Altron has tightened up its earnings guidance (JSE: AEL)

And the numbers look good!

Altron has released an updated trading statement for the year ended February 2026.

In their initial trading statement released in February, they had guided an increase in HEPS from continuing operations of at least 30%, and a jump in HEPS from group operations of at least 50%.

We now know that the increase in HEPS from continuing operations will be between 31% and 37%. From group operations, HEPS will increase by between 68% and 74%.

This has been one of the most impressive turnaround stories on the JSE. Through various important corporate actions and an overall improvement in performance, they’ve achieved share price growth of 160% over the past three years!

Datatec is doing extremely well (JSE: DTC)

Understanding the momentum through the year will be important

Datatec has released a trading statement for the year ended February 2026. The numbers look spectacular, with HEPS expected to jump by between 51% and 58.8% (in US cents – the company’s reporting currency).

If you use underlying earnings per share, which excludes share-based payments, the increase is between 31.7% and 37.3%. This is to help make the results more comparable to peers. Either way, these are excellent numbers.

The results were driven by Westcon International and Logicalis International, with Logicalis Latin America experiencing only a slight increase in gross profit.

Something to note is that the interim period was actually even better. In the six months to August 2025, underlying earnings per share had increased by 43% and HEPS had jumped by 109.5%.

When detailed results are released on 26 May, the market will want to look at the momentum in earnings and figure out the reasons for the significant difference in H1 vs. H2 performance.

Gold Fields gives us great data points on inflation (JSE: GFI)

For now at least, the gold price is more than making up for it

With the first quarter of the financial year behind them, Gold Fields remains on track for full-year guidance.

They just achieved an increase in attributable gold-equivalent production of 15% year-on-year, so they are looking to take full advantage of favourable gold prices. The Salares Norte mine’s first full year of production is an important driver of this increase.

Quarter-on-quarter production figures fell by 7%, so that’s something to keep an eye on. There was also a jump in all-in sustaining costs (AISC) of 13% year-on-year and 9% quarter-on-quarter, with inflation as one of the drivers of higher costs.

They give excellent disclosure on some of the underlying inflationary pressures. It goes beyond just diesel, with other inputs like cyanide and LNG also increasing substantially.

If the oil price sticks at around $100/barrel, then Gold Fields forecasts an impact on costs of $40/oz to $50/oz on a portfolio level.

For now, the gold price is protecting them from this issue. Despite the dip in quarter-on-quarter production, revenue increased by 16% in this quarter vs. the three months to December.

The balance sheet is even healthier as a result. Net debt has decreased by 34% over the past 12 months. Net debt to EBITDA is just 0.19x now vs. 0.26x at the end of December 2025. It’s not hard to see why the company feels confident to do share buybacks.

As you would imagine at a group of this size and importance, there are many underlying projects underway. They have no fewer than 21 active projects in the greenfields portfolio, including 13 in drilling!

Sustaining capex for the year is forecast to be between $1.3 billion and $1.4 billion. They will also spend between $600 million and $700 million on growth capex.

Lesaka Technologies has raised FY26 guidance (JSE: LSK)

This is the kind of thing that investors want to see

Lesaka suffers from thin liquidity in its stock, which is why the share price closed flat on a day that probably should’ve seen some fireworks.

They released an update for the third quarter that reflected performance at the upper end of profitability guidance. They even raised guidance for FY26! But for whatever reason, the market wasn’t particularly interested.

If we dig a bit deeper, we find that net revenue increased by 16% year-on-year in rand terms. Adjusted EBITDA increased by 45%, so the shape of the income statement in response to that revenue growth is encouraging.

Operating income increased by a casual 804% – and yes, that means it was 9x higher year-on-year. Perhaps most importantly, they’ve swung from a net loss to net income.

The disappointment in the numbers is the Merchant segment, where net revenue dipped by 4%. This is exactly what the market doesn’t want to see, especially from the largest segment. Consumer revenue jumped 41% and Enterprise was up 78%.

Worries around the Merchant business aside, Lesaka’s other growth engines are firing on all cylinders. This has led to the increase in guidance, with adjusted earnings per share for the year ending June 2026 expected to be between R5.50 and R6.00.

This guidance still excludes the Bank Zero acquisition, which remains subject to regulatory approvals.

Life Healthcare’s share price landed up in the hospital (JSE: LHC)

The market hated the latest update

Life Healthcare dropped by a 11% on Thursday, after releasing a trading update that was heavily impacted by a medical scheme being placed into curatorship. Other online reports suggest that Sizwe Hosmed is the scheme in question.

Either way, paid patient days were down by 0.4% thanks to the loss in volumes from this issue. If you exclude the curatorship, then paid patient days would’ve been up by 0.9%. The market doesn’t seem to have been very interested in that argument though.

With revenue up by between 2.2% and 2.6% for the six months to March 2026, it’s surprising (and impressive) that the company managed to achieved normalised EBITDA growth of between 4.9% and 5.3%.

The increase in HEPS is unfortunately a useless metric, as the prior period was heavily distorted by the Piramal liability associated with the Life Molecular Imaging deal. Instead, it’s better to just look at the expected HEPS range from continuing operations of between 50.6 cents and 52.6 cents.

The company has wisely split out the LMI issues and given us a pro forma movement. This is the key metric to remember: HEPS on that basis has moved by between 0% and 4% for continuing operations.

The market was clearly looking for more.

Sappi goes from bad to worse (JSE: SAP)

The share price is plumbing new depths

I’ve been keeping an eye on Sappi to see if the share price would find some positive momentum and deliver excellent cyclical returns. My worry has been that this time, it really is different in the paper market.

First, let me show you what this chart looks like over the long term:

The idea here is to buy at the extreme lows, strap yourself in and wait for the cycle to turn.

But with the share price dropping another 13% on Thursday in response to the second quarter update, it’s clear that the market still hates this thing and is losing faith in its ability to weather the storm.

There are two major problems here.

The first is that the digital age is unfriendly towards paper, so a cyclical industry has perhaps transformed into an industry in structural decline.

The other problem is that Sappi’s balance sheet has taken more punishment than a northern hemisphere prop after 70 minutes against the Boks, so they are in no shape to actually deal with disasters like the spike in energy prices and a potential recession.

In the latest quarter, revenue dipped by 1% and adjusted EBITDA tanked by 51%. That is truly awful. They are now deep in the red, with a loss of $413 million vs. a loss of just $20 million a year ago.

Net debt is up 18% to just under $2 billion, with efforts to reduce capex proving to be insufficient to address the slide. I somehow doubt that lenders are sleeping very well at night right now, with the net asset value having decreased by 24% in the space of 12 months.

There are pockets of hope, like a 27% increase in North American paperboard volumes. But with selling prices under pressure and inflation assaulting their manufacturing margins, I think Sappi’s share price is going to plumb new depths.

This time, it seems to be different. But what do you think?

Southern Sun had a fantastic second half (JSE: SSU)

They are dealing with a difficult macroeconomic period from a position of strength

In the six months to September 2025, Southern Sun struggled with a 6% decline in operating profit and flat adjusted HEPS. But the second half of the year clearly told a very different story, as a trading statement for the year to March 2026 notes adjusted HEPS growth of a delightful 17% to 21%!

In case you’re wondering, HEPS on an unadjusted basis increased by 18% to 22%, so there’s not much of a difference there.

Strong occupancy levels were a major driver here, with overall occupancy of 62.9% vs. 60.8% in 2025. It’s certainly worth noting that the Paradise Sun in the offshore business had been closed for refurbishment in the first half of the year, so that’s clearly part of the H1 vs H2 skew.

The South African portfolio ran at 64.3% (vs. 61.9% in 2025), with demand driven by foreign inbound travel and demand in the MICE segment – Meetings, Incentives, Conferences and Exhibitions. The G20 in Gauteng was just one example in the second half of the year.

It’s more than slightly funny that a hotel group describes one of its key drivers as being MICE!

Mozambique still sounds like a difficult situation, with only marginal improvements in trading performance in the second half of the year. The company has also flagged the impact of the war in the Middle East, with oil prices making travel far more expensive.

They have a strong balance sheet to weather any storms, with net cash of R86 million. With the share price up 4.5% year-to-date, the market is shrugging off the risks and giving the management team the credit they deserve. The reality is that even the best management team in the world can’t do much about the cost of inbound travel skyrocketing, so I worry about the impact on the next financial period of the prolonged spike in oil prices.

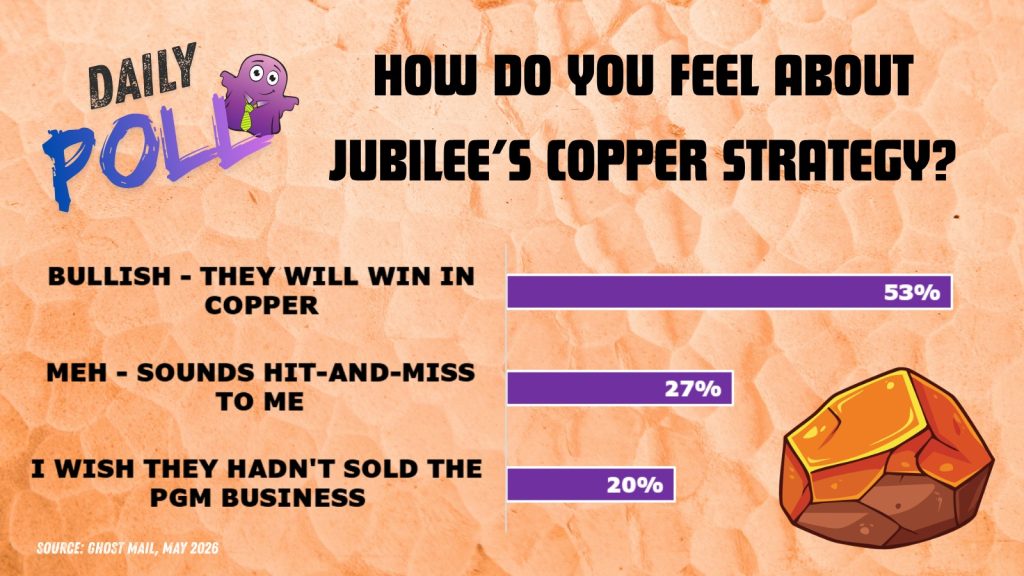

Results of previous poll:

Nibbles:

- Director dealings:

- In the latest game of musical shares at the Wiese dinner table, various entities related to Dr. Christo Wiese and Adv. Jacob Wiese have entered into swaps and associated transactions over Shoprite (JSE: SHP) shares worth R943 million.

- On such a busy day of news, MTN’s (JSE: MTN) update on the performance at MTN Uganda must land in the Nibbles. This is one of the smaller subsidiaries in the group, which is a pity as MTN Uganda has historically proven to be a dependable performer in Africa. But in the latest quarter, service revenue was up by only 7.7% and EBITDA margin actually declined by 180 basis points to 50.6%. Profit after tax dipped by 3.8%. Unlike in Nigeria and Ghana where MTN is growing rapidly in this environment, Uganda could only manage a “resilient” performance. This is why diversification is important.

- 4Sight Holdings (JSE: 4SI) – a small cap that behaves like a company that wants to be a large cap – announced some positive news around the X4 Group acquisition that they made in 2025. For the year ended February 2026, that business exceeded 110% of its agreed net profit after tax target of just over R6 million. These are small numbers in the greater scheme of things, but small successful deals add up very nicely over time. I’ve been very tempted to take a small position here.

- Tharisa (JSE: THA) is in the process of transitioning to underground mining. The latest update is that the company has concluded a five-year contract with Cementation Africa regarding the underground mining development and construction work at the Tharisa mine. They refer to the contract as being structured on a cost-plus-fee basis with “aligned principles” rather than a “traditional rates-based, risk transfer model” – interesting! And if the name Cementation Africa sounds familiar to you, it’s because this company was acquired out of the charred remains of Murray & Roberts by Differential Capital and a consortium of investors.

- Montauk Renewables (JSE: MKR) has released results for the quarter ended March 2026. They put literally zero effort into the SENS announcement, merely pointing investors in the direction of the SEC filing. They are still slightly loss-making despite a 9% increase in revenue.

- Sebata Holdings (JSE: SEB), which is currently suspended from trading, has issued a cautionary announcement – just in case there are people who are willing to do off-market trades! Jokes aside, cautionary announcements are still a requirement even if the shares are suspended from trading. The reason for the cautionary is that the company has entered into negotiations with a non-related third party regarding the potential disposal of assets. They haven’t indicated which assets, or given any other information at this time.