In this edition of Ghost Bites:

- Anglo American unlocks a copper adjacency at Los Bronces

- Growthpoint wants quality, not quantity

- Nedbank’s performance looks decent

- Optasia has resumed operations in Nigeria

- Primary Health Properties is in negotiations around a private hospital joint venture

- Schroder European Real Estate is throwing in the towel

Anglo American unlocks a copper adjacency at Los Bronces (JSE: AGL)

Copper is still the commodity that everyone is chasing

Anglo American has announced a joint mine plan with Codelco for the Los Bronces mine in Chile.

The adjacent Andina copper mine creates an opportunity for the two companies to work together, unlocking synergies and making more money for everyone along the way.

According to Anglo, this unlocks at least $5 billion in shared additional value, based on the uplift in production over the next 21 years.

Naturally, this number can technically be whatever anyone wants it to be – it all comes down to the underlying assumptions.

Ghost Bite: The actual value uplift is debatable, but the direction of travel is not – this seems like a sensible approach by the companies. It does remain subject to permits though, so something could still go wrong in the implementation process.

Growthpoint wants quality, not quantity (JSE: GRT)

But the numbers are still enormous at this R60bn market cap fund

Growthpoint has given investors an update on progress made over the nine months to 31 March 2026. It’s a very detailed look at the operations, so buckle up.

The iconic REIT is busy simplifying its portfolio and transitioning from quantity to quality, an important and necessary step in a difficult economy. South Africa has rewarded surgical strategies, not broad exposure. This is driving Growthpoint’s precinct-focused strategy, perhaps learning from the success of REITs who have been more focused.

We are talking serious numbers here, with previously targeted disposals of R3.5 billion for the year ending June 2026. B-grade and C-grade offices are on the chopping block, along with certain other assets. They’ve already sold and transferred R2 billion of assets at a modest profit to book value. Thanks to strong disposal activity, including the 55% interest in the Discovery building for R2.3 billion, they expect disposals of R5.1 billion for FY26 – way ahead of target.

Capital is being recycled into other, more desirable asset classes. This includes the Logistics & Industrial sector. Where it makes sense to do so, Growthpoint redevelops underperforming assets as well, with targeted investment of R1.3 billion in the year ending June 2026. Thus far, they’ve spent R793 million this year (including other capital expenditure).

It sounds like Growthpoint would be happy to pull the trigger on South African deals, as their balance sheet is almost too conservative now. It’s important for REITs to operate in an optimal window when it comes to leverage, especially when the weighted average cost of debt has come down (despite the recent SARB decision). Growthpoint has no problem tapping debt markets, evidenced by an oversubscribed R1.8 billion bond issuance in June 2026 at record-low margins.

One of the exciting projects in years to come is the Cape Winelands Airport, where Growthpoint will oversee Phase 1 of the development and will focus on the ancillary land opportunities thereafter.

The overall South African portfolio has seen vacancies improve from 8.2% to 7.3%. The lease renewal success rate is the highest in more than a decade, while negative reversions have improved from -4.0% to -2.8%. The office sector has been a notable source of improvement (from -9.6% to -7.1%), but I’m sure that is mostly thanks to the disposals of low-quality offices.

To give you an idea of the regional differences, Growthpoint’s office portfolio recorded vacancies of just 3.0% in the Western Cape vs. a massive 18.9% in Gauteng. KwaZulu-Natal sits at just 1.3%. Sure, the extent of the underlying portfolios will make a difference here, but Sandton is nowhere near the crown jewel that it once was.

Importantly, footfall in the retail portfolio increased by 1.2%. Malls are holding their own against eCommerce, at least for the time being. Trading density growth of 3.2% is decent, especially as it accelerated to 4.2% in the March 2026 quarter. Value-oriented formats continue to outperform, so take that into account as you consider your retail exposure.

The V&A Waterfront is the single most important asset in the portfolio, but EBIT was only up marginally year-on-year due to the redevelopment of the Table Bay Hotel. Footfall was up 1.2% and retail sales grew by 5.1%. There’s a significant development pipeline at the property, including more hotels and apartments. Residential sales will contribute to the expected double-digit growth in distributions for FY26.

On the international front, where Growthpoint has exposure to tricky markets like Australia, there’s a lot of talk around initiatives to unlock shareholder value. For now, Growthpoint Australia has reaffirmed guidance for funds from operations this year, despite the general challenges of that market.

I suspect that just about every option is on the table for the global assets. It will all come down to price and the opportunities that present themselves. One area where we know there will be action is Lango Real Estate, which is contractually required to list on a suitable exchange. The London Stock Exchange is the intended destination.

Overall, guidance for the year of distributable income per share growth of 3% – 5% is unchanged. The dividend per share growth expectation of 6.0% – 8.0% is also still in play. But Growthpoint has noted an overall shift towards a more conservative outlook beyond this period.

In leadership news, Norbert Sasse will step down as group CEO on 1 July 2026. Estienne de Klerk will step into the group role.

Ghost Bite: Growthpoint is up 31% in the past year, or 42% on a total return basis. This is one of the many reasons why I prefer putting my own money in REITs vs. a buy-to-let headache.

Nedbank’s performance looks decent (JSE: NED)

Especially in the context of the modest valuation multiple

Nedbank has added its name to the list of banks that have released pre-close updates. For the first five months of the year, headline earnings have been in line with management expectations. This has led to the group affirming its 2026 guidance.

Pre-provisioning operating profit has grown by high-single digits, which is encouraging. This was partially offset by higher impairments and the loss of associate income from Ecobank after they sold that investment. Thanks to share buybacks and other positive factors, it all filters down into growth in headline earnings of “upper single digits” – a reasonable outcome.

The core banking operation is making progress, with net interest income (NII) growth of low- to mid-single digits. Asset growth was in the mid- to upper-single digit range, but a decline in net interest margin took the shine off that number.

Where Nedbank seems to be deviating from peers is in the credit loss ratio, which is sitting in the upper half of the through-the-cycle range. This is worse than what we’ve seen in other recent sector updates. There was a major client default in Business and Commercial Banking that has affected the number, although it’s odd that there can be a client in the mid-market segment of sufficient size to have this effect.

Non-interest revenue managed upper-single digit growth, with insurance income as one of the major boosts.

Expense growth was below mid-single digits. They expect this level of control control to continue for the rest of FY26.

On the corporate front, the NCBA deal in Kenya has received a number a critical regulatory approvals. There are still some boxes to be ticked. Importantly, the offer to NCBA shareholders will close on 10 July, with the results expected to be announced by no later than 21 July.

Ghost Bite: On a P/E of just 7.6x, Nedbank achieving “upper-single digit” growth in headline earnings would put them on a PEG ratio of roughly 1x. Shareholders tend to make money when the valuation is that appealing.

Optasia has resumed operations in Nigeria (JSE: OPA)

But the damage to the investment case has been done

Having listed towards the end of 2025, Optasia promised the market a growth story built around distribution of financial and value-added services in Africa via smartphones.

It all sounded very impressive, with the share price doing well until the end of January. Then the story started to unravel, with considerable insider selling and of course the conflict in Iran as well.

But the real disaster was to come: a suspension of operations in Nigeria for regulatory reasons, along with damaging commentary from telcos about how little of an impact the loss of Optasia’s services was having on their business.

If your operations can shut down for a period of time without anyone really noticing, you have no moat. Without a moat, there’s no justification for a premium valuation.

The good news is that operations have resumed in Nigeria. The damage has been done though, with the share price having shed 31% of its value year-to-date.

Ghost Bite: IPOs are always very risky things to invest in. Even by those standards, this one fell apart incredibly quickly. They have much work to do to rebuild trust in the market.

Primary Health Properties is in negotiations around a private hospital joint venture (JSE: PHP)

There’s no certainty at this stage that anything will happen

Primary Health Properties previously told the market that they were looking at strategic options around the private hospital portfolio.

The company has now had its hand forced by press speculation, confirming that they are in negotiations around using the private hospital portfolio to seed a new joint venture.

Although they refer to “advanced discussions” with a potential partner, there’s no guarantee of anything going ahead. But this didn’t stop the share price from going bananas, up 26% on the day!

Ghost Bite: There’s nothing the market loves more than ignoring the risk of transaction failure. If you’ve ever been involved in dealmaking, you’ll know just how many transactions fall over during the negotiation stage.

Schroder European Real Estate is throwing in the towel (JSE: SCD)

They will execute an orderly wind-down over the next couple of years

Schroder European Real Estate released results for the six months to March 2026. But even more importantly, they are looking to achieve an orderly wind-down of the structure and a return of capital to shareholders.

This has been a terrible performer relative to sector peers, so I’m not surprised. It will take them two to three years to get it done, so this is a good example of the “marketability” discount in action – investors are smart enough to recognise the difficulties and delays in the sale of assets.

The group still hasn’t recognised a provision for the French Tax Authority dispute, despite it being an enormous €14.9 million vs. the current NAV of €151.3 million. Talk about an overhang!

I must note that the NAV fell by nearly 2% year-on-year purely due to valuation pressure in the underlying portfolio, so they have more problems than just the tax.

I had to chuckle at the Chairman’s comments that there’s a shift in investor sentient towards larger, more liquid equities. Sure, but there’s also a shift towards companies that aren’t at risk of losing 10% of their value to a tax dispute…

Ghost Bite: With a total return over 5 years of 7.4% (not per year – in total!), I don’t think anyone is going to miss this one.

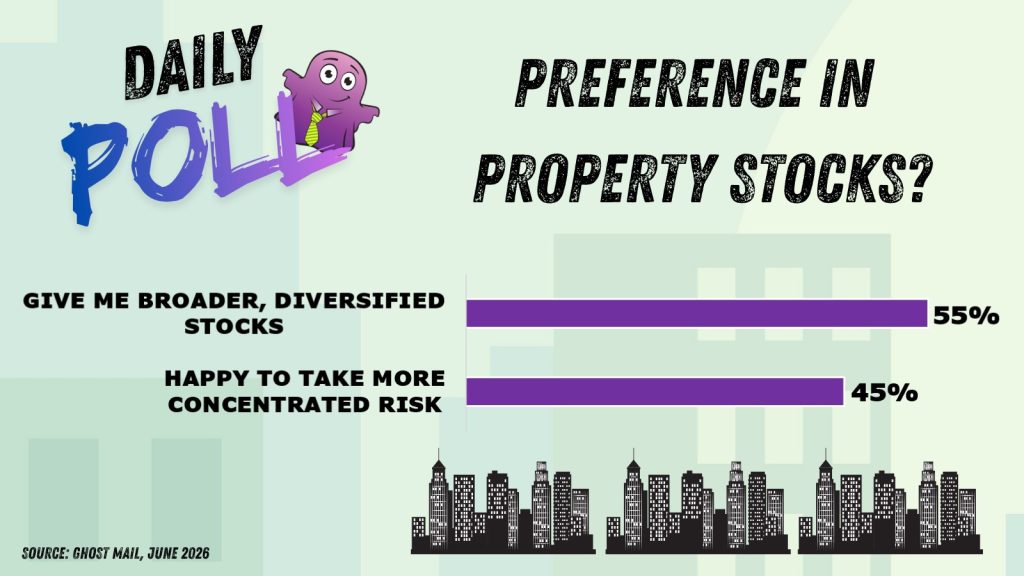

Results of previous poll:

Nibbles:

- Director dealings:

- The CEO and founder of Datatec (JSE: DTC) repriced options over the stock worth almost R220 million. They expire at the end of August 2027. The collar has a put strike price of R91.57 and a call strike price of R121.78. The current spot price is R94.86, so this is giving strong downside protection from current levels.

- A senior exec at Quilter (JSE: QLT) sold shares worth around R5.4 million.

- The Chair of Gold Fields (JSE: GFI) bought shares worth R275k.

- Salungano Group (JSE: SLG) released a trading statement for the year ended March 2026. They expect HEPS to jump to between 50.59 cents and 51.11 cents, vastly higher than 2.62 cents in the comparable period. Results will be released before 30 June 2026.

- Crookes Brothers (JSE: CKS) released an updated trading statement. We already know from the initial trading statement that the year ended March 2026 was awful, with lower earnings across all group segments. Farming is incredibly tough, with their macadamia business described as being “commercially unsustainable” at current prices. The headline loss will be 167.2 cents, much worse than the guidance in the initial trading statement (of HEPS being between 2.35 cents and 27.85 cents). One of the reasons for this difference is deferred tax balances in Mozambique. Either way, it’s a disaster.

- Greencoat Renewables (JSE: GCT) is moving ahead with the next tranche of share repurchases. They’ve completed €25 million of a €100 million share buyback programme. They are now commencing the next €25 million.

- Wesizwe Platinum (JSE: WEZ) suffered a cyberattack in December 2024 that led to huge delays in financial reporting. As part of the recovery, they are busy with a major SAP ERP system implementation. They had planned a go-live in June 2026, but they are going to miss that deadline due to how long it took to catch up on their financial reporting. They’ve made a lot of progress on the implementation, but no new go-live date has been given.

- Having moved its listing from the AltX to the Main Board of the JSE, Africa Bitcoin Corporation (JSE: BAC) has now executed a similar migration of its listing on the Namibian Stock Exchange. It wouldn’t make sense to be on the development board on one exchange and the primary board on the other.

- PSG Financial Services (JSE: KST) has decided to withdraw their listing on the Stock Exchange of Mauritius (SEM). This will leave them with listings on the JSE and Namibian Stock Exchange only.

- Omnia Holdings (JSE: OMN) received approval by the SARB for the special dividend of 280 cents per share. It will be paid on 8 June 2026.