In this edition of Ghost Bites:

- Afrimat is selling off some quarries and concrete plants for R215 million

- Fortress Real Estate is ticking over nicely

- MTN sets out Ambition 30 at its Capital Markets Day

- SPAR hits rock bottom – hopefully

Afrimat is selling off some quarries and concrete plants for R215 million (JSE: AFT)

They needed to do this from a regulatory perspective anyway, but it’s a welcome injection of capital

Afrimat’s share price is down 23.6% year-to-date, with this previous market darling now suffering at the hands of investors. Or perhaps investors are suffering at the hands of Afrimat?

Either way, it’s not pretty.

There are many reasons for the decline, with Afrimat’s recent reporting having demonstrated the perfect storm faced by the company.

I must disclose that I recently bought into Afrimat after it was announced that the smelters are being thrown a lifeline by NERSA and Eskom. Time will tell whether I made the right call.

In the meantime, the latest news at Afrimat is that they have found a buyer for certain general aggregates quarries and readymix concrete plants. They needed to divest these assets as part of the conditional approval by the Competition Tribunal for the acquisition of Lafarge South Africa.

The buyer is Saturc and the price on the table is R215 million. A cash amount of R160 million is payable on closing (1 July 2026) and the remaining R55 million is payable over three years. That’s a fair split.

The announcement doesn’t give any financial information on the assets in question.

Ghost Bite: It would’ve been nice to have information on the profitability of these assets. My suspicion is that because Afrimat was a forced seller here, the economics of the deal probably aren’t amazing. On the plus side, it’s an injection of cash at a time when Afrimat could do with some capital flexibility.

Fortress Real Estate is ticking over nicely (JSE: FFB)

They are delivering real growth for investors

Fortress Real Estate has provided a pre-close update dealing with the year ending June 2026. Remember, this is a complex portfolio that includes directly held assets in South Africa and Central and Eastern Europe (CEE) worth R36 billion, as well as a R14.4 billion stake in NEPI Rockcastle (JSE: NRP). There is also a small non-core portfolio of office properties worth R681 million.

The direct portfolio is strongly weighted towards logistics properties (R24.1 billion). With vacancy levels in South Africa and CEE of 1.4% and 1.8% respectively, these assets continue to provide a dependable income stream. Vacancy rates tend to be lumpy due to the size of the underlying warehouses. For example, the increase in the vacancy level in South Africa from 0.3% to 1.4% is thanks almost entirely to one warehouse at Eastport Logistics Park.

The retail portfolio is only in South Africa. Like-for-like tenant turnover growth of 4.2% seems reasonable in the context of recent numbers we’ve seen from retailers. The vacancy rate is just 0.8%, excluding the recently acquired 51% stake in Balfour Mall, where the vacancy rate is extremely high at 45%. This is clearly a property in need of a turnaround strategy, but they got it on a yield of 10% based on existing tenants. No value was placed on the vacant 45%, so the upside potential is clear!

In the non-core office portfolio, vacancies improved from 25.7% to 22.1%. Although Fortress likes to sweep this portfolio under the carpet, only two of the 14 properties are classified as held for sale. Perhaps the market is just too weak for them to be offloaded any faster?

Speaking of disposals, Fortress isn’t shy to recycle capital. They have disposed of R362.4 million worth of properties in this financial year, with the pricing reflecting a 5.5% premium to book value. Properties worth R277.4 million are currently classified as held for sale.

This is important, particularly as Fortress engages in ongoing development activities to grow the portfolio. Capital discipline is a critical element of this strategy. The development projects are a mix of speculative builds (no confirmed tenant yet) and builds to spec for confirmed long-term tenants.

To help fund these activities, Fortress has a successful DMTN programme on the JSE that allows it to raise debt. For example, they raised R1.6 billion earlier this year in the form of a 7-year note. The current loan-to-value ratio at the fund is roughly 38.8%.

Fortress Real Estate’s guidance for FY26 has been reaffirmed. They expect a distribution of 176.48 cents per share, which would be 8.6% higher than FY25.

Looking ahead to FY27, there’s a further 7.4% increase. The nuance is that the FY27 forecast is based on total distributable earnings, not the distribution per share. In other words, that percentage would change if Fortress either issues or repurchases shares.

Ghost Bite: It’s less about the exact forecast and more about the approximate growth rate. These are high single-digit increases, which means that Fortress is doing a great job of providing real returns to investors (i.e. in excess of inflation).

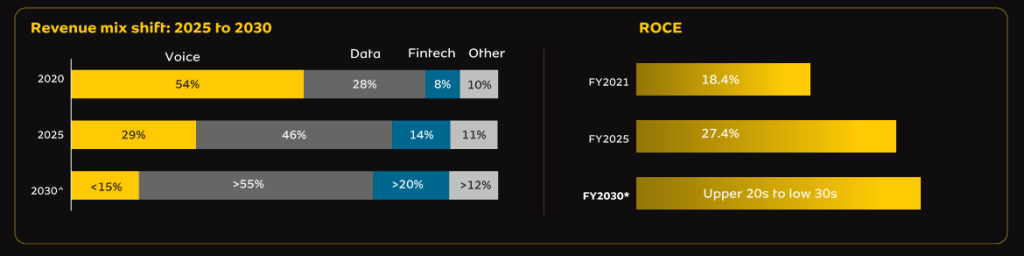

MTN sets out Ambition 30 (JSE: MTN)

And if there’s one thing they aren’t short of, it’s ambition!

MTN is hosting a Capital Markets Day this week. It’s actually a two-day event, which shows you how much they need to get through!

Naturally, if you want the full details, then you need to check out this link and work through the slides. I always recommend that you spend some time doing this, as there is much to learn from the Capital Markets Day decks.

This particular event is to take the market through the new medium-term targets. We’ve now moved from Ambition 2025 to Ambition 2030. The starting point for Ambition 2025 was the 2020 financial year, which was a Covid-infested mess, so the five-year track record of delivery was obviously given some additional help by the choice of base period.

Still, MTN deserves a lot of credit – they’ve made immense progress in recent years. Subscribers jumped from 258 million in 2020 to 307 million in 2025. Adjusted ROE climbed from 17.0% to 25.6%. HoldCo leverage is perhaps the most impressive story, down from 2.2x to 1.3x!

Today, just 16% of HoldCo debt is non-rand denominated. Back in 2020, that number was 48%. MTN has transitioned from fighting for its life to telling an exciting growth story.

The underpin of Ambition 2030 won’t be a surprise to you. Africa is an extremely fast-growing region that offers a mix of economic and population growth. More humans require more connectivity over time. Therein lies the opportunity, with financial inclusion and AI as further tailwinds.

Here’s a number that really brings that message home: smartphone penetration in Africa is expected to jump from 53% to 2025 to 84% in 2030. Now imagine what this means from a FinTech perspective, as Africa continues to move from cash to digital transactions.

There are other growth engines as well, like MTN’s modest share of the total addressable market for SMEs on the continent.

To address this opportunity, MTN is organising itself around three platforms. The first is MTN itself, which delivers connectivity. The MoMo business is the FinTech play, and I’m pretty sure the next few years will see a separate listing of that business as a value unlock. The third is bayobab for digital infrastructure (the recent IHS acquisition and other services).

What does this all mean from a financial perspective?

The expectation is that service revenue will grow by at least high teens over this forecast period. This expect this to drive margin expansion as well. But here’s the chart that I think tells the story the best, extracted from the financial presentation at the event:

Ghost Bite: We live in a very exciting place. Africa is a risky business environment where governments do their very best to make it tough to do business. But when governments just stay out of the way, companies like MTN can unlock serious growth. Macro tailwinds on the continent help as well – long may they last!

SPAR hits rock bottom – hopefully (JSE: SPP)

The latest financials show the extent of the problems

SPAR released results for the 26 weeks to 27 March 2026. The market had already been warned that they are shocking. Now we can see just how rough SPAR’s reality is, with an operating profit margin in Southern Africa of a paper-thin 0.5%!

Let’s start right at the top, where revenue from continuing operations increased by 3.6%. Group gross profit margin dipped from 10.7% to 10.5%. Operating profit has tanked from R1.35 billion to R741 million. HEPS is even worse, down 53.9% to 199.9 cents. Sigh.

The balance sheet is also a major concern, with group net debt up from R5.4 billion to R7.3 billion. Some of this is due to the timing of creditor payments, but there’s also a worrying story about weak EBITDA and how this has impacted group cash flow.

SPAR’s group balance sheet is running a leverage ratio of 2.73x. Leverage in South Africa is too spicy for my liking at 3.29x, with little headroom vs. the covenant of 3.50x.

The segmental analysis really tells the story here.

The Southern Africa business was impacted by many factors, including the ongoing woes of the KZN distribution centre (a R123 million impact on operating profit) and what the group describes as “promotional overspend” on Black Friday (a R212 million impact). There are also concerning metrics regarding the health of the independent retailers and the resultant impact on SPAR’s debtor book.

There was very little revenue growth in Southern Africa to cushion the business against these blows. Revenue was up just 1.7%. Grocery and liquor wholesale revenue could only manage 1.1%, while Build it was good for 1.3% growth and SPAR Health achieved an impressive 26.1%.

Here’s the real crisis: gross profit in South Africa was down 1.4%, yet operating expenses jumped by 18.5%. This absolutely crushed operating profit, down 60% to R396 million.

Retailer loyalty went backwards on a rolling 12-month basis, dipping from 78.9% to 78.5%. The relationship with the independent retailers remains very difficult, although the final months of the reporting period saw a stabilisation in the loyalty rate.

If we really dig for a highlight, then we can consider SPAR Rewards with sales growth of 9.3% year-on-year.

In Ireland, things were better than in Southern Africa, although that’s hardly saying much. Revenue was up 2.2% in euros, with gross margin up 20 basis points to 13.7%. Operating profit inched higher with a 0.8% growth rate. Thanks to a decrease in debt, there was a decline of 22.8% in net interest.

I don’t think anyone really cares about the joint venture in Sri Lanka, but I’ll mention it for completeness. Revenue growth was 7.6%, but operating profit fell year-on-year. With 12 corporate stores and 13 independent retailers, I’m not sure why they are bothering in that country.

Is the day darkest before the dawn?

Well, I keep asking SPAR for a Capital Markets Day to give the market access to the divisional executives and their plans. In the absence of such an event, we must rely on the strategic commentary provided by SPAR in the announcement. With the share price closing 5.9% higher on the day, the market seemed to be cautiously optimistic.

Aside from the SAP Finance go-live in the next period (I’m sure that will be a nervous moment), the group is taking steps to control marketing spend (there’s a new return on investment framework) and drive better procurement in an effort to protect margins and working capital.

They are also going to (finally) figure out a local store proposition on SPAR2U. Literally the only differentiator at SPAR is the community-focused nature of the franchisees. If they can find a way to deliver that value proposition digitally on a store-by-store basis, they just might have a chance.

I would certainly be a customer of that effort, if they get it right. I have an excellent SPAR a couple of kilometres from my house, but I have to go past a Woolworths Food and ignore the Sixty60 alternative in order to go there. SPAR2U solves that gap.

In the meantime, there’s obviously no interim dividend for shareholders. SPAR needs every cent they can get as they head into the second half of the year.

Ghost Bite: My tiny speculative position on SPAR has gotten a lot smaller. And I’m not adding to it until I see more compelling strategic plans from the group. SPAR2U is the ultimate test for me. Personalising the digital experience for each store won’t be easy. If they can achieve that level of execution and data integration with stores, then SPAR just might have a chance. If not, then it’s hard to see much of a future here.

Results of previous poll:

Nibbles:

- Director dealings:

- Although the CEO of AVI (JSE: AVI) opted to sell only the taxable portion of his share award, a different director sold his entire award worth almost R2 million.

- Four directors of Spear REIT (JSE: SEA) elected the dividend reinvestment alternative to the value of R465k. This isn’t quite as bullish a signal as a normal on-market trade, but it still speaks to alignment with management.

- An entity associated with the CEO of Africa Bitcoin Corporation (JSE: BAC) bought shares worth almost R250k.

- Shuka Minerals (JSE: SKA) announced further updates from the drilling at Kabwe Zinc Mine. As usual, unless you’re a geologist, the announcement will mean almost nothing to you. I always skip to the CEO commentary in these scenarios, as I know absolutely nothing about mining geology. It appears as though the CEO is pleased overall, so that’s encouraging.