Solid numbers at MAS, but watch that footfall (JSE: MSP)

eCommerce is a trend worth watching

Whenever a retail-focused property fund releases earnings, one of the first things I look at is footfall. The trend is clear across multiple geographies: people aren’t going to malls as often as they used to. In some cases footfall growth is still positive (driven by trends like urbanisation), but not by much. When footfall turns negative, then the only thing driving higher tenant sales will be the average basket size and the extent to which landlords can participate in omnichannel sales that are fulfilled by stores in the mall.

Long-term concerns aside, MAS Real Estate put out solid numbers for the year ended June 2025. With so much focus on the shareholder register and the board recently, it’s great to see that the underlying business is doing well. Distributable earnings per share jumped by 27.7% year-on-year and valuations were up 7.3% on a like-for-like basis. The loan-to-value ratio has improved from 26.3% to 23.2%. It all looks good.

As alluded to when I started this section on MAS, footfall isn’t the major driver of growth here. In the MAS retail portfolio (excluding the DJV joint venture), it was up 3.3% for the full year, but footfall only increased by 0.8% in the second half of the year. That’s a huge deceleration. The good news is that sales per square metre grew 6.9% for the full year and 6.3% in the second half, with higher rent reversions in the second half helping to blunt the impact of lower footfall.

The DJV retail portfolio did a lot better on key metrics, with sales per square metre up by 18.8% on a like-for-like basis and footfall up 4.2% for the full year. Rent reversions were a meaty 24%.

The tangible net asset value per share is 186 euro cents (roughly R38.40 vs. the current share price of R21.00). The market has been more focused on the dividend – or lack thereof – than the capital value recently. With the dust having settled on the shareholder register and with Prime Kapital (the joint venture partner) having given an undertaking to prioritise distributions of available profits over new investments, the hope is that dividends will soon return.

Costs are running too hot at Northam Platinum (JSE: NPH)

And this means that margins have suffered

Northam Platinum has released results for the year to June 2025. Despite a modest production increase in own operations of 0.7%, operating profit has dropped sharply from R4.8 billion to R3.6 billion. Operating profit margin has contracted from 15.7% to 10.9%. That’s clearly a problem.

We can’t even point to a poor sales result to explain this, as sales volumes were up 5.9% and sales revenue increased 6.9%. That really isn’t a bad result, but it wasn’t enough to offset the cost pressures in the group. The cash cost per equivalent refined 4E ounce increased by 8.1%.

If we dig deeper into the operations, Booysendal as the largest operation suffered a 14.4% decline in operating profit to R3.9 billion. This operation also required 11.7% more capex, so that’s quite a squeeze on free cash flow. At Zondereinde, they managed to grow operating profit by 5.5% to R570 million despite a deterioration in the cash margin per refined 4E ounce. Capex was 7.7% lower at Zondereinde, which also helped. Unfortunately, Eland more than offset the good news at Zondereinde. In fact, Eland more than offset Zondereinde full stop, with a 31.3% deterioration in the operating loss to R768 million! To add insult to considerable injury, capex was 31.9% higher at Eland.

Although Northam enjoys significant headroom on its facilities, it’s also worth noting that net debt increased from R3.1 billion to R5.1 billion. The net debt to EBITDA ratio more than doubled from 0.50x to 1.04x.

In terms of guidance for FY26, the unit cash cost per 4E ounce is expected to be between R27,500 and R28,500. The FY25 number was R25,728, so the cost pressure seems to be relentless. Even if PGM prices do well, it all seems very risky to me.

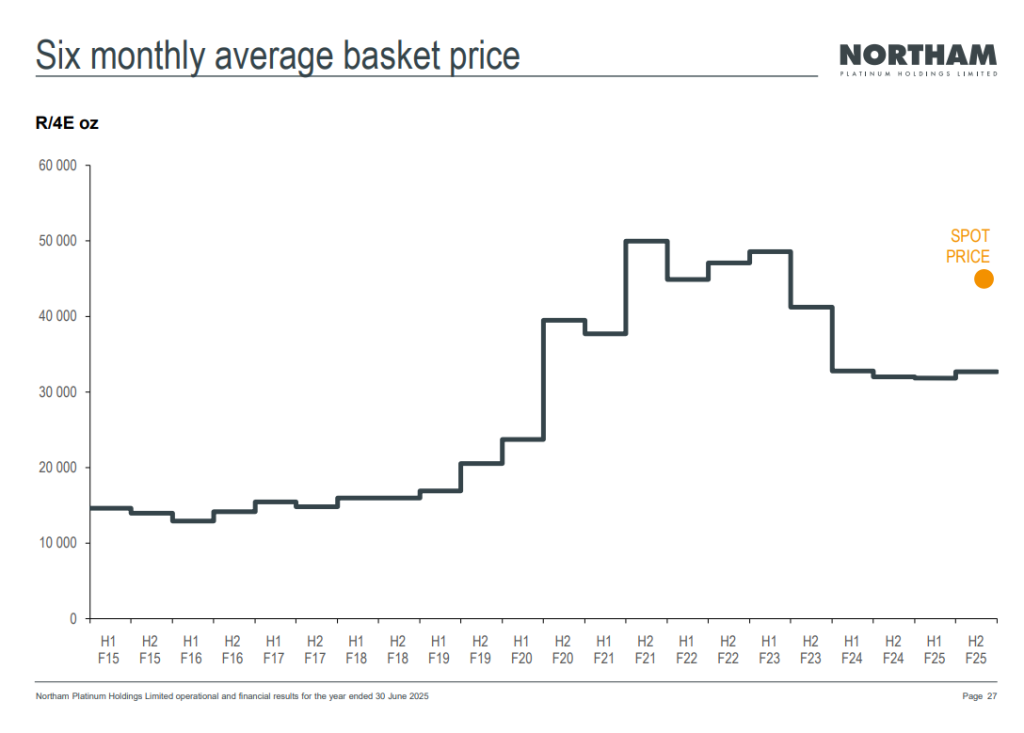

The share price is up 98% year-to-date. It’s cooled off quite a bit though, down 14.5% from its recent 52-week high. To finish off on Northam, I enjoyed this chart in the investor presentation that shows the six monthly average basket price going back over the past decade, along with an indication of where the current spot price is. It shows you why the share price has rallied in anticipation:

Super Group’s continuing operations are struggling for growth (JSE: SPG)

But the balance sheet is in good shape

Super Group released a trading statement for the year ended June 2025. It’s not exactly the easiest time in the world to be running a logistics business with heavy exposure to the European automotive sector, along with an automotive dealerships business that is clearly in that value chain as well.

Despite this, HEPS from continuing operations is expected to move by between -2.3% and 0.0%. They might be in the red, but not by much. This excludes the results of SG Fleet (which was disposed of), inTime (in the process of being disposed of) and the Suzuki, Kia and Hyundai dealerships in the UK (I can’t find any evidence of an announced transaction for this – happy to be corrected if wrong).

If you look at total operations instead of continuing operations, HEPS was up by between 24% and 28%.

Super Group notes that the balance sheet is strong, with debt leverages at “modest” levels and plenty of headroom on their borrowings covenants i.e. the ability to access capital if needed. We will find out for sure on 9 September when Super Group is expected to release earnings.

Nibbles:

Director dealings:

A director of Sabvest (JSE: SBP) bought shares in the company worth R7.3 million.

An associate of a director of 4Sight Holdings (JSE: 4SI) bought shares worth R1.4 million.

Des de Beer bought another R1.06 million worth of shares in Lighthouse Properties (JSE: LTE).

An associate of a director of KAP (JSE: KAP) bought shares worth R995k.

A director of STADIO (JSE: SDO) bought shares worth R298k and a different director bought shares worth R108k.

A director and an associate of the same director bought shares in Finbond (JSE: FGL) worth R118k.

A director of Vunani (JSE: VUN) bought shares worth R3.7k.

Accelerate Property Fund (JSE: APF) has suffered a delay in the release of the circular for the all-important Portside disposal. The JSE has granted an extension for the release of that circular until 15 October 2025. They really need to get that deal done to remove one of the many overhangs on the share price.

In mid-July, AECI (JSE: AFE) announced the disposal of Schirm USA. The good news is that the deal has become unconditional and has been implemented, with $40 million in proceeds flowing to AECI. The group is executing a strategy that includes focusing on AECI Mining and AECI Chemicals, while divesting from any distractions.

Shareholders in eMedia Holdings (JSE: EMH) gave almost unanimous approval for all the resolutions required for the transaction with Remgro (JSE: REM). I’m not surprised, as it seems like a solid deal for eMedia.

Sebata Holdings (JSE: SEB) did not release the results for the year ended March 2025 as expected on 29 August. They have unfortunately not even given an indication of when the results might come out, due to delays in the technical review in the audit of Inzalo Capital Holdings.

Salungano Group (JSE: SLG) announced that the board can no longer stand behind the previous guidance that the listing suspension will be lifted in mid-November. Due to ongoing delays in financial reporting, they can’t even give an updated timeline at this point.

Note: Ghost Bites is my journal of each day’s news on SENS. It reflects my own opinions and analysis and should only be one part of your research process. Nothing you read here is financial advice. E&OE.Disclaimer.

Coney Island had its peep shows, its freak shows, its barkers and rides. And tucked between them was an exhibit of premature infants in glass boxes, tended by trained nurses. This wasn’t entertainment – it was the beginning of modern neonatal care, smuggled in as a carnival act.

On a warm summer’s day in the early 1900s, the boardwalk at Coney Island was alive with noise and colour. Barkers shouted promises of firebreathers, snake charmers, and the world’s smallest horse. Music drifted from carousels, mingling with the smell of popcorn and salt air. Families came for spectacle, and spectacle is what they got.

But tucked between the sideshows and the thrill rides was a very different kind of attraction. Inside a pristine white pavilion, for the price of 25 cents, visitors could step into what was called The Infantorium. There, behind glass doors, tiny premature babies lay in metal incubators, tended by uniformed nurses. Some weighed barely one kilogram. Many had been declared hopeless by hospitals. Yet here they were – breathing, growing, and clinging to life.

The man behind this improbable exhibit was Martin Arthur Couney. To the public, he was the Incubator Doctor, a pioneer who brought medical technology out of hospitals and into amusement parks. To the medical establishment, he was something closer to a charlatan – mysterious in background, evasive about his qualifications, and far too willing to place fragile infants on public display.

And yet, over the course of four decades, Couney’s incubator sideshows saved thousands of lives.

The man who invented himself

Couney’s own story was as much a performance as the ones he staged. Born Michael Cohen in Germany in 1869, he later reinvented himself as Martin Couney and claimed a background that changed depending on the telling. Sometimes he said he had studied medicine in Leipzig or Berlin. Other times he insisted he had apprenticed under Pierre-Constant Budin, the French obstetrician credited as a father of modern perinatal medicine.

The record tells a murkier tale. For starters, there is no evidence that he ever earned a medical degree. Some reports suggest he emigrated to the United States as early as 1888, which would make his claims of extensive European training difficult to reconcile. Still, whether through apprenticeship or sheer force of will, he absorbed enough knowledge to talk convincingly about neonatal care. More importantly, he understood something that few in the medical profession grasped at the time: premature infants were not necessarily doomed, and the incubator might offer them a chance.

From chicken coops to child hatcheries

The incubator, by the time Couney discovered it, was not a new idea. Farmers had long used heated boxes to hatch chickens, and in the late 19th century, French physicians began adapting the idea for infants born too soon. One of them, Stéphane Tarnier, introduced a version that maintained a warm, regulated environment, while his assistant Budin (yes, the same Budin that Couney claimed to have studied under) refined the design further.

But the medical establishment was sceptical. Incubators were expensive, untested, and to many doctors, the effort seemed wasted on babies they believed were too weak to survive.

Couney thought differently. In 1896, he arranged to display Budin’s “child hatchery” at the Berlin Industrial Exposition. The public reaction was astonishing. Crowds flocked to see the tiny infants in their glass-fronted boxes. For many, it was the first time they had encountered a premature baby who had a chance of survival. Couney realised that spectacle could serve as persuasion. If doctors would not yet embrace the incubator, perhaps the public would.

A sideshow with a serious purpose

When Couney brought his incubator shows to the United States, he leaned fully into the pageantry. His exhibits travelled from one world fair to another before finding permanent homes at Coney Island and Atlantic City. The branding varied – sometimes “The Infantorium,” sometimes “Baby Incubators” – but the concept was the same. Visitors paid admission, nurses cared for the infants around the clock, and the curious filed past the glass cases in droves.

It was, in one sense, theatre. Nurses were encouraged to lift the babies out and cuddle them in view of the crowd. Posters declared, “All the world loves a baby.” But behind the theatrics was a sophisticated operation. The incubators were carefully engineered, warmed by boilers that circulated hot water through pipes beneath the infants’ cribs, with thermostats to regulate the temperature. Air was filtered twice, first through wool soaked in antiseptic, then through dry wool again before entering the chamber. Every effort was made to reduce contamination and maintain cleanliness.

As you can imagine, the costs were enormous. Round-the-clock feeding, equipment, and nursing care added up to more than most families could dream of affording. In 1903, Couney estimated that caring for one premature baby cost $15 a day, or roughly $400 in today’s terms. Yet he never asked parents to pay. The entrance fees, morally questionable as they were, funded the entire operation.

Critics and controversies

Not everyone was impressed. From the beginning, medical journals questioned Couney’s motives. The Lancet described the practice as an “unscrupulous way to make money”. Child welfare groups accused him of objectifying infants, treating them as exhibits rather than patients. The very location of his shows – wedged between animal acts and risqué peep shows – seemed to confirm the charge.

The 1911 Coney Island fire deepened the criticism. Though every infant was rescued, the idea that fragile lives had been placed in danger within a theme park struck many as irresponsible. Others pointed to the proliferation of imitation incubator shows, often poorly run and unsanitary, which further tarnished the concept.

And yet, for all the controversy, Couney’s results spoke loudly. His survival rates were significantly higher than those of hospitals that admitted premature infants. Parents who had been told to prepare for funerals instead brought home children who thrived.

A quiet defiance of eugenics

What made Couney’s work even more radical was the cultural climate in which he operated. The early 20th century was the height of the eugenics movement in America, a time when many in the medical community openly questioned whether premature babies should be saved at all. Eugenics exhibits, sometimes set up on the very same fairgrounds, celebrated the “fittest” families and promoted slogans like “Kill defectives, save the nation”.

To save premature infants was, in that worldview, to preserve weakness and to give it a chance to spread to future generations. Couney rejected the premise entirely. He insisted that given care and time, these children could survive and flourish. Every incubator he placed on display was not only a medical intervention but also a public argument against a brutal ideology.

The long arc of recognition

Couney spent decades travelling from fair to fair, and when he finally settled his operations permanently at Coney Island and Atlantic City, his shows ran year after year. Behind the glass, thousands of premature infants passed through his care. By his own reckoning, he and his nurses saved more than 6,500 lives.

Yet even as he racked up successes, Couney remained an outsider. Hospitals refused his offers to donate incubators when his shows closed. The medical establishment continued to view him with suspicion, partly because of his uncertain credentials, partly because of his unorthodox methods.

It was only in the years after his death in 1950 that his reputation shifted. By then, incubators had become standard equipment in neonatal units. Hospitals were doing what Couney had been doing for decades, though now with institutional legitimacy and without the carnival bunting.

The legacy of the Incubator Doctor

Couney’s life remains wrapped in mystery. We may never know the full truth of his training, or whether he embellished his past to protect his credibility. But what is clear is the scale of his impact. In an era when premature babies were dismissed as unfit to live, he proved otherwise.

His shows were at once bizarre and humane, a mixture of spectacle and science that unsettled many but comforted those who mattered most: the parents who watched their children grow stronger inside those heated glass boxes.

Today, neonatal intensive care is one of the most advanced branches of medicine, with technologies that would have looked like science fiction in Couney’s day. But the principle is the same – the belief that even the smallest, frailest infants deserve a chance.

That conviction, once dismissed as quackery, began its long march to acceptance not in the corridors of hospitals, but in the carnival pavilions of Coney Island.

About the author: Dominique Olivier

Dominique Olivier is the founder of human.writer, where she uses her love of storytelling and ideation to help brands solve problems.

She is a weekly columnist in Ghost Mail and collaborates with The Finance Ghost on Ghost Mail Weekender, a Sunday publication designed to help you be more interesting.She now also writes a regular column for Daily Maverick.

Altron flags a flat interim performance (JSE: AEL)

The market didn’t love it

Altron’s share price dropped 10% on Thursday based on a voluntary update that indicates a flat revenue and EBITDA performance for the six months to August 2025. They’ve noted a tougher operating environment with tight IT budgets.

Of course, a flat group performance doesn’t mean that there aren’t big swings at segmental level. The Platforms segment achieved double-digit revenue growth (which naturally means solid EBITDA growth as well), while the IT Services segment bore the brunt of the trickier environment. The Distribution segment has also had a tough time.

Full details will be available when interim results are released on 3 November.

Equites Property Fund remains committed to shifting capital from the UK to SA (JSE: EQU)

The loan-to-value ratio is expected to drop sharply thanks to disposals

Equites released a pre-close update that deals with the six months ending August 2025. They’ve used it as an opportunity to remind the market that the plan is to sell off the UK portfolio and allocate the capital to South Africa instead. How times have changed in the past decade in the property sector!

The UK portfolio seems to be in decent shape at the moment, which would support an exit on reasonable terms. In South Africa, the appeal is that there’s limited availability of large land that is suitable for logistics hubs, hence the desire by Equites to get moving on its land parcel for development. It’s been an expensive four years of development (peaking at over R2.5 billion in 2024) and they expect it to settle at R1 billion in FY26.

The loan-to-value ratio is estimated to be 37.9% at the end of this interim period. Thanks to the extensive disposals, they expect it to drop to 24.3% by the end of the 2026 financial year. Other important guidance is that they expect the distribution per share to increase by between 5% and 7% for the year.

Harmony has its heart set on copper, but they need to maximise the gold opportunity (JSE: HAR)

Gold production in FY26 is still expected to be below FY24 levels

Harmony Gold may have gold in the name, but they are definitely splitting their love across two commodities at the moment. They expect to conclude the MAC Copper acquisition in October as part of their diversification plan.

Of course, if gold wasn’t shooting the lights out at the moment, the market would probably be more enamoured with the copper strategy. Instead, we have a situation where Harmony is lagging its peers due to gold production that dipped by 5% year-on-year at a time when the gold price has dished up a huge opportunity. Just because they are “within guidance” doesn’t mean that investors are happy.

Here’s the bigger frustration: production guidance for FY26 is between 1,400,000 and 1,500,000 ounces. That’s not encouraging vs. FY25 at 1,479,671 ounces. It’s also well below the FY24 number of 1,561,815 ounces, so things are going backwards.

Unfortunately, the drop in production has been accompanied by a substantial increase in all-in sustaining costs (AISC) of 17%. Again, that’s in line with guidance, but that doesn’t make it good. Guidance for FY26 is AISC of between R1,150,000/kg and R1,220,000/kg, another significant increase vs. FY25 at R1,054,346/kg.

Despite major metrics going the wrong way in FY25, HEPS increased by 26% thanks to the one thing that Harmony cannot control: the gold price. Based on the guidance for FY26, they will need the gold price to keep shining brightly next year.

FY25 was a year to forget for Impala Platinum (JSE: IMP)

PGM prices were flat for the year ended June, with hopes of better times to come

As I’ve written many times in Ghost Bites, the PGM sector rally has been firmly forward-looking rather than based on the performance over the past year. Impala Platinum is further proof of that, with ugly numbers for the year ended June 2025 that saw revenue dip by 1.1% and EBITDA fall by 19.8%. HEPS was down by 69.5%.

The reason for the financial pain was a small dip in sales volumes at a time when the rand price per 6E ounce was flat. Mining costs certainly don’t sit still, so a year in which revenue goes nowhere means a period of margin compression.

The silver lining was the cash, with a major swing into positive free cash flow and even the declaration of a dividend of 165 cents per share (more than double HEPS for the year). Impala’s dividend policy is based on free cash flow.

The outlook for FY26 is growth in unit costs of between 4% and 9%. They expect saleable production of between 3.4 and 3.6 million ounces, which implies decent growth on the FY25 number of 3.37 million ounces. But of course, what they really need is for the PGM price to behave itself.

Nothing ever seems to get better for KAP investors (JSE: KAP)

The share price is way down this year and so are the earnings

KAP has released financials for the year ended June 2025. They aren’t good, with revenue down 2%, operating profit down 14% and HEPS nosediving 47%. Unsurprisingly, there’s no dividend.

Concerningly, it seems like the fourth quarter had the worst operating conditions of the year, which means negative momentum going into the new financial year.

The ramp-up of the new MDF line at PG Bison is absolutely key to getting the numbers into the green, with revenue up 10% and operating profit down by a nasty 28% in that business. Operating margin has fallen sharply from 17.4% to 11.3%. Sadly, margins are expected to be below historical levels in the near term, with market conditions making it difficult to optimise this investment.

Elsewhere, Safripol grew revenue by 4% and operating profit by 43%. Operating margin in that business increased from 3.8% to 5.2%, which is still a paper thin margin. At Unitrans, revenue fell 4% and operating profit was down 14%, a good example of operating margins going the wrong way. Feltex is a particularly nasty story in the OEM automotive value chain, with revenue down 8% and operating profit down 37% due to lower volumes and non-recurring costs related to a model changeover. Sleep Group went the right way at least, with revenue up 7% and operating profit up 27% thanks to improved mix. Finally, Optix remains a mess, with revenue up just 1% and an operating loss of R44 million – you definitely can’t scale into profitability with a growth rate of 1%!

KAP just never seems to catch a break.

Positive momentum at Libstar – at last (JSE: LBR)

I’ve certainly done my part in boosting cheese sales

Libstar has been a disappointing story in our market. The FMCG company has lost around 65% of its value since listing in 2018. Like so many consumer businesses in South Africa, things just haven’t worked out as planned.

The good news is that the six months to June 2025 reflect solid positive momentum in the business. If they can keep this up, then things could get very interesting for punters – as evidenced by the share price being up 14% in the past month.

For the six months, HEPS will be up by between 15.1% and 25.2%. Normalised HEPS from continuing operations will be up by between 10.4% and 20.4%. Much like a slice of their cheese, whichever way you cut it, that’s still yummy.

Metrofile’s earnings have dropped, but a potential deal is still on the table (JSE: MFL)

So, the usual story then

If you threw darts at a timeline in recent years, chances are good that you would hit a spot where (1) Metrofile’s earnings are under pressure, and (2) someone is considering an offer for the company. The latest period is no different.

For the year ended June 2025, a trading statement tells us that Metrofile expects HEPS to drop by between 12% and 27%. Ouch.

Luckily, a Delaware-based company is still serious about making an offer, with discussions at an “advanced stage” – although the timeline has been extended based on engagements with regulators.

The share price is up 20% year-to-date and a whopping 106% over six months. This has everything to do with the potential offer and nothing to do with the underlying earnings, that’s for sure.

A pot of gold at Rainbow Chicken – and yes, even a dividend (JSE: RBO)

The volatility in chicken earnings remains breathtaking

If you follow the poultry sector, you’ll know that modest changes in revenue can drive substantial moves in profits. This is because of the operating leverage inherent in the model, as well as the structurally low operating margins that are impacted by modest moves in e.g. gross margin.

What does this look like in practice? Rainbow Chicken’s numbers for the year to June 2025 reflect growth in revenue of 9% and a move in EBITDA margin from 4.4% to 6.7%. By the time you get to HEPS, you find an insane jump of 224%!

Such is the improvement in this sector that there’s even a dividend of 20 cents per share (vs. HEPS of 65.57 cents).

I must remind you that it doesn’t take much for earnings in this sector to very quickly head the other way, so tread carefully. Personally, I prefer to eat chicken rather than invest in it.

Gold and US PGMs gave Sibanye-Stillwater’s earnings a huge boost (JSE: SSW)

There’s a 19-fold increase in headline earnings!

For a long time, I considered myself a bit unlucky in Sibanye. I watched my stake sit in the red for ages, which is unfortunately a feature rather than a bug when it comes to cyclical stocks. Still, the PGM market felt like it took forever to get going.

But where I got extremely lucky was in my decision to take the money and run a month ago. It’s rare in life that you genuinely sell at the top of a chart, so I’ll take the wins where I can. The negative momentum over the past month has been pretty rough, with the share price having dropped by 20% in just a few weeks:

If you think the share price is volatile, wait until you see the earnings. Sibanye released results for the six months to June 2025 and they reflect headline earnings that have gone to the moon, up 19 fold vs. the prior year!

I always skip straight to the segmental reporting to see where the big moves were. The biggest contributor in this period was South African gold, with adjusted EBITDA more than doubling from R2.2 billion to R4.8 billion. That’s only slightly more than South African PGMs, with remarkably consistent adjusted EBITDA of R4.78 billion. So, that’s a strong performance locally.

Looking abroad, the big win was in US PGMs, with both the underground and recycling operations experiencing a huge positive move in earnings. If you add them together, adjusted EBITDA jumped from R635 million to R5.15 billion. A special mention must also go to zinc for an adjusted EBITDA turnaround from a loss of R351 million to profit of R657 million. The remaining ugly duckling is lithium, with a loss of R310 million that is even higher than the loss of R280 million in the comparable period.

Unfortunately, Trump’s One Big Beautiful Bill Act means that the big beautiful S45X10 credits that Sibanye enjoys on PGMs in the US will be phased out between 2031 and 2034. That may sound far away, but mining is a long-term game. This legislative change has driven an impairment of R3.8 billion to Sibanye’s PGM operations.

I must note that there’s an even larger impairment of R5.3 billion to the Keliber lithium project, based on changes to forecast lithium prices. Due to Sibanye’s efforts to have its fingers in many pies, in some cases in contrasting strategies (PGMs vs. battery technology), chances are that some parts of the group are doing well and others are in trouble at any point in time.

Overall though, the group is in a much better place than before. They are taking advantage of the improved market conditions and they are telling a bullish story around cash generation heading into 2026.

A strong year for South32 (JSE: S32)

Revenue and profits both came in significantly higher

South32 has released results for the year ended June 2025. Revenue from continuing operations was up 17% and the ordinary dividend increased by 71%, so there’s plenty for investors to smile about. Diluted HEPS was 91% higher

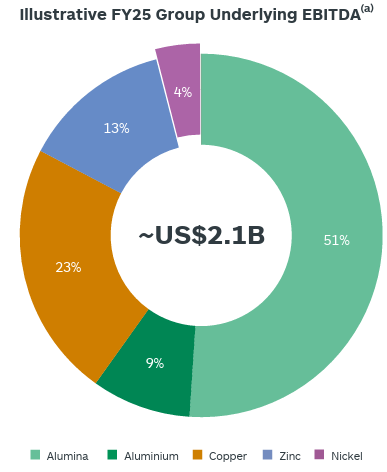

The results presentation includes this handy chart that shows how the group made its money in FY25, adjusted for the disposal of Illawarra Metallurgical Coal, the impact of a cyclone on manganese in Australia and a few other bits and pieces:

This gives you a really useful lay of the land. It also shows you just how important alumina and aluminium is to the group. Thankfully, Mozal Aluminium (which is likely to stop producing after March 2026 based on energy availability) is just one part of the group. It contributed 355kt of the total 671kt of aluminium in FY25, so it’s big enough to be an annoying drag on earnings, but definitely not big enough to cause a major issue all by itself.

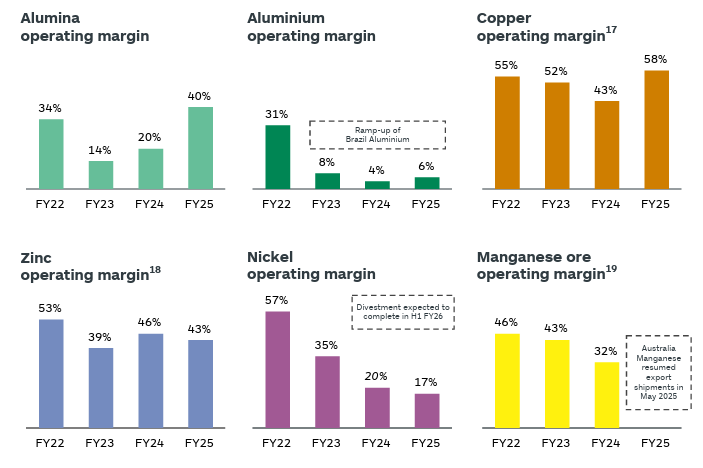

Another interesting view is to see just how different the margins are across these commodities, as shown in these charts:

When people talk about the “mix effect” in margin, this is what they mean. As revenue changes across the underlying businesses, group margins shift based on the changing mix of revenue. The effect is less noticeable in groups with more consistent margins across the segments.

Overall, South32 is telling a bullish story as they head into a new financial year, with significant focus on Worsley Alumina as major growth capex project.

Excellent growth at STADIO shows that tertiary education is firmly a for-profit business (JSE: SDO)

Student growth is expected to remain strong

STADIO has released results for the six months to June 2025. They are really good, with student numbers up 9% in semester 1 and revenue growth of 16%. A mix of price and volumes growth is exactly what investors want to see, along with cost control that has led to a 24% jump in EBITDA. By the time you reach the bottom of the income statement, you’ll find a 28% increase in core HEPS.

With almost 55,000 students currently in the group, they reckon they can reach 80,000 students by 2030. Thanks to having multiple tertiary offerings in the group, I certainly wouldn’t bet against them achieving that target.

STADIO’s share price has tripled in the past 3 years. The underlying growth in tertiary education has certainly helped, but they still needed to deliver on the opportunity.

Have we reached the bottom for Trellidor? (JSE: TRL)

Hopefully the latest financial year is the end of the slide– but the UK is a worry

Trellidor has confirmed that the sale of Taylor Blinds and NMC became effective on 25 August 2025. The final price (after balance sheet adjustments) was R51.9 million. The good news is that a portion of this price will go towards further debt reductions, with the group having made excellent progress in reducing net debt from R146.7 million as at June 2023 to R85.3 million as at December 2024. Based on those dates, you can see that they’ve been in trouble for a while.

Is the pain over yet? Maybe, maybe not. A trading statement dealing with the year ended June 2025 shows us that HEPS will drop by between -5% and -15%, coming in at between 30.6 cents and 34.21 cents. The Trellidor UK division has been a disappointment in this period, which is a worry given the ongoing poor performance of the South African business.

The current share price of R1.92 means a Price/Earnings multiple of mid-single digits. Given the recent track record and now the concern around the UK, I still wouldn’t call that a bargain. Things might get worse for this share price, as evidenced by it closing 11% lower on the day of this announcement on strong volumes.

Is there a worse retailer in South Africa than Truworths? (JSE: TRU)

Sometimes, shares are cheap for a reason

There are some really innovative and interesting retailers in South Africa. Truworths definitely isn’t one of them. About the only positive thing I can say is that they aren’t losing money offshore like some competitors are doing. Office UK grew revenue by 9% in the year ended June 2025. But even with that revenue growth, trading profit (if you adjust for a major once-off in the base) was basically flat.

“Flat” is more than we can say for Truworths Africa, still the biggest contributor to trading profit in the group but not for long at this rate. Revenue went nowhere in this period and trading profit fell by around 16%.

Add these two segments together into a group result and you’ll find sales up by 3.2%, gross margin down 100 basis points to 41.3% and operating margin down 730 basis points to 20%. HEPS dropped by just over 8% to 752.1 cents and the dividend followed suit.

Any highlights? Well, the balance sheet is in a net cash position rather than net debt, but this can often just be due to the timing of working capital movements for retailers.

Truworths is trading on a Price/Earnings multiple of 8x. In my view, that’s still much too high. This is probably the last name I would own in this sector.

Nibbles:

Director dealings:

Associates of two director of Renergen (JSE: REN) – including the CEO) sold shares worth R7.8 million.

The CEO of Grindrod (JSE: GND) – who is shortly leaving the group – sold share awards worth R4.4 million. The announcement isn’t explicit on whether this is the taxable portion or not.

A director of a major subsidiary of Sasol (JSE: SOL) sold shares worth R501k.

A director of a major subsidiary of PBT Group (JSE: PBG) bought shares in the company worth almost R80k.

An associate of the CEO of Acsion (JSE: ACS) bought shares worth R42k.

The CEO of Vunani (JSE: VUN) is still on the bid, buying R2k worth of shares in an illiquid market for the stock.

Frontier Transport (JSE: FTH) announced that CFO Mark Wilkin will be retiring with effect from August 2025, after roughly four decades with the company! He’s replaced by Ulandy Gribble, who is currently in charge of the numbers at Golden Arrow Bus Services (the largest subsidiary). It’s always good to see an internal succession plan playing out.

Randgold & Exploration Company (JSE: RNG) released results for the six months to June 2025. This is a tiny listed company, so it just gets a passing mention here. The operating loss improved by 24% to R8.3 million (but that’s still a loss obviously) and the headline loss per share was 8.80 cents.

Note: Ghost Bites is my journal of each day’s news on SENS. It reflects my own opinions and analysis and should only be one part of your research process. Nothing you read here is financial advice. E&OE.Disclaimer.

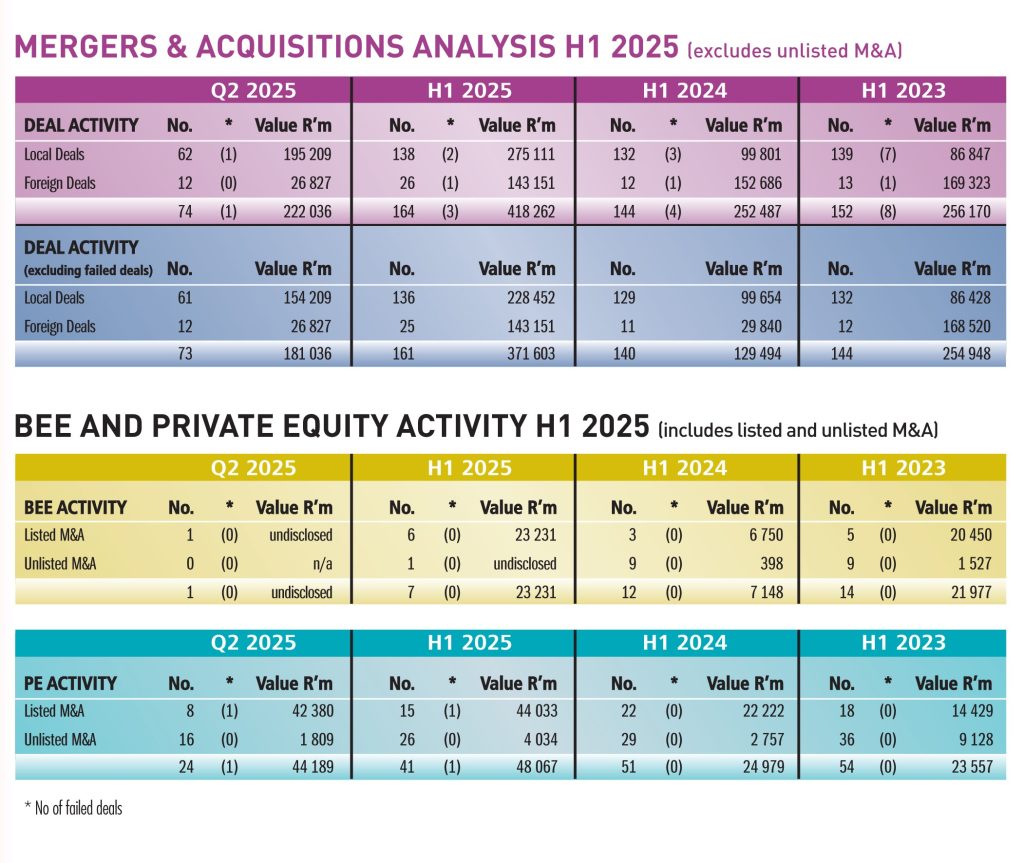

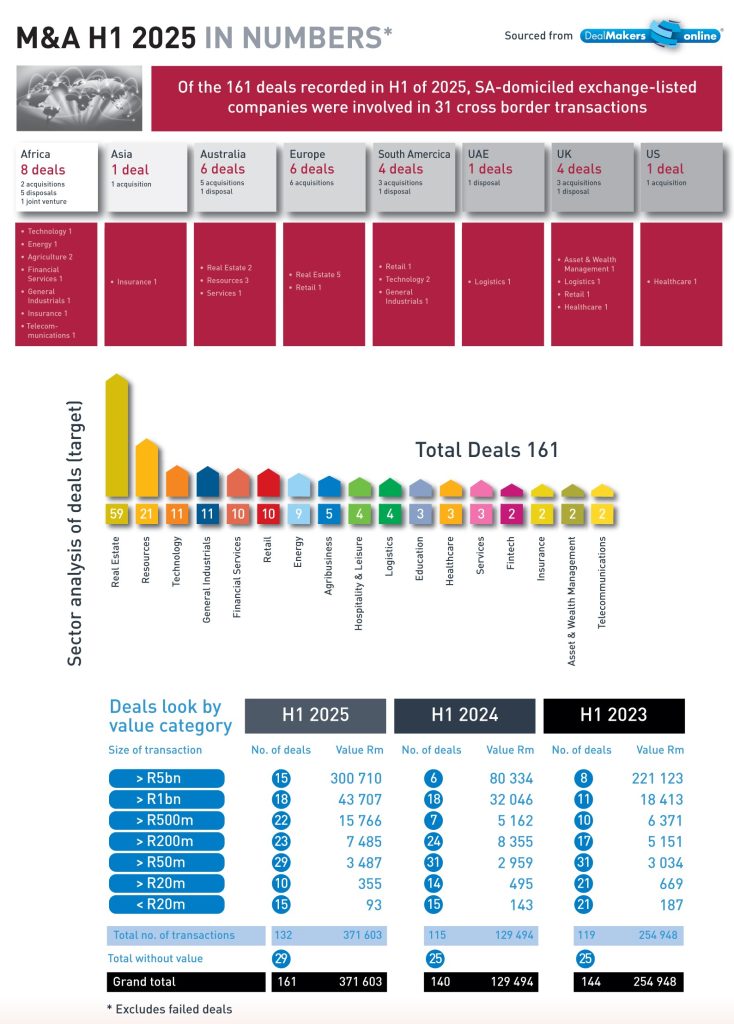

Global uncertainty and local budget-related wrangles still weigh on confidence and demand in South Africa. Yet, higher commodity prices and market volatility created opportunities. M&A activity by value of SA-listed companies rose 66% in H1 2025 compared with the prior year, and DealMakers recorded 164 deals worth R418,3bn.

Source: DealMakers Online

Excluding failed transactions, the real estate sector led activity (37%), followed by resources (13%), technology (7%), and industrial and manufacturing (7%) – broadly mirroring last year’s trends.

The top 10 deals by value reflected this pattern, with resources and real estate dominating. Highlights included Gold Fields’ acquisition of Gold Road Resources (A$3,7bn|R43,7bn) and Primary Health Properties’ acquisition of Assura (£1,79bn|R43,3bn).

Excluding deals by foreign companies with secondary listings in South Africa, deal value for H1 2025 more than doubled to R228,5bn. SA-domiciled, exchange-listed companies were involved in 31 cross-border transactions during the period, with Africa, Australia and Europe the most active destinations. Once again, real estate deals topped the list, followed by technology.

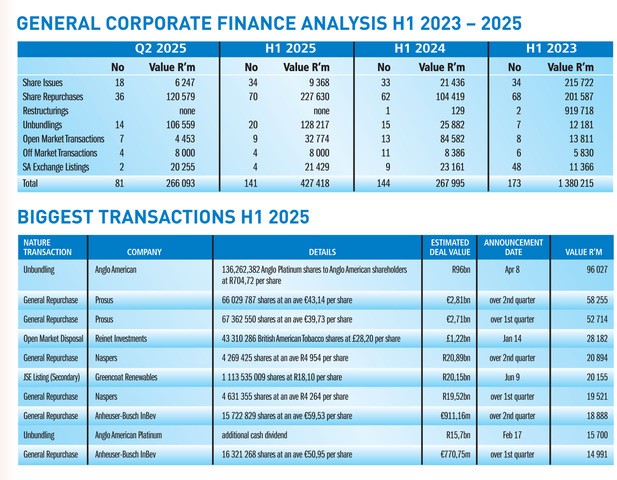

Despite increased opportunities, many companies remain cautious, holding cash yet to be deployed. Instead, firms have turned to multi-billion rand share buyback programmes and special distributions to reward shareholders.

Source: DealMakers Online

The scale of this shift is striking:

In H1 2010, repurchases accounted for 10% of General Corporate Finance (GCF) activity and just 2% of aggregate transaction value.

By H1 2020, in the midst of the COVID-19 pandemic, they had risen to 33% of activity and 10% of value.

Fast forward to H1 2025, repurchases dominated, representing 50% of GCF transactions and value (R227,5bn). Together with special and capital reduction distributions (R30,4bn), companies returned R258bn to shareholders in the period.

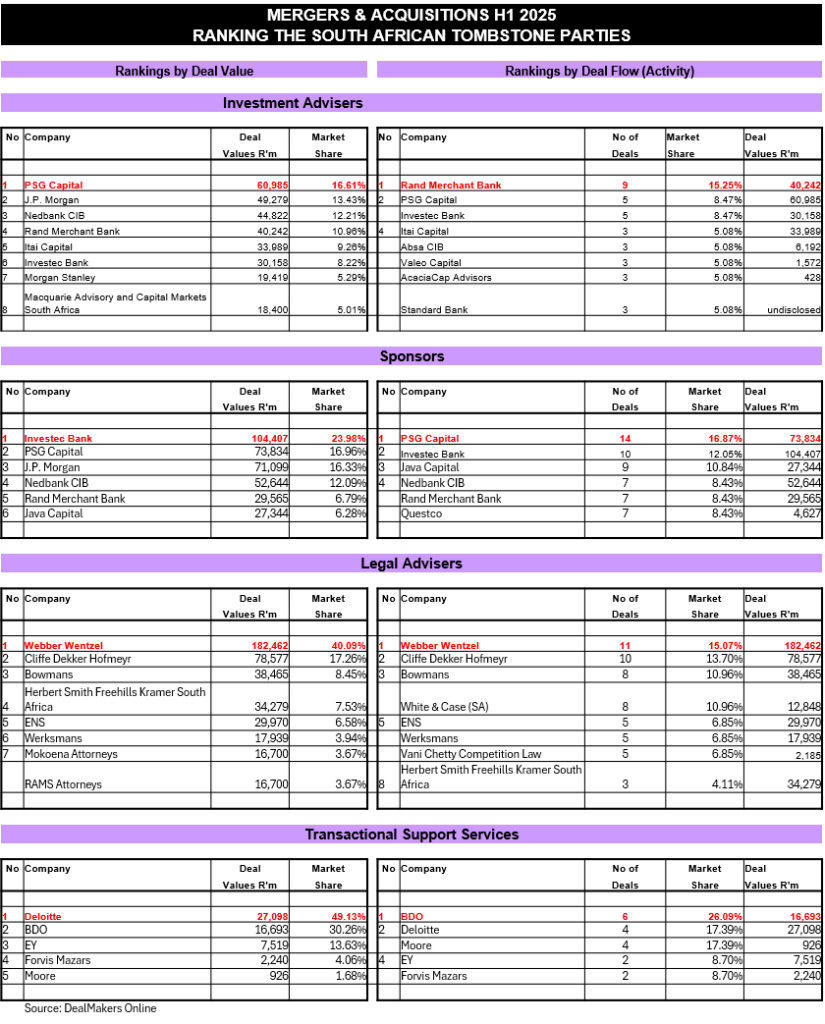

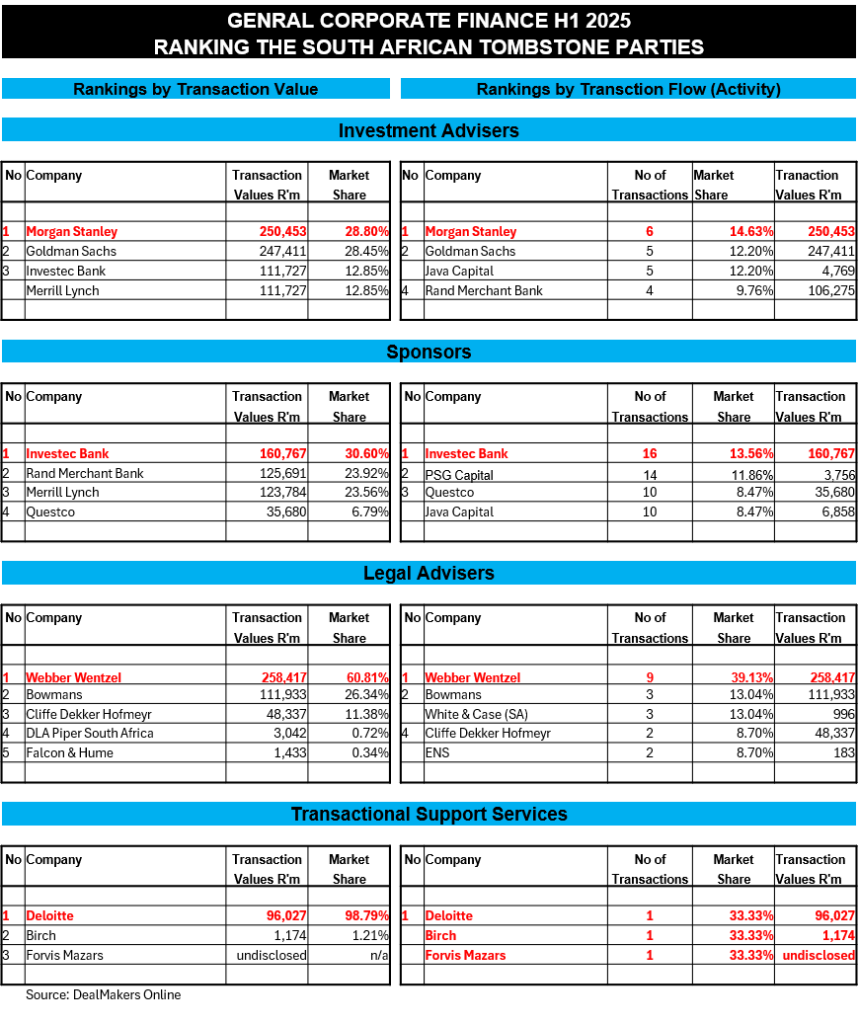

DealMakers H1 2025 League Table – M&A activity by the top South African advisory firms (in relation to exchange-listed companies).

DealMakers H1 2025 League Table – General Corporate Finance activity by the top South African advisory firms (in relation to exchange-listed companies).

DealMakers is SA’s M&A publication.

The latest magazine can be accessed as a free-to-read publication on the DealMakers’ website www.dealmakerssouthafrica.com

The deal grabbing the headlines this week is the proposed R7,2 billion acquisition of private schools group Curro by the Jannie Mouton Foundation (JMF). The delisting of the company and its reincorporation as a non-profit organisation would give it the flexibility to reinvest all profits by expanding its bursary programme and building schools in rural and lower-income areas. JMF which already holds a 3.36% stake has offered shareholders an equivalent of R13 per share – a 60% premium to the share price prior to the announcement. The R13 settlement is in the form of cash and a combination of shares in Capitec, and PSG Financial Services. While the deal will certainly redefine private education, public opinion as to the reason for the deal varies, ranging from an act of philanthropy to the need to adjust the current model, away from the shareholder spotlight, in response to the decline in demand for private schooling.

Rex Trueform has acquired a further 21% equity interest in Byte Orbit from majority shareholder A Ramdath for a purchase consideration of R21 million. The price tag will be settled through the issue of 1,69 million new N shares at R12.39 per share. Rex Trueform acquired its initial 30.2% investment in Byte Orbit in December 2024 for R21 million.

Continuing with its strategic repositioning and restructuring programme, Accelerate Property Fund has announced the sale of the Buzz and the Waterford Centre. The properties, located in Fourways in Gauteng, were disposed of to Dorpstraat Capital growth Fund (owned by Dorpstraat Property Investments, Rabie Property Group, Nedbank Property Partners and Alpha Plus) and Property House Group Investments (ultimate holders being the Wimson Trust and the Gray Trust) for an aggregate consideration of R215 million. The disposal yield is 9.5% after taking into account the agreed exit of Pick n Pay as the anchor tenant at the Buzz.

Delta Property Fund is to sell the Parkmore property situated at 142-144 Fourth Street in a category 2 transaction. Afrocentric Intellectual Property will pay R19 million in cash for the property. The sale is part of Delta’s business and portfolio optimisation strategy and proceeds will be used to reduce its debt balance.

Mahube Infrastructure has cautioned its shareholders that it has received a proposal from a third party in relation to proposed acquisition of all the issued ordinary shares in the company, excluding certain shareholders, leading to the delisting of Malhube. Further details will be provided to shareholders in due course.

Metrofile has advised that the company is still in discussions with Main Street 2093, a special purpose company through which the potential transaction will be implemented. While talks remain at an advanced stage, the company says the timeline has been extended due to regulatory engagements.

Shareholders have approved the disposal by Jubilee of the South African Chrome and PGM Operations to One Chrome announced in June for a disposal consideration of US$90 million (c. R1,59 billion).

Mantengu Mining has finalised the disposal of 30% of its shareholding in Blue Ridge Platinum (BRP) to BEE parties – a condition of the deal announced in October 2024 which saw Mantengu acquire BRP from Ridge Mining owned Sibanye-Stillwater and Imbani Platinum SPV (50%-owned by Entrepreneurs Business Group). The 30% stake was disposed of for R1.00 to the BEE consortium, represented by Vitai Resources (20%), the BRP Mine Employee Trust (5%) and the BRP Mine Community Trust (5%).

The scheduled general meeting of Ayo Technology Solution shareholders of 20 August 2025, to vote on the scheme offer by Sekunjalo Investment and delisting of the company, has been postponed a month at the request of the Public Investment Corporation. The institution requires additional time to adequately assess the merits and risks associated with holding shares in a delisted entity. Should shareholders vote in favour of the scheme, Ayo’s listing will terminate on 28 October 2025.

Unlisted Companies

Norwegian development finance institution Norfund and South African fund Infra Impact will, in partnership, invest in Green Create, a waste-to-value group with operations in South Africa and Mauritius. Green Create facilities treat both effluent wastewater as well as agricultural waste, reducing the load on the downstream municipal water treatment infrastructure as well as landfilling and generate biogas that can replace fossil fuels in industrial processes.

In terms of the revised offer to Assura plc shareholders by Primary Health Properties plc (PHP), a further 292,922,357 new PHP shares listed this week. The revised offer remains open for acceptances until 13h00 on 10 September 2025. As at 27 August 2025, PHP had received acceptances in respect of c.92.02% of the issued share capital of Assura.

Fairvest has successful completed a capital raise of R976,7 million via an accelerated bookbuild. Fairvest will issue 180,872,707 new B shares at a price of 540 cents per share – a 2.28% discount to the 30-day VWAP of 553 cents per share. Initially the company proposed to raise capital of c.R400 million but increased the raise on strong demand. The proceeds will be used for acquisitions, investments and the reduction of debt.

MTN Zakhele Futhi (MTNZF) has disposed of the last tranche of its MTN shares. The 2,476,448 MTN shares were disposed of in the open market over the period 18 to 20 August 2025 raising an aggregate R391 million after costs. The unwind of the MTNZF scheme will now be finalised – following the sale of the last MTN shares held, MTNZF’s NAV is c.R494 million (R4.00 per share).

Grindrod shareholders are set to receive a special dividend of 32.3 cents per share in terms of a cash return of 25% of the consideration received from the divestitures of non-core assets.

With strong cash generation and cash reserves in excess of operational requirements, Italtile will pay shareholders a special dividend of 98 cents per share as announced in the Group’s annual results released this week.

ASP Isotopes’ inward secondary listing on the Main Board of the JSE became effective on 27 August 2025. 91,41 million shares were listed at R217 per share reflecting a market capitalisation of R19,84 billion. In May the Nasdaq-listed company made an offer to Renergen minorities to take the company private, with the deal becoming unconditional during August.

Life Healthcare’s special dividend of 235 cents per share will be paid to shareholders on 22 September 2025.

Suspended Wesizwe Platinum has again pushed out the revised timeline for publication of its Annual Financial Statements for the year ended 31 December 2024 from 29 August to 30 September citing the status of the audit which is currently undergoing a final review and close out process. The company’s listing was suspended on 3 June 2025.

Following the approval of the scheme by shareholders and the payment of the scheme consideration by Eastern Trading on 25 August, AH-Vest shares were delisted from the JSE on 26 August 2025. Eastern Trading acquired the remaining 4.3% stake in AH-Vest at 55c per share – a significant premium to the share price prior to the announcement of 3c per share.

This week the following companies announced the repurchase of shares:

South32 will continue with its US$200 million repurchase programme announced in August 2024. The shares will be repurchased over the period 12 September 2025 to 11 September 2026.

On March 6, 2025, Ninety One plc announced that it would undertake a repurchase programme of up to £30 million. The shares will be purchased on the open market and cancelled to reduce the Company’s ordinary share capital. This week the company repurchased a further 48,846 ordinary shares at an average price of 189 pence for an aggregate £92,699.

Investec ltd commenced its share purchase and buy-back programme of up to R2,5 billion (£100 million). Over the period 20 – 26 August 2025, Investec ltd purchased on the LSE, 970,991 Investec plc ordinary share at an average price of £5.4694 per share and 889,606 Investec plc shares on the JSE at an average price of R130.9063 per share. Over the same period Investec ltd repurchased 757,369 of its shares at an average price per share of R131.887. The Investec ltd shares will be cancelled, and the Investec plc shares will be treated as if they were treasury shares in the consolidated annual financial statements of the Investec Group.

Bytes Technology will undertake a share repurchase programme of up to a maximum aggregate consideration of £25 million. The purpose of the programme is to reduce Bytes’ share capital. This week 374,522 shares were repurchased at an average price per share of £3.93 for an aggregate £1,47 million.

Glencore plc’s current share buy-back programme plans to acquire shares of an aggregate value of up to US$1 billion. The shares will be repurchased on the LSE, BATS, Chi-X and Aquis exchanges and is expected to be completed in February 2026. This week 9,3 million shares were repurchased at an average price of £2.94 per share for an aggregate £27,34 million.

In May 2025 Tharisa plc announced it would undertake a repurchase programme of up to US$5 million. Shares have been trading at a significant discount, having been negatively impacted by the global commodity pricing environment, geo-political events and market volatility. Over the period 18 to 21 August 2025, the company repurchased 47,617 shares at an average price of R21.09 on the JSE and 165,105 shares at 89.48 pence per share on the LSE.

In May 2025, British American Tobacco plc extended its share buyback programme by a further £200 million, taking the total amount to be repurchased by 31 December 2025 to £1,1 billion. The extended programme is being funded using the net proceeds of the block trade of shares in ITC to institutional investors. This week the company repurchased a further 358,878 shares at an average price of £42.00 per share for an aggregate £15,3 million.

During the period 18 to 22 August 2025, Prosus repurchased a further 1,305,123 Prosus shares for an aggregate €69,05 million and Naspers, a further 114,711 Naspers shares for a total consideration of R663,71 million.

Three companies issued profit warnings this week: Hulamin, Trellidor and Metrofile.

During the week two companies issued or withdrew a cautionary notice: MTN Zakhele Futhi (RF) and Metrofile.

Moody’s announced that it intends to secure a majority equity stake in Middle East Rating & Investors Service (MERIS – an affiliate of Moody’s), a domestic credit rating agency in Egypt. The transaction builds on a longstanding relationship between the two companies and is subject to regulatory approvals. Following the transaction, MERIS will continue to operate as an independent affiliate of Moody’s while developing its own rating methodologies, issuing its own credit ratings, and maintaining a separate management team. The terms of the transaction were not disclosed.

Finnfund announced a US$4 million debt investment in Poa Internet Kenya, a Kenyan internet service provider, to expand its network and improve internet accessibility. The investment aims to support Poa Internet in bridging the digital divide by providing affordable broadband internet to underserved communities in Kenya.

Hypeo Ai, a Moroccan startup streamlining influencer marketing through artificial intelligence, has announced an undisclosed investment from Renew Capital. Founded in 2024, Hypeo Ai helps brands and creators across Africa and the Middle East run faster, more efficient influencer campaigns by eliminating the need for manual tracking and fragmented tools. The platform connects brands with both human and AI-powered creators in under 15 minutes, offering an end-to-end campaign workflow that includes smart matching, pricing insights, and real-time performance tracking.

Norfund announced that it had taken a strategic minority equity investment in Kinetic Holdings Limited (popularly known as Kensta Group in East Africa), an East African distribution and manufacturing business. Kensta has been in existence for over 60 years and is dedicated to the supply of raw materials to the printing & packaging industry and the manufacturing of everyday essential paper-based products. Financial terms were not disclosed.

Inside Capital Partners announced and undisclosed investment in RDG Africa, a fast-growing leader in solar home systems and clean energy solutions across Southern and Central Africa. Founded in 2018, RDG delivers affordable, reliable, and sustainable electricity to underserved households and small businesses through its innovative pay-as-you-go model in Zambia and the DRC.

Ghanaian agritech company, Complete Farmer, has received a US$5 million debt investment from Symbiotics. Complete Farmer operates a platform linking farmers, buyers and agricultural input suppliers.

The Facility for Energy Inclusion (Cygnum Capital) has signed a facility agreement to provide US$5,7 million in senior debt to finance Qair’s renewable energy assets in the Seychelles. This financing will be utilised by Qair for the development, building, operations, and maintenance of a 5.80 MWp Floating PV plant located in the Providence Lagoon on Mahé Island in Seychelles. The Seysun Lagoon FPV is backed by a 25-year Power Purchase Agreement with the Public Utilities Corporation.

The global battery market is undergoing a period of rapid expansion, driven by the increasing demand for electric vehicles (EVs), renewable energy storage and industrial electrification. By 2030, the market is expected to reach north of US$300bn,1,2 underscoring the scale of opportunity for investors. However, the competitive landscape is evolving, with technological advancements, supply chain shifts and regulatory developments shaping the sector’s future.

For investors, the following two key questions are pertinent:

Will Lithium-Ion (Li-ion) become the dominant technology, and where are the biggest investment opportunities today?

What role does sub-Saharan Africa (SSA) play in the global battery value chain, and where are the real opportunities for investors?

This article examines the battery market dynamics and explores how investors can position themselves for both short-term gains and long-term strategic advantage.

The market opportunity: Lithium-Ion’s displacement of Lead-acid

For decades, Lead-acid batteries dominated the global energy storage market, supplying power for automotive starters, industrial applications and backup power systems. However, the rapid evolution of Li-ion technology has fundamentally reshaped the competitive landscape, displacing Lead-acid as the preferred solution across nearly all major applications. This transition is accelerating, with forecasts suggesting the Lithium-Ion battery market will expand from $54bn today to upwards of $182bn by 2030, commanding a share of 60% of the total battery market by 2030, up from 40% in 2024.3, 4

The market trajectory underscores the pace of this transformation.

• 2018: Lead-acid still accounted for a large portion of global battery capacity, maintaining a stronghold in traditional automotive and industrial sectors. Li-ion was emerging as a dominant force in consumer electronics and early EV adoption.

• 2024: Li-ion accounted for 40%3, 4 of the global battery market, driven by falling production costs, superior energy density, and rising demand from EVs and grid storage solutions. Meanwhile, Lead-acid’s market share continued to decline, sustained primarily by legacy applications in backup power and industrial machinery.

• 2030: Li-ion will capture 60% of the global battery market, leaving Lead-acid with just over 20% market share.3, 4 The combination of cost reductions, superior performance and environmental regulations will further accelerate Lead-acid’s decline.

The accelerating transition from Lead-acid to Lithium-ion (Li-ion) battery technology is being driven by a confluence of technical performance, economic performance (i.e., cost) and regulatory dynamics.

Technically, Li-ion batteries have established a clear advantage, offering superior energy density, faster charging, and significantly longer cycle life. These attributes are increasingly critical as energy storage applications grow more demanding across sectors ranging from electric mobility to grid infrastructure. Lead-acid batteries, by contrast, are struggling to keep pace, constrained by inherent limitations in chemistry and design.

Economically, the divergence is just as stark. Over the past decade, the cost of Li-ion batteries has dropped by nearly 90%,4 fuelled by rapid innovation, economies of scale, and global investment in research and development (R&D). Lead-acid, reliant on a mature and less scalable technology base, has seen only modest cost improvements. This widening cost-performance gap is fundamentally reshaping investment narratives in the energy storage space.

Environmental and regulatory considerations further tilt the scale. Lead-acid batteries contain toxic substances such as lead and sulfuric acid, exposing manufacturers and users to increasingly stringent environmental compliance requirements and costly disposal obligations. As sustainability standards tighten globally, Lead-acid’s risk profile is deteriorating, both reputationally and financially.

For investors, this transition presents a clear strategic opportunity: while Lead-acid investments are becoming riskier, Li-ion continues to gain momentum, making manufacturing, supply chain integration, and technology advancements in Li-ion the primary areas of focus.

Sub-Saharan Africa’s role in battery manufacturing: why investors should care

While much of the global battery supply chain is concentrated in China, the US and Europe, sub-Saharan Africa (SSA) is emerging as a key player in the sector. Historically, the region has been viewed primarily as a raw material supplier, but there is now growing momentum towards local beneficiation and manufacturing. This shift presents new investment opportunities, particularly in refining, precursor material production and, eventually, battery assembly.

SSA’s growing relevance stems first from its commanding position in the global supply of critical minerals. The Democratic Republic of Congo, Zimbabwe and Namibia are home to some of the world’s largest reserves of Lithium, cobalt and nickel – all core components of Lithium-ion battery production. As geopolitical tensions and resource nationalism prompt supply chain diversification, these countries are becoming focal points in global sourcing strategies.

Beyond raw materials, there is a noticeable policy shift toward localisation. Governments across the region are rolling out incentives to attract investment in local refining and processing capacity. This move seeks to reverse the longstanding pattern of exporting unprocessed ore, to capture greater economic value domestically. For investors, this creates compelling prospects in battery precursor manufacturing and related midstream infrastructure, with potential benefits in both cost and supply chain resilience.

Simultaneously, demand for energy storage solutions within the region is on the rise. The need for off-grid electrification, industrial energy reliability, and nascent interest in electric mobility is beginning to establish a local market base. This shift presents an opportunity to support the development of decentralised, locally produced battery systems tailored to regional requirements.

Despite these advantages, challenges remain, including logistical constraints, regulatory risks, and infrastructure gaps. Investors considering SSA should take a measured approach, focusing on projects with strong government backing, clear policy support, and robust offtake agreements to mitigate risks.

Strategic takeaways: How investors can position themselves

Investing in batteries requires a clear understanding of both near-term and long-term market shifts. While Li-ion presents a compelling immediate opportunity, emerging technologies and regional supply chain developments will shape the sector’s future.

• Near-term opportunity (2025-2030): Li-ion remains the dominant and most scalable investment option, with well-established manufacturing and supply chains. Investors should focus on Li-ion-related manufacturing capacity, supply chain integration, and localisation strategies.

• Mid-term positioning (2030-2035): Monitor new technologies like sodium-ion and solid-state battery developments, particularly in cost-sensitive applications. Explore strategic partnerships with battery innovators to gain early exposure to next-generation technologies.

• Long-term strategy (beyond 2035): Assess SSA’s potential as a major battery production hub, particularly as local policies and infrastructure improve. Track high-potential battery chemistries that may challenge Li-ion at scale, depending on material innovations and regulatory shifts.

The battery market is undergoing a fundamental transformation, with Li-ion overtaking and displacing Lead-acid technology across nearly all applications. Investors who position themselves early in Li-ion manufacturing, supply chain development, and emerging technology tracking will be best placed to capture value in this evolving market.

Rautenbach is Vice-President and Dempers, a Manager | Singular Advisory Africa

1 Battery Market Outlook 2025-2030, GlobeNewsWire (https://www.globenewswire.com/news-release/2025/02/04/3020360/28124/en/Battery-Market-Outlook-2025-2030-Insights-on-Electric-Vehicles-Energy-Storage-and-Consumer-Electronics-Growth.html) 2 Battery Market industry analysis, GrandViewResearch (https://www.grandviewresearch.com/industry-analysis/battery-market) 3 World Energy Outlook Special Report, International Energy Agency (https://iea.blob.core.windows.net/assets/cb39c1bf-d2b3-446d-8c35-aae6b1f3a4a0/BatteriesandSecureEnergyTransitions.pdf) 4 Lithium-ion Battery Market Summary, GrandViewResearch (https://www.grandviewresearch.com/industry-analysis/Lithium-ion-battery-market)

This article first appeared in DealMakers, SA’s quarterly M&A publication.

Afrimat is navigating quite the storm at the moment, with the business dealing with a most unfortunate cocktail of unfavourable commodity markets, major concerns around South African infrastructure and the overhang of potential corporate failure at ArcelorMittal (JSE: ACL) as a major customer. Although Afrimat has noted that the bulk of its supply to ArcelorMittal goes to ArcelorMittal’s Flats business, not the Longs business that is likely to be shut down, the market doesn’t like risk and especially not in a market like South Africa.

Speaking of risk, Afrimat recently rolled the dice in acquiring the Lafarge business, a transaction with substantial long-term potential and short-term pain.

The net result of all this is unfortunately a plummeting share price,

Afrimat has released a pre-close update dealing with the six months ending August. They note that although Q1 was weak, there were signs of improvement in Q2. This includes an improvement in sales volumes, as well as significant progress made on the integration of the Lafarge business.

Here’s a fun fact for you: 50% of the Transnet-approved quarries are owned by Afrimat. This gives you an idea of the potential upside in the business if we could just see an improvement to the South African infrastructure story. A separate and highly relevant point regarding Transnet is confirmation by Afrimat that the decline in logistics availability on the Saldanha export line has been stopped, which is obviously great news for the iron ore business.

Afrimat shareholders have historically been spoilt by the company’s diversification and ability to avoid the typical cyclical pain that is found in this sector. The recent combination of issues has proven to be too much for the market, leading to the huge decline in the share price. Afrimat is all the way back to the levels seen five years ago. Like all cyclicals, at some point this is likely to turn and those who buy at the bottom will make a fortune. Alas, figuring out the exact location of the bottom isn’t so easy.

Bidcorp just keeps delivering (JSE: BID)

This is one of the most solid names on the JSE

Bidcorp has released results for the year ended June 2025. With the recent performance of the rand, their position as one of the most effective rand hedges on the JSE was actually a negative in this period! This is evidenced by revenue being up 6.8% in constant currency, but only 4.3% as reported.

Trading profit increased by 6.4% and HEPS was up 6.5%. The dividend increased by 6.4%. It’s a dependable, simple shape to the income statement that appeals to long-term investors.

The share price closed 3.7% lower though, taking the year-to-date move to +4.7% (with very choppy trading along the way). Bidcorp trades at a lofty Price/Earnings multiple, hence why there’s no obvious direction to the share price in a period in which performance is positive, but also uninspiring.

As a quick note on underlying performance, it was the UK and Europe that saw a strong bump in profit in this period, with a positive contribution from emerging markets as well. Australasia was a drag on performance and is unfortunately the second largest segment in terms of profits, so that would’ve contributed to the share price dip on the day.

Blue Label Telecoms took an 18% bath on the day of releasing earnings (JSE: BLU)

And there was no shortage of fighting between bulls and bears on the socials

There are three types of people when it comes to Blue Label Telecoms: (1) those who claim to understand the financials, (2) those who at least acknowledge that they bought the stock based on momentum, rather than fundamentals, and (3) those who don’t buy complicated financials on principle. I fall into the third category.

It seems as though a number of people in the second category headed for the exit on Tuesday, with the share price closing 18% lower on the day of results. This is despite a 2% increase in gross profit and a 17% increase in EBITDA. Once you factor in the huge swing on the associates line though, you end up with a 262% increase in headline earnings!

It’s usually worth following the cash and seeing how a business actually makes its money. Blue Label generated cash from trading operations of R488 million and then spent so much on interest (and tax) that they ended up with a net cash outflow from operating activities of R466 million. The reason why the net decrease in group cash for the year to May 2025 was “only” R75 million is that they raised a whole lot of debt.

The sooner that Blue Label separates out Cell C and lists it as a standalone company, the better. The reaction by the market to these numbers tells you that people are jittery and unsure of what the fair value really is. Of course, this is both an opportunity and a risk, which is what makes markets so exciting!

Curro to be taken private at R13 per share (JSE: COH)

From growth darling to charity case – literally

A decade ago, Curro was the growth story on the JSE. People were fighting over each other for allocations in capital raises, with the story being clear: South Africa was failing its people and thus there was a huge opportunity in offering private education to middle-income South Africans. In some respects, they were right. The risk that was probably impossible to foresee at the time was a sharp decline in total births in South Africa, a function of both a huge shift in society and substantial emigration as well.

If you can’t fill the schools, it’s very hard to make money from them. Curro’s results for the six months to June tell a story of a company that is treading water, with revenue up 4.7% and flat EBITDA for the year. Recurring HEPS increased by just 0.2%.

Is that a sustainable business? Sure. Is it an appealing investment? No.

With very little likelihood (in my view) of the trend in learner numbers turning positive, Curro’s story has evolved from one of growth to one of social enterprise, where the company is capable of running at a sustainable profit, but probably not with the kind of metrics that investors want to see.

This is where the Jannie Mouton Stigting comes in, being a public benefit organisation that was founded by Mouton as an education investment vehicle and that currently has a 3.36% stake in Curro. Clearly, Curro is the perfect way to execute the overall dream of the organisation. The Jannie Mouton Stigting will be acquiring Curro and turning it into a non-profit company through this transaction.

I must say, I’m surprised that there is a reference in the announcement to a need to scale Curro even further. Perhaps they will invest in more schools aimed at lower-income families, with a price point to match. I hope so, as that would truly make a difference in South Africa. With the current pricing strategy, I just don’t think that Curro is targeting a broad enough group of kids.

The Jannie Mouton Stigting is paying up for the stake, with a price of R13 per share on the table for Curro. This is a reminder of the dangers of shorting, as having a short position in Curro would’ve been a perfectly reasonable thing to do under the current fundamental circumstances, yet this offer just came in at a 60% premium to the closing price on 25 August. Anyone caught short on this stock is seriously bleeding.

The deal will be paid for through cash (only 6.6% of the price) and a swap of Capitec and PSG Financial Services shares currently held by the trust. It’s therefore an incredibly clever situation in which the trust is using its capital base in highly successful companies to go and acquire a group that perfectly matches its objectives.

Other than for those who just saw their short positions obliterated, it’s hard to see how anyone could fault this deal. People like to hate on billionaires, yet another example of one stepping in to make up for the failings of government. Save your energy for hating on corrupt public officials instead.

A spectacular year for OUTsurance (JSE: OUT)

This adds to the positive sentiment in the financial services sector

Generally speaking, the insurance-based financial services groups are doing well at the moment. OUTsurance has added its voice (and growth) to that mix, with a trading update for the year ended June 2025.

They are enjoying not just decent premium growth, but also a favourable claims experience. Although they are incubating OUTsurance Ireland as a new business and are thus incurring start-up losses there, the growth elsewhere in the group is more than making up for it. In fact, it’s the Australian business that is really flying at the moment in terms of the larger segments, serving as a wonderful reminder that OUTsurance knows exactly how to build offshore businesses from scratch. If they can replicate the Australian success in Ireland, shareholders should be smiling.

The smiles are there already, with HEPS up by between 26% and 32% for the year to June 2025. Although OUTsurance trades at a substantial Price/Earnings multiple, that’s still good enough for a 12% year-to-date performance in the share price.

Spur is on the wrong end of an arbitration claim (JSE: SUR)

And it’s an oral agreement about ribs that is being debated, ironically

Two companies within the Spur group were served summons in 2019 by GPS Food Group RSA, based on an alleged oral agreement regarding the establishment of a rib processing facility. The damages claim is between R119.9 million and R167 million. If that first claim failed, there was an alternative delictual claim of R95.8 million.

The parties went to arbitration and the arbitrator made a “part award” yesterday in favour of GPS based on the first claim (the bigger one). No award was made on the second claim. Notably, the arbitrator hasn’t determined the quantum of damages.

Either way, Spur will appeal it within the next 30 days. This goes to a panel of three arbitrators and that ruling is final.

Transpaco reflects the broader SA industrial sentiment (JSE: TPC)

Almost every metric is slightly in the red

Transpaco released results for the year to June 2025. They are incredibly uninspiring, with revenue down 2.2% and HEPS down 0.9%. The dividend was down 2.1%. This isn’t the most liquid stock around, but a 13.3% year-to-date drop tells you that all isn’t well in the industrial segment of the South African economy.

The plastics division grew revenue by 0.2% at least, while the paper division fell by 4.6%. If there’s a silver lining in here somewhere, it’s probably that group operating margin was maintained at 8.6%. Under the circumstances, that’s actually quite impressive.

The SA Inc. dream really hasn’t come to fruition this year, despite all the exuberance we saw in 2024 around the GNU.

Nibbles:

Director dealings:

The spouse of the CEO of Huge Group (JSE: HUG) bought shares worth R675k.

A director of Invicta (JSE: IVT) bought shares worth R58k.

The CEO of Vunani (JSE: VUN) bought shares worth R8k.

Putprop (JSE: PPR) has guided an increase in HEPS for the year ended June 2025 of between 20.8% and 40.8%.

All the resolutions that would’ve been in favour of the group of institutional shareholders who demanded the extraordinary general meeting of MAS (JSE: MSP) failed to pass at the meeting. This is obviously because the Prime Kapital offer was a success in terms of getting enough votes locked in ahead of that meeting.

Primary Health Properties (JSE: PHP) has confirmed that the offer to Assura (JSE: AHR) shareholders will remain open for acceptance until 10 September 2025. Primary Health now has over 92% in Assura and they will be following the compulsory acquisition (or squeeze-out) process to take this to 100%, delisting Assura in the process.

ASP Isotopes (JSE: ISO) has officially started trading on the JSE! It will no doubt take a while for volumes to pick up, as is usually the case with a new listing.

Rex Trueform (JSE: RTO) will increase its stake in Byte Orbit from 30.02% to 51.02% for R21 million. They will pay for it through the issuance of more Rex Trueform N shares, which are listed on the JSE. It may sound like a toothpaste company, but it’s actually a software and digital innovation company. This is also relevant to shareholders of African and Overseas Enterprises (JSE: AOO).

AYO Technology (JSE: AYO) has pushed out its general meeting from 29 August to 29 September based on a request from the PIC to have more time to consider the “merits and risks associated with holding shares in a delisted entity”.

Salungano (JSE: SLG) has agreed a “standstill” with its banks, which means they standstill on their legal rights provided that the company complies with the terms of its debt. Salungano has been in breach of its loan facilities since 21 June 2023. Remember, when you owe the bank a fortune, you can get them to standstill. When you just owe them for a car, you’ll be the one standing still after they take it away.

Wesizwe Platinum (JSE: WEZ) is suspended from trading and hopes to finalise its audit process for the 2024 financials by the end of September.

Note: Ghost Bites is my journal of each day’s news on SENS. It reflects my own opinions and analysis and should only be one part of your research process. Nothing you read here is financial advice. E&OE.Disclaimer.

Accelerate Property Fund has sold two buildings at NAV – yet the market didn’t like it (JSE: APF)

Shareholders are clearly still panicky when it comes to this stock

There are a lot of reasons to worry about Accelerate Property Fund. There are significant overhangs on the share price, not least of all the related party issues that have become problematic once more. The ongoing turnaround of Fourways Mall remains uncertain, although there are significant green shoots. The TL;DR is that this is a risky play.

The fund trades at a huge discount to net asset value (NAV) due to these issues, which tells you at least one thing for sure: selling properties at NAV can only be a good thing. In fact, it would be a fantastic outcome for shareholders if the fund could sell absolutely all its assets at NAV, settle its liabilities and pay the rest to shareholders.

Now, a sale of the full portfolio isn’t on the cards right now, but partial sales along the way should be most welcomed. Instead, the share price closed 7% lower on the news of Accelerate selling The Buzz and Waterford Centre for a total price of R215 million, which is equal to the directors’ valuation (i.e. the NAV) as at 31 March this year.

It’s an odd response from the market that demonstrates just how much confusion and panic there is around this share price. Therein lies the opportunity for speculators of course, with the caveat that this is a high-risk turnaround story.

The buyer of the two properties is Dorpstraat Capital Growth Fund, with a number of backers including Rabie Property Group (a name you may know). The Buzz and Waterford are both situated in Fourways, as per usual when it comes to Accelerate Property Fund.

There are unfortunately some hurdles that need to be overcome for the sale, including a rezoning to unlock the final R10 million of the purchase price and an unconditional Competition Commission approval to get the entire transaction done. Thankfully there are no sales commissions at play though, as the parties have clearly been negotiating directly with each other. This means that the proceeds of R215 million can be fully applied to debt reduction and overall flexibility on the Accelerate balance sheet. It’s just going to take a few months to get the cash.

The disposal yield is 9.5% based on one-year forward income and taking into account Pick n Pay’s exit from The Buzz.

Down 7% for the day and now at R0.39 per share, the share price is changing hands below the recent rights offer price of R0.40 per share. Either the investors dumping the stock are wrong, or the anchor shareholders are wrong, but someone is wrong here. Only time will tell, but my view is that a sell-off in the stock in response to a sale of properties at NAV is a sign of an irrational market.

Cashbuild managed to increase earnings this year (JSE: CSB)

But nothing is coming easy at the moment

As we saw with Italtile (JSE: ITE) earlier this week, consumer discretionary retail has been a real slog this year. It’s hardly any better in the US by the way, with the likes of Home Depot and Lowe’s reporting that consumers are more willing to do small DIY projects than large projects at the moment. The reason is the same on both sides of the pond: interest rates are stubbornly high and consumers are taking strain.

With a retail-focused model rather than a manufacturing arm like Italtile has, Cashbuild is better equipped to weather the storm. It’s hard enough trying to generate decent returns from a store footprint. Once you add on the fixed costs of manufacturing, then operating leverage really kicks in and a weak consumer environment kicks you harder.

This is why Cashbuild’s trading performance for the 52 weeks to 29 June 2025 is well ahead of Italtile, with HEPS growth of between 7% and 12%. Italtile could only manage 2% over the same period. Given the underlying business model differences, I think both companies did pretty well under the circumstances!

Cashbuild is expected to release results by 3 September.

It looks likely that Mahube Infrastructure will be leaving the JSE (JSE: MHB)

Another day, another takeout offer

Mahube Infrastructure released a cautionary announcement on Tuesday and ended the day 32% higher. This combination usually means only one thing: a takeout bid is coming.

Sure enough, the cautionary confirms that the company has been approached by a third-party offeror looking to make a cash offer for all the shares in Mahube in the form of a scheme of arrangement, which would naturally lead to the delisting of the company if the scheme is approved.

It’s very important to note that nothing is finalised or guaranteed at this point. The company also hasn’t indicated the price of the potential offer, so the market is taking a guess right now around whether there’s more upside in this thing.