In this edition of Ghost Bites:

- Finbond is profitable again – but they need to grow faster

- Things don’t seem to be improving at Gemfields

- Hyprop invests in Bulgaria – and look who is on the other side of this deal!

- MAS is offloading properties and looking for new asset classes

- Orion Minerals achieved a strong capital raise

- Egg selling prices made life more difficult for Quantum Foods

- Can Reunert claw its way back in the second half?

- Richemont welcomes a return to growth in Asia Pacific

- Trematon might sell Generation Education

Finbond is profitable again – but they need to grow faster (JSE: FGL)

The share price is high relative to earnings

Finbond’s earnings for the year ended February 2026 reflect a swing from losses to profits. It took turnover growth of just 3.9% to help them shift from a headline loss per share of 1.9 cents in FY25 to HEPS of 5.2 cents.

But with the share price at R1.00, they need much bigger HEPS to keep it anywhere near the current level.

Another useful metric is return on equity. This has increased to 11.4%, which is certainly much better than before. Much like HEPS, it’s nowhere near high enough to justify the current share price. Finbond is trading very close to the NAV per share of R1.03 despite a modest return on equity.

Weirdly, the dividend per share is 9.57 cents. This is significantly higher than HEPS. It’s also identical to the dividend in the prior year – yes, a dividend that was paid during a time of losses!

Ghost Bite: The market seems to be pricing in a rapid increase in HEPS as the company moves through the profitability inflection point. The share price has quadrupled over three years! The risk in these situations is that the share price often runs too far ahead of where the company is executing.

Things don’t seem to be improving at Gemfields (JSE: GML)

If anything, they could be getting worse

Gemfields cannot afford to go back to the market to raise more capital. After previously taking the balance sheet to breaking point and then being tipped over the edge by conditions in the ruby and emerald markets, I just can’t see investors being willing to do it all again with this company.

But I’m also not seeing a material improvement in the company’s fortunes, so there are reasons to be concerned here.

Auctions are difficult to compare over time, as the underlying mix of rubies or emeralds will vary dramatically by size and quality. This leaves us reliant on management commentary and common sense.

In the latest emerald auction, management describes demand for higher-quality emeralds as “stable” while the market exercises caution. What they are implying is that pricing for lower-quality emeralds is under pressure. Gemfields has little influence over the stones that Mother Nature sends out of the ground, so this is a worry.

The latest auction was the smallest one we’ve seen in recent years in terms of the number of carats offered. The average pricing of $146.08 per carat is better than the auction in late November 2024 though, so this is only the second-smallest auction in recent years in terms of total sales.

Either way, it’s certainly not a set of auction results that suggest confidence in the market. It may be difficult to compare pricing, but if the market was more favourable, then Gemfields would be getting more emeralds into these auctions.

Here’s comes the even bigger worry though: an update on the ruby business.

Ruby production at Montepuez Ruby Mining is lower than expected. Gemfields has also noted weak ruby market conditions, driven in part by a lack of Chinese demand. This has led the company to review the auction schedule for the remainder of 2026.

Ghost Bite: It feels almost impossible to forecast the financial performance of Gemfields. This makes it too risky for me to consider for my own portfolio. It’s very important to identify the point at which you feel like you are speculating vs. investing. Due to varying risk tolerances, this point will be different for each person!

Hyprop invests in Bulgaria – and look who is on the other side of this deal! (JSE: HYP)

The fund wants more exposure to Eastern Europe

Hyprop has announced the acquisition of Galleria Burgas in Bulgaria. The town of Burgas is on the coast and is a major industrial and tourist centre. Hyprop quotes a pretty juicy statistic: personal income in Burgas grew by more than 15% in both 2023 and 2024.

This kind of growth is exactly why property funds continue to look for opportunities in Eastern Europe.

Here’s the really interesting part though: the seller is fellow JSE-listed company MAS (JSE: MSP) – you’ll find a separate update on that group further down.

The property has been priced at €122.2 for this deal. Hyprop is taking over the senior debt related to the property, so the equity cheque is €53.5 million after adjusting for debt and working capital.

They will fund it with the proceeds from the recent sale of 50% in Woodlands Boulevard for R824 million, as well as the funds raised in 2025 through accelerated bookbuilds.

The loan-to-value ratio will increase to 33.5% following this transaction. That’s still a healthy level.

Ghost Bite: Getting rid of cash drag (the cost of undeployed capital) is very important, so it was time that Hyprop announced a deal of this nature. But this is exactly why I’m not a fan of generic bookbuilds vs. raising for a specific opportunity, as the time value of money can really impact returns. At an extreme, it can put pressure on management to do less appealing deals out of desperation. We will have to see how this one pans out.

MAS is offloading properties and looking for new asset classes (JSE: MSP)

Minorities appear to just be passengers on this journey

You may recall the rather hostile reception that PK Investments was given by the South African institutional investor community when they made a play for MAS. In the end, it was PK Investments that came out on top.

Now that PK and its concert parties control MAS with a 61% shareholding, they can direct the strategy and make some changes to how capital is allocated. The company is now being run based on what the controlling shareholder believes is right. Minorities are simply along for the ride. MAS references a legal opinion that supports their view that they can do this without shareholder approval or triggering related party provisions.

Perhaps unsurprisingly, this comes with a change in management. Irina Grigore moves from CEO back to CFO. Mihail Vasilescu, a partner at Prime Kapital, moves into the CEO role.

If you’re investing in this story, it’s because you believe that a benevolent despot can be a good strategy. Sometimes, it can be! Several years down the line, we will be able to look back and see whether this turned out well for investors.

The change in strategy includes a desire to broaden the asset base beyond just real estate in Eastern Europe. As noted above, they’ve just agreed to sell a property in Bulgaria to Hyprop (JSE: HYP) for €122.2 million (a small discount to the fair value of €125.4 million as at December 2025).

They are also selling six open-air malls in Romania to a company listed on the Tel Aviv Stock Exchange. The expected selling price for the portfolio is €281.8 million (a significant discount to the €311.2 million on the balance sheet as at 31 December 2025).

But what will they actually do with the money? That’s the real question.

Ghost Bite: This is clearly a significant departure from the historical strategy of MAS. The prices are below fair value, but it’s well worth pointing out that a December 2025 fair value was calculated under very different global circumstances. The bigger thing to watch is the use of the net proceeds. At this stage, we don’t know what MAS will be investing in.

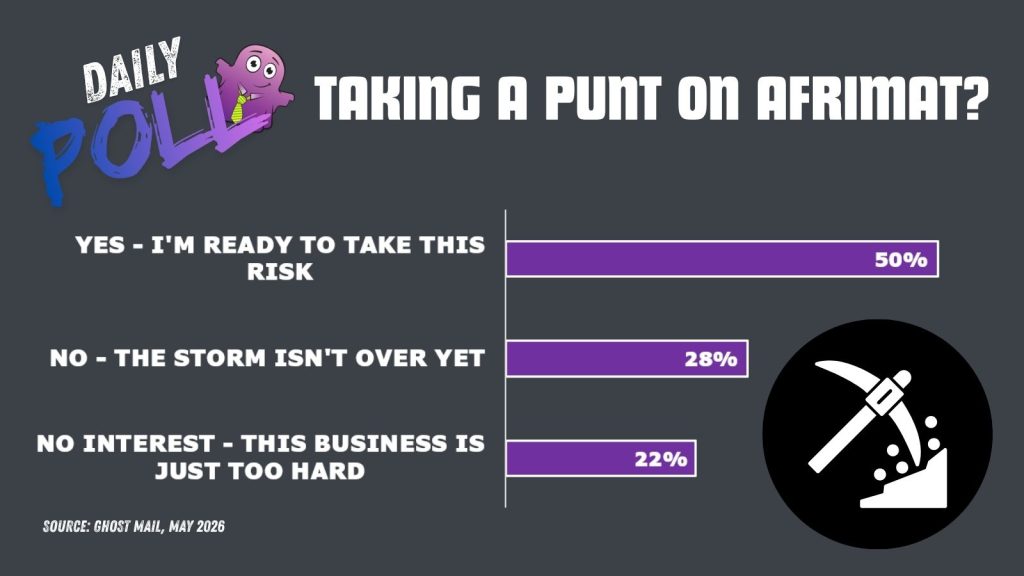

Orion Minerals achieved a strong capital raise (JSE: ORN)

Importantly, most of the capital has come from new investors

Orion Minerals has raised approximately R181.5 million from “sophisticated and professional investors” – in other words, retail investors didn’t get a sniff this time. Certain existing shareholders (known as cornerstone investors) committed R59.1 million of this raise, so around two-thirds of the raise came from new investors.

At a price of R0.26 per share for this raise, they are raising at the lowest price we’ve seen since January this year. It’s also a long way off the 52-week high of R0.49, although that was achieved before things went crazy with Iran and the oil price.

Participants in this capital raise also have an option to buy more shares at R0.37 per share, expiring in mid-2029. The only certainty when you invest in a junior mining company is that your stake will be diluted over time (as the company raises more capital from institutional investors). If things go well enough, that won’t make much of a dent in your returns though!

Interestingly, the company highlights the strong support achieved from South African investors. Perhaps the potential financing deal with Glencore (JSE: GLN) is the vote of confidence needed to get Orion on the map with local funders.

Thanks to this raise, Orion is ready to commence development of the Uppers Mine at Prieska, as soon as the Glencore financing transaction is finalised. They expect this to happen in the coming weeks.

Ghost Bite: Corporate financiers will tell you that capital raises are much easier when a trusted name has already made a commitment. It’s a bit like buying a car or a house in a particular area based on a friend’s recommendation, instead of just relying on the salesperson.

Egg selling prices made life more difficult for Quantum Foods (JSE: QFH)

Thankfully, the rest of the business more than made up for it

Quantum Foods has experienced quite the swing in its margins in the six months to March 2026. Although revenue was down by 5%, operating profit (excluding capital items) jumped by 13%. HEPS increased by 16%. These are the numbers that you expect to see when revenue has declined!

This is a reminder that the poultry industry is a tricky game with numerous external factors that impact margins. In this period, a 30.6% decline in SAFEX yellow maize prices did wonders for the cost of raising chickens. There were other favourable commodity moves in areas like soya bean meal and wheat bran.

Still, the segmental results were all over the show. For example, operating profit in the Eggs segment fell by a nasty 42% despite only a 5.1% decline in revenue. Eggs were a lot cheaper in this period, which is good news for Eggs Benedict enthusiasts like me and bad news for Quantum Foods.

The rest of the group more than made up for this issue. In fact, just the “Other African Operations” with an operating profit jump of R37 million did enough to offset the R30 million decline in eggs. The incremental operating profit gains in Farming (R13 million) and Animal Feeds (R10 million) did the rest of the work.

The group generated cash from operating activities of R409 million. Capital expenditure was in line with the comparable period at only R152 million. The cash surplus has led to a significant improvement to the balance sheet.

Ghost Bite: Given the macroeconomic uncertainty and all the risks faced on an ongoing basis by poultry businesses, a stronger balance sheet is exactly what shareholders want to see.

Can Reunert claw its way back in the second half? (JSE: RLO)

The Electrical Engineering segment has been a huge headache

Two of Reunert’s three segments delivered reasonable results in the six months to March 2026. Sadly, the third one (Electrical Engineering) was bad enough to ruin the story.

We begin with the group numbers. Group revenue from continuing operations was up by just 1%. Operating profit fell by 23%. HEPS was down by 22%. This won’t go down as a happy outcome for shareholders.

The variance at segmental level is quite something to witness.

The Electrical Engineering segment may have seen revenue increase by 2%, but operating profit tanked by 40% to R138 million. Operating margin contracted from 6.6% to 3.9%. There were many factors at play here, ranging from the exchange rate and tariff situation in the US through to lower volumes in South Africa. Investment in local infrastructure remains weak, creating problems further up the value chain for companies like Reunert.

The ICT Segment’s revenue fell by 4%, but segmental operating profit was up by just 1% to R321 million. This is the anchor of the group, operating a number of technology-focused businesses including Nashua. They aren’t shy of bolt-on acquisitions here, like iqbusiness agreeing to acquire 100% of Silversoft during this period.

Applied Electronics saw revenue increase by 9% and operating profit jump by an impressive 41% to R110 million. The Defence Cluster was the hero here. The renewable energy business had a challenging period, but they are making progress on various initiatives.

In terms of outlook, the Electrical Engineering segment is expected to have a better second half (but that isn’t saying much). The ICT segment is expected to achieve growth. The Applied Electronics segment will continue to be driven by the underlying defence businesses, but rand strength has a negative impact as this is an export-focused business.

Ghost Bite: There are too many different things going on here. The market appreciates focus and an ability to forecast the underlying performance with some degree of accuracy. Investing in Reunert is like being blindfolded, sticking your hand into a bowl of sweets and waiting to see what taste you get.

Richemont welcomes a return to growth in Asia Pacific (JSE: CFR)

Could this inject some momentum into the share price?

Richemont’s annual results reflect an increase in sales of 11% in constant currency, or 5% in reported currency. Unfortunately, this wasn’t enough for HEPS to go in the right direction, with a 3.5% decline in basic HEPS.

The volatile macroeconomic environment led to gross profit falling from 66.9% to 64.4%. Operating profit increased by just 1%, with strong cost control contributing to a positive trajectory in operating profit despite the pressure further up the income statement.

The constant currency numbers aren’t a reflection of the cash actually flowing through to investors, but they do give us great insight into the state of the market.

Aside from encouraging double-digit constant currency growth rates in the Americas (17%) and the Middle East & Africa (13%), there was a low single-digit increase in China, Hong Kong and Macau combined. This has been a major pressure point for the luxury industry, so investors will be very pleased to see this. Thanks to that improvement, Asia Pacific returned to growth, up 8% in constant currency.

Europe and Japan were in the middle, both up 9% in constant currency despite having a demanding base period.

The Jewellery Maisons are doing the bulk of the work, with sales up 14% in constant currency. The Specialist Watchmakers could only manage a slightly positive performance in constant currency.

Thankfully for Richemont shareholders, jewellery is where the money is made. The Jewellery Maisons achieved operating profit of €5 billion vs. just €107 million at Specialist Watchmakers. The problematic “Other” segment saw a loss of €96 million.

The fourth quarter represented positive momentum into the end of the year, with sales up 13% in constant currency. Although the share price is down 10% year-to-date, this is an encouraging sign for investors, particularly when viewed alongside the uptick in Asia Pacific.

In a separate announcement, Richemont noted that they spent three years repurchasing just 0.37% of shares in issue. They have announced a new programme to repurchase up to 1.69% of shares in issue. Before you get excited, they’ve noted that these shares will be held in treasury to hedge awards to executives under the long-term incentive plan.

Ghost Bite: Richemont’s total return over three years is just 10%. It’s quite possible that you would’ve been better off buying a collectible timepiece!

Trematon might sell Generation Education (JSE: TMT)

The value unlock strategy continues

Trematon now has a market cap of under R240 million. This isn’t necessarily too small to justify a listing, but Trematon has struggled to really capture the attention of investors over the years. For this reason, the company is firmly in a value unlock phase. They are selling off its major assets as and when opportunities present themselves.

The most recent example is the potential disposal of Club Mykonos Langebaan for R70 million in a related party transaction. The meeting to vote on that transaction is scheduled for 2 June.

In addition to that deal, the company has now released a cautionary announcement related to a potential disposal of Generation Education. There are no other details provided in the announcement.

Ghost Bite: Building schools isn’t the gold mine that people once thought it would be. There just aren’t enough kids being born in middle- and higher-income families! I’ll be interested to see what the pricing of a potential deal for Generation Education will look like, assuming they even get that far.

Results of previous poll:

Nibbles:

- Director dealings:

- A long-standing senior executive at Nedbank (JSE: NED) has sold shares worth R2.6 million.

- The chairman of Southern Palladium (JSE: SDL) bought shares worth around R460k.

- I’m not sure that dividend reinvestment plans are quite the same psychological decision as a director buying shares in the open market. I’ll nonetheless highlight that a director of Hammerson (JSE: HMN) reinvested dividends to buy shares worth around R186k.

- Dipula Properties (JSE: DIB) has released an announcement that really stretches the concept of a “bland cautionary” to breaking point. Unlike most cautionary announcements that at least give us a hint as to what the company is looking at, Dipula has simply noted that they are “considering potential corporate activities” – and that can mean anything. The company also released the circular for the dividend reinvestment alternative. Dipula is trying to retain capital, which suggests to me that they are looking at acquisitions rather than disposals.

- Afine Investments (JSE: ANI) is a REIT that owns a portfolio of fuel stations. Although the market cap is R319 million, there is close to zero liquidity in the stock. A trading statement for the year ended February 2026 notes a sharp drop in earnings per share (EPS). Luckily, HEPS will be slightly up on the prior year, but not by more than 20%. This is a good reminder of how significant the adjustments between EPS and HEPS can be.

- Putprop (JSE: PPR) is another highly illiquid stock on the JSE. They are selling Montana Park for R29 million to an unrelated party. As at 30 June 2025, the property was valued at R22 million. That’s a solid premium to book value for this warehouse and office space! Putprop plans to reinvest the proceeds in income-producing properties.

- At long last, Pan African Resources (JSE: PAN) has achieved all the steps required in the UK for the capital reduction. This ended up being an enormous hack that required the circular and the meeting to be redone!