Purple Group’s flywheel is really spinning now (JSE: PPE)

Welcome to the J-curve: we’ve been expecting you

Hot on the heels of a really strong trading statement, Purple Group has released results for the six months to February 2026. I’m a happy shareholder, with the group continuing to grow beautifully.

They’ve reached that juicy part of the J-curve where most of the incremental revenue is dropping straight to the bottom line. Revenue was up 8.8%, yet operating expenses only increased by 0.5%. This obviously did great things for profitability, with profit before tax up 33.3% and HEPS up 21.0%.

This benefit of operating leverage (fixed costs relative to variable costs) is even more visible once you drill down to Easy Group, the part of the business that everyone knows so well. Revenue was up 18.5% and expenses only increased 1.6%, so profit before tax jumped by 66.3%. That’s excellent!

The underlying drivers of these numbers include a 21.9% increase in active clients and a 41.2% increase in client assets. It was also a busy period in the markets, with activity-based revenue increasing by 23.4%. Notably, non-activity-based revenue grew 14.4%, and now contributes 52.6% of total Easy Group revenue.

Here’s another good stat for you: at the halfway mark in this financial year, retail inflows are already at 72% of FY25 levels. I’m hoping to see this continue in the second half of the year, even with the energy shock that is going to hurt consumers.

An exciting growth engine in the group is the retirement business. Assets have tripled over three years, with EasyRetire Retail offering incentives for clients to bring their retirement assets across to EasyEquities.

EasyTrader was definitely the ugly duckling in this period. A net hedging loss of R21.3 million was a nasty surprise, with the correlation assumptions in the underlying model breaking down. For context, revenue in that business is just R5.7 million. This is an interesting business that includes a planned entry into prediction markets in the second half of the year, but it does have a different risk profile to the “simpler” model of EasyEquities.

In case you’re wondering, EasyTrader has 6,842 funded clients. Few people realise just how small the premium South African market actually is!

The group is also chasing the opportunity in asset management. With nearly 1.25 million active clients in the ecosystem, they have incredible distribution strength. To what extent will we see disruption of the unit trust industry? Time will tell. But you should never, ever underestimate the power of distribution.

EasyEquities Philippines is also live, at long last. They are aiming to have 500,000 active users by the end of 2027. As a shareholder, I hope they get it right, as demonstrating the ability to scale internationally would do wonders for the valuation.

Here’s another interesting development: the launch of the ZARU rand-backed stablecoin. With various big names involved here (Luno / Sanlam Specialised Asset Management / Lesaka), they are looking to take advantage of many of the structural weaknesses in cross-border payments. Fees, banking hours – these elements are ripe for disruption.

It’s certainly an impressive set of numbers for a company that has doubled its market cap in the past year. With the market cap at nearly R2.9 billion, I believe that there’s still plenty of runway here.

What is your view here? Just how far can they go?

RMH is a lesson in liquidity – and why marketability discounts exist (JSE: RMH)

The circular for the AttBid offer has been released

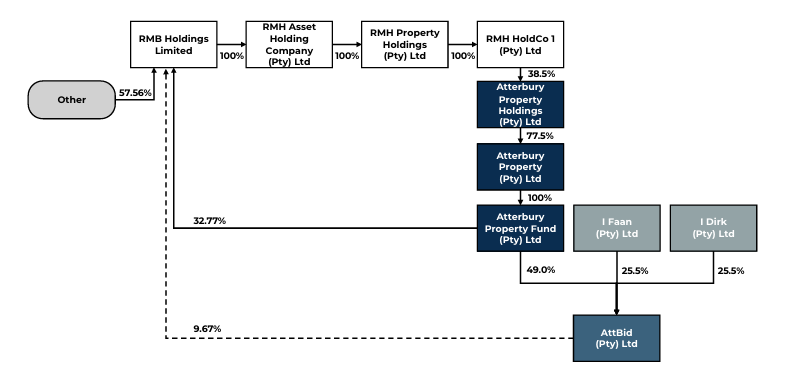

As you probably know by now, AttBid and Atterbury Property Fund are concert parties in the offer being made to shareholders in RMB Holdings (known as RMH).

The underlying relationships are complex, to say the least.

RMH has an investment in Atterbury Property Holdings, with this position representing 92% of RMH’s property portfolio. Atterbury Property Holdings is the indirect controlling shareholder in Atterbury Property Fund, wwhich in turn holds 32.77% in RMH.

You can see the circular reference going on here.

And just for some added spice, the founders of WeBuyCars (JSE: WBC) are sitting alongside Atterbury Property Fund in AttBid in their personal capacities.

It’s helpful to include the ownership diagram straight from the transaction circular:

This deal really boils down to one thing: RMH wants to unlock its capital and pay cash to shareholders, but the stake in Atterbury Property Holdings is incredibly hard to sell for structural reasons.

A minority stake in a company that doesn’t pay dividends is typically avoided by investors. If you can’t control the cash flows and you aren’t receiving any cash flows, then what justifies the value?

With no other buyers in town (and they certainly tried hard to find one), RMH shareholders face a tough choice here. It’s never good to have such little negotiating power in a corporate transaction.

This particular offer to shareholders in RMH is structured as a mandatory offer, as the concert parties bought up more than 35% of shares in the market. The price is R0.47 per share and there’s no minimum level of acceptance. Shareholders who want to monetise at this price can do so. Shareholders who want to stay invested can also do so.

The exception would be if 90% of holders accept the offer, in which case the offerors can invoke the squeeze-out provisions (s124 of the Companies Act) and force the remaining shareholders to sell.

But that’s not all, folks.

The entire RMH board intends to resign once the offer closes. No matter what happens, things will look very different going forwards.

It doesn’t look like RMH would immediately be delisted, but there’s an underlying intention by the Atterbury parties to work towards a delisting.

Investec, acting as the independent expert, has opined that the terms of the offer are fair and reasonable to RMH shareholders. I don’t think reasonability was ever in doubt, as RMH has already shopped this stake around town and came out empty handed. As for fairness, Investec’s estimated range is R0.47 to R0.53 per share.

The offer price of R0.47 is thus right at the bottom of the suggested fair value range.

In my opinion, the lesson to take from this entire saga is that non-controlling stakes in unlisted companies are dangerous things. This is exactly why investors place a marketability discount on these investment holding company structures.

It’s great to have a particular value on paper, but you need someone to actually pay you that number. When buyers are thin on the ground, the bid-offer spread widens (due to lack of liquidity) and things like this can happen.

Nibbles:

- Just one nibble today – and it’s the results of the general meeting of Jubilee Metals (JSE: JBL) shareholders. They voted in favour of the resolution to reduce the share premium account, paving the way for dividends later down the line. The resolutions related to share issuances and pre-emption rights were withdrawn before the meeting.