In this edition of Ghost Bites:

- Lesaka Technologies wants to sweeten the deal for the executive chairman

- Spear REIT has met all conditions for the acquisition of Watergate Centre

- Get the Nibbles (including director dealings)

- See the results of the previous poll

- Catch up on Remgro, South32, Hudaco, Optasia and Supermarket Income REIT in the Ghost Bites podcast

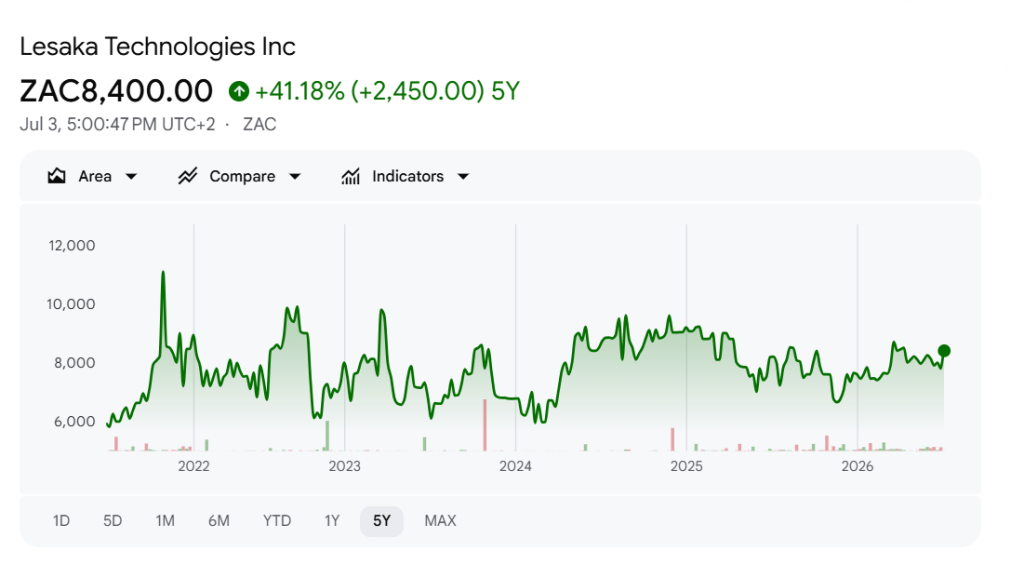

Lesaka Technologies wants to sweeten the deal for the executive chairman (JSE: LSK)

There are good arguments to be made for and against these share options

In May, the board of Lesaka Technologies approved the grant of share options to Ali Mazanderani, the Executive Chairman of the company. This gives him the right to buy 1,000,000 shares at $5.00 per share, provided he remains continuously employed by the company until at least April 2028. That might sound like a long time, but keep in mind that this is less than two years away!

Bulls may give this the nod based on a desire to create alignment between shareholders and top management. If the share price goes up, the options become more valuable, creating a win-win decision for Mazanderani and other shareholders. It’s also worth noting that the strike price of $5.00 is quite similar to the current price of R84 per share. In other words, this option only becomes valuable if the share price increases significantly.

Bears could argue that alignment is irrelevant if executives are simply topped up when the previous tranche of options becomes worthless (Mazanderani currently has options to buy 4,000,000 shares at between $6.00 and $14.00 per share – options that are clearly out of the money). The reason these options are in trouble is that the Lesaka Technologies share price hasn’t performed:

Another important element to debate is that the options only become exercisable a year after the vesting condition is met (i.e. in April 2029). The window for exercise lasts for 12 months i.e. the latest possible date is April 2030. This gives the options a life of nearly four years from date of issuance. When it comes to options, a longer period makes them more valuable (as there’s a higher likelihood of the market price meaningfully exceeding the strike price). Does it make sense for the options to be exercisable for so long after the minimum employment commitment ends?

Shareholders are now being asked to vote on this remuneration plan. The results should be interesting!

Ghost Bite: In November last year, I recorded a very useful Ghost Stories podcast with Ali Mazanderani. Listen to it here and be sure to use that discussion as part of your research process on the company.

Spear REIT has met all conditions for the acquisition of Watergate Centre (JSE: SEA)

Transfer is expected during August 2026

A few months ago in April, Spear REIT announced the acquisition of Watergate Centre in Mitchells Plain. The good news is that the Competition Commission gave the transaction the green light, so it has now become unconditional. Spear expects to take ownership of the property during August.

This R442 million transaction gives Spear shareholders exposure to a convenience-oriented shopping centre that is anchored by Shoprite and Brights Hardware.

Given the location, it won’t come as a surprise to you that this is a value-focused centre. In other words, the tenant mix is designed to appeal to lower-income shoppers, one of the most exciting growth segments in South Africa.

As evidence of how sought-after this type of space tends to be, the centre is fully let. The price implies a purchase yield of 8.37%, with a weighted average escalation of 6.70%. This escalation looks lucrative in the context of CPI inflation, but keep in mind that the actual inflation rate for retail centres tends to be considerably higher thanks to energy, security and municipal costs.

The most interesting element of the deal is that at the time of the initial announcement, the weighted average lease duration was only 1.86 years. This is because the property was developed roughly 9 years ago, so many of the leases are reaching their renewal phase. For Spear shareholders, it will be important for the property fund to achieve positive reversions on the leases.

Ghost Bite: This is a good indication of the diversification that can be achieved even by sticking to one region. The focus on the Western Cape doesn’t mean that all of Spear’s assets are shiny tourist destinations. Far from it, in fact!

Results of previous poll:

Nibbles:

- Director dealings:

- An alternate non-executive director of WeBuyCars (JSE: WBC) sold shares worth R21.4 million. This substantial sale is described as “being for the purpose of, inter alia, settling obligations relating to other instruments”. This could mean derivatives, funding deals or something else.

- The CEO of Africa Bitcoin Corporation (JSE: BAC) bought C preferred shares (linked to ACOF) worth R9k.

- For those keeping score, Novus Holdings (JSE: NVS) is now up to a 50.44% direct stake in Mustek (JSE: MST) and a 70.73% stake when combined with concert parties.

- Dipula Properties (JSE: DIB) renewed the cautionary announcement that was first issued on 22 May this year. We still don’t know what negotiations the company is actually busy with. They merely refer to “potential corporate activities”.

- Efora Energy (JSE: EEL) reminded shareholders that they are in the process of applying for a provisional liquidation of the company. This comes after the termination of a proposed transaction that they hoped might save the entity.