There may be 26 letters in the alphabet, but one has been getting more attention than the others recently: the letter X.

Elon Musk’s mysterious rebrand of The App Formerly Known As Twitter has garnered a mixed bag of opinions, from those who are lauding the billionaire’s plan to transition the digital soapbox into a broader-use app, to others calling the move brand suicide.

Of course, this isn’t the first time that we’ve seen this kind of rebrand in the tech space. Musk fans may argue that the media’s adoption of “Meta” instead of “Facebook” indicates the possibility of the general public eventually accepting a new name for Twitter.

That’s all well and good, but keep in mind that the media’s adoption of a new name is not the same as acceptance by the majority of the public. Journalists have a professional obligation to report the latest official names of companies and individuals. This doesn’t necessarily guarantee that the public fully embraces Meta or that the transition has been seamless.

The key difference here is that Musk hasn’t just rebranded the company, he’s rebranded the product.

Habits are hard to break

People are generally resistant to change, especially when it comes to established and well-known brands.

Tech companies face particular user resistance when trying to impose a new name or rebranding on their platforms. Users may read such efforts as corporate marketing strategies rather than genuine attempts to improve the platform. This scepticism can lead to pushback, and people may intentionally stick to the original name as a form of resistance to corporate influence.

For this reason, many individuals may still refer to Zuckerberg’s company as “Facebook” out of either habit, familiarity or sheer spite.

The comparison to Google’s rebranding to Alphabet in 2015 is another crucial example to consider. Despite the parent company of Google becoming Alphabet, most journalists and the general public continued using “Google” to refer to the tech giant. The failure of Alphabet to replace “Google” in everyday usage shows that even large, well-publicised rebranding efforts may not automatically succeed in altering public perception, even if Alphabet only tried to do it at group level rather than product level.

Again, Musk has gone all the way here by renaming the product.

A rose by any other name still has thorns

We’ve covered Meta twice on Magic Markets Premium before this week: once in February ‘22 (after the official name change but before the new ticker) and again in November ‘22 (after Zuckerberg made it clear that he was doubling down on his Reality Labs dream).

Around the time of that February report, the stock dropped 26% in a single day. That put the share price at approximately half the levels it traded at in the peak of September 2021, yet the pain wasn’t over. As the push into the Metaverse and broader Reality Labs dream continued, the share price continued to plummet. It eventually bottomed at $88, an extraordinary drop from around $380.

The problem was a combination of a sharp drop in free cash flow and a souring of public perception, although the latter is hardly anything new for Zuck and crew.

The name change to Meta had come shortly after a pivotal event: the testimony of Frances Haugen, a Facebook whistleblower, before the U.S. Senate. During her testimony, Haugen provided substantial evidence that the social media giant’s algorithms were designed to amplify divisive content, misinformation and harmful content to keep users engaged and spending more time on the platform.

Amid this mounting pressure and negative public perception, Meta’s rebranding served as a strategic move to reposition the company’s image and emphasise its focus on a “metaverse” vision. By adopting the name “Meta,” the company aimed to redirect attention away from the controversies associated with Facebook and present itself as a forward-looking, innovative tech company.

Of course, investors weren’t fooled by the idea that a simple name change would erase not only the social quandary that Facebook was in, but the group’s hellbent mission to invest in tech that nobody asked for.

With substantial shareholder pressure on the company (and of course, the helpful extreme bearishness of Jim Cramer as the world’s finest contra-indicator), Meta cut back on costs and got the core business right in the transition to Reels. The result was a massive run in the price this year, making Ghost feel good about buying the dip of all dips and saving his position in this stock.

The share price has been incredibly volatile, which is why we’ve covered the company yet again in Magic Markets Premium this week:

So, does X mark the spot?

Name changes are never spontaneous. In fact, they often follow on the heels of disaster.

When an organisation becomes associated with a catastrophic event or a major ethical breach, it can be challenging to recover public trust and salvage the brand’s reputation. In such cases, rebranding offers a way for the company to distance itself from the past, signal a fresh start, and rebuild its identity from the ground up.

Elon Musk has made no secret of the fact that he has wanted to burn Twitter to the ground from the moment he bought it. Which begs the question: is the X rebrand his way of wiping Twitter’s history off the table – or a distraction from the amount of money that the business has lost since Musk’s takeover?

Smart investors aren’t fooled by something as simple as a name change. With nearly 90 research reports on global stocks available in the library, a subscription to Magic Markets Premium for just R99/month gives you access to an exceptional knowledge base that has been built since we launched in 2021 – including our latest recap on Meta, which goes live this week.

The Ghost Wrap podcast is proudly brought to you by Mazars, a leading international audit, tax and advisory firm with a national footprint within South Africa. Visit the Mazars website for more information.

Challenges in the gold sector, with AngloGold, Sibanye-Stillwater and even Gold Fields releasing tough announcements. At least Pan African Resources had a good news story this week.

The telecoms sector and difficulties in that space, with MTN and Telkom facing different but equally serious issues.

The critical importance of the Bundu Power acquisition to Ellies, without which the business really is in doubt.

Curro’s surprisingly good earnings update, despite facing such obvious pressures in the economy.

Astoria’s NAV is flat in ZAR for the interim period (JSE: ARA)

The company reports in dollars but is exposed to rand assets, so the reported NAV is down

The rand depreciated significantly against the dollar in the six months to June. This is why the Astoria net asset value (NAV) per share is up by 0.1% in rand but down 9.6% in dollars.

Although the net asset value is flat in rand, the movements within the portfolio are notable in some cases. For example, the investment in Outdoor Investment Holdings (which owns Safari & Outdoor alongside other businesses) increased in value by 10% since December 2022.

In Trans Hex, the value was impacted by a significant dividend payment, of which Astoria received R7.5 million. Realised diamond prices were around 20% lower in this period. In the marine diamonds operations, the impact of lower diamond prices was mitigated to an extent by lower fuel prices for the ships.

The value of Goldrush (held via listed entity RECM & Calibre JSE: RACP) fell by 25% as it is valued with reference to the listed share price of RACP. Load shedding had a negative impact on this business, as was separately disclosed in RACP announcements.

The valuations of both ISA Carstens and Vehicle Care Group have moved slightly higher. Both are valued at nearly R55 million, although that is the only thing they have in common. ISA Carstens is a tertiary education business and Vehicle Care Group provides funding and other services to the used vehicle trade and related consumers.

Finally, the value of Leatt took a 40% knock in the past six months because of pressure on its share price in the OTC market in the US where it trades. Many global retailers were heavily overstocked at the end of 2022 and this has impacted sales by suppliers like Leatt. This investment now represents 3.8% of the group NAV.

Astoria has R12.9 million in cash on the balance sheet, similar to the R13.1 million held at the end of December 2022.

The company is currently trading under a cautionary announcement due to ongoing negotiations about a potential acquisition.

Curro flags strong growth in recurring HEPS (JSE: COH)

These look like strong numbers during a challenging time in South Africa

Curro finds itself staring down the barrel of a number of ugly South African realities, ranging from middle-class emigration and general lack of spending power through to utility and energy costs. Perhaps in the eye of the storm for now, the results for the six months to June actually look really good.

You need to work with recurring headline earnings per share (HEPS), as the comparable period included the receipt of a long-overdue education subsidy by Meridian. That metric is expected to be between 26.5% and 45.5% higher, coming in at between 32.3 cents and 37.1 cents.

The share price has had an extremely volatile 12 months:

Give that dog a Rathbone(s) (JSE: INL)

Investec gets the all-important regulatory approval for the Rathbones merger

The deal between Investec Wealth & Investment in the UK and Rathbones was announced back in April 2023. It’s an exciting merger that will see Investec achieve scale in the UK market and a 41.25% economic interest in the merged entity, with 29.9% voting rights.

The key regulatory approvals have now been obtained, so in the absence of a material adverse change the deal will go ahead on 21 September 2023.

I like this deal for Investec.

Gold Fields has also gone backwards (JSE: GFI)

Thankfully, to a far lesser extent than rival AngloGold

For the six months to June, Gold Fields has reported a drop in HEPS of between 9% and 16%. This is due to lower gold volumes sold and pressure on operating costs. Mining inflation is a theme that is playing out across the industry, leaving miners reliant on an increase in commodity prices.

All-in costs for the six months came in at $1,398/oz which is 3% higher year-on-year. The trend is worrying, as that metric was $1,454/oz in the second quarter. That’s not a great setup heading into the second half of the financial year.

Detailed results for the interim period will be released on 17 August.

The JSE reports flat operating results (JSE: JSE)

For the newbies: yes, the JSE is listed on the JSE!

This tends to blow a few minds every time I write about it. The JSE is listed on the JSE, because the JSE Limited is a public company and is effectively using its own product by being listed on the exchange. I hope that makes sense now.

Unless you really haven’t been paying attention, you’ll know that the number of listings has decreased over the years. This problem isn’t unique to South Africa. The good news is that the JSE has other markets as well, like the debt market that is used extensively by South African corporates and institutions. There are also several initiatives underway to move away from dependency on trading revenue, with non-trading revenue (like Information Services and JSE Investor Services) now representing 36% of growth.

Of course, the fact that a significant amount of trading has moved to competitor A2X is a contributor to this.

In the six months to June 2023, revenue increased by just 5% and operating expenses increased by 8%, with staff expenses up by a substantial 15% as the largest expense on the income statement. This means that Earnings Before Interest and Tax (EBIT) only grew by 1%. Pedestrian to say the least.

Below the EBIT line, it’s mainly about the balance sheet as tax rates tend to be consistent. The JSE earns net finance income rather than incurs a net finance cost, so net finance income jumped by 53% in an environment of higher interest rates. This is why net profit after tax grew by 10% despite the anemic operating profit performance. HEPS increased by 12%.

Investors who are focused on the dividend will be pleased to note that capital expenditure fell by 35%, although it isn’t great at all to see cash generated from operations dropping by 9%.

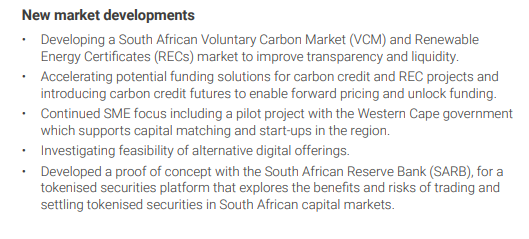

The new market developments section makes for interesting reading, especially the last bullet about what I presume means a crypto project:

MiX Telematics reports a much-improved quarter (JSE: MIX)

Key metrics have moved in the right direction

MiX Telematics operates a number of fleet management businesses, with Matrix as the brand that most consumers will know about. The company achieved 40,500 net subscriber additions in this quarter, bringing the total subscribers to 1,042,000.

Total revenue increased by 15% year-on-year on a constant currency basis. The company reports in dollars because it is listed in New York and makes most of its money in rand, so unfortunately the dollar growth is very modest at 3.8%.

Gross profit margin improved by 160 basis points to 63.6% and operating income margin jumped by 520 basis points to 12.1%, certainly a far better performance than in the comparable period and helped along by restructuring activities completed in March.

These businesses aren’t great at generating free cash flow, as most of the cash gets reinvested in devices. This quarter was no exception, with $5 million in cash from operating activities and capital expenditure of, wait for it, $5 million!

Despite this, there’s a quarterly dividend of 4.5 ZAR cents. On a share price of R4.84, that’s an annualised yield of 3.7%.

OUTsurance: solid numbers and a potential exit of OUTvest (JSE: OUT)

And an entry into Ireland, of all places!

OUTsurance Group has released a trading update for the year ended June 2023. You still have to be very careful when interpreting these numbers, as the base period included the group’s life as Rand Merchant Investment Holdings. In that period, it disposed of Hastings Group, settled preference share debt and unbundled the interests in Discovery and Momentum Metropolitan.

In other words, reading the group numbers in isolation will make no sense at all. I’m ignoring them.

To help with this issue, the group has released a voluntary trading update dealing specifically with OUTsurance Holdings, the 90%-held subsidiary that owns the OUTsurance business in South Africa and Youi in Australia. The company will also be entering the market in Ireland in the second half of 2024.

The growth is very much in Australia, with normalised earnings of R413 million, an increase of 220% to 250%. In South Africa, OUTsurance’s short-term business limped along with earnings growth of 0% to 10% and OUTsurance Life managed between 5% and 15%. As Australia is only 17.8% of the earnings base, the group level growth came in at between 35% and 45%.

Interestingly, the group is walking away from the OUTvest initiative as it remains sub-scale. They will try and sell the thing if they can find a buyer. Client investments will not be impacted by this. If nothing else, it just shows that plugging one set of financial services into an existing ecosystem isn’t a guarantee of success.

Workforce Holdings reports a collapse in profits (JSE: WKF)

The first six months of the year are a disaster

In today’s example of “things you don’t want to read as an investor”, I give you the drop in HEPS at Workforce Holdings of between 78.36% and 98.36%. That’s awful.

It’s thankfully only for the six months to June, with the company noting that corrective measures have been put in place to try and save face in the second half of the year. The reasons given for the performance are worrying as they aren’t exactly disappearing overnight, ranging from high interest rates to load shedding and low demand for services.

Although revenue was slightly higher, the problem is that the cost base was way too high for this level of activity. This explains the “corrective measures” – surely just a nice way of saying that people got retrenched.

4Sight Holdings sees HEPS approximately triple (JSE: 4SI)

The announcement is light on details

For the six months to June 2023, 4Sight Holdings expects HEPS to jump from 1.288 cents to between 3.704 and 3.952 cents. That’s potentially a tripling of its HEPS!

There are no further details in the announcement, so we will have to be patient for results. The share price has very little liquidity and is trading at 25 cents.

Little Bites:

Director dealings:

There was massive trade in Novus (JSE: NVS) shares on the 31st of July. A2 Investment Partners (linked to Andre van der Veen and Adrian Zetler) bought R32.26 million worth of shares and Sphere Investments (linked to director Marang Mashologu) executed exactly the same trade, so this was obviously a pre-arranged block trade through the market with a total value in excess of R64 million.

The ex-CEO of Emira Property Fund (JSE: EMI) is buying more shares, this time R248.5k worth of shares in a trust.

In an awkward one, a director of Remgro (JSE: REM) sold shares worth R85k without clearance. The portfolio manager apparently executed this in error. It doesn’t say whether the error was the trade (unlikely) or lack of clearance for it!

Although the impact on AYO Technology (JSE: AYO) is limited as the company now has banking arrangements in place, it’s interesting to note that the Competition Appeal Court ruled in favour of the banks that refused to provide services to this group. This is specifically on the basis that AYO couldn’t prove that the behaviour was anticompetitive in nature. I’m not sure how refusing to provide a service could ever be anticompetitive. Surely that is directly encouraging competition?!?

I gave up on gold miners a while ago. Having dabbled with them during the pandemic, I eventually grew tired of watching crazy things happen. The gold price simply doesn’t react the way you would expect, which means inflationary conditions are actually negative for gold miners as the commodity price tends to be too light relative to the cost pressures.

AngloGold just brought this message home once more for me, with a trading update for the six months to June that notes an expected drop in HEPS of between 48% and 58%. Compared to the base period of 71 US cents in earnings, the company notes that inflationary pressures had an impact on earnings of 26 US cents.

There were other issues, like higher non-cash environmental provisions following the implementation of new legislation in Brazil.

With an expectation of only marginally higher gold production for the full year vs. last year, the group is reliant on the gold price doing well. Good luck with that.

Aspen and the Latino lovers (JSE: APN)

Interestingly, the group can’t measure the profits it is buying

FinTwit became a rather juvenile place on Tuesday, with news of Aspen buying the rights to Viagra (among other products) in Latin America. Leaving the endless potential jokes aside, this is obviously a major product and there are many others in the Viatris portfolio as well.

The really interesting thing is that Aspen reckons the portfolio is worth $280 million. The price being paid is a combination of $150 million in cash and a supply agreement for seven years with Viatris, presumably on somewhat favourable terms to Viatris although the announcement doesn’t make that clear.

In any event, Aspen seem to have taken an educated guess at the fair value. You see, the company cannot actually identify the profits from this portfolio because of how Viatris is structured. All we know is that the annual sales number is $92 million. Aspen thinks that the gross margin will be higher than the gross margin in its Commercial Pharmaceutical segment of 60%.

A valuation is never an exact science but this really is just a guessing game. Nothing ventured, nothing gained I guess.

More debt transactions underway at British American Tobacco (JSE: BTI)

Here’s one for the comic book fans: BATCAP Notes

Hot on the heels of a $2.9 billion tender offer to reduce some of the existing debt instruments in issue, British American Tobacco has priced $4 billion worth of debt instruments with maturities ranging from 2030 all the way out to 2053.

The yield curve looks like this, across two different issuers within the corporate group:

2029: 5.931%

2030: 6.343%

2033: 6.421%

2043: 7.079%

2053: 7.081%

These are dollar-based instruments, some of which are entertainingly referred to by the company as BATCAP Notes.

The major thing to learn from this is that longer-dated money usually carries a higher cost.

The Crookes Brothers circular is late but imminent (JSE: CKS)

This relates to the deciduous fruit farming disposal to Witzenberg Properties

Crookes Brothers first announced this deal back in May, with an agreement to sell the deciduous fruit farming business and related properties to Witzenberg Properties for R200 million.

This requires a Category 1 circular to be issued to shareholders, which is a big job even for companies that are used to the requirements. Although no reason for the delay is given, Crookes Brothers couldn’t meet the rule to publish the circular within 60 days and went to the JSE for a dispensation.

The circular will be sent out before 10th August, with the blessing of the JSE.

Ellies heads into the Bundu (JSE: ELI)

The future of Ellies rests on this transaction

Ellies has now released its financial results for the year ended April. They don’t make for happy reading.

Revenue fell by 7.7% and the EBITDA loss has worsened to R46.9 million. This comes after a loss of R37.1 million in the prior year, although it does include restructuring costs of R18 million this year that should generate R30 million in annual savings. The attributable loss after tax is even worse, coming in at R85.4 million, nearly double the prior year’s loss.

The interest expense was R21.3 million. The company absolutely cannot afford this debt. With a term loan due on 30 April 2024, the current negotiations with the bankers are critical.

The headline loss per share is 10.78 cents. To put that disaster into perspective, the share price is 7 cents per share. The net tangible asset value per share is 6 cents.

It’s just a mess almost everywhere you look. The satellite installation business makes Telkom’s voice business look like the poster child of the 4th industrial revolution. The electrical products business should’ve cleaned up during periods of extreme load shedding, yet Ellies simply didn’t have the working capital to really capitalise on this.

To fund the Bundu Power acquisition and the last-ditch attempt to save this thing by moving into renewable energy installations, Ellies will undertake a R120 million capital raise at 7 cents per share.

The circular is being updated with this latest financial information and will be distributed to shareholders by 31 August.

MTN Ghana lost mobile subscribers, but grew revenue (JSE: MTN)

EBITDA margin also contracted slightly

After the release of a sobering trading update by mothership MTN and key African subsidiary MTN Nigeria, MTN Ghana has now joined the fray. This is also an important part of the group, plagued by the same forex issues that have caused grey hairs for South African investors as cash ends up getting trapped in underlying African subsidiaries.

At least the numbers in Ghana are (mostly) heading in the right direction. Mobile subscriber numbers fell by 1.6% due to SIM re-registration issues in the country. We’ve seen this play out in other markets. Service revenue grew by 32.3% and EBITDA grew by 29.4%, so EBITDA margin contracted by 130 basis points to a still-delicious 56.1%.

Core capital expenditure increased by 54.2%, so the rate of investment in the country is exceeding the rate of earnings growth. If you can’t get the cash out, you may as well reinvest it right?

Pan African closes the required funding for Mintails (JSE: PAN)

The R1.3 billion senior debt facility is now in place

Pan African Resources has been busy raising a R1.3 billion senior debt package to be used to fund the Mintails project. This has been underwritten by RMB, with Nedbank acting as co-financier. On projects of this size, there’s often more than one bank as they look to spread the risk. It also helps to mark each other’s homework on the credit assessment.

This takes the total funding for Mintails to R2.5 billion. The other constituents of that number are a Domestic Medium Term Note programme that raised R800 million in December 2022 and a derivative funding structure of R400 million that was finalised with RMB in March 2023.

Full scale construction of the tailings retreatment plant will now begin, with expected all-in sustaining costs similar to the Elikhulu operation at Evander. The project is expected to be commissioned in the latter half of the 2024 calendar year.

Royal Bafokeng results: for the final time (JSE: RBP)

Trading in the shares will be suspended on 2 August ahead of the Impala Platinum takeout

With the Impala Platinum (JSE: IMP) squeeze-out underway to take Royal Bafokeng Platinum private, this is the last time that the company will separately release results as a listed company. It’s not exactly going out on a happy note, either.

Impala Platinum is now the lucky owner of a platinum group that made a headline loss of R330 million in the six months to June 2023, a wildly negative swing from headline earnings of R2.2 billion in the prior period.

Production fell slightly and cash operating cost per ounce jumped by 19.5%, with profits destroyed in the middle because the average PGM basket price fell by 23.6%. Operating costs showed a particularly concerning trend at the Styldrift mine, which posted a huge loss of R655 million vs. profit of R760 million last year. BRPM also suffered but was at least profitable, with earnings of R440 million vs. R2.36 billion last year.

Total capital expenditure decreased by 10.9%, mainly in expansion capital. The group discloses stay-in-business capital, which increased by 17.2%. In mining, even when times are difficult, the need to keep investing just doesn’t go away.

I hope that this will work out for Impala Platinum. Northam Platinum was happy to cut its losses on this one.

Sibanye-Stillwater investors get shafted again (JSE: SSW)

There’s just no respite

A 6.1% drop in the share price has undone a decent chunk of the recent momentum in the Sibanye-Stillwater share price. The year-to-date picture remains very painful.

The local gold operations have had a particularly torrid time, particularly during the labour unrest that caused awful financial results. It’s quite incredible seeing the run of luck here. If it’s not the platinum business in the US flooding (despite the name Stillwater), it’s the local gold operations experiencing structural damage to the Kloof 4 shaft.

The practical impact is that operations at Kloof 4 have been suspended. This accounts for 14% of Sibanye’s annual gold production from local operations, excluding DRDGOLD. Thankfully, no employees were injured during the safety trial that led to the incident. Goodness knows it could’ve been a lot worse.

A jump in earnings at South Ocean Holdings (JSE: SOH)

This company has nothing to do with fish!

South Ocean Holdings is one of those locally-listed companies that you’ve probably never heard of. The company manufactures electrical cables, so the fishy-sounding name (and I mean that literally) probably doesn’t help.

It’s not as small as you think, with a market cap of around R200 million. The bid-offer spread is wide, so you need to be patient with any positions here.

For the six months to June, HEPS increased by 51.3% to 23.9 cents. With a share price of R1.15, this puts it on a very modest annualised Price/Earnings multiple of 2.4x.

Detailed results will be out on 3 August.

Textainer: another reminder of how cyclical shipping is (JSE: TXT)

If you’re looking for steady earnings growth, stay far away from shipping

Whether you look at the owners of the ships themselves (like Grindrod Shipping JSE: GSH) or a container business like Textainer, shipping is an incredibly cyclical industry where the shipping rates fluctuate and profits are even more volatile.

In the second quarter of 2023, Textainer’s income from operations was $97.7 million vs. $122.8 million a year ago. On a HEPS basis, it’s down from $1.63 to $1.20. The cadence (this quarter vs. the immediately preceding quarter i.e. Q1’23) is also negative, as earnings in Q1 were $1.22 per share.

The company adjusts the size of its container fleet based on demand. Utilisation has dropped from 99.6% a year ago to 98.8% despite the total fleet size being reduced by 3.9%. They measure the fleet size based on TEUs: twenty-foot equivalent units.

Despite the earnings trajectory, the share price is actually up 27% in the last year. The rand depreciation is certainly part of that, with share buybacks also playing a role.

Little Bites:

Director dealings:

The CEO of Spear REIT (JSE: SEA) has bought another R14.4k worth of shares in the company for his family.

Adcorp’s (JSE: ADR) special dividend of 91.3 cents per share is expected to be paid on 21 August.

Equity ETFs tend to dominate the narrative among investors, particularly retail investors. Fixed income or bond ETFs are often ignored, which is a pity now that yields have picked up to current levels.

Fixed income instruments can be difficult to understand. The trick is in the name, as the capital value fluctuates based on a fixed underlying coupon and the yield that the market demands.

In shining a light on this asset class with Siyabulela Nomoyi from Satrix, we discussed:

The reasons why a bond market exists, touching on how vibrant the local market has been for bond listings vs. equity listings

The capital risk that comes with not holding a bond to maturity

An indication of annual returns achieved in recent years by Satrix bond ETFs

How these can be used in balanced portfolios

Retail Savings Bonds and how they differ from Satrix bond ETFs

The different Satrix bond ETFs and the underlying constituents

The use of Satrix bond ETFs in a tax-free savings account

Disclosure Satrix Investments (Pty) Ltd is an approved FSP in term of the Financial Advisory and Intermediary Services Act (FAIS). The information does not constitute advice as contemplated in FAIS. Use or rely on this information at your own risk. Consult your Financial Adviser before making an investment decision. While every effort has been made to ensure the reasonableness and accuracy of the information contained in this podcast (“the information”), the FSP’s, its shareholders, subsidiaries, clients, agents, officers and employees do not make any representations or warranties regarding the accuracy or suitability of the information and shall not be held responsible and disclaims all liability for any loss, liability and damage whatsoever suffered as a result of or which may be attributable, directly or indirectly, to any use of or reliance upon the information.

For more from the Satrix – Ghost Mail partnership, visit this link to find various podcasts and articles.

British American Tobacco to reduce debt by $2.9bn (JSE: BTI)

This is a debt tender offer with different acceptance priorities

A group as large and complicated as British American Tobacco runs an equally large and complicated balance sheet, which includes numerous debt instruments that have different funding costs and tenures. Yes, British American Tobacco effectively has its own yield curve!

When they aren’t paying ESG consultants a fortune to make tobacco look like rainbows and unicorns, the group is highly focused on capital allocation decisions that help boost earnings growth off modest revenue growth. This debt tender offer is a perfect example of active balance sheet management.

British American Tobacco has allocated $2.9 billion to this initiative, in which holders of the various debt securities can “tender” their securities i.e. ask to be repaid. There are different pools of securities and the company has indicated the priority levels for each pool. Obviously, the priority is to repay the most expensive debt. The holders of those instruments are also the least inclined to sell them because the yields are good, so there’s a natural tension there.

Still, there will no doubt be sellers in every debt pool. The question is whether the full $2.9 billion will be taken up by debt holders and in which pools.

EOH seems to be stable (JSE: EOH)

There’s still a loss after tax for this period, hopefully for the last time

For the six months to January 2023, EOH grew continuing revenue by 8% and achieved 45% growth in international revenue, which tells you that the local story is slow. This is particularly the case in the public sector, where challenges continue to be faced.

Gross profit margin was stable at 29% and adjusted EBITDA more than doubled, with continuing operating profit of R110 million. That’s more than they managed in the last full financial year, let alone the interim period!

Unfortunately, the equity capital raise of R600 million was only completed in February 2023, so this period still reflects the full impact of the debt on the balance sheet. This is why there is still a loss after tax, albeit reduced by 82% vs. the comparable period. The company used the announcement to remind the market that the capital raise was significantly oversubscribed, although this was certainly helped along by the huge discount at which the capital was raised.

Aside from the IFRS2 charge on the discounted equity issue to the Lebashe Investment Group, there was also a R65 million impairment to the tech leasing book. Most of the legacy debts are from customers in the casino industry and they were badly hit by lockdowns. Although EOH is trying to recover the debt, they have provided for it in full.

Importantly, as at the end of July, there’s no overdraft and a positive cash balance of R255 million.

A strong half at Gemfields (JSE: GML)

The rubies and emeralds continue to shine

Gemfields is one of the most interesting companies on the local market. Unlike anything else we can invest in here, the group mines emeralds in Zambia and rubies in Mozambique. Unrest in Mozambique is one of the reasons why the company tends to trade on modest multiples.

For the six months ended June 2023, the company highlighted the third highest interim period in company history in terms of auction revenues. This includes the highest ever revenue from a Kagem emerald auction.

The group has net cash of $62 million and auction receivables of $64 million. The balance sheet is very strong despite paying a $35 million dividend to shareholders in May 2023.

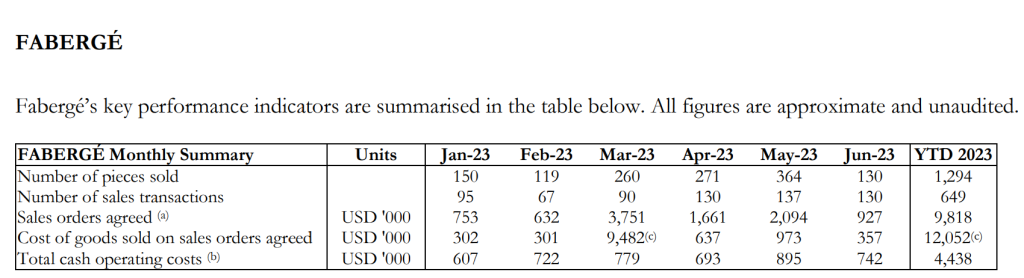

The problem child in the group is Faberge, which continues to have pretty questionable economics. I love the monthly disclosure, as it shows the big clearance of goods in March 2023 at a large loss. The provision on the inventory was recognised in previous years but that’s not the point. I highlight this because the harsh reality is that being in the “luxury” sector isn’t a guarantee of success. When there is strong demand for products, you don’t need to sell them at discounted prices.

Glencore invests further into Copper (JSE: GLN)

Does the deal team at Glencore ever rest?

The flurry of deals at Glencore is quite something. The group is always busy with something, ranging from large proposed mergers through to mine-level deals.

The latest announcement is a smaller transaction than some of the other opportunities the company has looked at, but is still substantial. The MARA project is a copper and gold project in Argentina that already has significant infrastructure, so Glencore describes it as one of the lowest capital-intensive copper projects in the world. The project has a life-of-mine of 27 years and has proven and probable mineral reserves of 5.4 million tonnes of copper and 7.4 million ounces of gold.

Glencore has been involved since the inception of the project in December 2020 when it was formed as a joint venture between Yamana Gold, Glencore and Newmont. Glencore subsequently acquired Newmont’s 18.75% stake in October 2022, taking its shareholding to 43.75%.

When Pan American acquired Yamana Gold Inc. it also acquired the company’s 56.25% stake in MARA. This is the subject of the latest deal, with Glencore acquiring that 56.25% for $475 million and a net smelter return royalty of 0.75%. Mining deal structures really are fascinating.

MARA is expected to be a top 25 global copper producer when operational and will be 100% owned by Glencore after this deal.

At this point, if you’re a young finance professional looking for M&A exposure, you would probably see more deal flow by joining Glencore than many of the local advisory houses!

Liberty Two Degrees releases results (JSE: L2D)

In case you’ve been under a rock, Liberty has made a bid to take the company private

We now know that the net asset value of Liberty Two Degrees is R7.59, up 0.8% and well above the R5.55 price that Liberty has put on the table. With retail reversions improving to -0.3% vs. -9.7% in full year 2022, Liberty seems to have swooped in just as things were improving. That makes sense for obvious reasons.

The interim distribution of 18.77 cents is 7.4% higher than the comparable period.

The loan-to-value is 24.58%, so Liberty is looking at acquiring a group with a solid balance sheet.

You may find it interesting to compare the trading density at Sandton City (R78,800/sqm) to Eastgate (R39,274/sqm). The fastest growing mall in the portfolio in terms of turnover was Melrose Arch, up 10.9% for the interim period. Sandton City was just behind it at 10.2%.

Office leasing remains a challenge, with occupancy of 82.1% vs. 97.1% in retail. The negative reversion in office was a monstrous -20.4%, which is at least an improvement on the truly shocking 2022 number of -25.5%. They are practically begging tenants to sign office leases.

MC Mining quarterly report (JSE: MCZ)

The focus is on Makhado, with the Uitkomst colliery continuing to be impacted by Eskom

In the quarter ended June 2023, MC Mining’s coal production at Uitkomst was 1% lower year-on-year, with load shedding and some geological conditions having a negative impact. Although production fell slightly, coal sales were way up on last year.

At the Makhado project, the updated life of mine plan and coal reserve estimate have improved the project’s economics. The tender processes to select the outsourced mining, plant and laboratory operators are expected to be completed in the next quarter. Where possible, the company is negotiating build, own, operate, transfer (BOOT) funding arrangements.

After the end of the quarter, the IDC extended the repayment date of the R160 million loan to 30 September 2023.

A change of CFO at Mr Price (JSE: MRP)

This sounds like a difficult exit

Mr Price hasn’t been performing well recently, so a change of management brings more uncertainty into the investment story. CFO Mark Stirton has stepped down from the CFO role as of 31 July 2023, which is basically “with immediate effect” without them saying as much. The change is on “mutually agreed terms” which also makes it sound like this wasn’t the standard process.

He will be sticking around until March 2024 to assist with a handover to new CFO, Praneel Nundkumar, who has been with the group for 7 years and is currently the Managing Director of Mr Price Money.

It’s been a very volatile year in the local retail industry, with Mr Price not escaping the sharp swings in sentiment:

MTN grows HEPS by between 0% and 10% (JSE: MTN)

A difficult industry is made much harder by African currency challenges

A trading statement has confirmed that in the six months to June, MTN grew HEPS by between 0% and 10%. This means a range of 506 cents to 557 cents for the interim period. The forex losses were huge in this period, impacted HEPS by 169 cents. Hyperinflation of 38 cents didn’t help either.

Within the forex losses, 128 cents is from Nigeria of which 95 cents was incurred in June when the naira was allowed to float. This caused a rapid depreciation in the Nigerian currency. The shortage of forex reserves in Nigeria (and Ghana for that matter) makes life difficult for MTN, with the company electing to receive scrip dividends rather than cash. This is good for attributable earnings and bad for cash upstreaming.

Group holding company leverage is towards the upper end of the guidance range of less than 1.5x. Net debt to EBITDA on a consolidated basis is in line with the December 2022 level. Consolidated numbers don’t really help though, as it matters where the cash actually sits in the group.

In a separate announcement, MTN Nigeria released numbers for the six months to June. Service revenue increased by 21.6% and EBITDA margin fell by 60 basis points to 53.0%. Because of forex losses, profit before tax fell 25.4% and earnings per share fell 29.3%. Capital expenditure fell by 14.4%.

Here’s a reminder that your life in South Africa can always be worse:

“As a result, the inflation rate in Nigeria rose to an 18-year high of 22.8% in June 2023, representing the sixth consecutive month-on-month increase in 2023, with an average of 22.2% in H1. To rein in inflation, the Central Bank of Nigeria (CBN) continued its monetary policy tightening, increasing the monetary policy rate by 2pp to 18.5% in H1, and a further 0.25pp increase in July.”

Orion Minerals quarterly report (JSE: ORN)

Cheekily, they start with the biggest news after the end of the quarter

Orion Minerals released an update on activities in the quarter ended June. The real news of course is the drawdown on the IDC and Triple Flag facilities, which only happened after the end of the quarter. This didn’t stop the company kicking off with a reminder of that news.

On a strict view of this quarter, the big news was actually the share placement with Clover Alloys. If all placement options are ultimately exercised, the total value of the equity funding package is A$73 million.

The focus is on the Prieska Copper-Zinc project, with the goal of accelerated development. An updated mineral resource estimate has been completed. A feasibility study is also well advanced at the Okiep Copper Project. The company is making solid progress at both hubs.

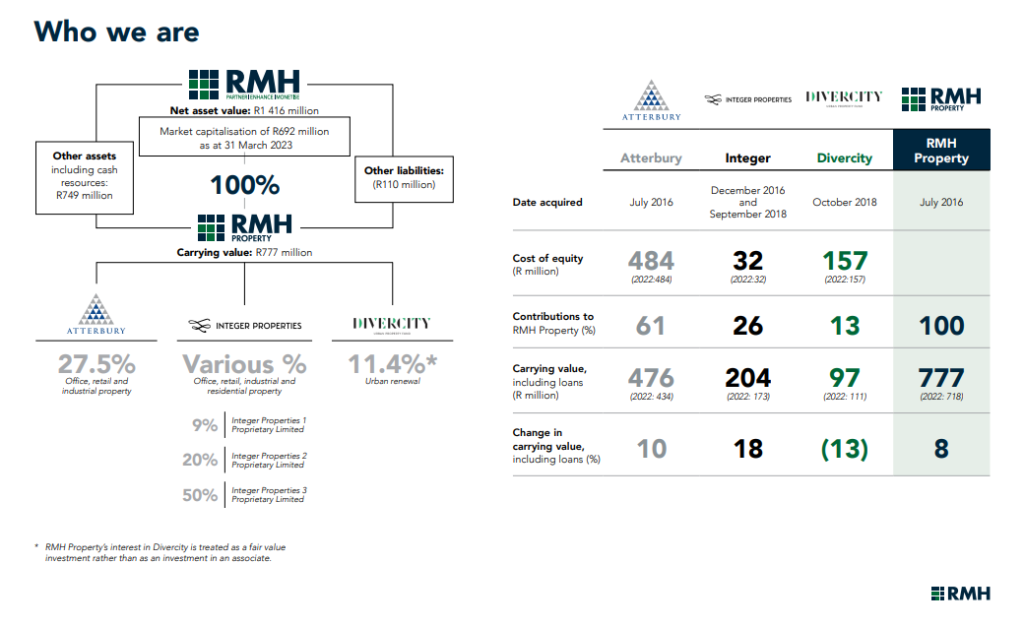

RMB Holdings releases results for the year ended March (JSE: RMH)

This will help you understand why the Atterbury dispute is so important

RMB Holdings had a net asset value per share of 100.3 cents at the end of March 2023. The current share price is 48 cents, which is why the market is focused on the company realising that value.

A very big chunk of the value sits in Atterbury, with whom RMB Holdings is currently in dispute. Here’s an excerpt from the annual report:

The current position is that RMB Holdings has demanded repayment of a R487 million loan from Atterbury. The company previously tried to issue shares to the bankers in repayment of this loan, which triggered RMB Holdings to step into the banker’s shoes and demand cash repayment instead.

Southern Palladium quarterly report (JSE: SDL)

This is a very early stage company that is focused on drilling

At Southern Palladium, the quarter ended June was all about drilling. The company is preparing for the pre-feasibility study in the first quarter of 2024.

Thanks to drilling efforts, the total mineral resource has been increased by 34% since drilling began.

The mining right application remains on track for submission in the third quarter, which is five months ahead of the original schedule.

The company has $11.55 million in cash, down from $12.93 million at the end of March.

More cash flows into Stefanutti Stocks (JSE: SSK)

The costs of the arbitration process have also been received

Back in May 2023, Stefanutti Stocks alerted shareholders to the receipt of a capital award of R90.85 million under the mechanical project termination arbitration.

To give you an idea of how expensive a legal process can be, the company has now also received R15 million for expert and legal fees incurred. This is obviously more good news for the company, especially with a market cap of just R270 million.

Telkom: revenue up, profits down (JSE: TKG)

Recent labour restructuring initiatives supposedly offset the impact of load shedding

Every time I write about Telkom, I remind you that the company finds itself on a treadmill. The legacy business is dying rapidly, with new revenue initiatives struggling to keep pace with the rate of decline in the old business.

In the quarter ended June, revenue was up 3.8% but group EBITDA fell by 4.2%. This is despite the group saying that labour restructuring initiatives offset the impact of load shedding.

Mobile revenue increased by 5.2%, Openserve grew new generation revenue by 10.6%, BCX was up by just 2.9% and Swiftnet limped along with growth of 1.2%.

Legacy voice services in Telkom Consumer fell by 24.2% and only account for 4.8% of group revenue. In stark contrast, mobile data traffic jumped by 25.1%. Once technology reaches an inflection point, the rate of change is remarkable.

In Openserve, fixed voice revenue fell by 29%. This led to the segment reporting an overall revenue decline of 2.7%. Expressions of interest for strategic equity stakes in Openserve have been received, though Telkom isn’t acting on any of them yet.

In BCX, the legacy Converged Communications business saw revenue drop by 12.8%. The IT business was 17.5% higher, giving the blended increase in revenue of 2.9%. EBITDA came under particular pressure in this business, down 38.2% with a margin of just 7.9% (down 520 basis points). Telkom is looking at options to introduce a strategic equity partner in this business, particularly to enhance its capabilities in key areas like cloud services and cybersecurity.

Swiftnet has been impacted by terminations by a mobile network operator customer. The towers business isn’t easy and profitability is very sensitive to changes in revenue. Swiftnet is currently up for sale and Telkom is in discussions with two bidders after refining a list of shortlisted bidders.

Telkom unfortunately finds itself with a portfolio of problematic businesses and a complicated road to travel to improve them.

Little Bites:

Director dealings:

Value Capital Partners, which has director representation on the board of Altron (JSE: AEL), has invested another R13 million in shares in the company.

A director of Argent Industrial (JSE: ART) – and not the CEO who has recently been active in the shares – has sold shares worth R182.6k.

Investec Property Fund (JSE: IPF) wants to change its name to Burstone Group. After the (very expensive) internalisation of the ManCo, moving away from the Investec branding is the logical next step.

Awkwardly, the chairperson of the Social and Ethics Committee at Clientele Limited (JSE: CLI), Pheladi Gwangwa, has been suspended for 6 months from practising as an attorney by the Supreme Court of Appeal pending an investigation into her conduct at a law firm.

Finbond’s (JSE: FGL) acquisition of Trustco Finance Namibia from Trustco (JSE: TTO) is taking longer than expected. The fulfilment date for conditions precedent has been extended from 31 July to 31 August 2023.

African Dawn Capital (JSE: ADW) reported a headline loss per share of 24.5 cents for the year ended February. That’s 20.7% worse than the prior year. The auditors have noted a material uncertainty regarding the group continuing as a going concern.

The Ghost Wrap podcast is proudly brought to you by Mazars, a leading international audit, tax and advisory firm with a national footprint within South Africa. Visit the Mazars website for more information.

Woolworths reported solid numbers that seemed to be in line with market expectations.

Shoprite has blown competitors away with exceptional growth across the LSM curve.

Liberty Two Degrees is only a happy story if you’re a recent investor, giving us another excellent example of why buying the “hype” sector (in this case property on the JSE in 2015 – 2017) is so dangerous.

Spur is buying a 60% stake in Doppio Zero, a restaurant group that has grown spectacularly over the past two decades.

AVI is proof that consumers will cut back on many things, but not on biscuits and snacks.

British American Tobacco is still growing profits, albeit very slowly.

Anglo American shows just how quickly a mining cycle can change, with a 55% drop in HEPS.

ArcelorMittal is the ultimate basket of risks: single-commodity exposure, high operating leverage and plenty of debt as well!

AYO releases the GEPF repurchase circular (JSE: AYO)

The AYO board has effectively chosen the lesser of two evils

AYO Technology has released the circular dealing with the repurchase of 17.2 million shares from the Government Employees Pension Fund (GEPF) for R619.4 million.

There’s some interesting commentary in the announcement. The independent expert notes that the repurchase is unfair to AYO shareholders. The board says that it is unfair but reasonable to shareholders. That decision is based on the board’s view that the alternative is much worse, being protracted legal action with the PIC and GEPF and the risk of a negative outcome that would “potentially have resulted in the liquidation of AYO.”

It’s a mess, either way.

Clientele is sniffing around a potential acquisition (JSE: CLI)

This cautionary announcement has more details than the last one

Clientele released a cautionary announcement on 15 June that didn’t give the market anything to work with. With the release of a further cautionary announcement, we now know that Clientele is considering a potential acquisition in the insurance sector.

At this stage, there is absolutely no guarantee of a transaction being announced, let alone successfully finalised. That’s exactly why shareholders are warned to act with caution.

Delta Property just can’t catch a break (JSE: DLT)

Transactions with DMFT Property Developers have fallen through

With a share price down 97% over five years, Delta Property Fund is one of those companies that just cannot seem to catch a break. The very last thing the company needs is for transactions to fall through, especially when they went through the expense of issuing a circular and getting all the required approvals.

It’s rare to see an unconditional transaction fall through for reasons other than regulators blocking the deal. In this case, the buyer (DMFT Property Developers) failed to provide the bank guarantee or the required cash. In other words, they didn’t have the money. This sounds a lot like breach of contract, but the announcement doesn’t give any indication that the company is seeking damages. If they can’t afford the properties, I guess there isn’t much available for damages either.

The Capital Towers disposal is thus no longer proceeding. Four other enterprises were also being negotiated for disposal to DMFT. Those deals are also dead, with DMFT trying to reduce the purchase price in a way that is unacceptable to Delta.

That really is bad luck for the company.

A number of ship transactions at Grindrod Shipping (JSE: GSH)

This industry is all about managing the fleet

There’s an argument that this announcement is business as usual, as shipping companies are constantly managing the size and age of the fleet. Perhaps the sheer number of transactions triggered the Grindrod Shipping management team to release this announcement.

Without going into too much detail on the underlying transactions, the interesting thing is to take note of the different types of transactions. For example, one of the deals was to exercise the purchase option on a chartered-in supramax bulk carrier. The company also charters boats out to other shipping companies.

To give you an idea of the value of each vessel, the prices on the various transactions range from $10.8 million to $33.75 million. Age and size are relevant factors.

As a final comment, the announcement talks about “disinterested members” of the board. That always makes me laugh. It means that they have no economic interest in the transactions, not that they were bored at the meeting!

Perhaps the more important announcement relates to disclosures made by Taylor Maritime Investments (which holds 83.23% in Grindrod Shipping) about the company. It notes that the net time charter equivalent (TCE) across the Taylor and Grindrod fleet was $12,735 per day for the quarter. The breakeven level (including finance costs) is $11,700 per day. Again, this is for both fleets, so there isn’t a direct read-through to Grindrod Shipping.

Taylor also disclosed that Grindrod Shipping has repaid $28 million in debt during the quarter, with debt to gross assets now at 37.8% at the end of June 2023 vs. 38.9% at the end of March. That ratio includes Taylor and Grindrod Shipping.

If you follow Grindrod Shipping very closely, that might help with your financial modelling. Just be careful of these numbers as they apply to the broader group, not just Grindrod Shipping.

A changing of the guard at Netcare (JSE: NTC)

After a long innings as CEO, Dr Richard Friedland is retiring

Dr Richard Friedland has been around at Netcare for a very long time: 30 years in total, 18 of which have been as CEO. He will be stepping down as CEO with effect from 30 September 2024. I guess after being in charge for this long, you need to give a lot of notice!

The past few years haven’t been easy at all. Ironically, the pandemic caused a lot of problems for healthcare groups, as evidenced by this chart:

A successor will be named in due course. Goodness knows they have enough time to find someone!

Old Mutual strategic update (JSE: OMU)

There’s a lot of fluff, but there’s some good stuff too

If you like, you can refer to the full presentation from the investor update at this link. You likely need to make time to listen to the recording though, as many of the slides aren’t hugely relevant without the associated voiceover.

The section that caught me eye relates to the launch of Old Mutual’s bank, with a targeted launch in 2024 and breakeven in 2027. As Discovery will tell you, successfully building a bank is a helluva thing.

The benefit to Old Mutual is that retail deposits offer the cheapest source of funding around. Your current account pays you no interest and most savings accounts don’t pay much. This is how banks with a strong deposit base enjoy cheap funding and high net interest margin, as they lend the money out at much higher rates than they pay to depositors.

The presentation notes that the bank will be differentiated by cost. Are we seeing a potential competitor to Capitec here?

Within six years, Old Mutual hopes to be achieving a return on net asset value equal to the cost of equity plus 600 basis points. If they get that right, it would justify the price trading at a substantial premium to book value.

Of course, plans on a slide are easy. Execution is hard, especially in this economy.

Salungano gives some encouraging news (JSE: SLG)

It’s been a weird time for the group

There’s an ongoing delay in the publication of Salungano’s results for the year ended March. Shareholders don’t like that, especially when the delay is because of funding negotiations with lenders that needed to be finalised before results could be released.

It certainly doesn’t help that three directors have resigned during this period, with no replacements named as of yet.

With the share price down a whopping 51% in the past three months, the company needs to get it together. The good news is that the commercial terms for the refinancing have been agreed, subject to lenders’ credit approval. That doesn’t necessarily mean that the worst is over. It’s just a step in the right direction.

The company has committed to released results by no later than 31 August.

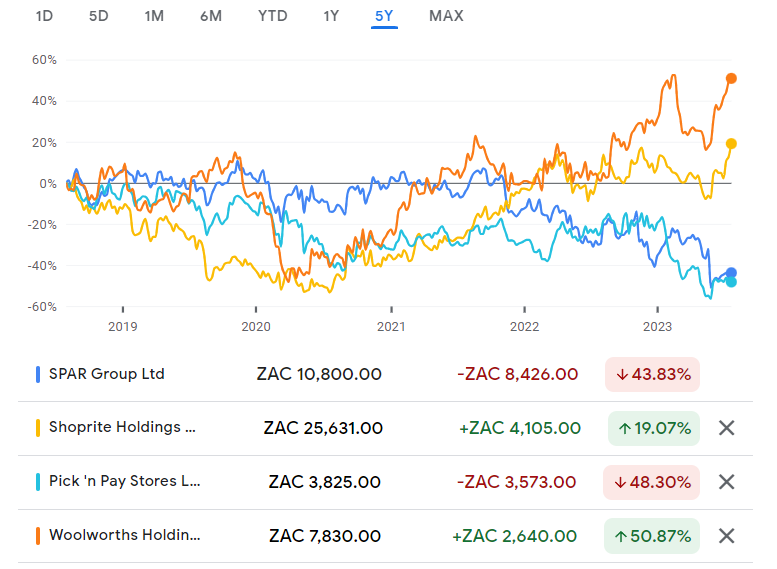

Spar announces its new executive team (JSE: SPP)

Megan Pydigadu certainly enjoys a challenge

Mike Bosman has been filling in as CEO after the significant recent upheaval of the Spar management team. New brooms have now arrived to sweep clean, with Bosman returning to his role as Chairman.

In the CEO chair, we find Angelo Swartz who has been with the Spar group for 16 years. His current role is Divisional Managing Director of SPAR KwaZulu-Natal, so he must’ve been having loads of fun with the disastrous ERP implementation that severely affected inventory flow in the region.

Megan Pydigadu joins as COO, moving to the retailer from EOH where she steered the group to financial sustainability as its CFO. She clearly enjoys a turnaround challenge, although Spar is in nowhere near as much trouble as EOH was when she joined.

The divergence in five-year share price performance in this sector is breathtaking:

Woolworths expects a decent HEPS uplift (JSE: WHL)

The share price didn’t really react to this update

In the 52 weeks to 25 June 2023, Woolworths needs to split its results into continued and discontinued operations. The latter is David Jones, which was disposed of with effect from 27 March 2023. It wouldn’t make sense to include those numbers in a financial analysis of Woolworths.

From continuing operations (i.e. excluding David Jones), sales increased by 10.8% for the year and 9.3% on a like-for-like basis. Despite the very tough local conditions in the second half of the year, sales increased 9.2% in H2.

There’s been solid follow-through in online sales, up 9.3% and now contributing 8.3% to group turnover.

In the Woolworths Food business, turnover grew 8.5% and 6.3% on a same-store basis. That’s way below the numbers being achieved by Checkers, though that’s not an entirely fair comparison as Checkers has a much broader product range and has likely won most of its market share from Pick n Pay in the past year. The second half of the year was impressive in Woolworths Food, with growth of 9.4% overall and 7.2% on a like-for-like basis.

With price inflation of 8.3% for the year, volumes are down by around 2%. Woolworths is being squeezed on price by competitors. Product inflation was 9.9%, which means the retailer had to absorb some of the pressure in its gross margin.

Online sales in Woolies Food increased by a substantial 28.5%, now contributing 3.8% of sales.

There has been significant focus on Fashion, Beauty and Home at Woolworths. The FBH business grew turnover by 8.9% and 8.3% on a like-for-like basis. Price inflation of 11.6% suggests a 3.3% drop in volumes. Unlike in Food where sales accelerated in the second half of the year, FBH only booked growth of 6.7% in the second half of the year. Online sales grew 3.8% and contributed 4.3% of local sales.

In Woolworths Financial Services, the book increased 14.5% year-on-year which suggests a higher proportion of credit sales. The impairment rate was up to 7.3% from 4.7% in the prior year, a clear reflection on the economic health of consumers.

In Australia and New Zealand, the only business that matters now is Country Road Group. It grew sales by 12% overall and 12.4% on a like-for-like basis. When like-for-like growth is below total growth, it tells you that trading space has been reduced (in this case by 3.9%). Price inflation unfortunately isn’t disclosed. Sales growth in the second half was just 0.6%, so that’s not encouraging. Online sales contributed 27.1% to total sales vs. 31.6% in the prior year, so there has been a return to bricks-and-mortar shopping in the region.

For the 52 weeks ended June, HEPS from continuing operations should be between 10% and 20% higher. If you are happy to work with adjusted HEPS, the range is 396.2 to 432.2 cents. At the midpoint, this implies a Price/Earnings multiple of 18.9x.

Little Bites:

Director dealings:

An associate of the ex-CEO of Emira Property Fund (JSE: EMI) acquired shares worth R249k.

The post-commencement finance facility at Tongaat Hulett (JSE: TON) has been extended to 6 October. This is critical to the ongoing nature of the business rescue process.

Conduit Capital (JSE: CND) is in the process of selling CRIH and CLL to TMM Holdings for R55 million. The fulfilment date for conditions precedent has been extended to 1 September. It’s already been extended once before, from 1 July to 1 August.

African Dawn Capital (JSE: ADW) has a market cap of just R8.5 million. That’s worth about as much as a successful restaurant! For the year ended February 2023, the headline loss per share will be between 23.49 cents and 25.52 cents. The share price is just 12 cents.

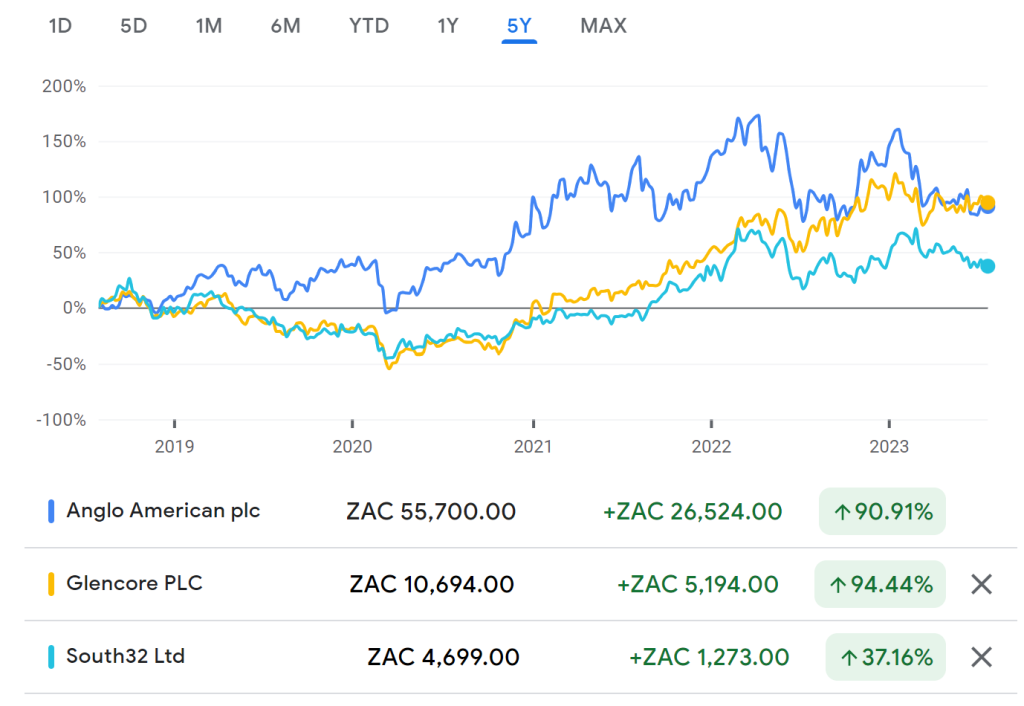

Anglo American reports a big drop in earnings (JSE: AGL)

A drop of 55% in HEPS isn’t pretty

The mining industry has been dealing with a drop-off in commodity prices this year. Cycles are nothing new to mining, with volatile earnings as standard practice in this game. That’s even true for the likes of Anglo American, with a diversified portfolio.

Over five years, you’ve still done alright in these names:

For the six months to June 2023, EBITDA fell by 41% in an environment of lower commodity prices. The basket price across the group fell by 19% and unit costs increased by 1%. Volume increases of 10% partially offset the impact, with group revenue down by 13%.

Net debt of $8.8 billion is less than 1x annualised EBITDA, so the balance sheet is ok. This is why the dividend payout policy of 40% has been maintained.

Here’s one for the books though: attributable free cash flow fell from $1.56 billion to -$466 million. Yes, that is negative free cash flow! Welcome to mining, where capital expenditure is huge.

Return on Capital Employed has fallen from 36% to 18%. This isn’t a good enough return for the risk in my opinion.

A headline loss of R448 million broke the share price when warning was first given

Let’s kick off with a share price chart, showing you exactly when news broke of how bad these ArcelorMittal numbers will be:

As you can see, the price partially recovered, although the downward trend is clear.

In the six months to June, a drop in realised rand prices of 8% ruined the fun. Although volumes were up 3%, there’s so much operating leverage in this business that EBITDA crashed by 86%. Operating leverage refers to the extent of fixed costs, something that is incredibly important in manufacturing and mining businesses. With vast fixed costs, a small drop in revenue can cause havoc for profitability.

EBITDA of R499 million was eaten up by the banks before we get to the headline loss of R448 million. Net borrowings increased from R2.8 billion to R2.9 billion, so ArcelorMittal is the poster child for the dangers of combining operating leverage and financial leverage.

As you’ve probably guessed, there is no dividend here.

With cash from operations of R891 million and a huge capital expenditure bill of R818 million, free cash flow is almost non-existent here. The company will need to make some major internal changes before it can make a dent in the debt.

Hammerson is paying dividends again (JSE: HMN)

This is important for local fund Resilient

A property fund that doesn’t pay dividends is about as useful as a leaky bucket. Nobody is buying property funds purely for capital growth, that much I can promise you.

After considerable pressure from shareholders (not least of all local fund Resilient), Hammerson has returned to paying cash dividends with the release of interim results. The disposal of £215 million worth of non-core assets has helped repair the balance sheet. Net debt to EBITDA is now at 7.7x vs. 10.4x at the end of the last financial year. The more common metric is loan-to-value, which is at 33% vs. 39% at the end of the last financial year.

Adjusted earnings increased by 15%, although most of that is because of lower net finance costs because debt was reduced. Like-for-like net rental income only increased by 2.3%.

The interim cash dividend is 0.72 pence per share, which works out to around 16 ZAR cents. The current share price is around R5.88.

A massive payday for Liberty Two Degrees shareholders (JSE: L2D)

There’s nothing quite like a 42% jump in the share price in a single morning

Liberty Group wants to take Liberty Two Degrees private. This will be via a scheme of arrangement, with a proposed cash price of R5.55 per share. Liberty Two Degrees closed at R3.90 the day before the announcement, so that’s a lovely premium for shareholders. Well, recent shareholders at least. If you held since listing, then I’m afraid you’ve had a bad time:

The net asset value per share at the end of December 2022 was R7.51, so Liberty is also getting a pretty good deal if we believe that number.

You may recall that Liberty Group is now a wholly-owned subsidiary of Standard Bank Group. This deal is ultimately a big property play by Standard Bank.

Liberty group already owns around 61% of the shares in Liberty Two Degrees It also owns 66.7% in the underlying portfolio, with Liberty Two Degrees holding 33.3%. In other words, this transaction is about taking out the minority shareholders.

Mazars Corporate Finance was appointed as independent expert on this one, concluding that the transaction is fair and reasonable to Liberty Two Degrees shareholders.

Non-binding letters of support have been received from Coronation (holding 22.5% of the shares or 61.1% of shares eligible to vote) and Sesfikile Capital (holding 1.3% of the shares or 3.6% of shares eligible to vote). This gets them very close to having a successful scheme of arrangement, which requires 75% approval.

Hot potato Royal Bafokeng Platinum is loss-making (JSE: RBP)

Impala Platinum will need to work this asset

Things aren’t great in the platinum group metals (PGM) industry at the moment. Royal Bafokeng Platinum is dealing with additional issues, like operational challenges at the Styldrift mine and a decrease in production.

Even if production went according to plan, it’s hard to do well when the rhodium price tanked by 50% and the 4E basket price fell by 23.6%. As a further squeeze on profitability, mining costs increased by more than CPI inflation.

The headline loss per share is a nasty -113.8 cents, which is way off HEPS of 767.3 cents in the comparable prior period. Impala Platinum is about to own this entire thing, so hopefully it can only get better from here.

Sirius recycles capital in the UK (JSE: SRE)

In other words, it has bought properties after recently selling a couple

In the property sector, funds are forced to “recycle capital” because raising money is expensive. There was a time on the JSE a few years ago when property groups could raise seemingly endless capital in literally a couple of hours. The days of accelerated bookbuilds are long gone, so management teams must earn their salaries by buying and selling properties intelligently.

Sirius Real Estate has announced that UK subsidiary BizSpace has acquired two mixed-use industrial assets for £9.5 million on a net initial yield of 9.6%. This comes after recent sales in the UK at a combined premium to book value. Sirius will want to demonstrate value creation to shareholders by actively managing these new assets.

Spur: people with a taste for Italian (JSE: SUR)

I have fond memories of the Doppio Zero group from my Joburg days

The Doppio Zero / Piza e Vino / Modern Tailors group is focused on Gauteng, so don’t feel bad if you haven’t heard of the restaurants in other provinces. In fact, with a footprint of 37 franchised and company-owned restaurants, only 4 of them are outside of Gauteng.

Spur is acquiring a 60% stake in the chain, as well as the central supply business and bakery. The sellers are the founders, who will remain as executives of the group for a minimum of five years.

The rationale for the deal is to almost double the size of Spur’s “speciality” portfolio, which includes The Hussar Grill, Nikos and Casa Bella.

The Doppio Zero group generated total sales of over R600 million in the year ended February 2023. That’s impressive for a group that was only founded in 2002 as a bakery and cafe in Greenside! There are 669 employees.

The announcement doesn’t disclose the transaction value. It also doesn’t indicate whether there are put / call option structures over the remaining 40%. For the sake of the founders, I hope they negotiated a liquidity mechanism to realise the rest of the value after the five year period as executives.

Super Group reports a super jump in earnings (JSE: SPG)

These are properly impressive numbers in this environment

For the year ended June 2023, Super Group has reported a 20% to 27% increase in HEPS. That’s juicy. Even more impressive is the fact that the base period included once-off benefits of 38.8 cents per share in the HEPS number of 380.7 cents.

The narrative sounds good, with market share gains on the top line and solid cost management to boost profitability. On top of this, the group remained highly cash generative. This supports the ongoing strategy to look for useful acquisitions to supplement organic growth.

The earnings range for the period is 456.8 cents to 483.5 cents. The share price is just over R35, suggesting a Price/Earnings multiple of around 7.5x.

Trustco finally announces the Meya Mining deal (JSE: TTO)

Perhaps unsurprisingly, it’s complicated

The overall story here is that Trustco has raised $75 million for the completion of the Meya Mining development, a diamond mine in Sierra Leone. If you read carefully though, it looks like only $50 million is confirmed.

Sterling Global Trading is subscribing for shares in Meya Mining for $25 million. This gives the company a 70% shareholding. Trustco Resources will hold 19.5% and Germinate will hold 10.5%.

On top of this, Sterling will advance a loan of $25 million to Meya. A mystery market lender is going to lend another $25 million, taking the total to $75 million. It sounds like only the $50 million has been finalised, though.

Trustco is going to subordinate its shareholder loan of $45.4 million in favour of this new debt. In other words, the new debt is repaid first and takes preference in a liquidation event.

Trustco has invested $116 million in this asset since inception. I’m not sure if this included any debt that has been previously repaid, but the current subscription price implies an equity value of $35 million. If we add in the shareholder loan, we get to Trustco having total value here of $45.4 million + $6.8 million = $52.2 million. That sounds like a significant loss, but I’m happy to be corrected here.

This is a Category 1 transaction and so a circular will need to be distributed to shareholders. Irrevocable undertakings have been received in respect of 63.26% of shares in issue, so that should be a done deal as it only needs an ordinary resolution.

Little Bites:

Director dealings:

An independent non-executive director of RECM & Calibre (JSE: RAC) bought shares worth R516k.

An independent non-executive director of Balwin (JSE: BWN) has bought shares in the company worth R135k.

Weirdly, the CEO of Argent Industrial (JSE: ART) is now selling shares after buying just a couple of weeks ago. The sale was for R51.8k.

A director of Mantengu Mining (JSE: MTU) has bought shares worth R31k.

Anglo American Platinum (JSE: AMS) has named Craig Miller as the incoming CEO to replace Natascha Viljoen from 1 October. Viljoen is moving into the COO role at Newmont Corporation. Miller is currently the finance director, a role he has held since 2019. This means that the company needs to find a new finance director, with no successor named as of yet.

Liberty Group (LGL), a subsidiary of Standard Bank, has announced its intention to acquire the remaining shares not already held in Liberty Two Degrees (L2D). L2D shareholders have been offered a cash consideration of R5.55 per share in a deal worth c.R1,9 billion. The share price closed 44% up on the day. Coronation Asset Management and Sesfikile Capital have confirmed that they will support the scheme and together they represent 64.4% of the shares that may vote.

Spur Corporation, in a move to strengthen its position in the day-time speciality dining space and enter the coffee speciality market, has acquired a 60% stake in the Doppio Group. The stake was acquired from founders Paul Christie and Miki Milovanovic. While financial details of the transaction were undisclosed, it was disclosed in the announcement that the Doppio Group generated total sales of over R600 million in the financial year ended February 2023.

Trustco aims to raise c.US$75 million which will be used to complete the Meya Mining development. Sterling Global Trading (SGT) will subscribe for shares valued at $25 million and will hold a 70% stake in Meya Mining. Trustco Resources will reduce its shareholding to 19.5% and Germinate SL will own a 10.5% stake. SGT will advance a $25 million loan and will work with Meya Mining to raise a further $25 million. The funds will ensure that Meya is fully capitalised and will enable the mine to scale production at an accelerated pace.

Labat Africa has acquired the remaining 30% stake in CannAfrica from H Maasdorp for a consideration of R6,43 million to be settled through the issue of 29,9 million Labat shares and the balance in cash of R2,8 million.

A preferred strategic equity partner (SEP) has been selected for Tongaat Hulett, currently in Business Rescue. The selected SEP is Kagera Sugar, a sugar manufacturing company situated in the North-Western part of Tanzania. The transaction will comprise the acquisition of the complete sugar division of Tongaat Hulett in South Africa and the investments in Zimbabwe, Mozambique and Botswana. Financial details were undisclosed.

Sirius Real Estate, through its UK subsidiary BizSpace, has acquired a portfolio of two mixed use industrial assets located in Liverpool and Barnsley. The assets have a combined area of 71,957 square feet of predominantly workshop accommodation. Sirius acquired the portfolio for £9,5 million representing a net initial yield of 9.6%.

The offer in Q4 2021 by Impala Platinum (Implats) to Royal Bafokeng Platinum (RBPlat) shareholders finally closed this week with RBPlat shareholders holding 121,437,384 shares (96.21% of shares not held by Implats at the time of the offer) accepting the offer. In aggregate Implats now holds 98.35% and will invoke section 124(4) of the Companies Act to compulsorily acquire all the RBPlat shares not already held. Application will be made for the termination of the listing of the RBPlat shares on the JSE which will become a wholly-owned subsidiary of Implats.

ArcelorMittal South Africa is proposing to modify its existing 2016 B-BBEE transaction which, according to the company’s announcement, has not yielded the envisaged value for the empowerment partners and employees. The modified transaction will see the BEE parties (Amandla We Nsimbi, Likamva Resources and the Isabelo 2 Share Trust) holding a 21.75% direct stake in the company. The transaction is subject to shareholder approval and will require the issue of a circular setting out the full terms and conditions of the transaction.

Unlisted Companies

Five35 Ventures a Johannesburg-based pan-African female-focused venture capital fund investing in early-stage tech start-ups, has made an undisclosed investment in Zuri Health. The Kenyan startup provides customers with affordable, convenient and quality healthcare services via its app, SMS and WhatsApp. Zuri Health’s services are available in Ghana, Nigeria, Senegal, South Africa, Uganda, Tanzania and Zambia.

Kasha Global, a Kenyan women-led and focused healthcare retail platform has raised US$21 million in a Series B round led by Cape Town-based Knife Capital. Kasha sells and delivers pharmaceutical products, household goods and consumer health products to low-income consumers, resellers, pharmacies and health facilities in East Africa.

The Competition Tribunal has conditionally approved the acquisition of a 51% stake in SAA by Takatso Aviation. SAA entered business rescue in December 2019. In terms of the deal, Takatso’s major shareholder Harith has raised R3 billion which it will commit to SAA. The Department of Public Enterprises will continue to hold the remaining 49% stake in the airline.

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept All”, you consent to the use of ALL the cookies. However, you may visit "Cookie Settings" to provide a controlled consent.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. These cookies ensure basic functionalities and security features of the website, anonymously.

Cookie

Duration

Description

cookielawinfo-checkbox-analytics

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics".

cookielawinfo-checkbox-functional

11 months