In this edition of Ghost Bites:

- Alphamin continues to ride the tin wave

- Brait, while promising a value unlock, is executing a rights offer to put more money into Virgin Active

- Tharisa’s production metrics and projects are on track

Alphamin continues to ride the tin wave (JSE: APH)

It’s just a pity that sales volumes were flat

Alphamin has announced its Q2 EBITDA guidance. The way the company reports is that they release extremely detailed “guidance” for the quarter that just ended. They subsequently release detailed financials as well, but by then the market has already been given the most important information.

For the quarter ended June 2026, Alphamin achieved record EBITDA of $167 million, up 6% vs. the previous quarter. This is despite an almost perfectly flat outcome in contained tin sold, so this uplift is thanks primarily to a 5% increase in the average tin price achieved.

The dip in processing recoveries that led to the disappointing outcome in tin volumes will need to be managed carefully, but these risks are a feature of mining.

The net cash position has decreased from $140 million to $91 million after paying significant distributions to shareholders. There were also large amounts for taxes in this quarter.

Other than the usual risks of operating in the DRC, the company is also monitoring an Ebola outbreak in the northeastern part of the country. Thankfully, this hasn’t impacted the area in which the mine operates. As disease outbreaks go, I don’t think it gets much scarier than Ebola.

Ghost Bite: Tin prices have been boosted by demand for the commodity in AI applications. I’ve seen it referred to as “the metal of computing power” – a nice way to remember it. Alphamin’s total return over 12 months is an incredible 61%. On a year-to-date basis, the total return is 19.4%.

Brait, while promising a value unlock, is executing a rights offer to put more money into Virgin Active (JSE: BAT)

And no, there are no prizes available for guessing who one of the underwriters is

Brait has been one of the more disappointing stories on the JSE over almost any time period. They’ve had some bad luck along the way, like the impact of COVID on Virgin Active, but there have also been a number of other issues.

With the company promising a value unlock to shareholders, they are now taking the most unusual step of raising R2.5 billion in a rights offer. Usually, a value unlock means that money flows from the company to its investors, not the other way around!

Part of the justification is that the company needs to redeem the convertible bonds for £138 million. Fair enough. But the other reason is that Brait is throwing another £108 million at a Virgin Active capital raise of £175 million. This may well be the right thing to do in this situation, but unfortunately the group’s investment track record isn’t anything that a personal trainer would be proud of.

In case you’re wondering about the balancing figures, Brait also has access to an existing revolving credit facility, so they are just swapping one type of finance for another. They also have the net proceeds from the sale of shares in Premier (JSE: PMR), Brait’s shining success story (no sarcasm there – it’s a great business).

As is usually the case when Christo Wiese is involved in a company, the rights issue is being underwritten by Titan Financial Services. To be fair, at least this offer has other underwriters as well in the form of various asset managers. Shareholders are also able to apply for excess offer shares, so there are some elements to this structure that make it fairer to minority shareholders than is sometimes the case.

Underwriting never happens for free. The underwriters will be paid 1% of the aggregate offer price, or a cool R25 million.

Ghost Bite: Brait’s share price has been a rather bleak story. I’m glad I haven’t been invested here. The closest I get to Brait is contributing to their income statement via regular smoothies at Kauai.

Tharisa’s production metrics and projects are on track (JSE: THA)

As you would expect during a period of heavy capex, net cash has decreased

PGM and chrome miner Tharisa has released a production report for the third quarter ended June 2026. They believe that they can deliver their FY26 guidance based on the year-to-date performance.

Importantly, the underground project is on time and in line with budget at this stage. This is a major transition for Tharisa that should further improve the investment case for the group.

On a quarter-on-quarter basis (i.e. Q3 vs. Q2), PGM production was up by 15.5%. This was driven by a significant improvement in recoveries and a better weather environment vs. the preceding quarter. Chrome production dipped by 2.5%.

Commodity prices haven’t played ball lately, with the PGM basket price down in the past quarter. Tharisa, like all mining houses, has to try and invest on a through-the-cycle basis. When prices are particularly high, they bank the excess cash and thank their lucky stars. When prices are under pressure, they have to vasbyt and stick to the plan.

The underground project, as well as Karo Platinum, will put pressure on the capex budget and thus the balance sheet. Debt has increased significantly from $129.6 million at the end of March 2026 to $188.1 million at the end of June 2026. The net cash position has dropped from $54.7 million to $10.7 million.

Importantly though, they are still in a net cash position!

Ghost Bite: Tharisa’s share price is down 8.6% year-to-date thanks to the PGM sector blowing off some steam. The total return over three years is 46%. Mining cycles tend to be longer than that, but that’s a decent indication of strategic delivery to shareholders.

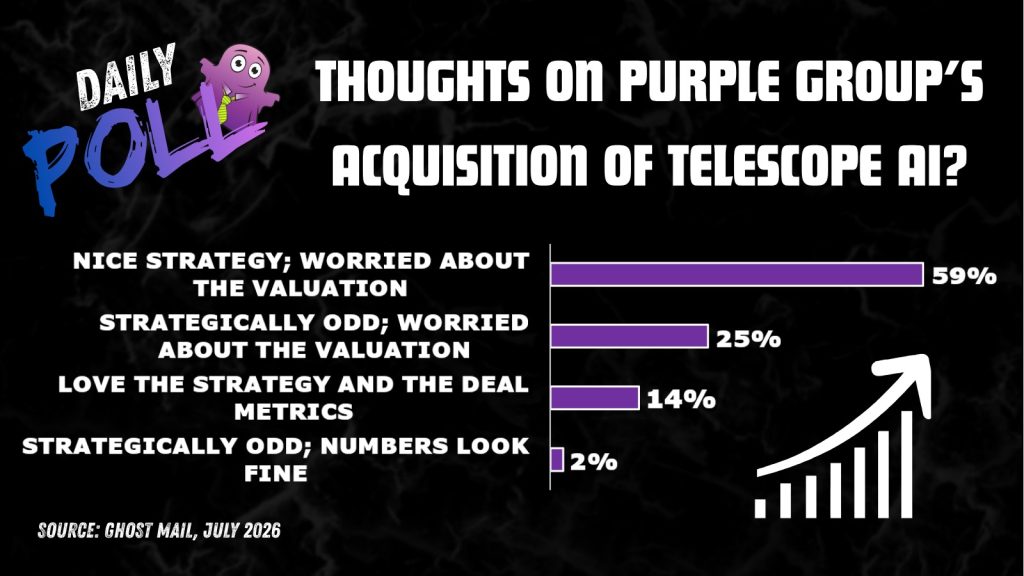

Results of previous poll:

Nibbles:

- Director dealings:

- The CEO of Bytes Technology (JSE: BYI) bought shares worth around R2.3 million. But this purchase was eclipsed by an independent non-executive director, who bought shares worth R9.3 million! It’s always very encouraging to see on-market purchases like these. Remember, VCP also recently bought a chunk of shares in Bytes. The share price is up 19% over 30 days and 14% year-to-date.

- The CEO of Africa Bitcoin Corporation (JSE: BAC) bought shares in the holding company worth R86k.

- Copper 360 (JSE: CPR) announced that the mining contract for the Rietberg mine has been awarded to Cementation Africa, the mining business that emerged from the Murray & Roberts corporate collapse. The contract is worth R874 million and is structured as a “strategic alliance” – that certainly sounds a lot friendlier than many of the construction contracts that end in disputes and large claims. Let’s hope that this one goes smoothly. This is a significant step for Copper 360, particularly as the share price has suffered a catastrophic decline of 91% over three years.

- Spear REIT (JSE: SEA) announced that the Competition Commission has approved the acquisition by Spear of the three office buildings at 1 Sportica Crescent, Bellville. Transfer is expected during September 2026.

- Raubex (JSE: RBX) has renewed the cautionary related to the ongoing evaluation of strategic options related to the investment in Bauba Resources. My view is that they need to try get out of that asset entirely, as it isn’t a good fit with the rest of the group. Much easier said than done, of course!

- Datatec (JSE: DTC) announced that the deal related to the refinancing of Westcon International and the investment in a minority stake by General Atlantic has been delayed by a few weeks. The closing date has moved from 14 July 2026 to 4 August 2026. A delay is not uncommon in corporate transactions.

- Lewis (JSE: LEW) announced that Global Credit Ratings (GCR) updated its credit ratings to AA-(ZA) and A1+(ZA) for long- and short-term debt respectively. As lending money is core to the Lewis business model in furniture retail, having cheaper access to finance is extremely helpful for margins. Ratings upgrades don’t tell you anything about whether the shares are a good purchase at this price, but they sure do tell you a lot about the underlying financial health of the group.

- I generally don’t comment on ongoing share repurchase programmes, but I’ll make an exception for Reinet (JSE: RNI) given the significance of their decision to return excess cash to investors. Between 6 July and 10 July 2026, they repurchased shares worth R582.6 million.

- Shuka Minerals (JSE: SKA) has completed the eighth drill hole at the Kabwe Zinc Mine. The “Speaks” orebody seems to be returning better results than management anticipated, so that’s positive.

- Master Drilling (JSE: MDI) has now received the necessary approval from the SARB for the special dividend of 40 cents per share. The payment date is 17 August 2026.

- PPC (JSE: PPC) has beefed up its board with the appointment of a highly experienced banker as an independent non-executive director. Nick Pagden, who has served as Chairman of Banking South Africa at Citigroup since 2022, joins the board (and investment committee) with effect from 1 October 2026. I enjoy seeing skills like these on corporate boards.