According to the Forvis Mazars C-Suite Barometer: Outlook 2025, business leaders are focusing on new or revised talent and retention strategies, which will play a major role in redefining organisations and creating opportunities to unlock growth, compete for market share, and sustain a competitive advantage.

However, as talent rises as a strategic priority in 2025, just under half (43%) of organisations continue to report a struggle to recruit talented people, with the emphasis shifting to high-quality employees at more junior levels.

“Executives are reporting widespread difficulty in attracting and hiring the right talent and the bigger challenge now is in recruiting entry and mid-level talent, rather than senior talent as we saw in 2024,” explains Daniella Frank, HR Senior Manager at Forvis Mazars in South Africa.

In some regions, C-suite executives are having an especially tough time finding the right people. Leaders in Africa report the most difficulty, with smaller businesses bearing the brunt of recruitment challenges, with more than half struggling to hire top talent compared to around a third of $1billion+ organisations.

“Locally, businesses are struggling to attract and retain skilled professionals, despite rising unemployment,” continues Frank.

Findings from the report reveal that South Africa faces a dual challenge of high youth unemployment and a skills mismatch, particularly in tech and finance.

From a talent acquisition standpoint, companies are seeking individuals who can effectively integrate artificial intelligence (AI) with business goals and utilise it adeptly.

“The success of AI and the businesses that embrace it is dependent on the skills of those who implement and operate it, because the technology will not replace professions like auditing,” explains Susan Truter, Audit Partner and Member of the Executive Committee for Talent at Forvis Mazars in South Africa.

Instead, Truter says AI will enhance organisational efficiencies and help distinguish the service offering by enhancing human skills and traits like understanding, trust, empathy, personal connections, and nuanced approaches to the specific cultures and needs of its people.

“Establishing trust with clients and effectively communicating findings and solutions are critical skills that AI cannot replicate,” she continues.

“Our auditors are evolving into strategic advisors, concentrating on higher-value tasks such as interpreting complex data trends, focusing on areas of judgement and estimate, offering insights, and making risk-based decisions. As such, all staff, from the CEO to team members, need to enhance their proficiency in AI applications, which is why we have launched initiatives like our data school.”

However, finding, attracting and retaining people with these skills is a major challenge facing organisations in every sector.

While a generous salary and benefits remain the top factor (96%) in the report, the salary premium already being paid in certain sectors is making it harder for organisations to put inflated offers on the table that are big enough to persuade candidates to join.

As such, companies need to look at other means to secure the right candidates for the business.

In this regard, learning and development opportunities (94%) continue to feature highly as important factors to attract and retain talent.

“To get the best people, organisations must recognise the importance of learning and development opportunities for employees and their business but may need to review with their people what they expect from their employer of choice,” continues Truter.

In addition, findings from the report suggest that companies need better employer branding, upskilling programs, and flexible work models to remain competitive, as how companies structure work will impact talent attraction and retention.

To make their organisations more attractive places to work, C-suite executives are focusing on flexibility and hybrid working.

However, there is still a split in consensus regarding ways of working. While many are leaning into flexible working, another group is doubling down on standard working hours, with compliance with this traditional model still chosen by 37% of executives. In South Africa, certain industries like finance, law, and consulting are resisting full flexibility.

“The reality is that business leaders cannot bring back the working models used before COVID-19, and they cannot lead an organisation as they did even 10 years ago,” cautions Truter.

“If leaders expect and push everyone back to the office, they will struggle to retain their best people. Business leaders need to consider intergenerational differences in how and where people want to work.”

Among organisations that use hybrid working, the aim is to be as flexible as possible for employees, not ensure that everyone is in the office.

Based on the findings shared in the report, three in five executives say that a key goal of hybrid working for their business is to “be fully flexible for our people”.

Business leaders should view the workplace model as an opportunity to readdress their business strategies, listen to their people and create a sustainable working model that retains experienced workers and attracts new talent, states the report.

Alongside this, a modern working environment with access to tech increased by three points (93%) in the 2025 report, with employee engagement emerging as another important factor.

“To create engagement, it’s important to give people the trust and responsibility to ensure they know that they matter,” explains Frank.

“At Forvis Mazars, we do this through our own people surveys to capture a consensus of opinions as well as the more personal day-to-day discussions during development. This is a great way to establish engagement and receive more value in return from your people.”

Ultimately, the talent is out there, leaders just need to approach their needs differently.

Talent today does not necessarily need or want to work from a specific location or office. The more flexible organisations can be with their people, the more opportunities they will have to attract the best talent when combined with other factors, such as top-paying jobs and access to the latest technologies.

Assura will formally respond to the revised Primary Health Properties offer later this month (JSE: AHR | JSE: PHP)

Assura’s board has a duty to keep assessing the offers

The latest attempt by Primary Health Properties to get the Assura board to back its offer at least has some chance of success, as Assura has committed to fully review the revised terms of the offer. I’m pretty sure that the sticking points will still be around the risks facing the merged entity, rather than the exact share ratio that Primary Health is willing to offer.

The Assura board has committed that by 27 June, they will have sent a response circular to shareholders that deals with its views on the Primary Health Properties offer.

Although this could still go either way, my view remains that cash is king in these deals and that puts KKR and Stonepeak at the front of the queue.

Astoria’s sale of ISA Carstens has been completed (JSE: ARA)

Diamonds are anything but sparkly right now, but Goldrush and Leatt are on the up

Astoria is an investment holding company with a diversified portfolio. This means that the constituents of the portfolio have varying performance at any point in time, with the overall direction of travel for the portfolio hopefully being up.

A significant change to the portfolio saw the sale of Astoria’s 49% in ISA Carstens Holdings for R71.0 million (cash and loan accounts), with that deal having now met conditions precedent and closed accordingly.

Elsewhere in the portfolio, the ongoing pressure on diamond prices has wreaked havoc on Trans Hex. With debt providers in Trans Hex having called for an equity injection to support the balance sheet, Astoria has elected not to participate in this round or to provide further funding. Thankfully, Astoria has not provided any guarantees either. The value of the investment in Trans Hex has been written down to zero.

In much happier news, the share prices of the two listed investments (Goldrush and Leatt) have increased significantly since 31 March 2025, the date of the last quarterly results. Goldrush is up 56% and Leatt is up 17%.

Gemfields seems happy with the latest ruby auction results (JSE: GML)

As always, comparability is very limited

It’s difficult to form a view on how Gemfields is performing in each auction, as the underlying mix of rubies (or emeralds, as the case may be) changes from one auction to the next. This leaves us largely reliant on management’s commentary about the auction, which isn’t a great position to be in as management is obviously at risk of giving a biased view.

To their credit, Gemfields isn’t shy to talk about the tough stuff in the market. The current economic and geopolitical backdrop isn’t exactly favourable to shiny stones. Despite this, Gemfields notes that pricing of fine-quality rubies is strong and that secondary-type rubies (recovered from a newer area of the MRM mine in Mozambique) found support with buyers.

The gems come out the ground in all shapes and sizes, with this auction including a 36-carat fine-quality ruby that achieved a high price.

This auction achieved an average price of $461.48 per carat and revenues of $31.7 million. This is a much higher average price than in other recent auctions, but that number was skewed by the mix of lots that actually sold at the auction, as well as the lack of small-sized rubies in this auction.

A point of concern here is that the total revenue of $31.7 million makes this the smallest ruby auction (and by quite some margin) of the past couple of years. Only 78 of the 90 lots offered for sale were sold. The market is clearly still struggling with weakness.

Powerfleet is growing rapidly – but where are the profits? (JSE: PWR)

The SA market isn’t very receptive to “adjusted EBITDA” as a metric

The US market is filled with eternal optimists who firmly believe that adjusted EBITDA will eventually lead to huge net profit growth and great rewards in the share price. Conversely, the South African market is filled with realists who want dividends above all else. As usual, somewhere in the middle is the truth.

But just where does Powerfleet lie on that spectrum? With the primary listing in the US, you can be sure that terminology like adjusted EBITDA is all over this thing. I would’ve loved to be a fly on the wall in the meeting where the concept of HEPS was introduced to them and how it deducts things like stock-based compensation, which most tech companies incorrectly view as a quasi-expense at best.

Like all US growth companies, most of the announcement is dedicated to talking about revenue. For the year ended March 2025, they bought plenty of revenue through acquisitions. The MiX Telematics deal closed right at the start of this year, so don’t treat metrics like revenue growth of 169% and adjusted EBITDA growth of 882% as being remotely sustainable numbers. The group reports numbers adjusted for the MiX deal, reflecting revenue growth of 26% and adjusted EBITDA growth of 65%. Now, those are still strong numbers of course, but is adjusted EBITDA worth focusing on?

In a business that relies on telematics devices and the associated working capital that gets tied up, I definitely wouldn’t look at EBITDA. Instead, I would look at the operating loss that worsened considerably, or the headline loss per share that came in at $0.43 (better than a loss of $1.14 in the comparable period).

In terms of exit velocity for the year, the fourth quarter net attributable loss was $0.09 per share (this isn’t the same as the headline loss but is certainly a lot closer than adjusted EBITDA and other fairy tale numbers).

Here’s the interesting thing though: the attributable fourth quarter loss is only better than it was a year ago because of a change in the capital structure. Instead of a large attribution of value to preference shareholders, we now have losses spread across more ordinary shareholders. If we just look at the net loss before tax (instead of on a per-share basis), it climbed from $1.4 million in Q4’24 to $12.7 million in Q4’25.

My final comment is on the cash flow profile of the group and the related debt. Net cash from operating activities was an outflow of $3.3 million in the year ended March 2025 vs. an inflow of $26.3 million in the prior year. They invested $137 million in acquisitions and had to raise long-term debt of $125 million to do it, along with a private placement of equity of $66.5 million. The excess proceeds from the placement were used to redeem the preferred shares mentioned above. Total cash at the end of the period is down at $49 million vs. $137 million the year before.

In summary, this is a heavily indebted technology company that is very focused on telling an American story. The problem is that the Americans aren’t exactly forming an orderly queue for the stock, as evidenced by the Nasdaq chart (note: this includes a few years before the recent acquisitions):

The market didn’t love the lower payout ratio at Stor-Age (JSE: SSS)

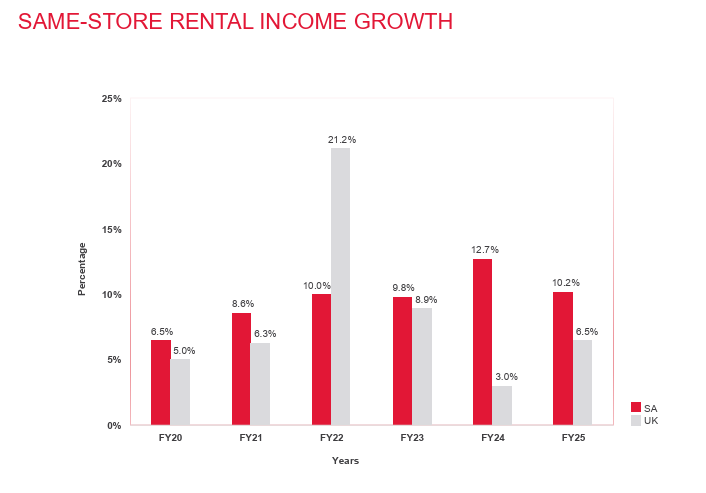

Being less of a cash cow than before leads to churn on the share register

Stor-Age released results for the year ended March 2025. The focus in the market is on the dividend per share, which decreased by 6.3% to 110.72 cents. This is despite distributable income per share increasing by 4.1%. The payout ratio has dropped from 100% to 90%.

Net property operating income grew by 11.1% in South Africa and 5.0% in the UK. Here’s a great slide for those who like to argue that the UK is a stable operating environment compared to good ol’ sunny South Africa:

In terms of the balance sheet, the loan-to-value ratio sits at a solid 31.3%. That’s almost identical to the prior year and well in line with where it needs to be. Stor-Age is a solidly managed business.

There’s a great slide in the investor presentation that tells the story of the past decade. Over 10 years, the distributable income per share grew at a compound annual growth rate (CAGR) of 4.9%, whereas net property operating income increased by 27.8%. Note that the former is a per-share metric and the latter is not. Another useful way to see this distinction is that investment property value grew at a CAGR of 27.8%, while the net asset value per share grew at 6.6%. This tells you that there are far more shares in issue than a decade ago, with Stor-Age taking full advantage of its listed structure to grow the group.

Speaking of the NAV per share, they are currently at R17.04, up 5.6% in the past year. The share price closed 3.6% lower at R15.86, so there’s a fairly modest discount here by REIT standards.

With a lower payout ratio, the group is focusing on NAV-accretive initiatives for the next chapter in its growth. To justify the retention of capital, they will need to be some interesting things.

They are also busy with joint ventures aimed at boosting return on equity, with the idea being that Stor-Age earns management fees on a portion of the portfolio that is paid for using that most illustrious of banking concepts: Other People’s Money. The management fees are still small in the group context (R71 million), but 70% of the fees are classified as recurring and I think we will see significant growth in this metric.

With the payout ratio of 90% now baked in, the outlook for the 2026 financial year is for distributable income per share growth of between 5% and 6%.

Vukile is growing in both regions of focus (JSE: VKE)

This is what investors want to see

When a company has diversified exposure, there’s always a risk to investors that a certain part of the business might drag the entire thing down. Groups are only as good as their weakest link. The good news at Vukile is that there is no weak link right now, with the portfolio doing well in both South Africa and Iberia (Spain and Portugal).

In the year ended March 2025, the South African portfolio achieved like-for-like retail net operating income growth of 6.4%, while enjoying lower vacancies and more efficient operations with a better cost-to-income ratio. The like-for-like retail portfolio value moved 8.5% higher thanks to the stronger metrics.

Over in Spain and Portugal, like-for-like net operating income growth was 6.4%. I must highlight positive rental reversions of 17.3%, as this indicates that new leases are being put in place at much stronger rates than before. The like-for-like valuation increase is only 3.6% though, as the property metrics are dovetailed with broader macroeconomic conditions when assessing the valuation. Recent acquisitions in the area have been at appealing yields, ranging from 7.2% for a flagship centre in Spain through to an interesting, more tourist-focused centre in Madeira for 9.5%. Remember, these yields are in euros.

Although the loan-to-value ratio of 40.95% is perhaps slightly on the high side by large REIT standards, the good news is that only 1.6% of debt is maturing in FY26. The credit rating outlook for both Vukile and Castellana (the subsidiary in Spain) improved from stable to positive. When they do come to market for refinancing in years to come, they are doing so from a place of strength.

The total dividend per share grew by 6.0% for the year. They aren’t offering a dividend reinvestment plan, so that will thankfully limit dilution of earnings for shareholders going forward. For the year ending March 2026, Vukile believes that the dividend per share can grow by at least 8%.

The market loved this, with the share price up 2.5% on the day and more than 20% higher in the past year.

Nibbles:

Director dealings:

Here’s a director purchase of shares that is well worth paying attention to: Willem Roos (one of the original founding members of OUTsurance, among many other achievements) is a non-executive director of WeBuyCars (JSE: WBC) and he’s bought shares (via an associated entity) worth nearly R20 million.

The CEO and another executive director of AVI (JSE: AVI) bought shares in the company worth a total of over R5.2 million.

There’s some selling of shares by directors and senior execs of Tharisa (JSE: THA). Notably, the CFO sold shares worth nearly R4.5 million. The sales by the company secretary and a director of a major subsidiary came to R1.2 million.

A prescribed officer of Thungela (JSE: TGA) sold shares worth R2.2 million.

An associate of an executive director of Trematon (JSE: TMT) sold shares worth R77.5k.

The company secretary of Alexander Forbes (JSE: AFH) sold shares worth R41k. Although these were related to a share award, the announcement isn’t explicit on whether this is only the taxable portion.

A director and an associated entity bought shares in Finbond (JSE: FGL) worth just over R30k.

The director of Italtile (JSE: ITE) who is busy selling pledged shares has sold another R20k worth of shares.

A non-executive director of Quilter (JSE: QLT) bought shares via a dividend reinvestment plan to the value of around R20k.

YeboYethu (JSE: YYLBEE) had a much better time in the year ended March 2025. Thanks to a sharp increase in the Vodacom share price that this B-BBEE structure relates to, the net asset value per share shot up from R31.51 to R73.77. The final dividend increased by 5% to 101 cents per share. YeboYethu is trading at just over R26 per share, so the discount to NAV is vast.

Brikor (JSE: BIK) has released a trading statement dealing with the year ended February 2025. They expect HEPS to be between 0.3 cents and 0.7 cents, which is a nasty drop of between 46.2% and 76.9% vs. the 1.3 cents in the comparable year. They have indicated that detailed results will be out by 20 June (which is particularly relevant as they are late with the release of financials – you’ll see that update further down as part of the broader naughty corner announcement by the JSE).

Ninety One (JSE: N91 | JSE: NY1) and Sanlam (JSE: SLM) have concluded the transaction related to Sanlam’s UK business that has been acquired by Ninety One. As consideration for the deal, Ninety One issued shares to Sanlam. Sanlam now has a 1.5% stake in Ninety One.

Glencore (JSE: GLN) announced that the merger of Viterra with Bunge has now met all conditions and will close in July.

Caxton and CTP Publishers and Printers (JSE: CAT) completed its odd-lot offer for total consideration of R340k. This reduced the number of shareholders by 31%, thereby significantly decreasing the administrative burden of the share register.

Eastern Platinum (JSE: EPS) has suffered a cybersecurity incident. This hasn’t disrupted business operations, but it does appear as though some sensitive files made their way onto the internet. No further details have been given at this stage.

In the naughty corner for late submission of financial statements, we find African Dawn Capital (JSE: ADW), Brikor (JSE: BIK), Efora Energy (JSE: EEL), Copper 360 (JSE: CPR) and Visual International (JSE: VIS). If they fail to release financials by the end of June, their listings may be suspended.

In case there are any desperate souls out there hoping that PSV Holdings (JSE: PSV) might one day return to life, the company has renewed the cautionary announcement on the basis of recent engagements between DNG Energy and the company liquidator regarding taking the business out of provisional business rescue. There is no further clarity at this point on what might happen. The fact that their old website domain currently reflects as being held for sale tells you a lot.

The Gemfields rights offer was well supported by the market (JSE: GML)

But there’s still a slice for the underwriters

After the near-perfect storm that severely broke the Gemfields balance sheet and forced them into a situation where they needed to raise capital from the market, it’s good to see that the overall narrative of “this is temporary, not forever” was accepted by investors.

The rights issue was fully underwritten, so there was no doubt regarding the company raising the full amount. Still, the response of the market to the rights issue tells you a lot about how investors are feeling about the company at the moment.

82.4% of the new shares to be issued were taken up by existing shareholders in proportion with their holdings. There were no excess applications allowed. This would of course include the underwriters taking up their rights in respect of their existing shares. The remaining 17.6% of shares were then taken up by the underwriters, Assore International Holdings and Rational Expectations.

The rights issue raised $30 million in gross proceeds. The ball is now in Gemfields’ court to make sure that they don’t find themselves in this position again by taking on too many risks at the same time.

Challenges continue at Merafe (JSE: MRF)

The South African ferrochrome sector is in trouble

Back in February 2025, Merafe alerted the market to a business review process in which they needed to take a hard look at their assets in the ferrochrome joint venture with Glencore. This eventually led to a decision to suspend the smelting operations at Boshoek and Wonderkop from 1 May 2025 and 31 May 2025 respectively.

The latest update is that the company has also suspended operations at the Lion smelter, although this is on a temporary basis for maintenance and rebuilds.

The company is “engaging” with “all relevant stakeholders” about the ferrochrome industry and the potential cost-saving measures and policy changes that would be required to get things right. In my experience, that’s the kind of wording that a company uses before announcing a permanent change to operations. We will have to wait and see.

A juicy payday is coming for MTN Zakhele Futhi shareholders (JSE: MTNZF)

The recent performance of the MTN share price has driven this decision

It’s incredible how quickly things can change in the market. At the end of last year, MTN had to take steps to extend the MTN Zakhele Futhi scheme to avoid it maturing in such a way that minimal residual value would go to investors. Fast forward a few months and we have a situation in which the directors of MTN Zakhele Futhi have chosen to unwind the structure based on the current strength of the MTN share price and the seemingly irresistible opportunity to put real value in the hands of investors.

To achieve this, MTN Zakhele Futhi executed an accelerated bookbuild offering of most of its stake in MTN, representing 1.26% of MTN’s total issued shares. This raised gross proceeds of R3 billion, which in turn will be used to settle debt in the structure.

The estimated current net asset value per MTN Zakhele Futhi share is between R20.00 and R21.50. They are looking to distribute R15 per share as a dividend or a return of contributed tax capital as soon as possible. The residual value of R5.00 – R6.50 per share will take longer, as they need to wind up the company and delist it from the JSE.

When it comes to volatility, there isn’t much out there to match MTN Zakhele Futhi:

You may notice that the current price is still well below the estimated net asset value. This is because of execution risk and the time value of money, although it feels like the current discount may still be too big. In illiquid stocks like this, there isn’t always a bid and/or offer available in the market to close the gap to sensible levels.

Novus is successfully evolving its business – but not without headaches (JSE: NVS)

With newspaper and magazine printing plummeting, the rest of the group is a mixed bag at the moment

Novus is a great example of why it’s important not to be blind to disruption. Once upon a time, the printing of magazines and newspapers was a lucrative business. Today, those publications are barely staying alive, which means that printers would be in just as much trouble if they hadn’t diversified.

Novus has found a couple of new growth avenues. One is the printing of books, particularly with an educational flavour thanks to the acquisition of Maskew Miller Learning – and even that’s far from being a guaranteed source of growth, as you’ll shortly see. Another important growth area is the packaging business. They aren’t sitting still either, with a well-publicised mandatory offer to Mustek shareholders that led to a nasty spat with the regulator. Other recent deals included the acquisition of 48.58% of Bytefuse and the acquisition of three divisions of Media24. These are much smaller transactions than the investment in Mustek, but are still relevant.

There’s plenty going on here, so the numbers for the year ended March 2025 are particularly important. Revenue increased by 6.6% and operating profit was pretty flat. Assisted by a small reduction in the number of shares outstanding, HEPS increased by 12.1% to 88.3 cents. Finally, the cash dividend was 10% higher at 56 cents per share. The end result for shareholders may have been solid, but there’s plenty of underlying volatility here that makes it difficult to guess how the future might unfold.

For all the efforts to find growth in the Print segment, they still struggled with a drop in sales volumes in that segment of 6.9%. Magazines and newspapers saw a far sharper decrease, with books helping to mitigate some of that pain. Margins moved much higher in this segment though, with the gross margin up sharply from 17.4% to 24.8% as the business has evolved. This takes operating profit from R55 million to R149.2 million.

In Packaging, there are no such challenges in finding growth. Revenue is up 12.5% and operating profit increased 14.8%. That’s solid.

Finally, on the Education side, revenue fell by 4.2% thanks to a Limpopo order that was below expectations. Operating profit fell sharply from R264 million to R162.6 million. This decrease is driven by not just the drop in revenue, but also by technology investment, an expected credit loss allowance (the joy of waiting for government to pay you) and the amortisation of product development costs. Supplying the public sector with textbooks isn’t an easy business and it’s difficult to forecast exactly what route government will take with the curriculum.

Net working capital pressures are clear, with net working capital cash outflows of R144 million. Government debtors are one of the factors here. Net cash after debt has dropped from R461.1 million to R375.8 million.

On the whole, Novus continues to face uncertainty. They are doing the best they can to navigate a disruptive environment in which nobody is quite sure what the steady state for print vs. digital mediums will look like. The share price may be up 42% in the past 12 months, but it’s really anyone’s guess regarding the level of maintainable earnings for Novus.

Primary Health Properties just won’t give up on the Assura deal (JSE: PHP | JSE: AHR)

Could this end up as a hostile takeover bid?

The game of to-and-fro continues at Assura in the wake of the decision by that company’s board to throw their weight behind the KKR and Stonepeak all-cash offer. Primary Health Properties is trying to convince the board that a merger is the way forward, which is of course a much trickier thing to get right than an all-cash offer. Sadly, the world has many examples of unfulfilled merger promises to refer to when deciding whether to go with a merger or a cash take-private offer.

To try and sweeten the deal and once again get Assura to give them a chance, they’ve made some tweaks to the proposed structure. For example, they will allow Assura to declare a dividend of up to 0.84 pence per share that won’t affect the purchase price. They’ve also reduced the acceptance condition to 50% of the voting rights, aligning it with the KKR and Stonepeak offer.

Perhaps more interestingly for those of us who don’t specifically have a horse in this race, Primary Health has also responded to the comments made by Assura regarding the outcome of their due diligence process and their concerns with a potential merger.

The easy one to address is the level of debt in what would be the combined group, which Assura is worried about over the next two to three years. Primary Health notes that the spike in the leverage ratios would be temporary and that they have a deleveraging plan, with Fitch confirming that the company would remain investment grade following the potential merger. They also try to make the argument that lenders also tend to be more supportive of listed groups rather than private equity structures, although I think that’s a stretch.

One of the other points is really a matter of personal taste, with Assura believing that private healthcare assets are the way to go and Primary Health building their business more around public sector assets. They may as well argue about religion or politics, as investors will have their own preferences here. The response does include a rather spicy comment that Primary Heath has achieved outperformance relative to Assura on total property returns in every year since 2017!

Another risk raised by the Assura board is the potential for regulatory delays. Primary Health has already commenced discussions with regulators and they believe that this issue can be managed if Assura cooperates with them on information flow.

For now, Primary Health is still hoping to get the Assura board to work with them. I just can’t see it happening to be honest, not after the last announcement by the Assura board regarding the KKR and Stonepeak offer. If Primary Health is serious about taking this all the way, then they may have to go the route of a hostile takeover.

To keep the ball rolling, Primary Heath released the prospectus and circular dealing with the issue of shares that would be needed for this merger. They certainly aren’t shy to incur advisory fees in the pursuit of this transaction. But despite all their best efforts, cash remains king and it’s the KKR and Stonepeak offer that ticks that box.

Remgro is seeing earnings growth at Mediclinic (JSE: REM)

The health strategy is a major part of Remgro’s investment case

Although Mediclinic is no longer listed, having been taken private by Remgro, the group continues to put the spotlight on Mediclinic’s earnings as the company is important to Remgro’s overall story.

Hospital groups have been seeing improved results lately and Mediclinic is no different, with the exception of the Swiss operations. More on that to come.

Group revenue is up 5% for the year ended March 2025, while adjusted EBITDA increased by 9%. This pushed adjusted EBITDA margin up from 14.7% to 15.3%. Adjusted earnings increased 21%, so that’s also encouraging. Finally, thanks to strong cash conversion, net debt dropped and the leverage ratio improved from 3.7x to 3.1x.

By now, you’re hopefully wondering what all these adjustments relate to. Sadly, there’s a large impairment of $279 million related to the assets in Switzerland and what Remgro refers to as ongoing changes in the market and regulatory environment in that country. If you included this impairment, you would find that earnings actually swung into a negative position!

The impairment certainly shouldn’t be ignored or swept under the carpet, but it doesn’t reflect the improved operating results that the sector is seeing in South Africa.

Vunani swings into losses (JSE: VUN)

Yes, even on a headline level

Vunani has released a trading statement for the year ended February 2025. It’s not good news I’m afraid, with an expected headline loss per share of between 2.0 cents and 3.5 cents. This is compared to positive HEPS of 7.4 cents in the prior year.

If I look at the interims for the six months to August 2024, they reported a drop in HEPS from 18.2 cents to 6.7 cents. This means that the second half of the year was severely loss-making for the group.

No further details are available at this point, with results due for release on 20 June.

Nibbles:

Director dealings:

The CEO of Barloworld (JSE: BAW) and an associated family trust pledged shares under a funding arrangement worth nearly R130 million.

Two officers of AngloGold Ashanti (JSE: ANG) sold shares worth a total of R72 million that are described as being “in part to fund the tax liability” related to share awards. In other words, that’s a sale over and above the taxable amount.

The CEO of Woolworths (JSE: WHL) sold shares worth over R38 million in a “portfolio rebalancing” – and if the CEO wants to tilt away from the company’s shares when they’ve been underperforming so much, goodness knows I would do the same if I was a shareholder here. Luckily, I’m not.

The CEO of Altron (JSE: AEL) has sold R16.3 million in shares, described as a sale of a portion of his stake to meet personal funding requirements. For context, Altron’s share price is up 67% over 12 months, though it has now come under some broader selling pressure that is worth keeping an eye on.

The Chief Strategy Officer of Investec (JSE: INL | JSE: INP) sold shares to the value of R15 million. That’s a meaty trade.

Here’s another sale of shares by a Discovery (JSE: DSY) director as part of the unwind of a collar structure, this time being a sale by Barry Swartzberg of shares worth R37.3 million. Again, this is a forced sale, so you can’t infer anything about the current valuation.

Here’s an interesting one: James Templeton (CEO of Castleview Property Fund (JSE: CVW) and an overall big-hitter in the property game) has been appointed as the chairman of Accelerate Property Fund (JSE: APF). Personally, I would add this to the bull case for this speculative story at Accelerate.

In case you wondered how the sale of Karooooo (JSE: KRO) shares by founder Zak Calisto is structured, I flicked through the underwriting agreement. It looks like the underwriting banks bought the shares from him at $47.50 per share and will try to place them in the market at $50 per share. They are allowed to place to certain investors at no lower than $48.50 per share. There are six underwriters buying the shares and subsequently placing them with clients, with Standard Bank as the only South African underwriter from what I can see.

In recent months, Ninety One (JSE: NY1 | JSE: N91) has been implementing an important transaction with Sanlam (JSE: SLM). As you may recall, this is part of a long-term active asset management relationship between the companies. The UK piece of the deal, which is the transfer of Sanlam’s UK active asset management business to Ninety One, has now been completed. Ninety One is paying for that business through the issuance of shares.

With everything going on at MAS (JSE: MSP) right now, it’s important that executive management is ready to deal with the wolves at the door. Nadine Bird resigned as CFO with effect from 30 June 2025 and the group has now announced the appointment of Bogdan Oslobeanu as her replacement. He seems to come with tons of experience, as one would hope.

Delta Property Fund (JSE: DLT) continues to chip away at the debt, with an agreement to sell 101 De Korte in Braamfontein for R25 million. The valuation is R27.09 million and the net operating loss for the year ended February 2025 was R2.75 million, so the purchaser clearly has significantly different plans in mind for the property. And in other good news, the sale of Unisa House has been completed and Delta has used those proceeds to settle debt.

Salungano (JSE: SLG) has once again announced a delay to the completion of its financials for the year ended March 2024. No, that isn’t a typo. They initially indicated a mid-June 2025 release but they’ve obviously missed that. They haven’t even given an indication of a new timeline.

Vodacom (JSE: VOD) and Remgro (JSE: REM) have extended the long stop date for the fibre transaction to 4 July 2025. You can expect to see further extensions, as the hearing dates at the Competition Appeal Court have been set down for 22 to 24 July 2025.

Northam Platinum (JSE: NPH) placed R5.7 billion worth of notes under the R15 billion Domestic Medium Term Note Programme. There are three tranches of notes: R2.6 billion maturing in 2028, R0.6 billion maturing in 2029 and R2.5 billion maturing in 2030. Corporates put a lot of effort into designing these tranches, with the goal of maximising capital flexibility and minimising the cost of debt.

Brimstone (JSE: BRT | JSE: BRN) is adding its name to the list of companies that have moved their listing to the General Segment of the Main Board of the JSE. This comes with a far less onerous regulatory burden, hence why so many smaller companies have taken advantage of this.

Ostriches might not fly, but their numbers (and their impact) are soaring. From dusty Karoo farms to global sustainability debates, this big bird is quietly paving the future of meat production. Welcome to the surprising world of ostrich farming.

Once upon a time, before TikTok trends and Temu hauls, personal style was measured in plumage. Big, fluffy, overpriced plumage. In the late 1800s and early 1900s, ostrich feathers were the pinnacle of status, practically the iPhones of the Edwardian wardrobe. And if you wanted to know where the world’s most lucrative fashion fantasy was being farmed, you’d look no further than a sunbaked corner of South Africa called the Klein Karoo.

The big bird boom

This was ground zero for the Great Ostrich Feather Boom, a global trade frenzy so intense it gave rise to a new class of colonial elite known as ostrich barons. These weren’t your average bird farmers: they were feather tycoons. With fortunes plucked from the backs of birds, they built sprawling mansions known as feather palaces, complete with imported chandeliers, Italian tiles, and occasionally, their own train stations. As one does.

South Africa wasn’t alone in chasing the fluffy stuff. The United States, Australia, and even Egypt tried to get in on the action, leading to a global plume-off. But Oudtshoorn had the head start, the birds, and (crucially) the infrastructure. Ostrich farms multiplied at the speed of light – suddenly, everybody and their second cousin was an ostrich farmer. Feathers were harvested, sorted, curled, dyed every shade from blush to canary, and shipped off to Paris, the trendsetting mecca where fashion dreams went to be born or buried.

And in those days, Paris was firmly Team Ostrich.

Plumes exploded across Edwardian high society like glitter at a drag show. Hats weren’t just big back in those days, and fans, boas, jackets, and parasols followed suit. You could argue no woman of means left the house without at least one large, floppy, feathery accessory attached to her outfit.

Feathers even snuck into less glamorous corners of life. They made excellent dusters (thanks to their ability to create static electricity), and were popular in theatre and decor. Basically, if it could be flounced, it probably was.

Barons go bust

But with great demand came great drama. Before long, South Africa had a bit of a monopoly problem. Other countries wanted in, especially those with access to the prized Barbary ostriches of North Africa, who were known for their long, silky, high-value plumes. As rivals set up competing farms, South Africa doubled down by tightening export controls, investing in better breeding programmes, and getting very territorial about its birds.

The stakes were high. The ostrich feather trade was minting fortunes, attracting immigrants, and paying for roads, railways, and quite a few colonial bureaucrats’ salaries. But, like all speculative bubbles, this one was fragile. The entire industry rested on the whims of fashion, which has proven time and again to be a notoriously unstable foundation.

Then came 1914.

With the outbreak of World War I, society collectively decided it had bigger things to worry about than accessorising hats. Luxury spending tanked, imports dried up, and ostrich feathers – once traded at prices higher than gold by weight – suddenly weren’t worth the box they were packed in. Within months, the market collapsed.

Oudtshoorn’s lavish feather palaces were abandoned, sold off, or turned into guest houses (like this example). The Klein Karoo, which had bet big on birds, had to face the uncomfortable reality that the party was over. And like any economy that ties itself too closely to a single commodity (consider this a cautionary tale, oil nations), the fallout was painful.

Feathers, it turns out, aren’t forever.

Protein rather than plumes

In 2023, humanity ate roughly 140 million tons of poultry worldwide. That’s billions of chickens, turkeys and ducks, devoured in curries, nuggets, and Sunday roasts. Poultry now officially rules the meat-eating world, with pork in second place, and beef and veal somewhere further down the buffet table.

While most of us appreciate a good roast, we don’t really love our planet getting roasted in the process. The unfortunate truth is that meat production is a heavyweight in the climate change arena, with beef wearing the champion’s belt for most greenhouse gas emissions per bite. Add deforestation, water use, and a side of ethical anxiety, and you’ve got the perfect recipe for a global rethink. By 2040, it’s projected that 60% of all “meat” consumed will be vegetable-based, lab-grown, or something science hasn’t branded yet, while traditional meat will drop to just 40% of global consumption. Projections certainly aren’t facts, but that’s still a significant shift to consider.

Still, not all traditional meat sources are created equal, especially when it comes to efficiency. Chickens and pigs, for example, produce multiple offspring per breeding season. A single sow can produce as many as 20 piglets a year, while a commercial hen can lay over 300 eggs per breeding season. Meanwhile, your average cow is producing one calf a year, and maybe twins if the stars align.

More animals in a shorter timespan gives pig and poultry producers more data to work with, which means more control over feed, breeding, and genetic optimisation. In the past few decades, this is exactly how they’ve supercharged feed efficiency and meat yield, while lowering production costs and resource use. It’s also no accident that poultry is outpacing pork in global growth. In many regions, pork is off the menu for religious or cultural reasons, making chicken the default choice. But what if there was another option? One that worked for pork and beef-free populations, sipped water like a minimalist, and came with built-in climate creds?

You guessed correctly. It’s the ostrich.

Ostriches might not be invited to many farmyard children’s books (probably because Old MacDonald couldn’t imitate whatever sound an ostrich makes), but they’re quietly making a case for being the next big thing in sustainable meat. First off, they need about a third of the water that cattle do to produce the same amount of meat. They also need less space and less feed, and they are incredibly efficient at converting feed into bodyweight. They hit slaughter weight (around 90kg) in just 10 to 12 months, and reach breeding age at around 2 to 3 years. For context, cattle farmers require two years minimum just to raise one slaughter-ready animal.

The numbers do the talking. One ostrich yields around 27kg of meatafter slaughter – a far cry from the 250kg you’ll get from a full-grown cow. But here’s where things get interesting: a cow produces just one calf per year, while a single ostrich can lay between 40 and 100 eggs in the same timeframe. So that’s 27kg of meat from the bird itself, plus up to 2,700kg from its combined offspring. And because ostriches grow faster and reach slaughter weight in under a year, those chicks will have grown up and hit the processing line in half the time it will take that cow’s lone calf.

Nutritionally, ostrich meat is also superior. It’s got the protein punch and a similar enough flavour and texture to beef but significantly less fat. It’s ideal for those trying to reduce their red meat intake without giving it up entirely, or for communities that need a non-pork protein source with legit sustainability credentials. So while cows continue their slow, methane-heavy waddle into the future, the ostrich might just be sprinting ahead. It’s fast. It’s efficient. It’s resource-light. And most importantly, it doesn’t require us to invent an expensive lab-grown alternative to red meat.

The ostrich barons of the future

Does that mean that South Africa is on the cusp of a second big bird boom? You would think so, having read this far. On paper, ostrich ticks all of the boxes for the meat of the future, and South Africa produces a lot of ostriches – 140,000 of them in 2024. What’s more, we produce some pretty good ostriches too. The Western Cape government owns the first dedicated ostrich research facility in the world. Since the 1970s, the province’s department of agriculture has been quietly running the show, digging into everything from genetics to production to feather quality, all in support of South Africa’s signature bird.

It started with a prestige breeding flock built from top-tier genetic stock donated by local farmers. The deal was that the department would maintain and improve the flock, and in return, the broader industry would benefit. Each year, offspring from this elite group are sold back to farmers, giving them direct access to the fruits of years of research, selective breeding and genetic gains.

But we’re not the only ones in the game. These days, you can find ostrich farms on almost every continent, and in countries and regions where you would never expect to see a big, flightless bird – China, Brazil, Israel, North and South America. Even parts of Europe are catching ostrich farm fever. Production is ramping up in order to meet the growing demand for ostrich leather and feather products, which are making a bit of a comeback in fashionable circles.

My guess, however, is that the real money is to be made in ostrich meat. Once the “exotic meat” angle wears off and Big Ostrich manages to land their sustainability talking points with a sustainably-minded consumer audience (Gen Z, anyone?), I reckon property prices in Oudtshoorn are ready to fly – even if the birds can’t.

About the author: Dominique Olivier

Dominique Olivier is the founder of human.writer, where she uses her love of storytelling and ideation to help brands solve problems.

She is a weekly columnist in Ghost Mail and collaborates with The Finance Ghost on Ghost Mail Weekender, a Sunday publication designed to help you be more interesting.She now also writes a regular column for Daily Maverick.

Fortress gives more details on the direct logistics portfolio in Europe (JSE: FFB)

I always enjoy presentations like these

Fortress Real Estate hosted a property tour in Poland this week, which means that institutional investors were able to see the properties in the flesh. The rest of us plebs are reliant on the online presentation, which the company has at least made available on the website.

The direct logistics portfolio in Fortress is an important part of the story, with an estimated value of completed buildings of €240 million. Recent like-for-like growth in net operating income is 3.0% and they are developing new buildings on a yield of 7.0% to 7.5%.

For those interested, the presentation focuses on the extent of the development opportunity. They’ve completed 320,409sqm of GLA and there’s a further 178,826sqm available for development across five major business parks, so there is still much growth to be unlocked there.

The Karooooo free float looks set to improve (JSE: KRO)

But the market didn’t like the news of founder Zak Calisto selling a portion of his stake

At some point, founders of companies need to liquidate a portion of their holdings and diversify. In these situations, the important thing is to consider how big the remaining stake is, as this shows the level of commitment to ongoing growth. When it comes to Zak Calisto at Karooooo, there’s no shortage of commitment.

He is selling 1.5 million shares at $50 per share, generating a lovely little payday of $75 million (or R1.35 billion). He deserves every cent, having built this company from nothing into a solid multinational group. The really incredible thing is that he will still own 17.9 million shares after this, so he’s selling less than 8% of his total holding! He will be left with roughly a 58% stake in the company.

You can’t just sell a stake of this size through on-market trades, so there are several banks/advisors who are acting as book-running managers to place the shares with large investors. There’s also the option for Calisto to sell up to an additional 225,000 ordinary shares within 30 days, which will depend on how strong the demand for the stock is.

One of Karooooo’s challenges has been relative lack of liquidity in its stock, so this should improve that situation over time.

This didn’t stop the market from throwing a tantrum though, which is either a buying opportunity or just a correction of a particularly wild recent rally. I’ll let you decide:

Another interesting move on the Quantum Foods shareholder register (JSE: QFH)

The technical definition of concert parties becomes interesting here

In South African Takeover Law, the definition of acting in concert is “any action pursuant to an agreement between or among two or more persons, in terms of which any of them co-operate for the purpose of entering or proposing an affected transaction or offer.”

Now, I’m no attorney, but this article that I found on the CDH website certainly is written by attorneys. It makes reference to acts of co-operation and even the concept of masterminding the acquisition of securities, with a fun reference to “a nod and a wink” as well.

Despite what appears to me to be a very broad definition, there are major shareholders in Quantum Foods who are adamant that they are not acting in concert.

On one side, we have Capitalworks Private Equity and Crown Chickens, a related party. On the other, we have Aristotle Africa. Now, Capitalworks and the related party have entered into agreements that will take them to a stake of 15.53% of total shares in issue. On top of this, they’ve entered into a right of first refusal agreement with Aristotle, in which the parties have granted each other such a right to acquire each other’s shares.

A right of first refusal means that if the owner of the shares wants to sell them, they must be offered to the holder of that right first. It’s not like a call option where you can force the holder to sell. The right of first refusal only does something if a decision is made to sell the shares.

These agreements, if triggered, would take the Capitalworks entities to a holding of more than 50% of shares in issue. This would of course lead to a mandatory offer for the remaining shares if they got to that level.

Now here’s the interesting part: Capitalworks has stated that they do not have an intention to make an offer to shareholders, but they reserve the right to do so in future. They’ve also said that they are not acting in concert with Aristotle and that no other agreements are in place between them.

I have zero doubt whatsoever that proper legal advice was taken here. It would’ve been an interesting legal opinion to read, as my guess is that much of the argument hinges on the parties granting each other a right of first refusal i.e. it’s not obvious which party might end up with the higher stake.

If not to facilitate a pathway to control, the agreements could also be there to prevent another major shareholder arriving out of nowhere and taking either of these parties out.

Here is the danger of speculating on potential corporate actions, with the ill-advised speculative buying in 2024 having backfired spectacularly on punters:

That share price chart is possibly the most exciting thing to have happened in the pretty little town of Wellington in the past year.

Renergen has released the ASP Isotopes circular (JSE: REN)

The structure is a scheme of arrangement with a standby offer

As you know by now from previous announcements, ASP Isotopes (which is coming to the JSE at some point this year), is looking to acquire Renergen. The preference is to do this as a scheme of arrangement, which is a mechanism whereby 75% approval ends up being binding all shareholders to the deal. If they fail to get this level of approval, then a standby offer will be triggered in which shareholders who want to sell can tender their shares to ASP Isotopes.

We’ve seen exactly the same thing play out in Barloworld, where the scheme failed and thus a standby offer was triggered. It’s common practice when the acquirer isn’t completely set on acquiring 100% or nothing.

ASP Isotopes itself is a fascinating company. The CEO was recently on Unlock the Stock (video below for those interested), although absolutely zero mention was made of Renergen (not even a small clue!) as this was before the news of the deal broke. It’s a great opportunity to learn more about ASP Isotopes:

There are a number of reasons given for the deal in the circular. But at the end of the day, ASP Isotopes is sitting with cash and Renergen is in need of funding. The team at ASP also has experience in getting difficult assets to work in South Africa, with the Renergen team having missed enough milestones that it’s been very hard to win the trust of the market. Once you layer on the interesting supply/demand dynamics for helium and isotopes, there’s a loose argument to be made that the assets might belong in the same group. But above all, I think this is just opportunistic dealmaking – and why not?

This is structured as a share-for-share offer, with ASP Isotopes currently listed on the NASDAQ and due to list on the JSE. The relative prices based on 16 May put the offer at a premium of 41.3% to the Renergen 30-day VWAP. The independent board of Renergen has been advised by Forvis Mazars as the independent valuation expert. Based on that report, the board sees the offer as unfair but reasonable to shareholders, which means that it is below the estimated fair value, but above the current traded price. I refer you to my opportunistic dealmaking comment. I must also note that the standby offer isn’t even conditional on a minimum acceptance threshold, so ASP Isotopes is happy to pick up any number of Renergen shares at this price.

Irrevocable undertakings have been provided by holders of 35.86% of shares in Renergen, including executive management. Mazi Asset Management led the way here, with a 13.5% stake in Renergen that I’m sure caused them many sleepless nights.

There are a number of conditions precedent for the deal, including AIRSOL agreeing to extend the maturity date for the convertible debentures to at least 31 March 2026. They also need banking and regulatory approvals, along with the approval for ASP Isotopes to list on the JSE.

The general meeting to vote on the scheme has been scheduled for 10 July.

Southern Palladium locks in A$8 million in fresh equity (JSE: SDL)

And at a solid price, too

Junior mining is all about making sure that the market is willing to support you with capital raises. It requires immense capex to get a mine off the ground (or into it, as the case may be!), funded via a spectrum of options from pure equity through to innovative debt and debt-like structures. Royalty agreements and prepaid offtakes also pop up from time to time.

At Southern Palladium, the latest raise of A$8 million is as simple as it gets. They’ve received commitments from one of the largest current shareholders to the tune of A$4.6 million, with this cornerstone investment helping to get a number of new and smaller institutional investors across the line. Institutions tend to move in packs on something like this, relying on the power of a joint due diligence.

Here’s the really good news: the placement is priced at A$0.50 per share, which means a 10.5% premium to the 10-day VWAP. That’s really impressive, as investors usually want to receive shares at a discount before supporting a raise like this.

The proceeds will be used for the Definitive Feasibility Study (DFS) work at Bengwenyama, along with other key milestone like the publication of the optimised Pre-Feasibility Study (PFS) and receipt of a Mining Right.

In junior mining, it’s all about hitting those milestones and having access to funding along the way.

Nibbles:

Director dealings:

Various directors of Hammerson (JSE: HMN) bought shares via a dividend reinvestment plan. The aggregate value of purchases is R800k.

The CFO of Spear REIT (JSE: SEA) bought shares worth R209k.

Recently listed Shuka Minerals (JSE: SKA) has received final authorisation from the Competition and Consumer Protection Commission for the proposed acquisition of 100% of Leopard Exploration and Mining in Zambia. The underlying asset is the Kabwe Mine. To pay for the deal, they will issue $3 million worth of new shares (at a premium to the current market price) and will fund the remaining $1.35 million in cash through a new unsecured and non-dilutive facility. Once issued, the shares will represent 29.99% of total shares in issue. The sellers of Leopard will also receive 2,000,000 share warrants. Importantly, there’s no deferred compensation here, so there is clarity up-front regarding the total acquisition price.

MTN Zakhele Futhi (JSE: MTNZF) closed 42% higher on Thursday based on the news that the board is unwinding the structure. This just shows you how big the liquidity discount is in these B-BBEE entities. The board will soon update investors on exactly how the cash proceeds from the sale of MTN shares will be used to settle debt before being distributed as part of the unwinding of the structure.

Here’s an unusual and interesting director appointment for you: Clientèle (JSE: CLI) has appointed Ian Kirk as what they refer to as a non-independent director. That feels like a typo and that it should be non-executive director. Kirk is of course the ex-CEO of Sanlam and Santam. He serves on several other boards at the moment.

We may be spared from further Italtile (JSE: ITE) director dealings announcements this month, as the non-executive director who is selling pledged shares has resigned from the board with immediate effect.

Sana Bidco, the consortium formed by US private equity firm Kohlberg Kravis Roberts and infrastructure investor Stonepeak, raised its offer to acquire UK healthcare real estate investor Assura in a bidding war with rival suitor Primary Health Properties (PHP). KKR raised the offer price to 52,1 pence per share, valuing the company at £1,7billion (R41 billion). The best and final offer includes declared dividends of 1,68 pence and represents a 39.2% premium over the pre-offer closing price of 13 February 2025. The Assura Board has recommended that shareholders accept the Sana Bidco offer. PHP is considering its options and will make a further announcement in due course but strongly advises Assura shareholders not to act in response to Sana Bidco’s increased offer.

PK Investments has further increased its offer to MAS minorities. The May offer, initially priced at €0.85 per share, was increased to €1.10 and now sits at €1.40 per share. During this period Hyprop undertook a private placement, raising R808,3 million which the company said would be used, in part, to propose a deal that would offer MAS shareholders the option of a share swap or a cash alternative.

Final authorisation has been received by Shuka Minerals from the Competition and Consumer Protection Commission for the proposed acquisition of 100% interest in Zambian mining and exploration company Leopard Exploration and Mining which owns the Kabwe Zinc Mine in Zambia. The transaction value of $3 million will be settled by the issue of 28,640,042 new ordinary shares at £0.07737 per share and a cash component of $1,35 million. The shares will represent on issue, 29.99% of the company’s enlarged issue share capital.

The circular detailing ASP isotopes’ offer to Renergen shareholders has been released – shareholders will vote on the scheme at the General Meeting to be held on 10 July 2025.

Unlisted Companies

Local agri-tech startup Nile has secured US$11,3 million in funding in an investment round led by the Cathay AfricInvest Innovation Fund alongside the Dutch entrepreneurial bank FMO and existing investors. The funds will be used to expand its agricultural inputs marketplace in Southern Africa and introduce innovative financing solutions in partnership with banks.

MyNextCar (MNC), the South African vehicle solutions company, has raised $10 million in its first funding round with support from Emso Asset Management, Bolt (MNC is a key partner in Bolt’s fleet network), Assemble Capital and E2 Investments. The capital will enable MNC to deploy c.1,500 company vehicles, earmarked specifically for Bolt Lite.

SA-H2 Fund, also known as CI3 South Africa, has made an inaugural investment in Hive Hydrogen, South Africa’s first large-scale green ammonia plant based in the Eastern Cape. Hive Hydrogen South Africa is a joint venture between UK-based Hive Energy and SA renewable energy investment company BuiltAfrica. SA-H2 Fund, which is a partnership between climate finance investor Climate Fund Managers and Dutch development financing institution Invest International, has committed up to US$20 million in development funding to complete the final stage of development of the ammonia project. SA-H2 has the option to participate in the construction phase for up to $200 million.

The Public Investment Corporation (PIC), the Industrial Development Corporation (IDC) and the Development Bank of Southern Africa (DBSA) have pledged a total of US$37 million to SA-H2 Fund to finance green hydrogen projects. The PIC will has pledged $17 million while the IDC and DBSA will each invest $10 million over several tranches.

With reference to the mandatory offer by Novus to Mustek shareholders in November 2024, Novus has acquired on the open market, 2,031,438 Mustek shares (a 3.53% stake) at R13.00 per share in a transaction valued at R26,41 million. The shares increase the company’s interest in Mustek to 38.6% which together with concert parties constitutes c.58.89% of the issued share capital in Mustek.

Final authorisation has been received by Shuka Minerals from the Competition and Consumer Protection Commission for the proposed acquisition of 100% interest in Zambian mining and exploration company Leopard Exploration and Mining, which owns the Kabwe Zinc Mine in Zambia. Shuka Minerals will issue 28,640,042 new ordinary shares at £0.07737 per share. The shares will represent on issue, 29.99% of the company’s enlarged issue share capital.

MTN Zakhele Futhi (RF) – MTN’s B-BBEE vehicle has completed an accelerated bookbuild placing 23,768,040 MTN shares (1.26% stake) at R128.00 a share in a private placement for gross proceeds of R3 billion. MTNZF intends to use the net proceeds of the placement to settle its outstanding preference share funding and related costs and to distribute the balance of proceeds to its shareholders.

In an equity placement, Spear REIT has raised R749 million which will be utilised in the short term to settle debt and to fund further solar projects. The group will issue 74,900,000 shares at R10 per share reflecting a premium of 1.06% to 30-day VWAP. Following the placement, the loan to value ratio of Spear will be within a range of 18%-20%.

Lighthouse Properties has raised R400 million in an equity raise, issuing 48,780,487 shares at R8.20 per share. The accelerated bookbuild was initially set at R100 million. Lighthouse signed an exclusivity agreement in February this year for the acquisition of a further mall in Spain which is expected to close during June, and which will increase the company’s exposure to Iberia to c.86%. Funds raised will be allocated to this and value accretive investments as they arise.

Oasis Crescent Property Fund will issue 350,785 new units to shareholders receiving the scrip dividend option in lieu of a final cash dividend, resulting in a capitalisation of the distributable retained profits in the company of R10,56 million.

Southern Palladium has undertaken a capital raising by way of a share placement. The company placed 16 million new fully paid ordinary shares at A$0.50 per share to raise A$8 million before costs. The shares were issued at a 10.5% premium to the 10-day VWAP of A$0.45 per share. The funds provide balance sheet strength to advance the next phase of Definitive Feasibility Study work and staged mine development at Bengwenyama.

Karooooo CEO Zak Calisto launched an underwritten secondary public offering of 1,500,000 Karooooo shares at US$50.00 per share for total gross proceeds of c.$75 million. The offering will close on 13 June 2025. The underwriters have a 30-day option to purchase up to an additional 225,000 shares at the public offering price.

Sappi has upgraded its presence in North America with its listing on the OTCQX with effect from 11 June 2025. Sappi’s current shareholder split is c. 70% South African and 30% non-South Africa.

This week the following companies announced the repurchase of shares:

Pan African Resources is to undertake a share buyback programme to purchase up to R200 million (c. approximately US11,1 million) ordinary shares in the market. The repurchase will commence on 17 June 2025.

In its annual financial statements released in August 2024, South32 announced that it would increase its capital management programme by US$200 million, to be returned via an on-market share buy-back. This week 756,925 shares were repurchased at an aggregate cost of A$2,31 million.

In October 2024, Anheuser-Busch InBev announced a US$2 billion share buy-back programme to be executed within the next 12 months which will result in the repurchase of c.31,7 million shares. The shares acquired will be kept as treasury shares to fulfil future share delivery commitments under the group’s stock ownership plans. During the period 2 to 6 June 2025, the group repurchased 350,000 shares for €21,75 million.

On 19 February 2025, Glencore plc announced the commencement of a new US$1 billion share buyback programme, with the intended completion by the time of the Group’s interim results announcement in August 2025. This week the company repurchased 16,250,000 shares at an average price per share of £2.91 for an aggregate £47,33 million.

Hammerson plc continued with its programme to purchase its ordinary shares up to a maximum consideration of £140 million. The sole purpose of the buyback programme is to reduce the company’s share capital. This week the company repurchased 253,632 shares at an average price per share of 292 pence for an aggregate £739,934.

In line with its share buyback programme announced in March 2024, British American Tobacco plc this week repurchased a further 580,051 shares at an average price of £35.02 per share for an aggregate £20,31 million.

During the period 2 to 6 June 2025, Prosus repurchased a further 4,427,203 Prosus shares for an aggregate €204,27 million and Naspers, a further 251,381 Naspers shares for a total consideration of R1,33 billion.

Two companies issued profit warnings this week: Aveng and KAP.

During the week three companies issued or withdrew cautionary notices: TeleMasters, Trustco and Renergen.

FirstAlly Capital has acquired a 60% stake in Mines.io Nigeria, operating under the brand name Migo. The Nigerian fintech focuses on delivering digital credit solutions using AI and machine learning. Financial terms of the deal were not disclosed.

ASX-listed Dalaroo Metals has signed a joint venture agreement with Reflex Exploration to acquire up to an 80% stake in the Bongouanou Gold Project in the Sefwi-Comé Birimian Greenstone Belts in Côte d’Ivoire.

Canadian solar energy company, Solar Panda, has acquired VITALITE Zambia for an undisclosed sum. The acquisition expands Solar Panda’s operational footprint into Southern Africa. VITALITE was the first company to introduce PAYGO solar home systems in Zambia.

uMunthu Investment Company II (managed by Goodwell Investments) has acquired a 26% stake in Nigeria’s Hinckley Ewaste Recycling. No financial terms were disclosed.

Wafa Assurance has submitted and mandatory tender offer to acquire up to 100% of Delta Insurance at EGP40 per share. The transaction is valued at a total of EGP5 billion and requires a minimum acceptance of 51%. Wafa and Axa Egypt made a non-binding offer to acquire Delta in December 2024, but Axa pulled out of the offer in May, which triggered a six-month mandatory cooling-off period. Should the transaction be successful, Wafa plans to delist Delta from the EGX.

Africa-focused private investment firm, Silverbacks holdings, has partially exited its stake in OmniRetail and secured a 5x return on its initial investment. The exit follows OmniRetail’s recent US$20 million Series A funding round led by Norfund and Timon Capital.

The International Finance Corporation is currently considering a US$10 million equity investment in Senegal’s AI healthcare startup, Kera Health Platforms. The investment is currently pending approval.

Kendrick Resources has entered into a 60-day option and joint venture agreement with Cooperlemon Consultancy for the exploration and, if appropriate, the development of the Blue Fox Licence, 34412-HQ-LEL located in Northwest Zambia.

At times, the move of a potential takeover bid comes about when least expected, and requires management and directors of companies to make quick and informed decisions. For South African companies, where the legal framework is shaped by the Companies Act 71 of 2008 (the Companies Act) and accompanying Takeover Regulations, responding strategically to a takeover attempt requires both legal acumen and commercial foresight. This article explores, at high-level, how companies can navigate such turbulent waters, balancing their statutory obligations with strategic imperatives while remaining neutral and objective.

Understanding the legal framework

The Companies Act and the common law provide the overarching foundation for corporate governance in South Africa. The law imposes fiduciary duties on directors, most notably under section 76, which requires directors to act in the best interests of the company and its shareholders. These duties become more critical in a takeover bid, where there is increased potential for conflicts of interest and divergent views and interests among a company’s stakeholders.

In addition, the Takeover Regulations play a pivotal role. They ensure transparency and fairness during takeover bids by mandating, amongst other things, disclosures of material information and restricting defensive measures that could frustrate the bid or otherwise deprive shareholders of an opportunity to fairly evaluate the bid and decide on its merits.

Together, the Companies Act and the Takeover Regulations ensure that a company’s response to a takeover is both legally compliant and geared towards protecting the collective interests of its shareholders.

Strategic defensive measures

When a takeover attempt is launched, the board of the target company must carefully assess the offer. The primary obligation is to evaluate the bid’s merits objectively, considering both immediate financial implications and long-term strategic impacts. At the heart of this evaluation lies the board’s duty to act impartially and in the best interest of all shareholders.

Part of the strategic response is to seek an independent expert opinion. This not only reinforces the board’s objectivity, but also provides shareholders with a robust analysis of the offer’s fairness. The expert’s assessment can cover valuations, the strategic rationale behind the bid, and the potential impact on the company’s prospects. By grounding their response in independent analysis, the board can help ensure that its recommendations are both credible and legally sound.

Another important strategic measure is the careful management of information disclosure. Under the Takeover Regulations, the target company is required to communicate material developments promptly and accurately to its shareholders. This includes circulating a response that outlines the board’s position on the bid, any concerns regarding potential conflicts of interest, and recommendations for shareholders. Transparency is crucial in preventing misinformation and ensuring that all stakeholders are equipped to make informed decisions.

Neutrality and fiduciary duties

Central to the strategic response is the board’s commitment to observe neutrality. The Companies Act, particularly section 76, emphasises that directors must not favour one outcome over another if doing so would compromise their duty to the company as a whole. In practical terms, this means that defensive measures should not be implemented solely to frustrate the bid, unless such measures have been explicitly approved by shareholders in a general meeting.

This principle of neutrality is reflected in the prohibition on defensive actions without shareholder consent. The Takeover Regulations restrict the board from taking measures such as issuing new shares or disposing of key assets during the offer period unless the shareholders have sanctioned these actions. This safeguard is designed to prevent management from unilaterally altering the company’s structure to deter the takeover attempt.

The Takeover Regulations ensure that directors are able to adequately comply with their fiduciary duties. They require that an Independent Board be set up to manage all aspects of the potential takeover, including negotiating the offer and evaluating its reasonableness; this is especially relevant when the directors are potentially conflicted. The primary purpose of the Independent Board is to ensure that the bid offer is fairly evaluated by independent directors whose assessment would not be swayed by personal interests or biases.

Case in point: BHP and Anglo American

As a case in point, the strategic manoeuvrings observed in the BHP/Anglo American deal are worth pointing out. In that instance, Anglo American embarked on a series of defensive strategies in response to an unsolicited bid from BHP. Although the specifics of the BHP/Anglo transaction remain a matter of public debate, the case illustrates several key points that are applicable to any takeover scenario.

The BHP/Anglo American case underscores the importance of a well-structured and transparent response. The board’s decision to engage with independent advisors, coupled with a clear communication strategy to shareholders, was critical in ensuring that the company’s actions were seen as fair and balanced. Moreover, by avoiding overtly aggressive defensive measures, Anglo American was able to preserve the integrity of its governance framework and maintain confidence among its stakeholders.

Balancing commercial and legal considerations

In formulating a strategic response to a takeover, companies must strike a delicate balance between commercial imperatives and legal obligations. On one hand, there is the need to safeguard shareholder value and ensure that any countermeasures do not inadvertently diminish the company’s market position or prospects. On the other hand, adherence to legal standards and regulatory guidelines is non-negotiable.

A comprehensive approach involves a thorough due diligence process that evaluates the bid from multiple perspectives. This includes assessing the financial valuation, understanding the bidder’s strategic objectives, and considering the potential impact on existing operations and long-term growth. Equally important is the need for proactive engagement with legal and financial advisors whose expertise can help navigate the complexities of both the Companies Act and the Takeover Regulations.

Practical guidance

For companies facing a takeover situation, several practical steps are recommended:

Engage independent advisors early: obtain unbiased valuations and strategic assessments to support the board’s decision-making process.

Ensure transparent communication: draft response circulars and disclosures that comply with regulatory requirements and clearly articulate the board’s rationale.