Choppies Enterprises intends to launch a partly underwritten renounceable rights offer to raise P300 million. The offer will be partly underwritten by Ivygrove and Export Marketing. The company will offer a total of 520,833,333 ordinary shares at an offer price of P0.576/R0.82368. The offer will open on 15 June 2023.

CA Sales has made an odd-lot offer to approximately 5,073 shareholders holding less than 100 CA&S ordinary shares. If the 117,861 shares are repurchased at an assumed price of R7.29 per share, the cost to the company will be c. R859,207 (excluding transfer costs).

Adcorp shareholders are to receive a special gross dividend of 91,3 cents per ordinary share in addition to a final gross dividend of 16,5 cents per ordinary share. This follows the release of the company’s audited results for the year ended 28 February 2023.

On June 30 2023, at a general meeting of the company’s shareholders, Nampak will propose a restructure of its share capital by consolidating and reducing the authorised ordinary shares by the consolidation of every 250 shares into one share, propose and increase in the authorised, unissued share capital of the company and the issue of new shares to implement a proposed rights offer to raise gross proceeds of up to R1 billion. The company will over the next two months conclude credit-approved term sheets for the refinancing package for the next five years. This, together with the group’s progress in its implementation of the restructuring plan, will determine the size of the rights offer required. The date by which credit approved term sheets for the refinancing of the group debt needs to be finalised has been extended from 15 June to 15 July 2023.

Kibo Energy is to issue 48,000,000 in respect of a warrant exercise notice received. The shares will be issued at a price of £0.001 with an aggregate value of £48,000.

The Mediclinic and Bidco deal, first announced in August 2022, has become effective. Mediclinic is expected to delist from the JSE and the NSX from commencement of trade on 7 June 2023.

Tradehold has received confirmation that the special resolution for the change of name of the company to Collins Property Group Ltd. The company will trade on the JSE under its new name from 13 June 2023 under the share code ‘CPP’.

Barloworld and Astral Foods have taken secondary listings on A2X with effect from 7 June 2023. These companies with market capitalisations of c.R16 billion and R6,1 billion respectively, will retain their listings on the JSE. These listings will bring the number of instruments listed on A2X to 134 with a combined market capitalisation of over R9 trillion.

A number of companies listed on one of South Africa’s Stock Exchanges have initiated share buyback programmes and each week update shareholders. They are:

Over the period 2 December 2022 to 31 May 2023, Southern Sun has repurchased 50,604,422 shares at an average price of R4.47 per share for an aggregate R226,31 million. The repurchased shares represent 3.4% of the company’s issued share capital. A further 16.6% may be repurchased in terms of the General Authority granted by shareholders in September 2022.

Lewis has repurchased a further 2,801,999 shares, representing 4.8% of the issued share capital of the company at the beginning of the share repurchase programme. The shares were acquired for an aggregate R114,14 million.

The Old Mutual Board believes that the Old Mutual share price is trading at a discount to its intrinsic value and believes that a share repurchase programme will deliver longer term incremental value to shareholders. The Group has commenced a Repurchase Programme of R1,5 billion and will continue to repurchase the company shares until the maximum amount is reached.

South32, this week, repurchased a further 1,043,510 shares at an aggregate cost of A$4,10 million.

This week Glencore repurchased a further 12,330,000 shares for a total consideration of £51,78 million. The share repurchases form part of the second phase of the company’s existing buy-back programme.

Prosus and Naspers continued with their open-ended share repurchase programmes. During the period 22 to 26 May 2023, a further 2,313,758 Prosus shares were repurchased for an aggregate €151,98 million and a further 514,577 Naspers shares for a total consideration of R1,64 billion.

Seven companies issued profit warnings this week: Mahube Infrastructure, Buka Investments, Brikor, Trustco, Huge Group, Capital Appreciation and Spar.

Three companies issued or withdrew a cautionary notice: Choppies Enterprises, Primeserv and Afrimat.

Nigerian Breweries Plc has advised shareholders that it is considering a proposal by Heineken Beverages of South Africa that it acquire Heineken Beverages’ majority interest (via Distell International) in Distell Wines & Spirits Nigeria Ltd. The outcome of the brewer’s decision will be communicated to shareholders in due course.

Bestfly, an Angolan multinational aviation group, has acquired Austrian aircraft asset management company MS Aviation as part of its broader European expansion drive. Financial details of the transaction were not disclosed.

Egyptian developer Tatweer Misr and Naif Alrajhi Investment, a Saudi Arabian company, are to form a joint venture. The JV will focus on construction and real estate investment with an emphasis on the development of residential, commercial, educational, entertainment and hospitality projects in Saudi Arabia. The intention is to expand into Egypt. Financial details were undisclosed.

The acquisition of KEL Chemicals, a manufacturer of phosphate fertilizers, water treatment products and sulfuric acid-based industrial chemicals, has been unconditionally approved by the Competition Authority of Kenya.

In a further filing, the Competition Authority of Kenya has given Abland Diversified Holdings unconditional approval to acquire the remaining 50% stake in Buffalo Mall Naivasha.

Oryx Properties, a Namibian, NSX-listed property fund is to undertake a renounceable rights issue to raise N$379,6 million. The issue is in respect of 32,698,877 rights issue units in the ratio of one rights issue unit for every 2,5 linked units held.

PrestaFreedom, a Morocco-based home services marketplace, has raised US$1,1 million from Casablanca-based Azur Innovation Fund. PrestaFreedom intends to use the investment from the venture capital fund in its logistics and technology development with the aim of accelerating growth and scaling its footprint to a number of African markets.

Moroccan healthtech startup DataPathology was also the recipient of an investment from the Azur Innovation Fund, raising US$1m in its second seed round of funding. The investment will be used to recruit talent to support its growth trajectory.

South African listed property struggled last year and ended 2022 as the worst performing sector on the JSE, delivering a negative total return of circa 2%. This was largely due to rapidly rising inflation (exacerbated by the Russia-Ukraine war), followed by interest rate increases by the South African Reserve Bank and international central banks, aimed at curbing inflation.

Europe’s reliance on Russia for gas led to an energy crunch during the Northern hemisphere winter months, which caused heightened concern for global investors regarding the ability of companies to withstand escalating energy costs and economic pressure. Geographically, South African listed property was shielded from direct war exposure, but nevertheless suffered from the broad-brush effects of the resulting capital reallocations.

Higher interest rates caused concern for investors in respect of property valuations, especially those properties that were already valued at lower than industry average discount rates/yields. Any expansion in these yields due to higher interest rates, which are not offset by increasing net income, result in a depressed valuation of the underlying properties. Companies with higher loan-to-value (LTV) ratios have been dealt a particularly hard blow, as investors expected these LTVs to increase off the back of reduced property valuations, combined with higher interest on loans. As a result, investors have priced in significant additional risk, which has led to the sell-off of listed property stocks.

A major difference between South African property companies and developed market global property companies is that South African businesses are accustomed to operating in a low growth environment, with elevated inflation levels and high interest rates, whereas many developed market global peers have traditionally benefited from higher economic growth, low inflation and very low interest rates. While significant economic growth in the South African economy appears a distant mirage at present, local property companies could benefit from the expected peaking of inflation and subsequent slow-down in interest rate hikes.

The three key performance metrics for listed property investors are total return, total return and total return (much like location). Investors usually gauge total return from expected increases in the property stock’s net asset value (NAV) and/or dividend yield/income. Many locally listed property companies trade at deep discounts to their underlying NAV, which may seem like a bargain to investors at face value, but which could also result in a value-trap scenario. When hunting for bargain property stocks in the market, the value trap is unlike a bear trap in that the gap between price and value does not always close (or may take a very long time to close), which poses risk for these value investors.

Due to ongoing loadshedding, many South African property businesses are allocating capital investment to alternative energy solutions, like solar, to ensure that their operations are better equipped for disruptions and to keep tenants incentivised to stay locked into medium-to-long term rental agreements.

Many South African property stocks that pay high dividend yields are compared directly to “risk-free” government bonds and/or risk-adjusted corporate bonds. But in the current high interest rate environment, it is anything but plain sailing for these listed property stocks that compete with bonds for capital in the market, and potentially also with safer bets, such as cash investments. Earnings growth will be key for South African property stocks to continue growing their dividends, and hopefully their NAV too. In the absence of earnings growth, investors may opt to be risk averse and stick with bonds and cash investments at the peak of the interest rate cycle.

Portfolio managers and analysts often regard certain Real Estate Investment Trust (REIT) sectors as resilient investment vehicles during times of recession, which can outperform general equities during high-inflationary periods. Experts note that REITs also outperform when bond yields continue to increase, and especially when a slow-down or pause in interest rate hikes are imminent. Whatever the environment, listed property companies benefit from having a strong balance sheet. A South African REIT is obliged to pay out at least 75% of its earnings to shareholders as dividends on an annual basis and, given that REITs receive the benefit of only being taxed on the portion of earnings that do not get distributed to shareholders as dividends, this translates into a larger pool of capital that can be allocated to dividends for shareholders, which can, in the right circumstances, provide good income opportunities for investors.

When considering capital allocation and, more specifically, returning capital to shareholders, several strategies are available to listed property companies, ranging from paying cash dividends to share buy-backs and scrip dividends. Listed companies typically consider share buy-backs in the open market where they believe that their share price is undervalued. In terms of the JSE Listings Requirements, a listed company may not buy back its own shares in terms of a general repurchase authority at a price greater than 10% above its trailing five-day volume weighted average price, which provides protection to shareholders from a capital allocation perspective.

Strategic share buy-backs, followed by the cancelling of the repurchased shares, could attribute tangible value on a per share basis to shareholders, especially where earnings grow. Scrip dividends are usually offered to shareholders as a mechanism to preserve cash reserves for the company and/or to provide shareholders with an opportunity to receive additional shares on a pro-rata basis relative to their current shareholding, without incurring transaction costs that would ordinarily need to be spent in buying shares on the open market. Scrip dividends are, however, not viewed favourably by shareholders if implemented when the share price of a listed property company trades at a substantial discount to its NAV, as issuing cheap equity is not value accretive.

Depending on how the remainder of 2023 unfolds from an inflation and interest rate perspective, the result is expected to drive and/or change investor risk appetite in the markets, which could benefit well-positioned JSE-listed property companies.

Calvin Craig is a Corporate Financier | PSG Capital.

This article first appeared in DealMakers, SA’s quarterly M&A publication

In this inaugural issue of our Corporate Law Digest, we look at significant events that have taken place in Kenya’s business environment over the last quarter, to provide you with a glimpse into the country’s transforming M&A market. We find that despite growing concerns about the devaluation of the Kenyan Shilling, the increasing cost of living, unemployment and civil unrest, investors seem undeterred: banking, fintech and alternative fuel sources feature prominently in a market that is diverse, flush with entrepreneurs, and backed by its new government. Kenya is open for business, and with an election well behind it, ready to flourish.

Recent M&A Trends in Kenya

In recent years, the M&A space in Kenya has been punctuated by transactions in the financial industry, specifically where investors are looking to expand or diversify their portfolios. Two key deals of note in Q1 are those of Equity Bank (Kenya) Limited (EBKL), the largest financial services institution in the region, which purchased certain assets and liabilities of a local “troubled” Spire Bank, and the acquisition of 55.8% of Maisha Microfinance Bank by Cactus Cantina Investments Limited, a sister company of lending app Shara, which is currently awaiting Central Bank approval. On completion of the EBKL transaction, loan customers and customers holding deposits in Spire Bank become EBKL customers, significantly expanding EBKL’s asset portfolio and customer base. With respect to Maisha, customers of the lending app Shara will be able not only to borrow more, but save with the lender.

Within the fintech space, there has been a continuing upsurge of activity. According to a Fintech Global study published in February 2023, Kenya’s fintech deal activity increased by 14% from 2021 to a total of US$158 million. The largest Kenyan fintech deal in 2022 raised $75 million for M-Kopa, a linked asset finance platform. This is nothing to sniff at.

Impact investment funds, as well as green energy companies, have equally been hot targets in Kenya. BlackRock Alternatives, a climate-focused fund, is set to acquire a stake in Lake Turkana wind park, Africa’s largest wind turbine complex. Furthermore, Australian hydrogen project developer Fortescue Future Industries plans to build a 300 MW green ammonia and fertiliser plant in Kenya, the country’s first project involving green ammonia production. This is not to forget that in late 2022, New Forest launched the Africa Forestry Impact Platform (AFIP), a partnership between British International Investment (BII), Norfund and Finnfund with the goal of helping to transform the forestry sector in sub-Saharan Africa. Green investments seem destined to take pride of place in M&A deals in the near future.

SMEs in Kenya

A report issued by the Central Bank of Kenya indicated that SMEs constitute 98% of all businesses in Kenya, contributing 3% to GDP. A survey by the Kenya National Bureau of Statistics released in 2018 indicated that approximately 400,000 micro, small and medium enterprises do not make it past the second year, while very few reach their fifth year. In this respect, SMEs have generated a lot of local and international interest in their quest to capital raise. Government support has not lagged far behind with initiatives such as the Start-Up Bill 2021, proposing to provide a legislative framework that fosters a culture of innovative thinking and entrepreneurship.

In March 2023, the African Development Bank Group approved a $30 million Trade & SME Finance Facility for Family Bank Limited (FBL) in Kenya, aimed at boosting intra-Africa trade, promoting regional integration, and reducing the trade and SME finance gap in the country. The facility aims to provide a trade finance line of credit, a transaction guarantee, and a targeted line of credit to support short- and medium-term financing for SMEs in the health, renewable energy, and agriculture sectors, including women-owned businesses.

So while SMEs have room to grow, it is also important to note that in March 2023, a new report commissioned by Kenyatta University shows that debt funding is the most popular method of raising capital among micro, small and medium enterprises (MSMEs) in Kenya, with 42% preference, compared to grants and equity financing at 36% and 22%, respectively. Investors should take note: entrepreneurs are not likely to be willing to let go of control, especially when they are confident that a debt instrument may help them to scale.

Looking ahead 2023

Kenyan firms are increasingly turning to cleaner energy sources to reduce carbon emissions. This has seen a significant rise in the businesses entering the Kenyan market-focused on clean energy and e-mobility. We are seeing start-ups like Ecobodda Inc, Africa’s first electric motorbike taxi, providing battery-swapping charging technology for electric motorcycles. Roam Rapid and BasiGo, are also cementing their position in the electric vehicle industry by providing electric bus solutions to the Kenyan market. Large companies and state corporations such as KENGEN are also dipping their toes in the industry by installing electric vehicle charging infrastructure at some of their petrol stations and by proposing a special tariff for electric vehicles.

Earlier in March 2023, the European Investment Bank (EIB) mobilised $1,9 million in grants to support green hydrogen in Kenya, and the European Union, together with the UK government, is investing Ksh13,5 billion ($108 million) in the Menengai geothermal project in Nakuru County, Kenya, which will provide cheap, clean and reliable energy to over 700,000 Kenyans.

We look forward to sharing further positive developments that further cement Kenya’s position as a regional M&A market leader.

Njeri Wagacha is a Partner and Rizichi Kashero-Ondego a Senior Associate at CDH Kenya.

This article first appeared in DealMakers AFRICA, the continent’s quarterly M&A publication.

Significant investment has already been secured from individual and corporate investors looking to claim their SARS-approved 125% Section 12BA tax deduction in this tax year.

Twelve B is the first private equity fund that entitles taxpayers, including individuals, trusts, companies and pension funds, to invest in a portfolio of renewable energy-producing assets and benefit from the Section 12BA tax incentive.

Twelve B Green Energy Fund marks another milestone for Grovest, the pioneers of Section 12J, and the largest small cap fund administrator in South Africa, with over R3.5 billion in assets under administration.

During the extensive pre-launch period, the Twelve B team focused on sourcing viable projects as well as establishing strategic partnerships with EPC (Engineering, Procurement, and Construction) and O+M (Operations and Maintenance) entities. This meticulous preparation ensured that when Fund I opened for investment, they were well-prepared to deploy capital as and when it was raised.

Current status of the Fund

Twelve B Green Energy Fund currently has a pipeline of over R300 million of solar projects at various stages. Jeff Miller, Twelve B’s CEO and Co-Founder anticipates the average investment across the various projects to be between R8 million and R12 million, resulting in a diversified portfolio of around 25 projects in Fund I’s R200 million portfolio.

In April 2023, the Fund’s first two projects were approved by the Investment Committee and construction has since commenced. They are on track to become energy-generating in July of this year. The profits of the partnership which have been generated from the sale of electricity, net of costs, will be distributed to investors bi-annually, and current investors can expect their first income distribution in September this year.

The first project approved is a sectional title complex situated in Dunkeld, Johannesburg. The solar system will have a peak power capacity of 175 kilowatts and the energy storage system will have a capacity of 300 kilowatt-hours.

The second project is a commercial business in Sandton, and the solar system will have a peak power capacity of 201.7 kilowatts and the energy storage system will have a capacity of 500 kilowatt-hours.

Although the ability of a fund to reach final close may be a key consideration for an investor, fund success is ultimately determined by its ability to deliver consistent and attractive returns (i.e. deploying capital into projects that have the potential to generate cash flows). Therefore, investors should carefully evaluate the capability and project pipeline of the Fund Manager before committing their capital.

Miller emphasises the crucial nature of conducting comprehensive due diligence on all projects to manage risk, evaluate project viability, remain compliant, promote transparency and accountability, as to ensure that the projects are aligned with the Fund’s Investment Mandate.

Furthermore, each project is bound by 20-year Power Purchase Agreements (“PPA’s”) which sets out the amount of electricity to be supplied, the initial pricing and the annual escalations.

Twelve B Green Energy Fund’s strategic alliance

The Fund has a strategic alliance with Hooray Power– the pioneers of large battery storage systems in sectional title complexes. The Fund has the right of first refusal on all projects introduced by Hooray Power.

Hooray Power’s sophisticated load management software manages power via solar, battery and the grid which provides an always-on power solution for their clients.

They have a 4-year proven track record and are the longest operator of these actively-managed battery systems in South Africa.

According to Miller, the Fund’s secret sauce and differentiating factor within the market is their relationship with Hooray Power, who sources all projects and handles all EPC and O+M of each approved project. This relationship is unique to the Twelve B Green Energy Fund and to the investment opportunity.

Miller is of the view that deployment and execution of the funds into energy producing assets is key, and has unwavering confidence that Twelve B Green Energy Fund will raise and deploy R200 million before the end of the February 2024 tax year.

The risk profile of the Fund is low to moderate, and there is currently no gearing within the portfolio. That said, the Fund Mandate does allow gearing which may be considered in the future.

Fund I is still open for investment and the positive market response confirms that investors within the current market climate have an appetite for a moderate risk, tax incentivised investment.

Twelve B Green Energy Fund invites savvy investors wanting to decrease their tax obligation and achieve superior returns, to invest today and add to a greener, more sustainable future for South Africa.

Twelve B Fund Managers Proprietary Limited (Registration No. 2022/832884/07) is an approved juristic representative of Black Mountain Investment Management Proprietary Limited (Registration No. 2018/230022/07) an authorised Financial Services Provider under the FAIS Act (FSP No 49908).

Afine’s profits are in line with the pre-listing forecast (JSE: ANI)

Year-on-year comparability is limited due to restructuring activities

Afine Investments is a REIT that owns a portfolio of fuel filling stations. The numbers for the year ended February 2023 reflect some big year-on-year moves, but the company is reminding investors that comparability on that basis is limited.

Instead, the focus is on the results vs. the forecasts made in the pre-listing statement. On that basis, distributable profits are actually slightly higher (6.5%) than the forecast levels and HEPS is in line with the forecast.

The total dividend per share for the year was 43.83 cents. The current share price is R4.49 but the bid-offer spread is absolutely huge, so good luck getting a trade through.

At Capital Appreciation, growth comes at a cost (JSE: CTA)

Strong revenue growth has been offset by expense growth and a large credit loss provision

In a trading statement for the year ended March 2023, Capital Appreciation noted an impressive 19% growth rate in revenue. That’s largely where the good news ends for investors, as there has been a significant increase in expenses and there’s a nasty credit loss provision as well.

The expenses relate to the core business, so let’s start there. The rate of growth in expenses isn’t disclosed in this announcement but we know that HEPS is between -2% and -1% lower than the prior year, which means between 13.13 cents and 13.27 cents.

That HEPS number excludes the credit loss provision for the GovChat associate of R70.8 million. If we take that into account by looking at EPS, there’s a drop of between -45.5% and -44%.

The share price closed 6.3% lower at R1.48, which implies a Price/Earnings multiple of roughly 11.2x. Detailed results are expected on 6th June and I’m sure that investors will take a detailed look at the expense growth and how it supports future growth.

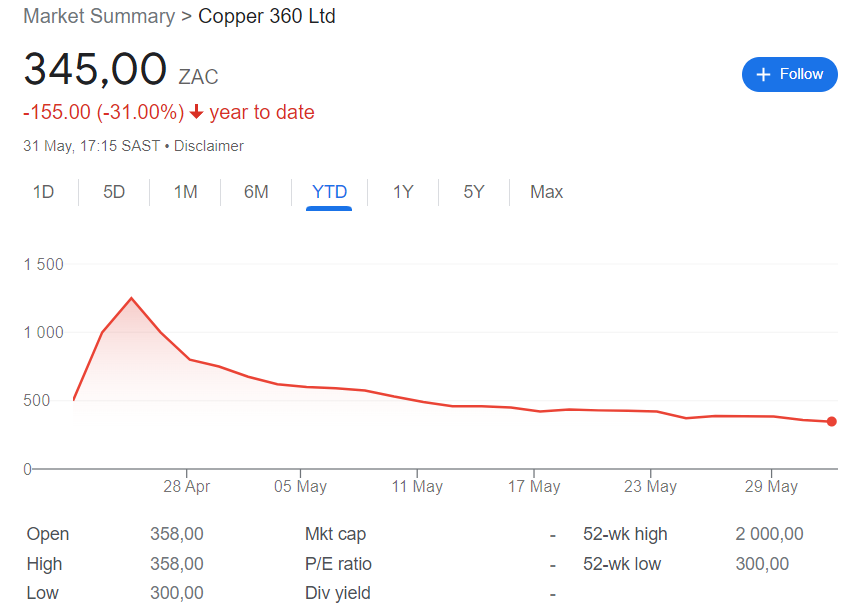

Copper 360 was classic IPO silliness by punters (JSE: CPR)

As I joked at the time of the listing, the ticker CPR might indicate what some people will need!

It certainly isn’t the company’s fault that investors love throwing money away shortly after an IPO. This is a story as old as time, which is precisely why I avoid IPOs as a rule (just look at Zeda as another example). Here’s the Copper 360 chart:

The company has released results for the year ended February 2023 and has also given an operational update.

Growth is rapid, with tons milled up by 296% and copper sales up by 191% The average copper price received fell by 5.4% measured in rand. I must highlight that there was only five months of focused trading in this period, so I’m not sure that the growth rates are all that useful.

With the group very much in the early stages of its life, the revenue increase of 175% was overpowered by a 279% increase in operating expenses. This drove a swing from an operating profit of R9.8 million to an operating loss of R78.5 million. That’s the number that I would keep in mind.

I would also take note of management’s commentary around a decrease of 36% in the delivered copper grade, a direct result of lower grade stockpiles of ore that necessitated the acquisition of a R30 million crushing plant. The company still believes that the forecast copper production for FY24 that was noted in the pre-listing statement can be achieved.

Fairvest: it matters which class of shares you own (JSE: FTA JSE: FTB)

The A shares are smiling – the B shares not so much

In property funds with two classes of shares, you really need to do your homework. These legacy structures were put in a place during a time when institutional investors demanded a mix of safer and riskier structures. The theory is that one class is more defensive than the other, but then offers less upside as well.

At Fairvest, the results for the six months to March 2023 reflect a drop in net asset value (NAV) per share for both share classes. The dividend for the A shares is 5% higher and for the B shares is 2% lower.

The loan-to-value sits at 38.4%.

In addition to its portfolio of 137 properties, Fairvest holds 60.9% in Indluplace and 5.1% in Dipula Income Fund. Remember, Indluplace is currently under offer from SA Corporate Real Estate.

The market is sending a Huge message about valuation (JSE: HUG)

Some of these investment assumptions are breathtaking

Despite the obvious economic pressure we find ourselves in, Huge Group somehow managed to increase the net asset value (NAV) per share by 5.3%. It now sits at R9.4385 per share, with the share price at R2.74. This discount to NAV is gigantic even by investment holding company standards, so something isn’t adding up.

I decided to go digging into the way in which the assets have been valued. It’s not hard to see why the market puts more faith in Eskom’s promises than this valuation.

Let’s start with the R571.9 million valuation on the Huge Connect preference shares. With the total unlisted portfolio apparently worth R1.46 billion, this is a very big contributor. I therefore find it remarkable that the valuation yield is 10.85% at a time when the South African 10-year bond yields are over 11%.

Is Huge less risky than the government of the country in which it operates? Do me a favour.

We then arrive at Huge TNS, valued at R641 million. The weighted average cost of capital applied here is 16.81%, with meaty revenue growth of 10.13% in the model. This division is the combination of Huge Networks and Huge Telecom, with the Telecom side of the business having historically struggled. Personally, that discount rate feels too low for me.

The share price is down 27% in the past year. Against that backdrop, I cannot see how any valuation increase of 5.3% in the NAV per share could hope to be taken seriously.

The bun fight between Northam Platinum and Impala Platinum is setting interesting precedent

If you have deal fatigue regarding the battle for control of Royal Bafokeng Platinum (JSE: RBP), can you imagine how the parties and advisors involved must feel?

Northam Platinum (JSE: NPH) eventually walked away from the deal, citing a drop in PGM prices. This left Impala Platinum as the only horse in the race to get control of Royal Bafokeng. This has finally happened thanks to the PIC selling its 9.26% stake in Royal Bafokeng Platinum to Impala Platinum.

After the latest trades, Impala Platinum holds 55.46% in Royal Bafokeng Platinum – a controlling stake. This triggers the public interest and related conditions of the approval by competition authorities, which inevitably means a requirement to execute B-BBEE ownership transactions. This will include community and staff trusts as well as the introduction of an empowerment consortium.

Black retail investors get shut out as usual, although Royal Bafokeng Platinum does have a history of being highly focused on regional empowerment rather than broader, national empowerment. This is a more reasonable outcome than when Absa didn’t do a retail B-BBEE deal, for example.

Although Northam Platinum pulled out of the deal, they remained a thorn in the side of Impala Platinum, as the offer requires a compliance certificate from the Takeover Regulation Panel (TRP). To get that certificate, certain complaints made by Northam Platinum needed to be resolved.

To this end, Impala Platinum has elected to formerly withdrawn certain statements made by executives to the media and in results presentations over the course of the offer. The comments vary, with references made to the market dynamics of the deal, the appetite for time extensions and comments on the Competition Commission approval.

The official line is that Impala Platinum has withdrawn the statements and advised the public to ignore them in consideration of the offer. This is not an admission that the statements were false or misleading. We will now wait and see how long the Compliance Certificate takes to come through. The longstop date for the offer has been extended once again to 28 June, so that’s the (very loose) deadline that Impala Platinum has set to meet this condition.

Mahube Infrastructure needs more wind, please (JSE: MHB)

A feel-good asset isn’t always a good asset

Mahube Infrastructure has investments in solar PV and wind farm projects. We would all love these to be slam-dunk winners, but sadly life is never so easy.

For the year ended February 2023, the revenue was actually negative R14.1 million. I don’t think I’ve ever seen negative revenue before and I didn’t have time to dig into the financials on this. They note positive dividend income of R18 million and then a negative change in the fair value of the assets, which decreased revenue by R33.1 million.

Perhaps someone who is more up to date than me on IFRS can explain why the change in fair value is recognised as revenue.

Either way, the worrying bit isn’t just the change in macroeconomic inputs that has affected the valuation. No, I would be more worried about the comment that the wind IPP industry across the country is experiencing lower winds than expected. This certainly highlights the risks inherent in such projects.

The tangible net asset value has dropped from R11.21 last year to R9.91 in this period. There is no final dividend after an interim dividend of 45 cents was declared earlier this year.

Nampak prepares for its rights offer (JSE: NPK)

A share consolidation is necessary to escape penny stock territory

After the monumental destruction of shareholder value at Nampak, the share is now trading at 73 cents (down another 4% for the day). This isn’t great for a rights offer that is clearly going to be priced at a discount, with Nampak worried about setting the rights offer price at a “practical level” – that says a lot about what is coming.

In preparation for the R1 billion capital raise that is desperately needed to save the balance sheet, Nampak is proposing a share consolidation that turns every 250 shares into 1 share. In other words, the price should be 250 times higher after this as there will be fewer actual shares in issue.

Some cash will change hands, as fractional entitlements (i.e. where you own fewer than 250 shares) will be cash settled at a 10% discount to the VWAP of the first day of trading.

The slide in Nampak’s value has been extraordinary and I wouldn’t be surprised to see more pain before this rights offer is concluded.

Sirius reports strong growth in its distribution (JSE: SRE)

The benefit of low funding costs was still in these numbers

Sirius Real Estate has given the market guidance on the total expected dividend for the year ended March 2023. The increase is between 26.2% and 31.4%, which is obviously a good outcome for shareholders.

After the recent announcement around the refinancing of debt and the increase in funding cost as rates have gone through the roof in the past year, I would caution that this growth probably isn’t sustainable.

Spar is the latest retail casualty, tanking 15% (JSE: SPP)

The South African retail apocalypse continues

The local retail industry is being smashed by load shedding. I was bearish on this sector coming into 2023 and had written on that view a few times. I wanted to be wrong, but sadly I wasn’t.

Spar has guided a decrease in HEPS of between -35% and -25% for the six months ended March 2023. This horrific outcome isn’t from a lack of turnover growth, but rather from huge jumps in operation expenses.

Spar is a wholesaler, so fuel and distribution cost pressures sit squarely in this group. There was also substantial investment in IT, so that didn’t help matters against this economic backdrop, as I don’t think I’ve ever seen a SAP implementation that hasn’t been accompanied by major inventory issues and implementation challenges. Even the European operations weren’t immune from the cost pressures.

And of course, the environment with higher interest rates is driving an increase in net finance costs.

If we dig deeper, Spar’s wholesale grocery business grew turnover by 7.9%. TOPS, usually a strong performer, suffered a 1.9% drop in sales vs. a high base period when South Africans were unleashed to behave wildly after lockdowns. Build it reported further declines, down 3.8%.

Looking abroad, BWG Group in Ireland and South West England reported 8.8% turnover growth measured in euros. SPAR Switzerland fell by 4.3% in local currency thanks to volume declines. Turnover in Poland was up 4.9% in local currency despite contracts being terminated with 58 retailers in July 2022.

The pharmacy business is tiny but was actually the highlight, with sales up 20%.

The group reckons that the retailers spent over R700 million on diesel in this period. At wholesale level, diesel costs “more than tripled” and pressure in the retail stores obviously flowed to the top, as Spar doesn’t have a business without its franchisees doing well.

Much like the entire sector right now, I continue to avoid this one.

Tongaat Hulett has published the business rescue plan (JSE: TON)

It looks like a JSE delisting is likely

If you would like to see what a business rescue plan looks like, you’ll find the plan for the group holding company at this link.

In summary, the business rescue practitioners are looking for strategic equity partners for the business and it looks likely that a delisting from the JSE will take place. The plan notes that if the company was liquidated, unsecured creditors would receive nothing. Shareholders would therefore also receive nothing.

In case you’re wondering how that happens, BDO has estimated the assets to have a gross realisable value of R5.1 billion. Secured creditors have claims of R7.3 billion and unsecured creditors had another R1.7 billion excluding inter-company loans.

With 2,500 direct employees and 23,000 indirect jobs depending on this group, the reality is that saving Tongaat Hulett is a social imperative. The effect on the local sugar industry would be horrific if this group was not able to continue in some form or another.

To achieve that, a strategic equity investors will need to buy the assets of the group out of business rescue, with the creditors being dealt with through this process. Expressions of interest have been requested from eight bidders, so there is interest in the asset. It just won’t help existing shareholders who have essentially been wiped out.

Little Bites:

Director dealings:

Two directors of Calgro M3 (JSE: CGR) bought shares worth R436k.

MTN (JSE: MTN) is holding a capital markets day over two days this week (so the name is a bit odd, but it’s an industry standard). There are a large number of materials, including several podcasts, available at this link for those interested.

In a very interesting move, Serialong Financial Investments is being required to deliver nil paid letters to Glen Anil Development Corporation even on the Purple Group (JSE: PPH) shares that Glen Anil only has the option to acquire. The argument is that the rights were attached to the shares at the time of the original option agreement, even though the rights offer hadn’t been announced at that stage. I really can’t see why Glen Anil would exercise the options then, as the rights offer lets them mop up a large number of shares at a vastly lower price than the strike price in the option agreement. This is painful for Serialong.

Renergen (JSE: REN) has released its financials for the year ended February. With the group very much in the early stages of production, I don’t pay much attention to the headline loss per share of 19.89 cents. The current share price is being driven by a multitude of factors and I don’t think last year’s results feature highly on the list.

RH Bophelo (JSE: RHB) is a healthcare investment entity that focuses on net asset value as its leading metric. In the year ended February 2023, this has decreased by 3.5% overall and 3.6% on a per share basis. Cash is up from R8 million to R152 million but borrowings have increased from nil to R102.5 million and I’m not sure this is the right environment for borrowing money. There was no dividend in this period, unlike in the last period.

Metals business Insimbi Industrial Holdings (JSE: ISB) announced results for the year ended February 2023. A drop in revenue of 5% drove a decrease in operating profit of 3%. At net profit level, there was a 2% increase and at HEPS level, there was growth of 12%. The metric to keep an eye on is cash from operating activities, down 30%.

Trustco (JSE: TTO) released results for the six months ended February 2023, reflecting a drop in NAV per share of 10.6% that the company largely attributes to the resources portfolio and associated dilution in underlying assets.

Brikor (JSE: BIK) released results for the year ended February, showing a 14.3% increase in revenue but a collapse in HEPS to a loss-making position of -0.1 cents per share. The coal segment was loss-making for the year but showed improvement towards the end of the period, while the brick segment performed very well overall.

The most useful thing about the release of financial results by Buka Investments (JSE: ILE) is that at least I now know how to find the corporate website. The company is a “suspended shell” on the JSE that had no assets at the end of February other than some cash. The initial plan was to acquire a shoes business, but that was stopped for various reasons (even though the website seems to imply otherwise). The idea is now to acquire fashion businesses. After burning through R1.9 million in FY23 just to be a listed company, they better get on with it.

The scheme of arrangement to delist Industrials REIT (JSE: MLI) was approved by shareholders, with the delisting date on the JSE anticipated to be 27 June.

In case you’re wondering, the acquisition of Bundu Power by Ellies Holdings (JSE: ELI) is still intended to go ahead. The publication date of the circular has been extended to no later than 31 July.

Metair (JSE: MTA) has announced that the current interim CEO and interim CFO have both been appointed to the roles permanently, which is good news for investors in terms of stability.

Lewis Group (JSE: LEW) has repurchased a further 4.8% of issued shares during May, with a value of R114 million. Another 2.2% of shares outstanding can be repurchased under the existing authority from shareholders, calculated with reference to the number of shares that were in issue at the time the authority was granted.

Shareholders of Tradehold (JSE: TDH) have approved the change of name to Collins Property Group Limited. It will be made effective during June.

In other renaming news, Tsogo Sun Gaming (JSE: TSG) shareholders have approved the change of name to Tsogo Sun Limited. It will be interesting to see how the strategy develops in this group.

Delta Property Fund (JSE: DLT) has delayed the publishing of results from 31 May to 12 June.

Acsion (JSE: ACS) is another company with delayed results, expected to be released on 15 June.

In this episode of Ghost Stories, Duma Mxenge (Business Development Manager at Satrix) joins the platform for the first time for a great discussion around ETFs, trends around this type of investment and the way that investors understand the products and use them.

More specifically, we discussed:

Some of the generational trends coming through in the attitude to investing and particularly ETFs, including fees.

The impact of fees in a wealth creation journey.

Whether investors tend to have a good understanding of the underlying indices tracked by ETFs

The approach to using ETFs and whether investors see this as a “playing safe” approach or a more active investment decision.

A discussion around ETFs as the core underpin in a portfolio, leaving space for more speculative opportunities in single stocks.

The value of local ETFs that track global indices vs. moving cash into foreign currency and incurring forex costs.

The benefit of ETFs in the context of rebalancing of a portfolio of single stocks.

Whether retail investors can do it all themselves vs. using financial advisors as part of the journey.

The SatrixNOW platform and how it helps investors navigate this process.

For more from the Satrix – Ghost Mail partnership, visit this link to find various podcasts and articles.

Disclosure Satrix Investments (Pty) Ltd is an approved FSP in term of the Financial Advisory and Intermediary Services Act (FAIS). The information does not constitute advice as contemplated in FAIS. Use or rely on this information at your own risk. Consult your Financial Adviser before making an investment decision.

While every effort has been made to ensure the reasonableness and accuracy of the information contained in this podcast (“the information”), the FSP’s, its shareholders, subsidiaries, clients, agents, officers and employees do not make any representations or warranties regarding the accuracy or suitability of the information and shall not be held responsible and disclaims all liability for any loss, liability and damage whatsoever suffered as a result of or which may be attributable, directly or indirectly, to any use of or reliance upon the information.

A rare update from farming group Crookes Brothers (JSE: CKS)

A substantial farming operation in Caledon is being sold for R200 million

Crookes Brothersisn’t a company that you’ll hear from very often on SENS. They tend to just get on with it, navigating the challenging world of primary agriculture. The group is in the process of selling certain farming properties that aren’t generating returns in line with targets. This will enable Crookes Brothers to reduce debt and invest in other diversification projects.

The big news is the sale of Vyeboom Fruit Farm for R200 million, consisting of 404 planted hectares and related infrastructure.

One of the conditions is the purchaser (a Western Cape fruit farming business) obtaining a loan from Standard Bank. There’s no guarantee of this sale going through until the conditions are met.

The profit after tax for the farming operation for the year ended March 2022 was just R9.8 million and the net asset value was R265.2 million.

This is a Category 1 transaction, which means a circular will be sent to shareholders to approve the deal. It will no doubt include many interesting details around farming!

Hudaco announces a significant R315 million deal (JSE: HDC)

The acquisition of Brigit is a big investment into the fire protection space

Hudacois an industrials group that tends to do interesting deals. The latest example is the Brigit group of fire protection companies, clearly named after the founder Brigit van Zyl. This is a complementary acquisition for Hudaco as it bolsters the services already being sold into the security industry.

There are 65 employees in the business and revenue is R215 million per year. Profit for the year ended February 2023 was R36 million.

The maximum price is R315 million, based on average annual profits for the two years after the deal. The initial payment is R143 million and the rest is payable over two years.

Importantly, the current managing director of the business will enter into an employment contract for two years and has signed a restraint of trade covering a further three years.

Huge Group closed 14% higher, but watch the spread (JSE: HUG)

The net asset value per share is between 4.92% and 5.42% higher

The bid-offer spread on Huge Group is worthy of the company’s name, which is why you can see massive swings in a single day. The price action needs to always be interpreted very carefully.

After Huge Group decided to call itself an investment entity and change its accounting approach to rather reflect the fair value of underlying assets, the right metric to look at is technically net asset value (NAV) per share. This increased by between 4.92% and 5.42% in the year ended February 2022, implying a range of R9.41 to R9.45.

The share price of R2.74 is your best evidence of what the market thinks of the director valuations underpinning that NAV.

Invicta: focus on HEPS, not EPS (JSE: IVT)

Major asset disposals and fair value gains in the prior period are distorting things

There are very good reasons why investors tend to focus on HEPS rather than EPS. The H for “Headline” makes all the difference, as it splits out many of the accounting funnies and once-offs that tend to skew results.

For example, in the latest Invicta trading statement for the year ended March 2023, HEPS is up by between 43% and 53% whereas EPS is down between 32% and 42%.

To understand this properly, you need to take note of the profit on disposal of businesses in the comparable prior period and a large fair value gain on remeasurement of joint venture investments. This is included in the base period for the EPS calculation but not the HEPS calculation.

HEPS is thus the best measure of the performance in the core business and with a range of between R4.72 and R5.05, Invicta is trading on a Price/Earnings multiple of roughly 5.8x at the midpoint.

For the nine months ended March, normalised HEPS grew strongly

There aren’t many local companies that provide quarterly updates. Momentum Metropolitan is one of them, with an operational update released for the nine months ended March 2023.

Normalised HEPS has increased by over 32%, with a major driver being an improved mortality experience in the life business thanks to a less severe impact of Covid in this period. Share buybacks helped here as well, as normalised headline earnings increased by 29%. The additional 300 basis points was thanks to the number of shares in issue.

As is usually the case in these groups, new business volumes were up in some areas and down in others.

Annualised return on equity for the period of 18% was within the target range of 18% to 20%.

It looks like Hillie Meyer will be leaving the group on a high, despite the challenging economic conditions in which the business is operating.

Even Pepkor can’t escape these retail pressures (JSE: PPH)

These are dark days in our economy – literally

Pepkor is seen as a relatively defensive retailer in this market, or at least as defensive as a clothing and homeware retailer can really get. With a firm focus on a value offering, Pepkor competes on a combination of price and quality rather than brand. The challenge is that “defensive” is a relative term in South Africa, as the core client base of lower income consumers is under immense pressure from food and transport inflation.

I think there’s an argument that retailers further up the pricing curve are perhaps more defensive in this environment, as their customer base isn’t part of the “working poor” group of South Africans whose plight is genuinely heartbreaking.

That plight is clearly visible in the numbers for the six months to March, with 4.3% growth in revenue and an 11.7% drop in HEPS (or 8.6% excluding non-recurring items). Diesel costs increased by 142% to R72 million, which isn’t a total disaster in an expense base of R7.8 billion but definitely doesn’t help in a low-growth environment.

Ackermans is really struggling in this environment with an 8.3% drop in like-for-like sales, driving a 2.0% drop in like-for-like sales in the clothing and general merchandise segment. Overall growth in that segment was 7.0% thanks to Avenida in Brazil performing ahead of expectations.

Amazing, isn’t it? Businesses can function when they have electricity.

The trouble with poor performance at a retailer is that the balance sheet deteriorates rather quickly, with inventory levels up by 11.7% thanks to slower sales in the core operations. So not only is profitability down, but more working capital is tied up on the shelves.

PEP Home grew by 18.8% as another desperately needed highlight in this story.

Furniture, appliances and electronics retailer JD Group was impacted by weak demand and a 3.7% drop in like-for-like sales. Online sales are now 10% of the tech division’s turnover.

The Building Company managed to maintain its sales levels, which frighteningly means that it outperformed its competitors.

On the FinTech side, Flash improved profitability by over 20% and the Capfin lending business expanded its loan business. A sad reality of tough times is that it isn’t difficult to find people to lend to.

On that note, group cash sales grew by 2.6% and credit sales grew by 36.7%.

In terms of outlook, Pepkor notes that April trading was weak but May was better. Overall, the operating consumer environment is not expected to “improve any time soon” – ouch.

Our economy is severely broken and I do not see any obvious way for that to change. You hold shares in local retail businesses at your own peril, with Pepkor down over 11% in afternoon trade.

And guess what? Steinhoff is also impacted by this. If the equity in Steinhoff was worthless before, what is it now?

We finally know who Primeserv is buying (JSE: PMV)

On a market cap of just R130 million, I guess a deal worth R11 million is material

This transaction isn’t going to blow your socks off in terms of deal value, but at least we now know that Primeserv is acquiring Pinnacle Outsource Solutions and AJR Enterprises for just under R11 million.

These businesses supply temporary employment services within the logistics industry.

The purchase price is payable over three years based on net profit after tax targets for each of 2024, 2025 and 2026. This is a sensible structure when acquiring such a small company.

The profit after tax for the group was R4.5 million in the 2022 financial year, so there’s a good example of how low the valuation multiples are for private companies in South Africa.

Sirius refinances debt at 4.25% (JSE: SRE)

Welcome to the yield curve

When assessing property funds, it is very important to consider the impact of refinancing of existing debt. In a steady rate environment, that’s not a big deal. In a rising rate environment, it absolutely is.

Sirius Real Estate has refinanced a €58.3 million 7-year facility approximately seven months in advance of expiry, which I suspect is just a sign of the company’s expectations for further rate increases.

The all-in fixed rate is 4.25%, which is enough to take the group’s weighted average cost of debt from 1.4% to 2.1%. The total weighted average debt expiry has increased from 3.3 years to 5.0 years.

Another €49.3 million worth of debt is expiring within the next three years.

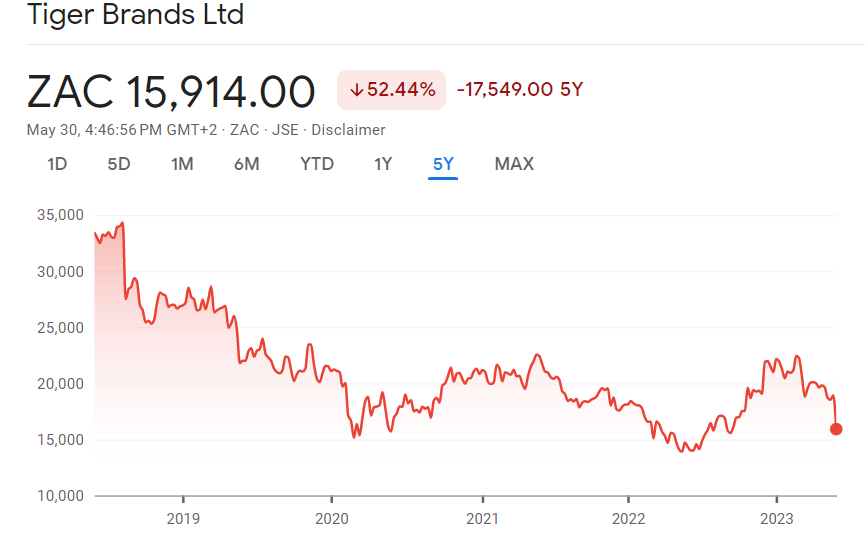

Tiger gets slashed down to March 2020 levels (JSE: TBS)

Food inflation is out of control

In case you’ve recovered from reading the Pepkor numbers, I’ll now hit you with the revenue growth of 16% at Tiger Brands.

But that’s great, isn’t it? It would be, if it wasn’t for the fact that 17% is from price increases and -1% is attributable to volumes.

Just let that food inflation story sink in and ask yourself: where does this end for the working poor of South Africa? Frankly, where does it end for the middle class?

Fascinatingly, Tiger Brand spent almost the exact same amount as Pepkor on diesel over the six months (in this case R76 million), which it reports as an incremental energy cost of R48 million. It’s good of Tiger to do that, as it gives us a reference point that running generators is costing roughly 60% more than using power from Eskom in those hours.

But here’s the difference in energy costs: while Pepkor only attributes 1% of operating costs to diesel, at Tiger the diesel spend is 1.9% of operating costs. Again that may not sound like a big difference, but these businesses are fighting for growth in an economy on life support and value is literally being transferred from shareholders to suppliers of diesel.

With gross margin down from 29.2% to 27.0% and pressure on expenses, group operating income fell by 9%. If you exclude the distortion of insurance payments in both periods, it was down 2%.

HEPS increased ever so slightly from 729 cents to 731 cents and an interim dividend of 320 cents was declared, which is bravely in line with the interim dividend last year.

The share price has retreated to March 2020 levels:

Trustco gives wide guidance for its NAV (JSE: TTO)

If you’re looking for precision, you won’t find it here

In the latest strange behaviour from Trustco, the company has released a trading statement that suggests its net asset value per share could be between 0.81% and 20.81% higher for the six months to February 2022. I think we can all agree that this isn’t exactly a tight range.

Results are due on 31 May, so I am sure they will be busy through the night to get that range tighter. Or perhaps they could’ve just released a trading statement timeously, rather than the day before results?

Little Bites:

Director dealings:

The CEO of MTN (JSE: MTN) has bought shares in the company worth $123.5k. You read that currency correctly – he bought American Depository Receipts. Fascinating.

The CEO of Pan African Resources (JSE: PAN) has taken advantage of the share price sell-off to buy £26.4k worth of shares and a similar exposure in CFDs on the UK market where the company is also listed. The financial director followed suit but on the local market, buying shares worth R757k.

Directors of Santova (JSE: SNV) have bought shares worth R1.27 million.

A director and an associate of that director bought shares in Redefine (JSE: RDF) worth R470k.

Old Mutual (JSE: OMU) has commenced its R1.5 billion share repurchase programme.

Afine Investments (JSE: ANI) announced that its HEPS for the year ended February 2023 will be within 10% of the profit forecast at the time of listing and 20% of the prior period.

Stefanutti Stocks (JSE SSK) has received R90.85 million under the project arbitration award and has made a capital repayment of R50.6 million towards the funding loan.

Southern Palladium (JSE: SDL) announced a mineral resource update that shows a 39% increase from the resource presented in the prospectus last year. The management team also sounds pleased with the conversion of Inferred to Indicated. These are technical terms that make sense to geologists.

Delta Property Fund (JSE: DLT) has agreed to sell 5 Walnut Road, Durban for R46 million. The proceeds will be used to reduce debt with the loan-to-value expected to decrease from 58.2% to 58%. Depressingly, a circular is needed for the deal which is costly and time consuming. This really is picking up pennies in front of a steamroller, but it’s not like the company has a choice.

If you want to reinvest your dividend in Dipula Income Fund (JSE DIB), the reinvestment price is R3.52 per share which is a 3.00% discount to the 30-day VWAP.

Mantengu Mining (JSE: MTU) announced the successful commissioning of the Langpan Mining Co chrome processing plant. First deliveries from the plant are expected imminently. There are another two processing plants that Langpan has invested in, both expected to be commissioned in August 2023. The company has also announced the appointment of a general manager of Langpan who comes with extensive experience, most recently within Northam Platinum.

In other commissioning news, Wesizwe Platinum (JSE: WEZ) has announced the commissioning of the Bakubung Platinum Mine processing plant.

The creditors of Tongaat Hulett Developments (the property subsidiary of Tongaat Hulett JSE: TON) have approved the business rescue plan.

Sable Exploration and Mining (JSE: SXM) released results for the year ended February that reflect a 2% drop in EBITDA and a 24% drop in the NAV per share. This is a highly speculative mining group in a state of flux and the financials aren’t the major focus for exploration companies.

With tough times at the company, it’s not ideal that the Company Secretary of Nampak (JSE: NPK) has resigned from the group after 19.5 years of service.

Unlock the Stock is a platform designed to let retail investors experience life as a sell-side analyst. Corporate management teams give a presentation and then we open the floor to an interactive Q&A session, facilitated by the hosts.

This year, Unlock the Stock is delivered to you in proud association with A2X, a stock exchange playing an integral part in the progression of the South African marketplace. To find out more, visit the A2X website.

In this nineteenth edition of Unlock the Stock, Calgro M3 returned to the platform with a triumphant set of results and a clear strategy for the way forward.

As usual, I co-hosted the event with Mark Tobin of Coffee Microcaps and the team from Keyter Rech Investor Solutions. Watch the recording here:

Is the value unlock at Adcorp finally working out? (JSE: ADR)

Revenue has grown for the first time since 2016

If ever you want to learn about the pain of a bid-offer spread in small caps, Adcorp is a great way to do it. The spread has come down a lot if there’s a busy trading day. On other days, you could park a bus in there. This makes it difficult to trade the stock and you have to patiently sit on the bid or offer at your desired price, hoping for a trade. You can’t just give an instruction to execute at the best available bid or offer at any given time as you’ll get a nasty surprise.

Looking at the results for the year ended February, the (rather shocking) news is that revenue from continuing operations has grown for the first time since 2016. Talk about a lost half-decade! Cash flow is also a lot better, with cash generated from operations up 45.2%. Operating profit from continuing operations is down 18.4% though, with the major culprit being a significant impairment of goodwill.

It’s a complicated result to try and work through, but cash is a language we all understand. With a share price at time of writing of R5.44, a special dividend of 91.3 cents and a final dividend of 16.5 cents have been declared.

Brikor warns of a headline loss per share (JSE: BIK)

The brick and coal group will release detailed results this week

Brikor released a trading statement noting a headline loss of between 0.09 cents and 0.11 cents per share for the year ended February 2022. This is a move from green to red over the past year, as the prior period reflected positive HEPS of 1.1 cents.

The current share price is 15 cents.

Exemplar enjoys a rebound in retail property (JSE: EXP)

Some of the malls could probably fit inside the bid-offer spread!

Exemplar REITail is a perfect example of the liquidity that investors complain about on the local market. This property fund is worth a few billion rand, so it’s certainly not a small cap. Despite this, bids are at R9.00 and offers at R12.00, which is a gigantic spread that makes trade very difficult.

Leaving that issue aside, let’s focus on results for the year ended February 2023. The 26 retail assets in the portfolio enjoyed a much better year, with revenue up by 18.4% and the total dividend per share by 20% to 141.12192 cents. I’m loathe to quote the current price of R9.00 in giving you a trailing yield, as the spread is huge and the yield will change drastically depending on the bid vs. offer. Perhaps that’s the point, with the huge spread reflecting a yield of between 15.7% and 11.8%.

At a yield of 15.7%, it’s not hard to see why some people are sitting on the bid at R9 and waiting to be hit.

The net asset value per share is R13.74, up 11.8% year-on-year.

Take a trip to Poland with Redefine (JSE: RDF)

After the takeover of EPP by Redefine, there’s a lot for shareholders to consider in Poland

Redefine announced that a property tour is being held in Poland over the next few days. Aside from being a lovely excuse for the fortunate few to travel and enjoy a country with electricity, this is a also useful opportunity for all Redefine investors to learn more about the EPP portfolio that Redefine acquired as part of that takeover and delisting.

EPP is the largest asset manager of retail real estate in Poland when measured by gross leasable area (GLA). There are 35 projects of which 29 are retail and 6 are offices. The portfolio is split across 23 Polish cities, absolutely none of which can be successfully pronounced by anyone whose surname doesn’t have a lot of Zs and Ws in it.

The presentation also deals with the ELI portfolio, a group incorporated in the Netherlands and held 48.5% by Redefine Europe. The portfolio is also based in Poland, with a strong slant towards logistics properties.

You can find the full presentation at this link if you want to really dig in.

Steinhoff might be forced by SdK Schutzgemeinschaft der Kapitalanleger to appoint a herstructureringsdeskundige (JSE: SNH)

Spare a thought for business radio presenters everywhere

Reading that sentence will either give you anxiety or make you want to order a beer. Or both.

I’m not going to pretend to be close to the details on this Steinhoff restructuring plan. Frankly, it’s good enough for me that management has said multiple times that the equity is likely worth nothing.

With the group trying to enter into the WHOA Restructuring Plan, it was the shareholders who said “whoa!” in the end. Unsurprisingly, the creditors who stand to receive some value all voted in favour of the plan and the shareholders left out in the cold didn’t.

From my understanding, the potential outcomes are that a court sanctions the WHOA plan regardless of the shareholder vote, or Steinhoff will end up in liquidation.

To celebrate the equity possibly being worth zero in an unexpected way rather than the communicated way, punters drove the share price around 3.8% higher in afternoon trade. No, I still don’t understand why anyone is buying here.

Transcend Residential Property has 97.4% occupancy (JSE: TPF)

People need somewhere to live

The latest results from Transcend Residential Property Fund cover the 15 months to 31 March 2023. The year end was changed, so the year-on-year growth numbers are pointless as we are comparing 15 months to 12 months. To make it worse, the base period had a whole lotta Covid in it.

Instead, I’ll just look at the latest facts, like an occupancy rate of 97.4% and a loan-to-value ratio of 37.1%, which is far more palatable than it used to be. This was achieved through the sale of 425 residential units to raise R390.7 million in cash, which was then used to reduce debt.

The company is taking full advantage of the availability of so-called “green” finance, comprising 68% of the total loan book and offering a rate benefit based on the underlying use of the funds and the ESG metrics.

The distribution per share is 72.34 cents which implies a yield of 11.3%. Again, I would caution that there are three extra months’ worth of profits in that number.

The net asset value per share is R8.40 and the share price is R6.40.

The market didn’t love the Zeda numbers (JSE: ZZD)

Car rental activities are still way below pre-pandemic levels, but the debt is the focus

It was rather interesting to see the Zeda share price come under pressure particularly in afternoon trade after releasing interim results early in the morning. On the face of it, they really didn’t look bad with revenue up 20%, EBITDA up 19% and operating profit up 25%.

Return on equity was up by 590 basis points to 28.3% and net debt to EBITDA improved by 60 basis points to 1.6x.

So, for the six months to March, it’s unlikely that the year-on-year numbers were the cause of concern in the market. I suspect that the balance sheet and the lack of dividend were to blame.

The trouble might be in some of the commentary, which touches on obvious pressures in the market. For example, margin on used cars reduced in the second quarter of the financial year as supply chain issues normalised. This is a worry for the second half of the year, as the used car side of the business is a critical part of the car rental value and leasing value chain. Those cars are eventually sold through the used car retail footprint and online auction platforms, so Zeda needs a robust used car environment.

Zeda owes a big chunk of money to Barloworld based on a loan from its old parent company. Now as a separately listed entity, Zeda’s balance sheet needs to be able to stand on its own feet. Some of the market jitters might be around this debt which is due by the end of the calendar year. Still, Zeda says that the company is on track to settle the debt.

Looking at the car rental business, the huge growth in inbound travel and corporate travel drove increases in revenue of 138.7% and 69.5% respectively vs. the prior period. If you read deeper into the results, you’ll see a comment that total car rental activities are still operating at only 26.8% of pre-pandemic levels. As always, bulls will see this as growth runway and bears will see this as a structural decline in demand.

I’m a bit on the fence with this. I think the adoption of video calling has removed a layer of business travel forever. I also think that the unreliability of Uber in South Africa is a major boost for car rental firms, with so many people on Twitter experiencing horrible service from Uber. I’ve also really struggled to get an Uber at times, which doesn’t build confidence in the platform.

The leasing business is a useful part of the group, helped along by commercial vehicles and the higher interest rate environment that makes it more difficult to buy rather than lease. But with revenue only up by 6% and EBITDA down by 2% in that segment, this could be another area that caused concern in the market.

Interim HEPS was 189 cents per share, up just 4% because of the net interest costs increasing by 56%. There is no interim dividend per share, with the group presumably focused on the debt reduction. The share price slipped below R10 in afternoon trade, so the Price/Earnings multiple looks modest on an annualised basis. It all comes down to the debt.

Little Bites:

Director dealings:

Directors executed small additional purchases of Calgro M3 (JSE: CGR) shares to the value of R14.5k.

Holders of 70.75% of shares in AfroCentric (JSE: ACT) tendered their shares in the offer from Sanlam (JSE: SLM). Each participant can now choose the split between cash and Sanlam shares in line with the circular, with a value of R60 per Sanlam share being used in the formula as the 30-day VWAP came in at R54.

Buka Investments (JSE: BUK) has absolutely no bids and offers in the market, so the trading update only earns a spot in Little Bites. The headline loss per share is expected to be between -25 and -31 cents for the year ended February 2023. The share price is only 73 cents. In case you are wondering where you’ve heard this name before, Buka Investments is what became of the Imbalie Beauty listed shell. I would love to give you a website link but I can’t find one and got tired of looking – the company clearly isn’t bothered about anyone finding information.

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept All”, you consent to the use of ALL the cookies. However, you may visit "Cookie Settings" to provide a controlled consent.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. These cookies ensure basic functionalities and security features of the website, anonymously.

Cookie

Duration

Description

cookielawinfo-checkbox-analytics

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics".

cookielawinfo-checkbox-functional

11 months

The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional".

cookielawinfo-checkbox-necessary

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary".

cookielawinfo-checkbox-others

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other.

cookielawinfo-checkbox-performance

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance".

viewed_cookie_policy

11 months

The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Advertisement cookies are used to provide visitors with relevant ads and marketing campaigns. These cookies track visitors across websites and collect information to provide customized ads.

")

")

")

")