In this edition of Ghost Bites:

- Africa Bitcoin Corporation’s best business isn’t a surprise to me – yes, it’s ACOF!

- Balwin looks set to go private thanks to the PIC.

- Mantengu is considering a reverse takeover.

- Southern Sun achieved excellent growth.

- Vukile Property Fund had no trouble raising the capital for Italy.

Africa Bitcoin Corporation’s best business isn’t a surprise to me (JSE: BAC)

As I’ve said for a while, ACOF is the best option they have

Africa Bitcoin Corporation has released a trading statement dealing with the year ended February 2026. It’s complicated, as there are four different classes of shares!

The ordinary shares cover the bitcoin holding and the exposure to the underlying preference shares and equity layer. The net asset value (NAV) per share has increased by between 7.6% and 17.6%.

As we dig deeper into the preferred shares, things are playing out as I expected.

The Umganu Lodge, represented by the preferred A shares, is struggling with an operating loss that was worsened by repairs, maintenance and marketing. I still see this as a lifestyle asset, with steady occupancy levels and only a small increase in revenue. The NAV for these shares has fallen by between 15.5% and 5.5%.

Bambanani is a sad story, with that restaurant chain fighting for its life in an operational reset. The preferred B shares saw the NAV drop by between 28.8% and 18.8%.

We then reach the preferred C shares, which provide direct access to the Altvest Credit Opportunities Fund (ACOF). This is by far the best business in the group, although I must be honest that this isn’t saying much. Assets under management reached R502 million in this period, with new institutional mandates coming through. The key is to get big enough to offset the operating costs and then enjoy the benefits of operating leverage. The NAV on these shares has increased by between 15.4% and 25.4%.

Ghost Bite: When detailed results are released, I’ll read about ACOF first. I’m rooting for them to make that business work, as SMEs are desperate for access to fairly priced funding.

Balwin looks set to go private thanks to the PIC (JSE: BWN)

This deal makes a lot of sense to me

Balwin has been a value trap on the JSE for as long as I can remember. It came to market in 2015, right at the top of that property cycle that saw immense capital raising on the JSE. The IPO offer price was R9.88. Before the latest announcement, the stock was trading below R4. You don’t need to get your calculator out to figure out whether this was a good investment or not.

Of course, it’s all about timing. Balwin has been on an absolute charge in the past year (up 91%), but the five-year return is just 8.6% including dividends. That’s not the return per year – that’s the total return!

The time to punt Balwin is probably coming to an end, as the PIC is looking to take the company private. This makes sense from the government’s perspective, as Balwin has a proven track record of building housing in very important price brackets. There’s no reason why that skill set can’t be levered to do more housing projects at different price points in the market.

CEO Stephen Brookes is front and centre in this deal. His investment entity has a 33% stake in Balwin. The consortium also includes the management director of Balwin (with a 9.5% stake) and a company named GRE Africa that has a 7.6% stake. With all said and done, the GEPF (represented by the PIC) would have a 49.3% stake.

There’s going to be a lot of complaining about the price, as the offer on the table is for R4.35 per share. It’s not a massive premium to spot, but the 23% premium to the 30-day VWAP is reasonable. The 41% premium to the 180-day VWAP gives you a good idea of how strongly this stock has traded recently!

Or hasn’t traded, as the case may be – a lack of liquidity is one of the issues here. Sure, retail investors can dart in and out, but you really need institutions to be involved before a share price settles into a rhythm.

The combination of illiquidity and the company’s trading history inspired holders of 63.5% of shares (excluding those held by concert parties) to provide irrevocables to vote in favour of the offer. That’s a very strong level of irrevocables that significantly improves the chances of this deal being a success.

I’ve seen a lot of talk around the tangible net asset value (NAV) per share of R9.72. My view on NAV as a valuation tool is that it is only useful in very limited circumstances, specifically where a company is holding its assets and liabilities at or close to fair value. Banks and REITs are good examples. A property developer probably isn’t the best application of NAV-based methods.

Based on diluted HEPS for the year ended February 2026 of 46.60 cents, the offer is at a Price/Earnings (P/E) multiple of 9.3x.

Ghost Bite: Given all the underlying risks faced by Balwin in this country and the serious questions I have about valuation of properties targeting white-collar workers in the AI era, I don’t think this price is unreasonable. But what are your thoughts?

Mantengu is considering a reverse takeover (JSE: MTU)

Perhaps this really is the best way forward

The good news is that I haven’t seen anything really weird out of Mantengu in a while. It’s also been a while since I was threatened publicly on X with legal action, or “doxxed” in the High Court for that matter.

The bad news is that the investment in Sublime has probably turned out to be too good to be true. As the company recently announced, electricity tariffs have put that business in an unsustainable position. Unless they get a major win with Eskom, that bargain purchase gain will turn out exactly as I feared.

Underneath all of this, Mantengu does actually have a business. It’s just been covered by a layer of noise. If the latest potential transaction goes ahead, then perhaps it will reset the story and actually give them a chance.

So, onwards to the latest deal. Mantengu is in negotiations with Averi Finance regarding a potential reverse takeover. Practically, this would lead to Averi injecting their portfolio of power transmission, energy trading, renewables, oil and gas and digital infrastructure assets into Mantengu’s listed structure. Talk about a big change in the business!

In return, Averi would hold roughly 66.6% of the enlarged group. Mantengu shareholders would be diluted to around 33.3% of the enlarged group. This is why it’s called a reverse takeover, as Averi’s valuation ($120 million) is larger than Mantengu ($60 million).

Mantengu’s market cap is only R123 million though, so this deal values Mantengu at a huge premium to its current traded price. Before anyone gets too excited, we currently have no idea what the valuation of Averi was based on. In a relative share swap, all that really matters is the exchange ratio rather than the absolute numbers.

I look forward to reading the circular when it comes out, assuming the parties achieve a successful due diligence process.

Ghost Bite: If the Averi valuation is based on reasonable metrics, then this could be a spectacular deal for Mantengu. You’ll have to forgive my ongoing skepticism, particularly when the numbers are wildly different to Mantengu’s market price. Let’s wait and see what the circular says.

Southern Sun achieved excellent growth (JSE: SSU)

How does a dividend increase of 20% grab you?

Southern Sun’s results for the year ended March 2026 are a fantastic display of some of the growth opportunities we have in the local market. Income was up by 9% (significantly above inflation), with this increase working its way down the income statement to arrive at HEPS growth of 20%. The dividend per share followed suit.

This was driven by a 210 basis points increase in the occupancy rate to 62.9%, accompanied by a 5% increase in the average room rates. Another useful metric is that food and beverage income increased by 9%.

With operating cost increases of 8%, the group does face significant inflationary pressures across areas like property costs, technology requirements and even online travel agent commissions. Thanks to such strong revenue growth though, EBITDAR (the “R” isn’t a typo in this industry) increased by 13%.

One of main reasons for the much higher growth in HEPS rather than in EBITDAR is that net finance costs (excluding IFRS 16 leases) declined by 61%.

International conferences and events proved to be lucrative for the company. The Sandton business saw its income jump by 21% thanks to the G20 and B20 conferences. The rest of Gauteng didn’t do quite that well, but still managed income growth of 7% and EBITDA growth of 9%.

The Western Cape has more of a mix of tourism and conferences. It saw income increase by 7%. The importance of tourism is evidenced by the Western Cape business contributing 47% to group EBITDAR.

Even the KZN business got a slice of the conferencing action, with income up 13% and EBITDAR up by 15%.

In the offshore business, income was down by 4%. It was firmly a tale of two halves, as the Paradise Sun was completely closed for refurbishment in the first half. After reopening in the second half, it achieved occupancy of 64.7% vs. 59.9% before the refurbishment.

They have the good sense to remind the market that the oil price could have an effect on demand going forwards. It’s certainly making air travel far more expensive. If inbound tourism slows down, then it will likely put pressure on pricing.

Thanks to a strong balance sheet, Southern Sun is well positioned to weather an economic storm. Not all competitors may be in that position, which is how economic dislocations can quickly create opportunities for dealmaking.

They generated free cash flow of R909 million in this period, only R43 million down year-on-year despite investing an incremental R150 million in capex (R600 million vs. R450 million in the prior period).

In addition to dividends of R344 million, Southern Sun implemented share buybacks of R359 million. If the share comes under pressure this year, I hope to see more buybacks.

Ghost Bite: The share price being flat year-to-date is testament to just how good the management team and this business actually is. If it does suffer a nasty correction this year, it will be on my shopping list.

Vukile Property Fund had no trouble raising the capital for Italy (JSE: VKE)

That’s R2.8 billion raised overnight

Being a listed company isn’t easy. It comes with a lot of regulatory requirements and intense public scrutiny. But it also gives successful management teams access to an immense pool of capital to fund new projects.

In private company world, a R2.8 billion raise would be a landmark transaction that would probably take two years to close. At Vukile Property Fund, they’ve raised that amount overnight from institutional shareholders. Sometimes we have to sit back and consider how amazing that is!

Having said that, capital raises are something that investors should always be wary of. Vukile will need to show investors that Italy is as strong a market as the Iberian Peninsula. There’s a strong track record here, which is why the market has happily invested the capital behind this ambition.

By now, you must be itching to know the price at which they placed shares. They managed to raise 9% of their market cap at a discount of 4.43% to the 10-day VWAP. I’m not surprised to see a discount of this size, as institutional investors need an incentive to invest more capital vs. buying shares in the market at leisure.

Ghost Bite: Vukile is one of the few companies that has made an offshore expansion work. I’m excited to see how this pans out.

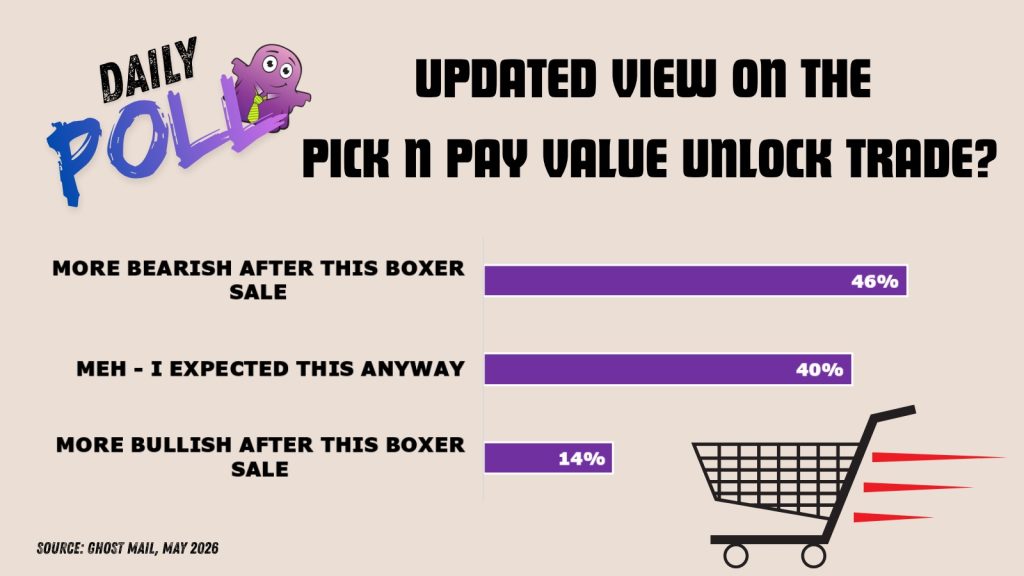

Results of previous poll:

Nibbles:

- Director dealings:

- An associate of the CEO of KAL Group (JSE: KAL) bought shares worth R1.5 million.

- A non-executive director of Momentum (JSE: MTM) sold shares worth R1.3 million.

- A director of Standard Bank (JSE: SBK) sold shares worth just over R1 million.

- The CEO of Choppies (JSE: CHP) bought shares and another director sold shares worth R249k. Even though it was an on-market deal, it looks like they traded with each other.

- The CFO of Heriot REIT (JSE: HET) bought shares worth R115k.

- Exemplar REITail (JSE: EXP) announced that the board is considering the award of immediately vested restricted shares to the CEO and CFO in line with the new plan approved by shareholders in April. This would replace forfeited awards under the previous plan. The announcement doesn’t indicate the value. I’m just mentioning it here as it has relevance to director remuneration and associated dealings.

- RMB Holdings (JSE: RMH) has released a trading statement for the six months ended March 2026. Due to various impairments, the net asset value (NAV) per share is expected to drop by between 20% and 30%. This suggests a range of 46.06 cents to 52.64 cents. In case you’re wondering, the offer by AttBid is priced at 47 cents per share. Some will argue that this is most convenient!

- YeboYethu (JSE: YYLBEE), the B-BBEE structure that holds a stake in Vodacom (JSE: VOD), has released a trading statement for the year ended March 2026. Thanks to Vodacom having such a strong run at the moment, the net asset value (NAV) of the structure has jumped by between 40% and 45%. The expected range is R103.27 to R106.96. The share price is trading at R55, with the discount to NAV being a common feature of an illiquid stock that can only be held by qualifying individuals. The price is up 110% in the past year though!

- Here’s an interesting non-executive director appointment for you! I don’t usually cover this kind of news, but Novus (JSE: NVS) has announced the appointment of Phil Roux as an independent non-executive director. Roux comes with quite the track record for turnarounds, most recently at Nampak (JSE: NPK) where he recently moved from the CEO role into a non-executive capacity.

- There might be a related party transaction at CMH (JSE: CMH), with the board contemplating the acquisition of properties owned by certain executive directors and leased to CMH. If they are highly strategic properties and the price is fair, then that could be fine. We will have to wait for the details.

- Despite a trading halt on the Orion Minerals (JSE: ORN) shares on the Australia Stock Exchange due to a potential capital raise, the company has released drilling results from the Okiep Copper Project. What must make this even more frustrating for Australian investors is that the JSE doesn’t have a corresponding trading halt, so shares are trading on this news on the JSE while punters in Australia are unable to get involved. I skip over the technical geological stuff and just look at the management commentary. It seems as though the CEO is very happy with the latest results.

- ISA Holdings (JSE: ISA) is busy with a small related party transaction in which they will sell their shares in Dataproof back to that company as a share buyback for R62 million. In an extremely confusing announcement trying to deal with two distinct corporate actions at the same time, it appears as though the conditions to the disposal have been fulfilled. I’m not even going to try and cover the rest of the regulatory word salad that was included in that SENS.

- With MC Mining (JSE: MCZ) under the control of Kinetic Development Group, there’s unsurprisingly been a change of chairman. Thankfully, their choice of Jianheng (Albert) Deng is encouraging, as he already has a lot of experience in the South African mining and broader ecosystem.