In this edition of Ghost Bites:

- Attacq’s precinct-focused approach is still paying off

- FirstRand’s business is performing well – outside of the UK at least

- Grindrod’s Port and Terminals business is the highlight of this period

- Labat Africa declares a dividend and promises shareholder engagement

- Sibanye-Stillwater gives investors plenty to chew on at the Capital Markets Day

- Vunani has swung into profitability, with Fairheads as the anchor of the story

Attacq’s precinct-focused approach is still paying off (JSE: ATT)

The pre-close update looks encouraging

In Attacq’s pre-close update for the year ending June 2026, they gave performance highlights based on the 10 months to April 2026, as well as the most important news of all: they are on track to achieve the guided growth in distributable income per share of 11% to 14%.

This is being driven by factors like a 4.8% increase in the weighted average trading density in the portfolio, along with solid occupancy rates. They’ve even managed foot count growth of 1.5% on a rolling 12-month basis, despite all the risks of eCommerce adoption!

Attacq always has significant development projects on the boil. Waterfall City still offers plenty of opportunity across different asset classes. They believe in the precinct strategy and they aren’t afraid to take on development risk.

For example, the Gateway East office development has only signed leases for 37.6% of Gross Lettable Area thus far, with another 27.5% awaiting signature. It’s difficult to fully de-risk these types of developments, unlike in the logistics space where warehouses are often built to client spec based on long-term leases. But even among the warehouses, Attacq takes on some speculative developments for more generic buildings.

As a sign of the times, they are also busy with data centre developments in the precinct!

The balance sheet remains in good health, with a gearing ratio of 25.1% vs. 25.3% as at June 2025.

Ghost Bite: The collapse in Gauteng infrastructure creates opportunities for property funds to focus on making things as good as possible in a particular area. Attacq is one of the best examples of this strategy in action.

FirstRand’s business is performing well – outside of the UK at least (JSE: FSR)

The group is doing well in SA and Africa

FirstRand has given shareholders more information on the performance for the year ending 30 June 2026. As most companies have done, they kicked off the announcement by reminding investors of the macroeconomic disruption of the past few months.

But the biggest headache of the period by far had nothing to do with oil (or even Iran). The FCA UK motor redress scheme was the shock for FirstRand investors this year, with a further provision of £510 million raised during the year. This takes the total provision to £750 million.

This provision means that normalised earnings will drop by below 4% and 9%, with Return on Equity (ROE) below the bottom end of the targeted range.

Naturally, the next thing they want you to do is strip out this most unfortunate event. If you do that, they are in line with guidance for both growth in normalised earnings and ROE.

FirstRand is getting out of the entire UK business, so perhaps just ignoring it and moving on is the right approach for investors. Heavy-handed regulators in low-growth economies do no favours for their countries, with such authoritarian stupidity as common in Europe or the UK as it is in South Africa.

Focusing on the continuing operations, we reach the section of this announcement that is heavy on narrative and light on numbers, as is usually the case at the banks.

Thanks to strong growth in advances, net interest income (NII) is slightly higher than guidance, a pleasant surprise given the overall caution in the market among borrowers. Wesbank has been a major driver here, as has the rest of Africa. The credit loss ratio is expected to be at the lower end of the through-the-cycle range, so that’s a further boost to the lending business.

The non-interest revenue (NIR) side of the group is usually a strength at FirstRand, with this period once again delivering a positive performance in trading, investment and other sources of income. Interestingly, the private equity business had fewer realisations (crystallised sales of assets) in the second half vs. the first half.

Operating expenses are slightly higher than guided, with a few major projects taking them above where they wanted to be.

Results are due for release on 10 September 2026, at which time we will have all the details.

Ghost Bite: FirstRand can officially be added to the list of local companies that should’ve just focused on regions they fully understand.

Grindrod’s Port and Terminals business is the highlight of this period (JSE: GND)

This is the power of a focused strategy

After the simplification of Grindrod’s group, they are changing their approach to their financials. The segments going forwards will be Port and Terminals, Logistics and Group, so all the non-core stuff will be reported in Group.

In an update for the five months to May 2026, Grindrod highlighted a jump in earnings at the Port of Maputo of 23.3%. EBITDA margin in the Port and Terminals segment more than doubled (up from 15% to 38%).

It can’t all be good news, of course. The Logistics segment saw its EBITDA margin decline from 20% to 15%.

In the Group segment, they’ve benefitted from the Marine Fuels settlement with insurers, leading to a reversal of R90 million worth of credit losses.

From a balance sheet perspective, Grindrod’s net debt at the end of May was R38 million, a significant move vs. net cash of roughly R0.7 billion as at December 2025.

Looking at the underlying operations, the Port of Maputo’s dry-bulk terminal saw an increase in volumes from 5.2 million tonnes to 6.8 million tonnes. The Maputo Car Terminal enjoyed a 23% increase in volumes.

The Matola terminal wasn’t so lucky, with export volumes down 8% due to adverse weather (and overall volumes down 3%).

In South Africa, there were highlights at the Navitrade facility at Richards Bay and the Maydon Wharf multi-purpose terminal in Durban, up 46% and 42% respectively. But the other port facilities at Richards Bay were down year-on-year.

Ghost Bite: Simplification is a strategy that pays dividends – literally. Grindrod’s total return over 3 years is 225%!

Labat Africa declares a dividend and promises shareholder engagement (JSE: LAB)

This should be interesting!

Labat Africa has been a fascinating story. They’ve pivoted in the unlikeliest of ways, from cannabis to technology distribution. The group has changed completely, including the people involved, so a change of name is probably justified here as well.

The name stays the same for now, but at least there’s a dividend to show shareholders that there’s some value here. Incredibly, with shares changing hands at 3 cents each, there’s a dividend of 1 cent per share! You won’t see a yield like that every day.

This means that many of the investors who bought their shares in recent times at 1 cent each will be getting their entire investment back as a dividend. This is just one of the many crazy potential outcomes in penny stock land.

Labat has also promised a “comprehensive investor engagement and shareholder roadshow programme” – and I do hope that Unlock the Stock will be part of it. Let’s wait and see.

Ghost Bite: There are a number of “boring” companies on the JSE. Labat Africa certainly isn’t one of them!

Sibanye-Stillwater gives investors plenty to chew on at the Capital Markets Day (JSE: SSW)

Capital allocation is going to be key to the next phase of the journey

Sibanye-Stillwater hosted a capital markets day on Tuesday. This gives you a lovely opportunity to dig through the slides and learn more about the group.

The podcast I recorded with CEO Richard Stewart in May is just as relevant now as it was then. It gives you a highly efficient way route to understanding the strategy of the group. Listen to it below or check out the full transcript here.

Among many other things, it will help you understand what they mean at Sibanye when they talk about contiguous assets, a concept that comes through strongly in the presentation.

Perhaps the strongest concept of all is that Sibanye enjoys genuinely world-class PGM assets in South Africa, with the world taking a far more favourable view on the long-term relevance of these metals.

Along with the gold operations and the profits being generated by the broader group as well, this is driving an overall strategy at Sibanye-Stillwater that should see a reduction in debt and the payment of solid dividends to investors.

There’s far too much from the capital markets day to cover in detail here, particularly as Sibanye is such a large group. My strong recommendation is that you listen to the podcast and flick through the slides from the event here.

If you are a DRDGOLD shareholder, then take note that the company also presented at the Capital Markets Day. This is because Sibanye-Stillwater is the controlling shareholder. You’ll find that presentation here.

Ghost Bite: Capital Markets Days are beautiful things. I want to see more of them from more companies on the JSE!

Vunani has swung into profitability, with Fairheads as the anchor of the story (JSE: VUN)

They still have a number of marginal underlying businesses

Vunani committed one of the sins of financial reporting: an updated trading statement on the same day as the release of financials. I’ll never understand how this goes wrong in practice, as trading statements are meant to come out well ahead of earnings.

At least they had released an initial trading statement that wasn’t far off the final numbers, which is more than we can say for some companies on the JSE that go from initial trading statement to full results in the space of a few hours.

For the year ended February 2026, Vunani achieved a swing from losses to profits.

Revenue and insurance revenue climbed 17%, while results from operating activities increased 51%. HEPS was the real star of the show, moving from a headline loss per share of -2.8 cents to HEPS of 10.2 cents.

They are paying almost all of this out as a dividend, with 10 cents per share declared for the year. The dividend in the prior year of 35 cents per share is an anomaly.

The significant jump in the fund management segment’s revenue (from R136.1 million to R177.1 million) must be viewed in the context of the merger with Sentio Capital Management. They’ve highlighted underlying growth in funds under management as well, but you can’t extrapolate that growth rate as being a reflection of business as usual.

If you’re looking for a growth highlight, you’ll find it in the insurance segment as the largest contributor (R335.2 million in revenue, up 21%). But profitability remains marginal, with profit of only R5.5 million (vs. a loss of R3.6 million in the prior period).

The asset administration segment (Fairheads) is the anchor of the group, but showed very little growth with revenue of R215.5 million. Profit is a different story though, up from R34.6 million to R47.5 million.

Ghost Bite: Vunani is still a volatile group built around Fairheads as the most dependable operation. It will be interesting to see how the increased scale in the fund management business comes through in future periods.

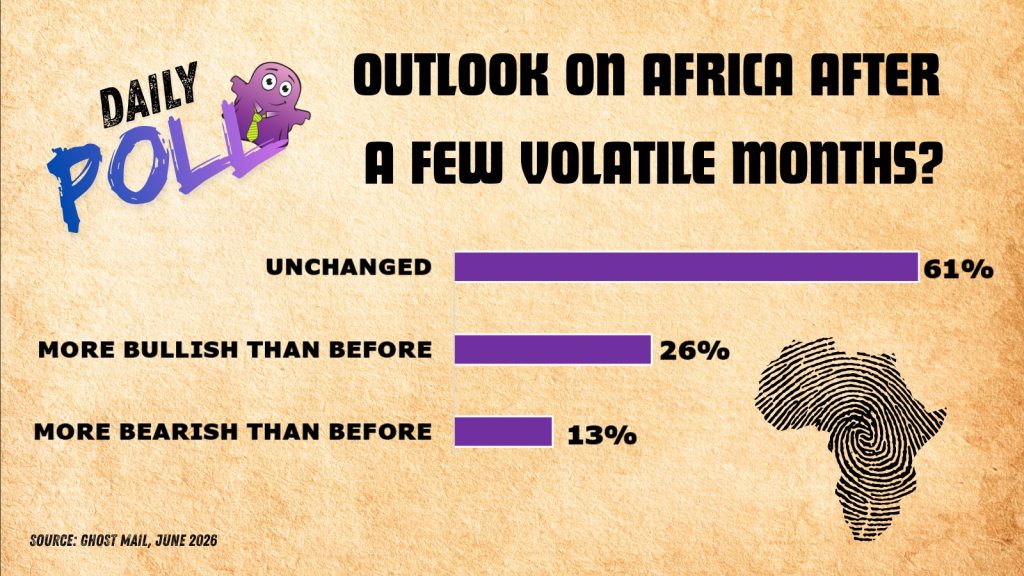

Results of previous poll:

Nibbles:

- Director dealings:

- ASP Isotopes (JSE: ISO) announced that Renergen has entered into its first take-or-pay contract to supply contained helium to an Asian industrial gas company. They are targeting the commercialisation of Phase 1 of the Virginia Gas Project in the third quarter of 2026. This is a five year take-or-pay contract priced at $600/MCF of helium, covering roughly 15% of the expected production of Phase 1. Phase 2 is where the real money happens (we hope), with the project being 13 times larger than Phase 1! This is where the substantial funding from partners like the US DFC and Standard Bank will be utilised.

- Equites Property Fund (JSE: EQU) noted that GCR Ratings has affirmed the credit rating of AA-(ZA) and A1+(ZA) for the long- and short-term ratings respectively. Among many other factors, this considers the impact of UK asset disposals and the logistics development pipeline in South Africa.

- Santam (JSE: SNT) announced the appointment of Michael Fleming as an independent non-executive director. Fleming is the ex-CFO of Clicks and Tiger Brands, so there’s no shortage of experience here!

- Grindrod (JSE: GND) announced that Raymond Ndlovu has been appointed as Chairperson, while Hubert Brody will be the Lead Independent Director.