")

If you enjoy Ghost Bites, then make sure you’re on the mailing list for a daily dose of market insights in Ghost Mail. It’s free! SIGN UP >>>

Corporate finance corner (M&A / capital raises)

- MTN and Telkom have renewed their respective cautionary announcements. Discussions regarding a potential offer by MTN for all the shares in Telkom are still underway. The announcement notes that the potential offer would be to acquire all the issued share capital of Telkom in exchange for shares in MTN or a combination of cash and shares.

- Afrimat updated the market on the Glenover phosphate and Gravenhage manganese projects. The Glenover deal was announced in December 2021 with a total deal value of R550 million. The implementation of the initial phases has progressed well and feasibility studies of follow-up phases have yielded “pleasing results” – so that’s clearly good news. The payments for inventory stockpiles (a total of R250 million) have been made to the sellers. The option to acquire the Glenover shares remains at Afrimat’s sole discretion and is valid until November 2022. The news on the Gravenhage project isn’t good I’m afraid, with the water use licence granted by the Department of Water and Sanitation deviating materially from the application that was made. This means that conditions precedent weren’t met and the deal has fallen over as far as Afrimat is concerned. The counterparty disagrees, with a formal dispute now underway that may end up in arbitration. If you’ve ever read a proper sales agreement, you’ll know that there are many clauses that are legal in nature rather than commercial. They exist for scenarios just like these.

- Ascendis Health announced the results of its rights offer. The company aimed to raise around R101.5 million and the rights offer was fully underwritten, so there was no chance of that amount not being raised. The debate was simply around where the money would come from. 32.6% of the rights offer shares were subscribed for and all the remaining shares were issued under excess applications, which refers to existing shareholders who put in an application for more shares than they would otherwise be entitled to. The underwriter didn’t need to spend a cent as all the shares were allotted to existing holders, so the underwriting fee was a great deal in the end. A few directors participated in the equity raise with Carl Neethling as the largest by far (over R22.3 million across various associated entities).

- Raubex and Bauba Resources announced the results of Raubex’s general offer to shareholders of Bauba. The offer was accepted by holders of 13.29% of shares in issue. The delisting will now take place, so anyone who didn’t accept the offer will be the proud owner of an unlisted share, an asset that is usually as rewarding and valuable as one-ply toiletpaper.

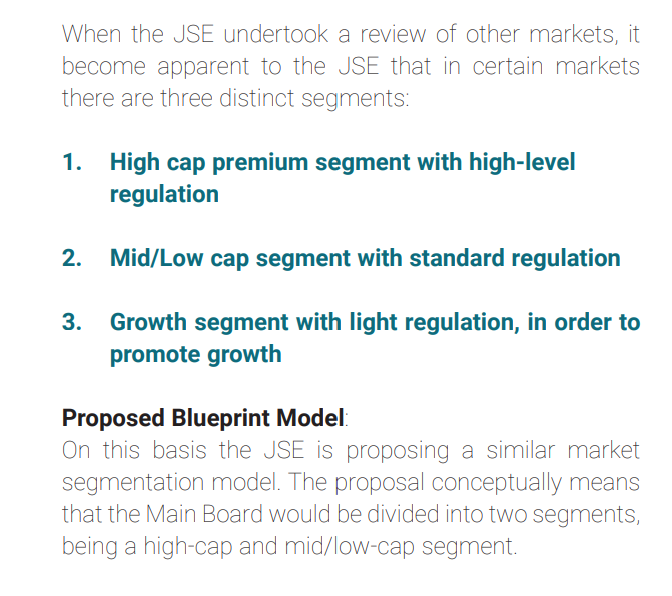

- Corporate finance advisors are impacted by the way in which JSE listings requirements are applied to listed companies (the same applies to other exchanges – though they are still in their infancy in South Africa). For that reason, I’m including the JSE’s response paper in this section, which was issued after consulting with the industry about potential changes to the the listings requirements and the strategy going forward. Something that jumped out at me was a proposal to move from two market segments (Main Board and AltX) into three segments, effectively carving out a set of rules for “mid-caps” that create a greater regulatory burden than on the AltX board but not as severe as for the largest companies on the JSE. This is a bit like Pick n Pay’s long overdue recognition of the need for a store format that caters for the middle market. Here’s the relevant excerpt from the JSE response paper:

Financial updates

- Motus Holdings has released an updated trading statement approximately a month after the initial trading statement was issued. For the year to June 2022, HEPS increased by between 68% and 73%. The actual range is between 1,980 cents and 2,040 cents per share. On a share price of nearly R118, this puts the group on a trailing Price/Earnings multiple of below 5.9x. Detailed results will be published on 31st August.

- Sun International Limited has released a trading statement for the six months to June 2022. When companies talk about a “strong recovery in revenue and EBITDA and a significant reduction in group debt” then you know it’s been a much happier time than before. Both HEPS and adjusted HEPS have swung massively into the green after losses in the comparable period. HEPS is between 83 cents and 101 cents for the interim period. Adjusted HEPS relates to a change in the estimated redemption value of the Tsogo Sun put option. If you’re happy to go with management’s view on that, you’ll focus on the adjusted HEPS range of between 167 cents and 185 cents. The share price traded nearly 3% higher after the announcement at almost R30 per share.

- I noticed a SENS announcement for “SuperDrive” and decided to dig further. It turns out to be part of BMW Financial Services, so I couldn’t wait to dig in and see what I could find. There are some great stats to remind you that most people in flashy cars can’t afford them. The weighted average balloon payment is 23.16% and used vehicles are 47.22% of the portfolio, so many people have bought used cars with balloon payments. The weighted average margin is prime + 0.74%, so it’s not cheap to finance these cars. The geographical split is also interesting: Gauteng 57.51%, KZN 16.96% and Western Cape 10.68% of the total portfolio. If you’re wondering whether BMW Financial Services is a listed company, I’m sorry to disappoint you that it isn’t. The company issues debt through the JSE, hence the need for a SENS announcement.

- Workforce Holdings has announced results for the six months to June 2022. The staffing, outsourcing, recruitment and training group (amongst other services) grew its revenue by 21% and EBITDA by 19%, so EBITDA margin fell slightly. Those margins are already tiny, with only R68.7 million in EBITDA off R1.9 billion in revenue. HEPS improved by 30% to 14.6 cents. No interim dividend was declared.

- One for the diaries – Spear REIT is hosting a pre-close investor presentation at 11am on 31st August. You’ll be able to watch at this link.

Operational updates

- Transnet is in the process of upgrading two key ports and plans to structure this as a partnership with the private sector. The idea is to create a special purpose vehicle between Transnet Port Terminals and the winning bidders, with ownership reverting to Transnet after 25 years. In others words, Transnet is looking for an operational partner for the next 25 years and that partner needs to extract enough value in that period to make it worthwhile. The ports in question are DCT2 in Durban and NCT in the Port of Ngqura in the Eastern Cape. The goals are different: DCT2 needs to achieve better commercial performance and throughput, whereas NCT has been loss-making for years and needs additional shipment volumes. After running a process since 2021, there are ten shortlisted partners for DCT2 and four for NCT. Within the DCT list, I recognised names like DP World (the new owner of Imperial), Grindrod Freight and an entity working in conjunction with Remgro. The Remgro bidder also made the shortlist for NCT. Preferred bidders are expected to be appointed by February 2023.

Share buybacks and dividends

- British American Tobacco continued with its daily share buybacks.

- Schroder Real Estate has announced the exchange rate applicable to its dividends. The third interim dividend will be R0.3157950 per share and the special dividend will be R1.707 per share.

Notable shuffling of (expensive) chairs

- Buffalo Coal has announced the resignation of CFO Willie Bezuidenhout and has appointed CEO Emma Oosthuizen to act as interim CFO as well.

- Bowler Metcalf has appointed Ms Debbie van Duyn to the board. This is notable because she is also the Chairman of the Plastic Converters Association of SA and plays a role in other industry bodies. Bowler Metcalf is a classic example of a JSE small cap that many people have never heard of. Now you have!

- Balwin Properties has appointed Ms Keneilwe Moloko to the board. Her academic background is really interesting, qualifying as both a quantity surveyor and a CA(SA)! Ms Moloko also served on the boards of Attacq, Fairvest and Long4Life.

Director dealings

- A director of Kumba Iron Ore has sold shares in the company worth R206k.

- A trust related to the chairman of BHP has bought shares worth around R2.95 million.

- The CEO of Mondi’s South African business has sold shares in the group holding company worth nearly R1.6 million.

- A director of a subsidiary of Nu-World has sold shares in the company worth around R52.5k.

Unusual things

- The sad tale of Pembury Lifestyle Group continues, with the company receiving letters of demand from various parties since the passing of the CEO. The company is in so much trouble that it can’t even pay historical debts to its previous auditors. Moore has put in a proposal to be reappointed and Abacus just wants to get paid for old work. Pembury needs to raise money to settle old debts and finalise audits. In positive news, the Northriding property is being let out profitably to commercial tenants, with the proceeds ensuring that monthly obligations to Abacus can be met. This is like watching a cricket team trying to save an innings after losing 8 wickets in the first 10 overs.