In this edition of Ghost Bites:

- Omnia’s Agriculture business boosted group margins

- PPC’s wonderful turnaround continues

- Sygnia’s growth path is a reminder of how the right strategy can win

Omnia’s Agriculture business boosted group margins (JSE: OMN)

The broader continent offers exciting opportunities in this space

Omnia is an excellent example of operating leverage: the process of turning modest revenue growth into excellent growth in profits. Revenue for the year ended March 2026 was up 6%, yet EBITDA jumped by 21% and HEPS was good for a 21% increase as well.

South African businesses have become masters of operating leverage over the past decade. I sometimes catch myself imagining how well they might do if we experienced proper economic growth!

The net cash position is largely flat year-on-year, so the group is in a sound financial position. This has facilitated an 18% increase in the ordinary dividend, as well as another special dividend of 280 cents (vs. 275 cents in the previous period).

It can’t all be good news, of course. Omnia is still fighting with SARS over a tax assessment dealing with the 2014 to 2016 tax years. This is a prime example of how SARS will bring up a painful past even more effectively than your ex-lover. They are in Alternative Dispute Resolution proceedings that are at an advanced stage.

Digging into the segmentals, we begin with the Agriculture segment as the largest. With revenue moving through the R13 billion milestone, it’s great to see revenue up 13% and operating profit up 28%. Operating profit margin increased to 9.6%. The operations in Rest of Africa drove the performance here, with South Africa and the international business as more of a mixed bag.

In Mining, revenue was up 8% to R9.8 billion. Operating profit could only manage a 1% increase though, so margin dipped to 11.7%. With exposure to multiple commodities and countries, the performance in this segment is always a game of give-and-take.

In Chemicals, revenue increased 38% to R1.3 billion. Operating profit remains marginal at best, with profit of just R4 million at a paltry margin of 0.3%. This is a particularly difficult space.

It’s clear that it was the Agriculture segment that did the heavy lifting in this period. Thankfully, it’s also the segment with the biggest muscles, so that worked out well for shareholders.

Ghost Bite: Omnia is up 44% in the past 12 months. If you include the dividend, then the total return is 56%. The P/E multiple of 12.4x shows that local investors are feeling more comfortable about buying “real economy” stocks at double-digit P/Es.

PPC’s wonderful turnaround continues (JSE: PPC)

Soon, we can safely refer to it as a growth strategy instead

PPC’s strategy is called Awaken the Giant, which I’ve always felt is a lot juicier than the typical corporate wording you’ll see out there around “optimise” and “grow”. Putting a great tagline on a turnaround strategy is a good idea.

The giant has been slow to get out of bed on the revenue line, but much of that is outside of PPC’s control. Infrastructure investment remains fast asleep in South Africa, so PPC’s revenue growth of 3.9% in the year ended March 2026 is a decent outcome in that context.

The real value unlock is happening further down, with EBITDA up by an impressive 31% for the year. EBITDA margin has moved from 12.3% in FY24, to 16.1% in FY25, and now 20.3% in FY26.

HEPS as reported is up by 25% for the year to 50 cents. If you exclude the forex losses on the hedge for the RK3 project, HEPS would be up 45% to 58 cents.

The ordinary dividend is up by 71.6% to 30.2 cents, reflecting the combination of higher profitability and reduced financial risk on the balance sheet.

Looking at the segmentals, you’ll soon see that Zimbabwe is strongest on top line growth, but the South African business has a strong EBITDA trajectory.

In South Africa, PPC could only manage revenue growth of 1.8% thanks to volumes growth of 1.3%. EBITDA was up by 28% if you exclude the impact of the sale of a non-core property, with margin up 320 basis points to 16.9%.

In Zimbabwe, cement volumes were up significantly. An 18.2% increase in volumes was partially offset by currency translation effects into rand, so revenue as reported was up 14.3%. In USD terms, it was up 20.5%.

EBITDA margin in Zimbabwe came under pressure, with a 30 basis points decline to 26.9%. In H2, that margin was much better at 30.9%. The margin pressure means that EBITDA grew by 13%, below the rate of revenue growth but still an impressive number.

As long-standing PPC investors will know, none of this matters if you can’t translate the earnings into cash flow. Thankfully, the net cash inflow in South Africa was up 26% to R1.04 billion. In Zimbabwe, it was up by 124% to $37.6 million!

What’s next for PPC? Well, FY28 will be a big financial year, as this is the planned completion period for the new integrated plant in the Western Cape. Given the extent of development in the province, having more cement production capacity nearby makes sense. They need a solid period of execution in FY27 as they transition into this growth phase.

In a leadership update, the company previously announced that CFO Brenda Berlin will be retiring at the end of June 2026. They haven’t announced her replacement yet, but the process is described as being well advanced.

Ghost Bite: PPC is an incredible self-help story. Next time you see a management team throw their hands up in the air and blame the economy for their woes, just think about what PPC has achieved in the past few years.

Sygnia’s growth path is a reminder of how the right strategy can win (JSE: SYG)

It’s lovely to see another period of net inflows from retail investors

Sygnia is an excellent example of a company that has carved a growth path in a tricky industry. South Africa’s savings culture is infamous, yet Sygnia has found a way to grow to over R460 billion in assets under management and administration (up 13.6% in the six months to March 2026).

This underlying growth in the business has pushed revenue up by 24.3%. It’s pretty hard for things to go wrong from there, although HEPS growth of 22.0% is a reminder that there isn’t as much leverage in this business model as investors would like. The interim dividend is up by 24.5%.

As a sign of the times, the CEO’s letter in the results includes this line at the bottom: “This overview was written without assistance from ChatGPT or any other large language model.”

Respect. AI is an important assistant, but should never be a replacement for the brain. Great writing by a human still beats anything that the LLMs can do.

The irony, of course, is that AI has defined this period in the markets. Sygnia’s funds that are focused on tech have enjoyed strong popularity with retail investors. The retail business has been an important growth engine for Sygnia, with assets under management up from R78.7 billion to R91.6 billion. This included net inflows of R1.9 billion.

Ghost Bite: Increasing the market awareness and understanding of retail investors is the purpose of my work in Ghost Mail. When I see stats like these at Sygnia, I’m reminded of how important this is.

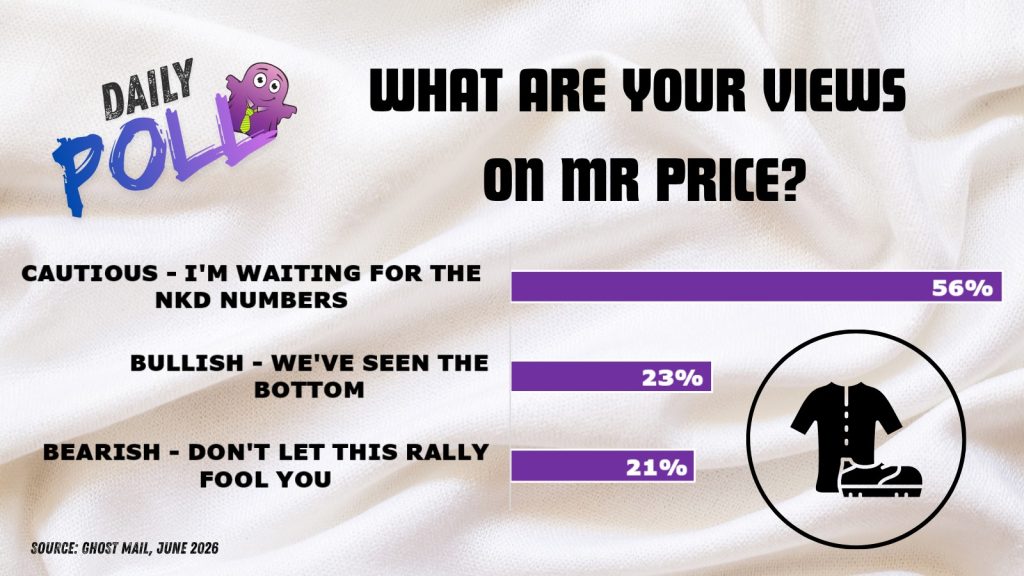

Results of previous poll:

Nibbles:

- Director dealings:

- A related party of a senior exec at British American Tobacco (JSE: BTI) bought shares worth around R340k.

- The COO of Metair (JSE: MTA) bought shares worth R200k.

- The CEO of Libstar (JSE: LBR) bought shares worth R24.5k.

- Spear REIT (JSE: SEA) announced that holders of 48.79% of shares in issue elected the dividend reinvestment alternative. This allowed Spear to retain equity of R107.6 million. One way to think of this is as a mini-rights issue, in this case priced at just over R13.00 per share (the spot price is R13.30).

- At Oasis Crescent Property Fund (JSE: OAS), holders of 64.3% of units in issue elected to reinvest their distribution. The fund therefore issued new units to the value of R24.5 million.

- Tharisa (JSE: THA) has launched an ADR programme, which means they want to give US-based investors a way to invest in the company in the over-the-counter (OTC) market in the US. If the programme is successful, this can do good things for liquidity in the stock. Importantly, this doesn’t mean that any new shares have been issued. This is purely a US-based structure that provides market access to the existing base of shares.

- Altron (JSE: AEL) announced that SARB approval for the special dividend has been received. The payment date is 22 June.

- For those keeping track, Mustek (JSE: MST) has confirmed that Novus (JSE: NVS) has a 41.85% stake in the company.

- Bidcorp (JSE: BID) has successfully renewed its €300 million revolving credit facility. There are a number of banks in the lending syndicate. Bidcorp is an exceptional global business, so I’m sure they had little or no trouble in these negotiations. The renewal has a tenure of 3 years, with an option to extend for a further 2 years.

Question out of curiosity – do companies pay for every posting on SENS – yesterday saw 10+ announcements of dealings by Investec directors?

Yeah that was wild! And no they don’t. Usually, the sponsor (the advisor who releases the announcements) doesn’t even charge per SENS. They charge flat fees instead (unless something changed in the past decade).