost of R2.9 billion. The solar plant and battery energy storage system generates 47% of Ergo’s energy needs, helping the company avoid peak tariffs. Load shedding may be a thing of the past, but the economics generally still make sense in these projects thanks to Eskom’s tariff increases.

With that out of the way, DRDGOLD could move forward with five key projects and a total capex plan of R10 billion. This includes a number of projects across Ergo and FWGR.

The presentation goes into extensive detail on each of these projects, but even the efforts to explain the projects “simply” aren’t enough to offset how technical they are. I’m certainly not an engineer, so I won’t comment further on them.

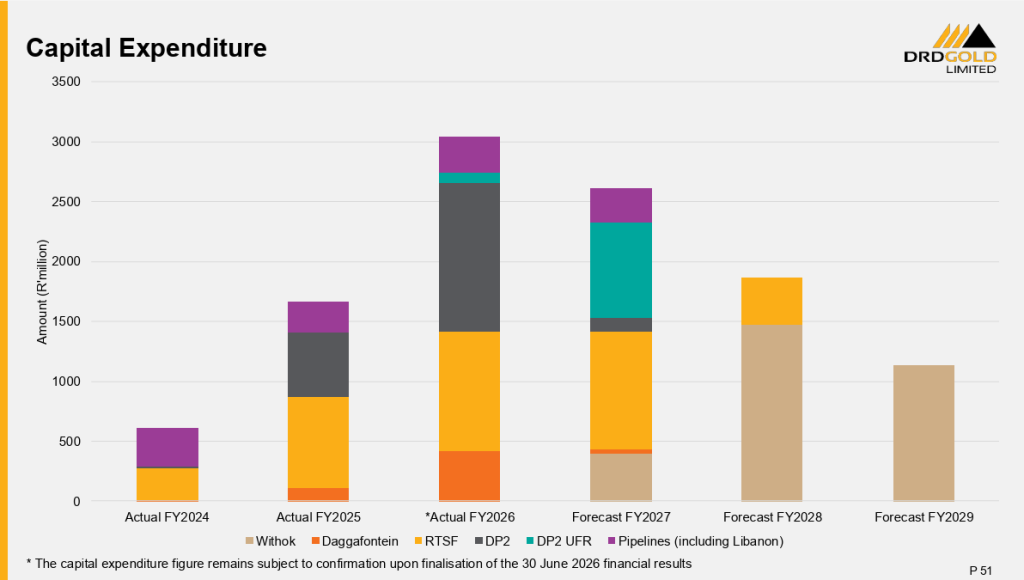

Luckily, there’s a language that I can speak: chart. Here’s one showing the capex profile from FY24 to FY29:

Ghost Bite: As you can see, we are in the peak of this capex cycle. The timing of this presentation is no accident, as the company obviously wants to remind the market why they are spending all this money.

Hudaco locked in the world’s strangest (or most efficient?) share repurchase (JSE: HDC)

Talk about a market anomaly…

Hudaco announced a very odd share repurchase. On the 14th of July, the company repurchased nearly 1.5 million shares for a total price of R283 million. This is a casual 4.855% of the total shares in issue, repurchased on a single day.

For context, the average traded volume in Hudaco shares is 26,351 shares per day (according to Moneyweb data). In other words, this repurchase represents nearly 57x the average daily volume traded. Odd.

Now, block trades like these can be arranged between parties and can still be done through the JSE order book. But here’s the weirdest part: Hudaco says that there was no prior understanding or arrangement between the company and the counterparties.

For this to be correct, holders of nearly 5% of shares in issue casually offered these shares at R189 per share and watched Hudaco buy them.

Is it possible? Technically, yes. Is it weird? Yeah, it is.

Ghost Bite: The share repurchase is within the authority given at the last general meeting, so perhaps someone wanted to get out of their position and figured that Hudaco would be on the bid. Still, it’s a wild amount of shares to go through on a single day. The repurchase authority (5% of shares in issue at the time of the authority) has almost been fully utilised.

Richemont’s blowout sales growth brings luxury back in vogue (JSE: CFR)

You won’t often see 20% growth from a company of this size

Richemont released results for the quarter ended June 2026 that set many tongues wagging. I don’t think anyone was expecting a rather spectacular 20% increase in constant currency sales! Reported sales (i.e. net of currency movement) are almost as good, up by 17%.

Jewellery Maisons did the heavy lifting, up 24% at constant rates. Specialist Watchmakers put in a decent, if not spectacular performance. That segment grew sales by 8%. The “Other” bucket, where Richemont chucks all the other stuff, grew by 9%.

Onwards to the geographical split, which is very important at Richemont and for the luxury sector at large.

We find the Americas with an outrageous 27% increase in constant currency sales and a contribution of €1.67 billion in sales. This puts it even further ahead of Europe (€1.43 billion), where sales were up by only 11%. I must point out that 11% is still a solid outcome!

But the star of the show, if you consider size and growth rate together, was Asia Pacific. The region increased by 21% on a constant currency basis, coming in at just over €2 billion in sales. Sales in China rose by double digits, putting the shine back on the luxury story.

In the smaller segments, we have Japan with an exceptional 36% increase in constant currency. The yen has been a wild story, so this is only 20% in reported currency. Japan contributed €0.6 billion in sales, so this growth rate must be read in the context of the smaller base.

Middle East & Africa wasn’t great, as you might expect, with the conflict in Iran playing out in this quarter. Still, sales growth of 3% in constant currency is impressive against that backdrop. The region contributed over €0.5 billion in sales.

Richemont notes that some of the spend that would’ve been in the Middle East transitioned into Europe. Therein lies one great truth about the wealthy: they tend to be just as mobile as their capital!

If we look by distribution channel, then we see a promising picture for margins. The retail channel grew sales by 24% in constant currency, while wholesale and royalty income was up 9%.

Online retail remains an anomaly in this space, up 18% despite being tiny in comparison to the rest of the retail operation. I still don’t see much of a market for people spending a fortune on jewellery and timepieces online vs. in boutiques.

Ghost Bite: Clearly, the wealthiest people in the world are doing just fine, thanks. Importantly, they also seem willing to spend money in China. That’s a big deal for the luxury market, with Richemont closing 6.6% higher on the day.

Supermarket Income REIT is raising £100 million (R2.2 billion) for acquisitions (JSE: SRI)

They will be raising from a mix of institutional and retail investors – but not from South African retail investors, sadly

Supermarket Income REIT kept SENS nice and busy on Wednesday. They announced the acquisition of three supermarkets, as well as the terms of a capital raise to support that acquisition.

We begin with the acquisitions. Supermarket Income REIT will acquire a portfolio of three supermarkets for a total of £118 million. The average net initial yield is 6.9%.

These are triple-net leases, which means that the costs associated with maintenance etc. are borne by the tenant. This de-risks the property for the landlord, allowing them to focus on the optimal funding structure without variability in the underlying cash flows. The exception is if the tenant goes bankrupt, but tenants like Sainsbury’s and Tesco should be just fine.

The leases have inflation-linked rent reviews with caps and floors. Each lease is different of course. The floors range from 0% to 3%. The caps range from 4% to 5%.

Now, how will they pay for these properties that are expected to transfer in September this year?

First, I need to point out that the pipeline of acquisitions is actually much bigger than just these three properties.

Supermarket Income REIT has its eye on nine grocery assets for a total of £216 million. In addition to the aforementioned three assets, they are looking at five UK supermarkets and one distribution asset (i.e. a warehouse). In all cases, the tenants are investment grade grocery tenants, so the fund is doing exactly what is says on the tin.

To give further context to the extent of the portfolio, the company directly and indirectly has 131 supermarket assets across the UK and France. This includes the joint venture exposure, like the 50:50 venture with Blue Owl Capital. Buying nine properties is meaningful, but not ridiculous when seen as part of the bigger picture.

Like all good property funds, Supermarket Income REIT uses debt to try and juice up equity returns. They recently issued £250 million in unsecured bonds at a fixed rate of 5.125%. They recently refinanced £445 million in debt across six lenders. Even with these new transactions, the group loan-to-value ratio won’t exceed 45%.

Along with the use of debt, a raise of £100 million in equity will be enough to help the company pursue this pipeline. They are reserving the right to increase the size of the raise if demand is strong enough.

The raise will take the form of an accelerated bookbuild in both the UK and South Africa. There’s a retail offer as well, but only in the UK. South African retail investors aren’t being given a bite at this cherry, unfortunately.

Importantly, the issue isn’t underwritten by any major investors. In terms of insider activity, certain directors (including the CEO and CFO) will participate to the tune of around £0.18 million.

Ghost Bite: At least South African institutions are being given an opportunity to consider this raise. This is exactly why a fund like Supermarket Income REIT is listed on the JSE.

Results of previous poll:

Nibbles:

- Director dealings:

- Afine Investments (JSE: AFI) announced that a few directors and related parties elected the dividend reinvestment option instead of receiving cash. The total value of the reinvestment across these parties was around R625k. It’s certainly not as strong a signal as an open-market purchase, but it’s still positive.

- Newpark REIT (JSE: NRL) has renewed the cautionary announcement related to a proposal that would allow shareholders to monetise some or all of their shares in the company. At this stage, there’s no guarantee that any such proposal will be finalised or implemented, hence the need for caution.

- Eastern Platinum (JSE: EPS) has announced the appointment of David Li as the CFO. He has extensive experience in the mining sector, gained across multiple regions over the past two decades.

- Numeral (JSE: XII) released a change statement that details multiple adjustments to the financials for the year ended February 2025. This is never a good look, although it was a complex year that included a recovered interest of 50% in Cryo-Save. There’s almost no trade in the stock anyway, so few people will really care about FY25. If anything, the focus will be on the financials for the year ended February 2026. The biotechnology and healthcare services segment saw revenue more than double to nearly $1.8 million. Operating profit more than tripled to $426k. Oddly, the group also has a financial services segment, where revenue more than tripled and profit increased tenfold to $141k. If this company wants the market to give it any attention, they will need to put much more effort into telling the story to investors.

Hi, and thanks. I really like your decluttered new format. As a retired engineer Ghost Bites gives me financial insights way beyond my capabilities, and I’m learning. Unlock the stock and podcasts are the cherry on top. Thanks again -Great Stuff!

Love to hear it, thanks so much Mike!

Thoroughly enjoy Ghost Bites