In this edition of Ghost Bites:

- ACOF, the best part of Africa Bitcoin Corporation, is making progress

- Decent growth at Argent Industrial

- Fortress taps the market for capital

- Goldrush battles disruption from online gambling

- Invicta could do with a boost from South Africa

- Lighthouse Properties is doing well in Europe

- Prosus has grown free cash flow significantly

- SA Corporate Real Estate is generating real growth for investors

ACOF, the best part of Africa Bitcoin Corporation, is making progress (JSE: BAC | JSE: BACC)

They are plugging an important gap for SMEs

I’ve made no secret of my appreciation of what they are trying to build at the Altvest Credit Opportunities Fund. Access to funding is critical for SMEs in South Africa. The banks really aren’t great at lending into this space, so any effort to address that should be applauded.

The rates need to be high due to the default risk, with the ACOF book running at an average of prime+7.8%. But for an SME that needs inventory or a shop fit-out, the potential returns are vastly higher than this effective interest rate. This is why a lack of access to funding can be so frustrating.

In an update for the quarter ended May 2026, ACOF confirmed that their average loan size is R6.2 million and that they currently have 45 funded SMEs. Alongside the average term of 43 months, that gives you an idea of how they operate.

There’s no shortage of demand for loans at these levels, with the fund reducing its cash balance from R156 million to R80 million based on deployments. They cannot possibly achieve profitability without having a large book out there working for them and earning a return, so deployments are key.

The outstanding loan book balance at 31 May 2026 was R338 million.

The provision for bad debts is 3.77% of the current loan book, an improvement from 4.12% as at February 2026. This shows you why the interest rates need to be higher than secured consumer debt. ACOF needs to cover the credit losses, the cost of its funding (e.g. its DMTN programme) and its operating expenses.

The security coverage ratio across the loan book is between 1.5x and 2.6x. Even at ACOF, it’s very hard to borrow money as an entrepreneur if you don’t have assets as security. Skin in the game is critical.

And in other news from the group, Africa Bitcoin Corporation (the holding company) is pursuing a listing on the Aquis Growth Market in London. They are calling all pockets in terms of potential access to capital.

Ghost Bite: ACOF is the part of the group that I think is most interesting. I just hope they can scale to profitability in time.

Decent growth at Argent Industrial (JSE: ART)

But they could do with more leverage

Argent Industrial’s results for the year ended March 2026 reflect decent growth overall. Revenue was up 7.7%, EBITDA was good for 9.5% growth and HEPS increased by 9.1%. Dividend per share growth crept into the double digits, up 11%.

It’s a good outcome for shareholders, but there’s not much leverage in a business that only grows HEPS by 9.1% based on revenue growth of 7.7%.

The modest level of debt also results in return on equity of just 14.2%, which doesn’t feel exciting enough for this industry.

Looking at the segmentals, the Manufacturing area of the business achieved revenue growth of 11.9% and profit before tax growth of 16.6%.

This strong performance was dragged down by the Steel Trading segment, which saw revenue fall by a nasty 20%. This was severe enough to put that segment in a loss-making position of R11 million (vs. profit of R6. million in the prior year).

From a geographical perspective, the group’s South African operations grew profit before tax by 8.3%. The local operations contribute only 27% of group profit before tax, showing you the extent to which Argent has built offshore operations. The offshore business grew profit before tax by 13.3%.

Argent’s share price has jumped by 35% in the past year, giving shareholders a total return (including dividends) of 41%.

Ghost Bite: On a P/E of 6.8x, Argent Industrial is one of the many South African companies that is trading at a low multiple. The earnings growth looks fine in that context. They have a particularly strong balance sheet that could probably absorb more risk, so let’s see what route they take going forwards.

Fortress taps the market for capital (JSE: FFB)

They want to fund their development pipeline

Fortress Real Estate announced an accelerated bookbuild of approximately 52 million new shares, or 4.3% of shares in issue. This would raise around R1.3 billion at current share prices, with the pricing of the bookbuild to be established through the process run by the bookrunners.

This is one of those invite-only capital raises, so only institutional investors would’ve received their phone calls and emails on Monday evening.

The capital isn’t needed for a specific acquisition. Instead, Fortress is looking to bulk up its war chest for a variety of purposes. This includes expansion of the South African retail portfolio, as well as development of the logistics portfolio in South Africa as well as Central and Eastern Europe.

They have a development pipeline of roughly R5.2 billion. They plan to execute over the next three to five years. The non-core portfolio that they are looking to dispose of is worth around R2.5 billion. This leaves a hole that needs to be plugged through a combination of equity and debt.

Ghost Bite: It’s a pretty sound rationale, as the idea is to have the cash available to prevent rushed sales of non-core assets to fund the development pipeline. I can’t fault that. I’m quite sure that Fortress will have no problem raising the funding.

Goldrush battles disruption from online gambling (JSE: GRSP)

How important will the lottery licence be for this group?

Goldrush released results for the year ended March 2026. Revenue was flat and HEPS dropped sharply from 141.91 cents to 54.47 cents. The group reported a swing in fortunes from an operating profit of R243 million to an operating loss of R425 million.

Importantly, cash generated from operations was R287 million. This is down 27% year-on-year due to the investment required in equipment on behalf of Sizekhaya, the consortium that won the South African lottery licence.

The group is still generating cash, but earnings have clearly moved in the wrong direction.

The proliferation of online gambling is to blame here, with immense competition to attract customers on their smartphones. This has changed the game in this market, as licence holders in the brick-and-mortar space (like bingo halls etc.) cannot rely on sensible geographical exclusivity to compete.

A good analogy would be the pharmacy industry, if online pharmacy suddenly became prolific. Community and traditional pharmacy groups would find themselves competing against online behemoths with marketing budgets that benefit from scale and entirely different margins. You can imagine how that would end.

Goldrush’s shareholder letter has the kind of transparency that you won’t usually see in corporate settings, with a detailed explanation of how online betting has impacted the industry in recent years. The management team acknowledges that this has reduced the value of all gambling licences, including theirs.

The bigger question of course is around where things will settle. Management quotes a statistic that 69% of gambling revenue is now online, with land-based options scrambling for the remaining 31%. Land-based won’t go to zero, but just how low might it go over time?

Goldrush has an online business which grew revenue by 22% to R292 million. The problem is that total group income was R1.95 billion, so online is a small part of the overall story.

The lottery will be an important defensive underpin for the group in years to come. Although there is still a legal challenge around the award of the licence, previous court judgments have been favourable for Sizekhaya (and thus Goldrush).

Ghost Bite: There’s all to play for, literally. The lottery infrastructure has been put in place ahead of time and below budget, so that’s a good sign. The 2027 financial year is going to be critical for Goldrush, as the economics of the lottery licence should become visible to the market (for better or worse).

Invicta could do with a boost from South Africa (JSE: IVT)

The pressure on local industry is permeating many value chains

Invicta is one of those positions in my portfolio that I’ve learnt to just leave alone to do its thing. With a total return over 3 years of 45%, the group is doing a great job of delivering returns.

This doesn’t mean that every period looks good, with HEPS up by just 1% for the year ended March 2026. Importantly, the group reports sustainable HEPS growth of 7%.

Naturally, any management-specific view on earnings should be treated with caution. Invicta gives a thorough breakdown of the adjustments to arrive at sustainable HEPS, many of which relate to accounting adjustments on acquisitions and asset disposals.

Despite the growth in sustainable HEPS, this will go down as a tough year for Invicta. Revenue was up just 4%, which was nowhere near enough to offset the 10% increase in expenses. Operating profit fell by 9% and EBITDA was down 7%.

Digging into the segmental performance, the Industrial Solutions and Parts segment saw revenue dip by 1.7% and sustainable operating profit before forex movements fall by 10%. Return on net operating assets came down sharply from 19.3% to 16.5%. With 77% of revenue generated in South Africa, the general pressure on the local economy in areas like steel has filtered through to Invicta.

At Capital Equipment and Parts, revenue jumped by 19.1%, yet sustainable operating profit before forex movements dipped by 2.5%. Return on net operating assets also declined slightly from 15.7% to 14.5%. This business only generates 52% of its revenue from South Africa.

As is usually the case, Invicta has been busy with various acquisitions and disposals. The big one in this period was the acquisition of Spaldings in the UK for £10.5 million.

Ghost Bite: Invicta trades on a mid-single digit P/E. Nobody is expecting them to generate double-digit growth in HEPS. It would certainly be nice to see the local situation in South Africa improve and boost Invicta, but I’ll let management allocate my small amount of capital in this stock accordingly.

Lighthouse Properties is doing well in Europe (JSE: LTE)

France has been a particular highlight of recent trading

Lighthouse Properties released a pre-close update for the six months to June 2025. This is a European-focused fund, so get ready to read about places you would probably want to visit on holiday.

The update uses the numbers for the first quarter of the year (i.e. to March 2026), which are quite outdated. I guess it’s better than nothing.

For that quarter, tenant sales were up by 7.9% and footfall was up 2.4%. Vacancies were just 1.4%. This is what a successful retail portfolio looks like.

Spain led the way with sales growth of 8.6% for the quarter, an acceleration from 5.9% in FY25. Next up was Portugal at 7.0%, admittedly a slowdown vs. 8.2% in FY25. Even France showed strong growth of 6.5%, a significant jump from just 2.3% in FY25.

The performance in France isn’t because of the macroeconomic environment in that country. In fact, it’s despite the macro story. Lighthouse got some important leases across the line, achieving solid growth in income despite the vacancy rate sitting at 5.7% (by far the highest in the portfolio).

Lighthouse has reaffirmed the FY26 distribution guidance of 2.95 EUR cents per share, which implies anticipated growth of 6.9% vs. FY25.

Ghost Bite: I’m sure Des de Beer can’t wait to buy more shares once the interim results are released!

Prosus has grown free cash flow significantly (JSE: PRX)

And at Naspers (JSE: NPN), Takealot achieved its maiden profit

Prosus is the name that the group seems to be focusing on, so I’ll spend most of my energy there as well.

These results must be read against the backdrop of the Tencent share price having shed a third of its value year-to-date in USD terms, dragging Prosus (and Naspers) down with it.

To break this strong correlation, Prosus needs to convince the market that there is material value in the rest of the group.

Group revenue jumped by 57%, but acquisitions played a major role here. Strip them out and you’ll find 12% growth in revenue in local currency. That’s not exactly eye-watering growth, sadly.

Thankfully, the benefit of having moved through the inflection point for profitability is being seen at adjusted EBITDA level. This metric was up 44% in local currency (excluding acquisitions). This is the hockey stick that investors often talk about in platform businesses.

Another critical metric is free cash flow, coming in at $1.5 billion including the Tencent dividend. If you take out that dividend, the rest of the group generated free cash flow of $275 million vs. just $18 million in FY25. That’s an encouraging sign for investors in the group (like me).

The challenge Prosus faces is that the Latam ecosystem is dealing with immense competition, so they need to up the marketing spend to maintain their market position. This doesn’t do great things for short-term profitability, so look out for that in the next period.

In Europe, they took on the brave task of trying to turn Just Eat Takeaway.com (JET) into a growth asset in a region that is practically allergic to innovation. After shrinking for four years before the Prosus acquisition, JET is expected to return to revenue growth by the end of the year. Europe is also where you’ll find the OLX classifieds business, a solid contributor in terms of adjusted EBITDA margins (up 800 basis points to 48%).

In China, Tencent is dealing with the difficulties plaguing many tech assets at the moment: concerns around AI.

AI is core to the entire group these days, with Prosus working hard to convince the market that this is going to create value across the ecosystems. Time will tell.

Looking at Naspers, which is basically Prosus plus some rats and mice, Takealot grew revenue by 18% in local currency. Takealot achieved their first-ever annual profit, showing you just how long it takes to scale to profitability. With Amazon starting to scale in South Africa, I am not convinced that annual profits are guaranteed at Takealot.

Ghost Bite: I remain long here, as Prosus plugs an important gap in my portfolio around ex-US tech. But they certainly aren’t immune to the intoxicating mix of AI threats and opportunities that are a feature of the global tech sector.

SA Corporate Real Estate is generating real growth for investors (JSE: SAC)

Part of the portfolio is buy-to-let at scale – and it’s working

SA Corporate Real Estate has delivered a pre-close update for the six months ending June 2026. They use April 2026 metrics where appropriate, as the period obviously hasn’t ended yet.

Overall, distributable income per share is expected to increase by between 6% and 7% for the interim period. For the full year, they expect growth of between 5% and 7%.

In the retail portfolio, vacancies have ticked up from 2.3% to 2.9%. Reversions are expected to be positive 1.5%, up from 1.1% in December 2025. Rolling 12-month trading density is a concern, down from 6.2% in December 2025 to 4.8% in April 2026. The vacancy rate needs to be managed carefully as well.

On the industrial side, they have no vacancies at all. This isn’t unheard of in the industrial space, particularly when a portfolio is focused on large buildings and tenants. The challenge is that this creates a lumpy profile, so vacancies can hit hard if they do come through. For now though, the fund enjoys a fully-let portfolio.

In residential, the vacancy rate is down from 3.6% to an anticipated 3.1% by June. They expect to achieve rental increases of 4.3% vs. 4% in December 2025. This is the opposite to the industrial portfolio in terms of lumpiness, as a residential portfolio is split across many tenants.

In Zambia, improved performance at the Arcades Mall means that the fund expects 7% growth in the distributable income from that country (measured in USD).

On the balance sheet, the loan-to-value (LTV) has come down from 42.1% in December 2025 to 41.8% in April 2026. There are no further debt expiries this year. 68.3% of the debt is hedged at a tenor of 2.9 years.

Asset disposals are focused on the residential portfolio, with R709 million in transfers year-to-date. Another R743 million will transfer by the end of July, with a further R182 million in conditional disposals this year. They are selling the properties at a 32.7% premium to book and a 63.3% premium to acquisition price!

They are also looking to development opportunities, so don’t make the mistake of thinking this is one-way traffic in terms of disposals.

Ghost Bite: SA Corporate Real Estate s up 15% over 12 months. The total return including dividends is 24%. Do the maths and compare this to that buy-to-let investment that you felt was such a good idea. I’ll stick to buying REITs, thanks!

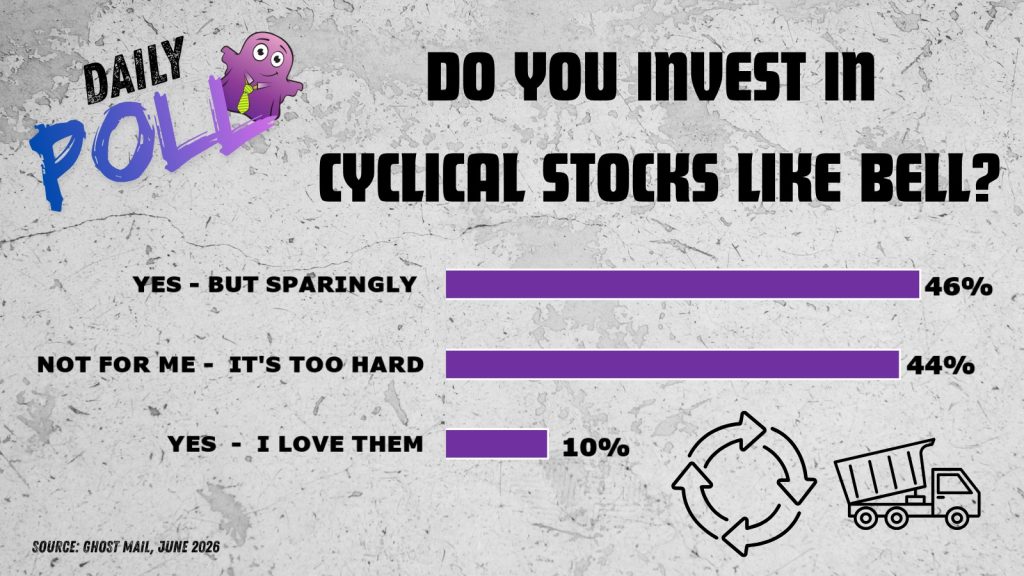

Results of previous poll:

Nibbles:

- Director dealings:

- Here’s an interesting one: the founder of Optasia (JSE: OPA), Bassim Haidar, got back on the bid for the shares. With the share price under immense pressure, he bought shares worth R23.7 million at a VWAP of R14.24 per share. You may recall that he previously sold R1.5 billion in shares at R20 per share! The CEO of the company joined him on the bid, buying shares worth R7.3 million. Will it be enough to stop the falling knife? Optasia is down 31% year-to-date.

- The CEO of AVI (JSE: AVI) was awarded shares in the company and sold the whole lot for R15.9 million.

- Acting through Titan Fincap Solutions, Dr Christo Wiese bought another R4.3 million worth of Brait Exchangeable Bonds (JSE: BIHLEB). This is relevant to holders of Brait ordinary shares (JSE: BAT).

- Most of the director dealing at Ninety One (JSE: NY1 | JSE: N91) happens in the form of employee trusts. In an unusual example, a director and his associate bought shares worth roughly R2.1 million.

- An independent non-executive director of Nedbank (JSE: NED) sold shares worth R38k.

- MAS (JSE: MSP) announced that PKMI Limited is looking to increase its controlling stake in the company. PKMI has launched a bid to shareholders to acquire up to 30 million MAS shares. If successful, this would increase the stake from 61.3% to 65.7%.

- Heriot REIT (JSE: HET) got the green light from shareholders for the issuance of shares to related parties. This allows them to move ahead with the Heriot family injecting more assets into the REIT.

- In case you understand what it means when a mineralised interval consists primarily of blebby to disseminated bornite and chalcopyrite in norite, then be aware that Orion Minerals (JSE: ORN) has released more drilling results. The non-geologists among us just skip through to the CEO commentary, where Tony Lennox seems very happy with the drilling results from the Okiep Copper Project.

- As the chairman of Raubex (JSE: RBX) is the ex-CEO of the group and thus not deemed to be independent, the company needs a Lead Independent Director. Setshego Bogatsu is stepping down from that role (having been in it since 2022), with Nosisa Fubu named as her replacement.

- I’m not sure if we can read much into this at Numeral (JSE: XII), but the company has appointed a non-executive director who has extensive experience in industrial assets in South Africa. Perhaps that’s a clue as to their future plans?

- Trustco (JSE: TTO) has renewed the cautionary announcement related to its potential delisting. This has been going on for a while now.