In this edition of Ghost Bites:

- CA&S dips into digital

- Chuckles all around for Premier investors

- Stor-Age is struggling in the UK

- Vukile is doing well everywhere – but especially in South Africa

CA&S dips into digital (JSE: CAA)

This is an interesting acquisition!

CA Sales Holdings (JSE: CAA) (known as CA&S) has earned a solid reputation for making excellent use of bolt-on acquisitions to bolster their operations across Africa.

We are used to seeing them acquire route-to-market companies. This helps FMCG players reach customers through a combination of distribution and merchandising services.

But the latest deal is quite different, as CA&S has stepped into the digital and eCommerce space. Omnichannel retail is becoming an increasingly important element of the retail landscape and this has been a blind spot for CA&S.

To address this gap, they’ve taken a 30% stake in The Digital Media Consultancy (TDMC), a company that offers services from Shopify development right through to email marketing and even influencer management. This is an interesting step!

In classic CA&S style, the deal includes a pathway to control. They are able to take a further 21% stake via call options, which would give them a total of 51%.

There’s no indication of the financial value of the deal. All we know is that it is too small to be categorised for the JSE or the Botswana Stock Exchange.

Ghost Bite: It’s great to see CA&S dipping their toes into the future. Bricks-and-mortar retail has a long way to go (especially in Africa), but bringing in an omnichannel skillset can only be valuable over the long term.

Chuckles all around for Premier investors (JSE: PMR)

Hopefully a new era at the company won’t leave a bad taste

Premier continues to be a wonderful example of the power of operating leverage. Revenue increased by 6.6% in the year ended March 2026, which you wouldn’t exactly classify as an exciting growth story. But once you work your way down the income statement and find HEPS growth of 27.7%, you might feel differently!

Premier is a food business with extensive exposure to bakery categories (Millbake was 81% of revenue in this period). This means that there are many factors at play here, including external commodity prices like maize. If price deflation is met by strong enough growth in volumes, then manufacturing efficiencies can be realised.

With group EBITDA margin up by 130 basis points to 13.1%, as well as operating profit margin up 150 basis points to 11.1%, there’s plenty for shareholders to feel good about here. The chef’s kiss for HEPS was a 27.5% decrease in net finance costs, driven by reduced debt levels.

When your cash generated from operations increases by 39.5%, chances are good that the health of your balance sheet will improve as well. The group leverage ratio is just 0.5x, so most of the uplift in growth between revenue and HEPS is thanks to operating leverage (fixed costs) rather than financial leverage (debt).

Digging deeper, Millbake achieved revenue growth of 5.1% and EBITDA growth of 18.3%, so the bakery team deserves plenty of credit (as usual).

The Groceries and International segment was skewed by the acquisition of RFG in March 2026. Although the results were only included for less than a month, this still bumped up growth in this division, as Premier essentially bought more earnings. Groceries and International grew revenue by 13.5% and EBITDA by 29.6%.

The shape of the group will change given the recent acquisitions. Millbake is expected to be two-thirds of EBITDA going forwards. My hope is that they don’t dilute the elements of the Premier business model that make it so special. The history books are filled with FMCG companies that tried too hard to diversify and ended up diworsifying instead.

Ghost Bites: On top of all the other good news, Premier also took on the chocolate range at Woolworths. With the share price up 34% over 12 months, it’s Chuckles all round for investors. But I must be honest that I can taste a difference in Chuckles (other than the red pack, which hasn’t changed), while a quick online search reveals that I’m not the only one. I suspect I’m heading back to Whispers for my chocolate fix.

Stor-Age is struggling in the UK (JSE: SSS)

The UK economy can be unforgiving

Stor-Age has a more even split across SA and the UK than most people realise. These days, they have 64 properties at home and 46 in the UK. Stor-Age isn’t thought of as an example of a major offshore expansion strategy, but they probably deserve more credit for their growth ambitions.

The UK market hasn’t delivered great numbers in the latest period though. For the year ended March 2026, the SA portfolio achieved rental income growth of 10.5%, while net property operating income was up 11.1%. In the UK, rental income was up by just 1.1% and net property operating income dipped by 0.8%!

This is why the blended group results aren’t going to set anyone’s hair on fire. There was an increase in the number of shares in issue (they raised R500 million in December 2025), so growth of 8.4% in distributable earnings was diluted into dividend per share growth of 5.1%. It’s ahead of inflation, but not by much.

The net tangible asset value per share is up by 3.9%, so that at least that adds to the growth story alongside the dividend. With a loan-to-value ratio of 29.7%, the balance sheet is a decent story overall.

There’s clearly a lot of work to do in the UK, particularly as the occupancy rate is only 81.6% in that market vs. 93.4% in SA. They talk about a “tougher cyclical environment” for the UK platform.

Investors will hope that these are cyclical rather than structural issues, otherwise Stor-Age might start to be used as an example of offshore expansion for all the wrong reasons!

These difficulties mean that guidance for FY27 is distributable income per share growth of just 5.0%, much the same as we’ve seen in FY26.

Ghost Bite: The market didn’t love these numbers, with the share price down 3% on the day. At R16.70, Stor-Age is a long way off the 52-week high of R19.32 achieved in late February (before the macroeconomic situation changed thanks to the Iran conflict).

Vukile is doing well everywhere – but especially in South Africa (JSE: VKE)

These results are the perfect foundation for the expansion into Italy

Vukile Property Fund has released excellent numbers for the year ended March 2026. The total dividend for the year was up by 9.3%, offering investors a strong real return (the return ahead of inflation).

This growth was underpinned by exceptional numbers in South Africa. The local portfolio achieved like-for-like retail net operating income growth of 10.3%, with trading density up by an impressive 5.3%. This means that the shops are busier, so tenants are making money. And if tenants are doing well, the same is true for the landlord!

Aside from turnover clauses, the benefit also comes through in rental reversions, a measure of how the rental amount changed on a new lease vs. the previous lease. Reversions increased from +2.4% to +37%. The “+” signs are important there, as reversions can turn negative – just ask office property funds!

These solid numbers drove a 12.3% like-for-like increase in the value of the retail portfolio in South Africa.

Then, in Iberia (Spain and Portugal – for those who didn’t take geography), Castellana achieved like-for-like net operating income growth of 7.9%. Rental reversions were excellent at +9.1%, driving a like-for-like valuation increase of 6.6%. That’s a solid outcome when you consider the difficult macroeconomic environment in the developed world.

Vukile’s balance sheet is healthy, with a loan-to-value ratio of 38.4%. They make extensive use of green loans, with solar installations now generating 29% of electricity in the portfolio. The credit ratings for both Vukile and Castellana were recently upgraded as well.

When they need equity for growth, there’s no shortage of interest from investors. Vukile had no problems raising R2.8 billion in an oversubscribed equity issuance in May 2026 (i.e. after this reporting period). This enabled their entry into Italy, with Vukile’s European portfolio starting to sound like something out of a travel brochure!

For FY27, they are forecasting growth in funds from operations (FFO) per share of between 8% and 10%. By slightly increasing the dividend payout ratio, they expect to grow the dividend per share by between 10% and 12%.

Ghost Bite: Vukile is an excellent example of the high quality companies available on the JSE. The total return over 12 months (i.e. including the dividend) is 35%!

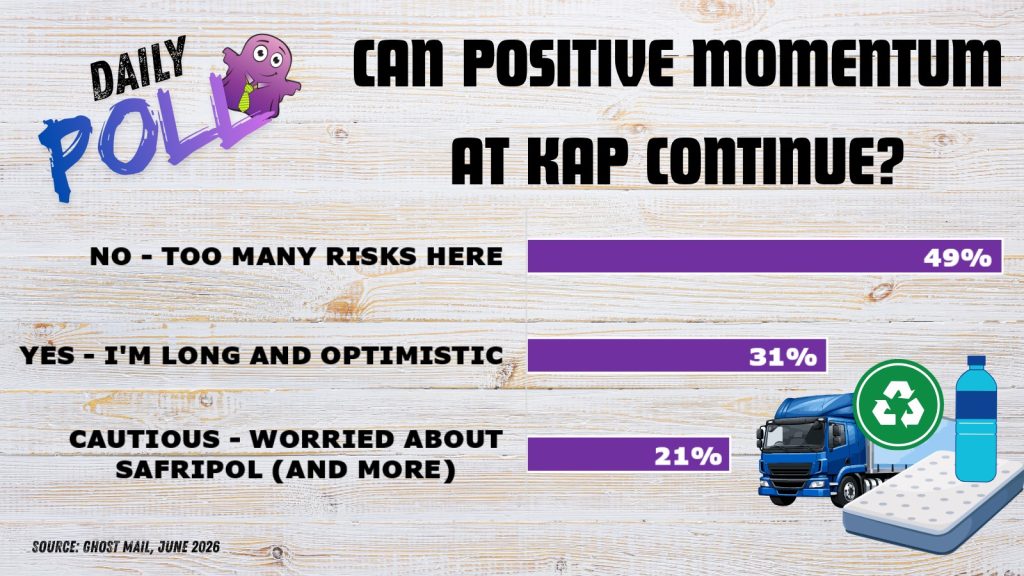

Results of previous poll:

Nibbles:

- Director dealings:

- A director of Nu-World (JSE: NWL) acquired shares worth R2.4 million.

- An independent non-executive director of NEPI Rockcastle (JSE: NRP) bought shares worth R281k.

- A person closely associated with the CEO of Sirius Real Estate (JSE: SRE) bought shares worth around R110k.

- Powerfleet (JSE: PWR) has released results for the year ended March 2026. Although revenue was up 22%, they still reported a headline loss of $20.6 million vs. a loss of $51 million in the prior period. At least they were profitable at operating profit level, with positive $19.6 million vs. a loss of $25.9 million in the prior period. Like all good US-based tech companies, adjusted EBITDA went in the right direction, up by 44% to $97 million.

- Brikor (JSE: BIK) released results for the year ended 28 February 2026. They are late, with the JSE having fired a warning shot a few days ago regarding this release not being on time. Revenue fell by 16.6% and they experienced a nasty swing from positive HEPS of 0.5 cents to a headline loss of 1.1 cents per share. They were impacted by weak demand in the bricks sector as well as lower coal production volumes. To give you an idea of how tough it is, the gross margin in the bricks segment was just 13.6% (vs. 29.2% in the prior period). Gross indeed! As a reminder, the board of Brikor is currently weighing up the delisting of the company.

- Holders of 46.12% of Dipula (JSE: DIB) shares elected the dividend re-investment option. This allowed Dipula to retain R128.5 million in equity, as shares were issued to these investors in lieu of cash dividends. Property funds love these outcomes, as it’s like executing a little capital raise without going through nearly as much admin.

- Advtech (JSE: ADH) has been busy with share repurchases. Between 30 March 2026 and 10 June 2026, they’ve invested R250 million in repurchasing 1.04% of shares in issue. The share price has been doing very well, up 42% over 12 months and 17% year-to-date.

- Investec (JSE: INP | JSE: INP) announced that Fitch has upgraded their credit rating on long-term debt from BB- to BB, with a stable outlook. This is related to Fitch’s decision to upgrade South Africa’s sovereign debt earlier this month. When a country’s financials are in better shape, banks can access cheaper funding. These benefits then flow through the economy.

- AB InBev (JSE: ANH) announced that existing independent director Dirk Van de Put has been appointed as the new Chairman of the Board, having already served on the board for three years. Interestingly, Van de Put is the current Chairman and CEO of Mondelez International. How does he find the time for this role as well?

- There’s a change to the governance structure at MAS (JSE: MSP), with Martin Slabbert resigning as a director and Chairman of MAS and being appointed as Chairman of PKM Development (the joint venture company). This is after Mihail Vasilescu moved from Chairman of PKM Development to CEO of MAS. Dewald Joubert has been appointed as Chairman of MAS, stepping into that role from his current position as Lead Independent Non-Executive Director.

- Clientèle (JSE: CLI) has confirmed that the final offer price is R19.90 per share. This will be structured as a dividend, so shareholders accepting the offer will need to take that into account in their tax considerations. Dividend tax of 20% will apply for shareholders who are not exempt from this tax.

- Numeral (JSE: XII) has changed its classification on the Stock Exchange of Mauritius (SEM). They are moving to the Investments category, reflecting the plan to build a portfolio of business interests beyond the biotechnology, healthcare and pharmaceutical businesses. Essentially, this just gives them the flexibility to execute investments in a wider variety of sectors. The results for the year ended February 2026 are still in the audit process, with the SEM granting an extension until mid-July 2026 for their release.

- A couple of companies are late in the release of their financial statements. Financials are supposed to be filed no more than three months after the end of a period. Mantengu (JSE: MTU) and Visual International (JSE: VIS) are in the naughty corner. For now, they are just on the radar of the JSE – the listings haven’t been suspended at this stage.

- Oando (JSE: OAN) is still trying to get its 2025 financial statement released. They are falling behind, as the Q1 2026 numbers are also due. The delay is related to a regulatory review of the 2025 financials by the Financial Reporting Council of Nigeria.