")

Solid earnings at Choppies, but a flat dividend (JSE: CHP)

It’s somewhat hilarious that this has been the pick of the retailers in 2025

I’m not sure what you had on your bingo card coming into this year, but I certainly didn’t have an expectation for Choppies to be massively outperforming the South African retailers. Yet here we are, with a year-to-date move of 26% at a time when most local retailers are firmly in the red!

The results for the six months to December 2024 give some support to this move. Revenue was up by 19.4%, with sales in like-for-like stores up by 15.1%. Although gross profit margin came under some pressure with a decline of 10 basis points due to promotional behaviour by competitors, they still saw a strong increase in gross profit of 18.7%.

The shine does come off once we take expenses into account, with a 22.9% increase driven by a number of factors including forex losses on lease liabilities and the loss on sale of the Zimbabwe segment. Some of this sounds non-recurring in nature.

Operating profit was up just 6.1% due to the jump in expenses, with operating margin down 50 basis points to 4.06%. In terms of HEPS, which reverses out those irritating impairments and other non-recurring issues, they were up 32.7%.

Tempting as it may be to focus on the HEPS number, it’s worth pointing out that net cash from operating activities fell by 6% and the dividend was flat at 1.6 thebe per share. Still, the market is clearly pricing in growth for this business!

Investec’s UK business has negatively impacted their latest numbers (JSE: INL | JSE: INP)

To be fair, they faced a demanding base period in the UK

Investec has released a pre-close update dealing with the year ending 31 March 2025. This is designed to update the market on performance before heading into a closed period which only ends when results are released. Not all companies do this, but it’s always good to see more disclosure rather than less.

The group’s pre-provision operating profit is between 5% and 12% higher than the prior year. That sounds great, yet HEPS is between 8% lower and just 1% higher. Impairments had a significant impact on the numbers, even though the credit loss ratio is still within the through-the-cycle range of 25 basis points to 45 basis points.

If you dig deeper, you’ll see that the South African business expects a credit loss ratio around the lower end of their through-the-cycle range of 15 basis points to 35 basis points. In the UK, the expected credit loss ratio is at the upper end of the guided range of 50 basis points to 60 basis points. The impact of specific impairments in the UK business has hurt them, although the Specialist Bank segment was also trying to grow against a base year in which operating profit had increased 33.9%. When you consider that the latest performance is a move of -4% to +4% in the UK, the two-year view is still strong in that business.

Notably, the cost-to-income ratio improved, so cost control was decent. This confirms that it was firmly an impairments story that took the shine off the growth numbers. Another highlight worth mentioning is the 14.5% increase in funds under management in Southern Africa, boosted by net inflows.

Group return on equity is between 13% and 14%, which is at the lower end of the medium-term target range of 13% to 17%.

Momentum shows what happens when everything goes right (JSE: MTM)

The share price closed almost 11% higher on the day of results

Momentum has released results for the six months to December. They are certainly living up to their name, as the group enjoyed a period in which its key business units delivered strong growth.

Normalised headline earnings per share increased by a delicious 48%, followed closely by the interim dividend with 42% growth. Those are exceptional numbers, leading to return on embedded value per share jumping from 11.6% to 16.8%.

With underlying drivers of performance like improved persistency in life insurance, better underwriting profits in the short-term business and favourable market returns, there’s a lot to smile about here. Even the operating loss in India was reduced!

Despite this, the embedded value per share of R39.29 is significantly higher than the share price of R32.68. This suggests that there might be more room for this share price to run, even though its up 58% over 12 months. Alternatively, you could argue that the market is worried about how maintainable these returns are.

The group has affirmed its financial ambitions for 2027, which include return on equity of 20%. Considering they just banked a return on equity of 24.6%, this perhaps suggests that conditions in this period were just unsustainably good. The share price trading at such a discount to embedded value would support this view. South African investors do tend to have a “it’s too good to be true” mentality, given the last decade or so on our market.

Shaftesbury is allowing a minority shareholder into Covent Garden (JSE: SHC)

The order of events on SENS was rather funny

Before the market opened on Thursday, Shaftesbury released a “response to market speculation” that confirmed that discussions with underway with Norges Bank Investment Management (NBIM) regarding a potential sale of 25% of Covent Garden. That announcement went on to say that there’s no certainty of a transaction being agreed.

Certainty came rather quickly, as just two hours later there was an announcement of the full terms of the deal!

So, onto the deal we go. Shaftesbury will sell 25% of Covent Garden to NBIM for £570 million, which values the asset in line with its balance sheet value as at December 2024. This is an iconic property in the West End of London, which has to be one of the best places in the world to have property. This is why the net initial yield is just 3.6%, which tells you how low a return investors are willing to accept for the underlying risk – or perceived lack thereof.

This is a NAV-neutral deal, as they are selling the stake based on current book value i.e. they are just exchanging an equity investment for cash. But from an earnings perspective, they note that this is accretive as they are unlocking capital through selling down the stake and still earning fee income based on the management of the property.

Shaftesbury has a solid balance sheet, but they will still use the proceeds to reduce debt. The remaining cash will be deployed as opportunities arise for acquisitions and portfolio refurbishment and improvement projects.

South Ocean Holdings had a horrible time in 2024 (JSE: SOH)

Revenue is pretty much the only thing that went up

When a set of results starts with a 9% increase in revenue, you would expect to see the rest of the income statement looking good as well. Alas, South Ocean Holdings suffered an ugly drop in HEPS of 62%. The dividend was 50% down. Clearly, the year to December 2024 didn’t go well.

Things went wrong right near the top of the income statement, as gross profit margin plummeted from 9.7% to 5.8%. This is a low margin business that just got a whole lot lower. Despite revenue increasing, gross profit itself was down 35% and the rest of the numbers didn’t stand much of a chance from there.

The pressure is being caused by imported goods in the market. That’s really bad news, as it suggests that this isn’t a temporary issue. To add to the worries, the overdraft facility has ballooned from R224 million to R417 million and is due for renewal during July 2025. Ongoing support from the bankers is required here.

The group is still profitable at least, so that should hopefully keep the bankers at bay. As for shareholders though, it’s a rough situation. This sounds like a structural problem rather than a temporary one.

Nibbles:

- Director dealings:

- The former CEO of Standard Bank (JSE: SBK) sold non-redeemable preference shares in the bank worth R2.4 million.

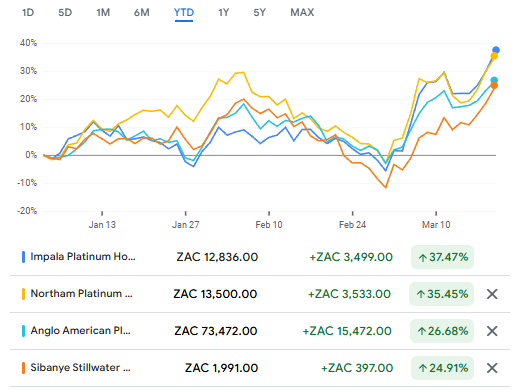

- The company secretary of Impala Platinum (JSE: IMP) sold shares worth R1.2 million.

- The CEO of Putprop (JSE: PPR) bought shares worth R212k.

- Des de Beer bought shares in Lighthouse Properties (JSE: LTE) worth R183k.

- Libstar (JSE: LBR), which has indicated to the market that they are considering various strategic options, announced the appointment of ex-Pioneer Foods CEO Tertius Carstens to the board as a non-executive director.

- AngloGold Ashanti (JSE: ANG) is busy with site tours for analysts. After releasing a presentation earlier in the week dealing with the Obuasi mine, there’s now one on Sukari. If you enjoy (and understand) the more technical elements of mining, you’ll find them on the home page of the AngloGold website.

- Anglo American Platinum (JSE: AMS) is planning a change of name, so they are trying to make it as clear as possible to the market that they are splitting from Anglo American (JSE: AGL). The proposed new name is Valterra Platinum.

- Wesizwe Platinum (JSE: WEZ) is suffering a delay in the publication of its 2024 financials. This is due to a cyber attack towards the end of 2024, which impacted the financial systems of the company.

- In the incredibly unlikely event that you are itching for Globe Trade Centre (JSE: GTC) to release the 2024 annual report, you’ll have to wait a bit longer as it’s scheduled for 29 April. The Q1 2025 release has been pushed out to 29 May.

")

")