In this edition of Ghost Bites:

- Encouraging signs at Exxaro

- Gold Fields is trying to allay fears about the Tarkwa mine

- A slower quarter at Standard Bank, but a positive outlook

Encouraging signs at Exxaro (JSE: GFI)

Detailed interim results will be interesting

Exxaro has released a pre-close message for the six months to June 2026. This is part of the broader capital markets day hosted by the company.

Exxaro has seen an increase in coal export, iron ore fines and manganese ore prices over the past year. Coal export prices spiked recently due to the Iran conflict and a switch from gas to thermal coal by many international users. Spot prices have since moderated, based on expectations of the conflict ending, but the spike obviously helped Exxaro on a short-term basis.

For this interim period, they expect coal production to be up by 10% and sales to increase by 6%. Export sales were up by 15%, so it was domestic sales that dragged that number down. Eskom demand is stable, while sales to the ferrochrome market and ArcelorMittal (JSE: ACL) were down.

The export business was assisted by an important 7% increase in performance at Transnet Freight Rail.

Capex in the coal business is expected to be 69% higher in this interim period, so they’ve had some significant capital replacement projects to execute. They expect capex for FY26 to be in line with previous guidance of between R4 billion and R4.5 billion.

Exxaro is also pushing hard in their renewables business, with construction of the Karreebosch wind farm in progress. They are also busy acquiring the operating assets of Acciona Energia, giving them more wind and solar power. Exxaro’s mix of legacy and renewable energy sources is particularly unusual.

The overall story is one of consistent full-year guidance in key areas, as well as some promising underlying metrics for the interim period. We will only know for sure when interim results are released in August.

Ghost Bite: Working through the detailed presentations from a capital markets day is always a good idea. You can find them here.

Gold Fields is trying to allay fears about the Tarkwa mine (JSE: GFI)

Media reports have suggested that there is a significant risk here

Various recent reports in the media have suggested that Ghana is considering a change of control of the Tarkwa mine, where the lease held by Gold Fields expires in 2027.

This is a critical asset for Gold Fields, accounting for roughly a fifth of the group’s total production!

Gold Fields responded to the media reports with a SENS announcement noting that negotiations with the Government of Ghana are in process, regarding the terms of the mining lease renewals. An early application for renewal of the leases had already been submitted in 2025, so this has been going on for a while.

Ghost Bite: Nothing is ever certain when you’re dealing with African governments. It wouldn’t surprise me at all if there’s at least some truth to the media speculation. Gold Fields will hopefully manage to get this one across the line.

A slower quarter at Standard Bank, but a positive outlook (JSE: SBK)

Periods of geopolitical upheaval are difficult for lending businesses

Standard Bank’s voluntary trading update for the five months to 31 May 2026 covers a volatile period in the market, where inflation expectations spiked thanks to the oil price.

We also saw a small rate hike by the SARB, as well as credit rating agencies recognising the progress made in South Africa.

In summary, it hasn’t been a boring time in the world!

If you’re hoping for precise numbers in this update, you’ll be disappointed. They are heavy on narrative and light on actual details, other than an overall message that earnings growth has “moderated” vs. the 12% earnings growth in the first quarter of the year. In other words, the second quarter was a slower growth rate, but we don’t know to what extent.

Africa is a critical part of the Standard Bank investment case. West and East Africa did well, more than offsetting a weaker performance in the South & Central Region.

It sounds like net interest income (NII) came under pressure due to lower average rates and particularly competitive environments in areas like home loans. Impairments were lower though, so that should drive a better result net of impairments.

Non-interest revenue (NIR) was boosted by trading revenue, which isn’t a surprise during a volatile period. They’ve also flagged strong momentum in the Insurance and Asset Management business.

Cost growth was in line with revenue growth, so there’s no sustainable margin uplift story to tell here. With impairments coming in lower though, we still might see a better percentage increase in earnings relative to revenue.

The balance sheet remains in excellent health, with a CET1 ratio of 13.2%. This measures the extent of equity on the balance sheet. A higher CET1 ratio is less risky for investors, but also makes it harder to generate a strong Return on Equity (ROE) as there is simply more equity running around.

For now, Standard Bank has left full-year guidance unchanged, while noting that this quarter put a dent in client confidence and related activity. The market is expecting these issues to dissipate, so Standard Bank remains positive on the full-year picture for now.

Ghost Bite: With Standard Bank’s share price up 46% in the past year and 13% year-to-date, the market hasn’t been concerned about the global geopolitical picture. Positive sentiment around Africa is carrying this share price.

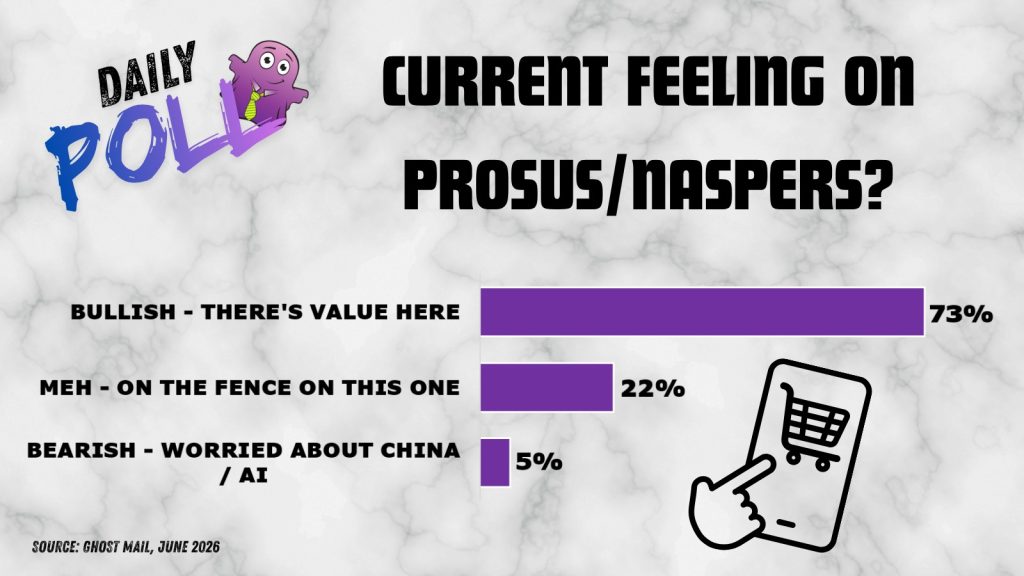

Results of previous poll:

Nibbles:

- Director dealings:

- The crew at Vukile Property Fund (JSE: VKE) are cashing in on a fantastic run in the share price. Top execs, including the CEO and CFO, sold share awards (in excess of the taxable portion) worth a total of over R40 million. I must commend the company on the brilliant layout of their announcement, which makes it very easy to see the taxable vs. non-taxable portion. This should be the industry standard!

- The CEO of SA Corporate Real Estate (JSE: SAC) sold only the taxable portion of a share award, but the same can’t be said for a few other execs who sold shares worth R4.7 million (including their taxable portions).

- Good news for Pan African Resources (JSE: PAN) investors: the acquisition of Emmerson Resources has been approved by the shareholders of that company. Court approval in Australia has also been obtained, so Pan African has now been admitted to the official list of the Australian Stock Exchange (ASX) as well. Trading on a normal settlement basis on ASX will comment on 2 July 2026.

- Eastern Platinum (JSE: EPS) is in the market for a new CFO, as Wylie Hui has resigned with effect from 10th July 2026. He will assist during a transition period for whoever the new CFO will be.

- Quilter (JSE: QLT) is busy with a share buyback programme of up to £100 million. For context, the group market cap is R57 billion, so this is around 4% of the market cap. Thus far, they’ve repurchased £32 million in shares on the London Stock Exchange and £8 million on the JSE.

- Mantengu (JSE: MTU) has released an updated trading statement that reflects a headline loss for the year ended February 2026 of 90 cents. To add further insult to the ridiculous situation that happened last year, the JSE has also censured Merchantec Capital for releasing Mantengu announcements that were found to be “speculative, unverified and lacking the required degree of specificity and precision”. As I was one of the people who Mantengu threw mud at in the hope that something would stick, I 100% support this decision. Lacking in precision is probably the nicest way to put it. Even Merchantec’s attempts to get the company to retract the announcements didn’t prevent this censure, giving the entire market a reminder of the responsibility carried by Sponsors and Designated Advisors who release SENS announcements on behalf of companies.

- If you are a shareholder in Afine (JSE: ANI), the REIT that has a portfolio of fuel forecourts, then be aware that the company has announced the reinvestment price for the dividend reinvest alternative. Shareholders are able to reinvest up to 25% of their dividend in the company at 437.89 cents, calculated as the 30-day VWAP minus the gross dividend.

- As a reminder of how dangerous the mining sector still is, Harmony (JSE: HAR) reported a tragic loss-of-life incident at Moab Khotsong mine. This was due to a fall-of-ground incident.