Altron flags a flat interim performance (JSE: AEL)

The market didn’t love it

Altron’s share price dropped 10% on Thursday based on a voluntary update that indicates a flat revenue and EBITDA performance for the six months to August 2025. They’ve noted a tougher operating environment with tight IT budgets.

Of course, a flat group performance doesn’t mean that there aren’t big swings at segmental level. The Platforms segment achieved double-digit revenue growth (which naturally means solid EBITDA growth as well), while the IT Services segment bore the brunt of the trickier environment. The Distribution segment has also had a tough time.

Full details will be available when interim results are released on 3 November.

Equites Property Fund remains committed to shifting capital from the UK to SA (JSE: EQU)

The loan-to-value ratio is expected to drop sharply thanks to disposals

Equites released a pre-close update that deals with the six months ending August 2025. They’ve used it as an opportunity to remind the market that the plan is to sell off the UK portfolio and allocate the capital to South Africa instead. How times have changed in the past decade in the property sector!

The UK portfolio seems to be in decent shape at the moment, which would support an exit on reasonable terms. In South Africa, the appeal is that there’s limited availability of large land that is suitable for logistics hubs, hence the desire by Equites to get moving on its land parcel for development. It’s been an expensive four years of development (peaking at over R2.5 billion in 2024) and they expect it to settle at R1 billion in FY26.

The loan-to-value ratio is estimated to be 37.9% at the end of this interim period. Thanks to the extensive disposals, they expect it to drop to 24.3% by the end of the 2026 financial year. Other important guidance is that they expect the distribution per share to increase by between 5% and 7% for the year.

Harmony has its heart set on copper, but they need to maximise the gold opportunity (JSE: HAR)

Gold production in FY26 is still expected to be below FY24 levels

Harmony Gold may have gold in the name, but they are definitely splitting their love across two commodities at the moment. They expect to conclude the MAC Copper acquisition in October as part of their diversification plan.

Of course, if gold wasn’t shooting the lights out at the moment, the market would probably be more enamoured with the copper strategy. Instead, we have a situation where Harmony is lagging its peers due to gold production that dipped by 5% year-on-year at a time when the gold price has dished up a huge opportunity. Just because they are “within guidance” doesn’t mean that investors are happy.

Here’s the bigger frustration: production guidance for FY26 is between 1,400,000 and 1,500,000 ounces. That’s not encouraging vs. FY25 at 1,479,671 ounces. It’s also well below the FY24 number of 1,561,815 ounces, so things are going backwards.

Unfortunately, the drop in production has been accompanied by a substantial increase in all-in sustaining costs (AISC) of 17%. Again, that’s in line with guidance, but that doesn’t make it good. Guidance for FY26 is AISC of between R1,150,000/kg and R1,220,000/kg, another significant increase vs. FY25 at R1,054,346/kg.

Despite major metrics going the wrong way in FY25, HEPS increased by 26% thanks to the one thing that Harmony cannot control: the gold price. Based on the guidance for FY26, they will need the gold price to keep shining brightly next year.

FY25 was a year to forget for Impala Platinum (JSE: IMP)

PGM prices were flat for the year ended June, with hopes of better times to come

As I’ve written many times in Ghost Bites, the PGM sector rally has been firmly forward-looking rather than based on the performance over the past year. Impala Platinum is further proof of that, with ugly numbers for the year ended June 2025 that saw revenue dip by 1.1% and EBITDA fall by 19.8%. HEPS was down by 69.5%.

The reason for the financial pain was a small dip in sales volumes at a time when the rand price per 6E ounce was flat. Mining costs certainly don’t sit still, so a year in which revenue goes nowhere means a period of margin compression.

The silver lining was the cash, with a major swing into positive free cash flow and even the declaration of a dividend of 165 cents per share (more than double HEPS for the year). Impala’s dividend policy is based on free cash flow.

The outlook for FY26 is growth in unit costs of between 4% and 9%. They expect saleable production of between 3.4 and 3.6 million ounces, which implies decent growth on the FY25 number of 3.37 million ounces. But of course, what they really need is for the PGM price to behave itself.

Nothing ever seems to get better for KAP investors (JSE: KAP)

The share price is way down this year and so are the earnings

KAP has released financials for the year ended June 2025. They aren’t good, with revenue down 2%, operating profit down 14% and HEPS nosediving 47%. Unsurprisingly, there’s no dividend.

Concerningly, it seems like the fourth quarter had the worst operating conditions of the year, which means negative momentum going into the new financial year.

The ramp-up of the new MDF line at PG Bison is absolutely key to getting the numbers into the green, with revenue up 10% and operating profit down by a nasty 28% in that business. Operating margin has fallen sharply from 17.4% to 11.3%. Sadly, margins are expected to be below historical levels in the near term, with market conditions making it difficult to optimise this investment.

Elsewhere, Safripol grew revenue by 4% and operating profit by 43%. Operating margin in that business increased from 3.8% to 5.2%, which is still a paper thin margin. At Unitrans, revenue fell 4% and operating profit was down 14%, a good example of operating margins going the wrong way. Feltex is a particularly nasty story in the OEM automotive value chain, with revenue down 8% and operating profit down 37% due to lower volumes and non-recurring costs related to a model changeover. Sleep Group went the right way at least, with revenue up 7% and operating profit up 27% thanks to improved mix. Finally, Optix remains a mess, with revenue up just 1% and an operating loss of R44 million – you definitely can’t scale into profitability with a growth rate of 1%!

KAP just never seems to catch a break.

Positive momentum at Libstar – at last (JSE: LBR)

I’ve certainly done my part in boosting cheese sales

Libstar has been a disappointing story in our market. The FMCG company has lost around 65% of its value since listing in 2018. Like so many consumer businesses in South Africa, things just haven’t worked out as planned.

The good news is that the six months to June 2025 reflect solid positive momentum in the business. If they can keep this up, then things could get very interesting for punters – as evidenced by the share price being up 14% in the past month.

For the six months, HEPS will be up by between 15.1% and 25.2%. Normalised HEPS from continuing operations will be up by between 10.4% and 20.4%. Much like a slice of their cheese, whichever way you cut it, that’s still yummy.

Metrofile’s earnings have dropped, but a potential deal is still on the table (JSE: MFL)

So, the usual story then

If you threw darts at a timeline in recent years, chances are good that you would hit a spot where (1) Metrofile’s earnings are under pressure, and (2) someone is considering an offer for the company. The latest period is no different.

For the year ended June 2025, a trading statement tells us that Metrofile expects HEPS to drop by between 12% and 27%. Ouch.

Luckily, a Delaware-based company is still serious about making an offer, with discussions at an “advanced stage” – although the timeline has been extended based on engagements with regulators.

The share price is up 20% year-to-date and a whopping 106% over six months. This has everything to do with the potential offer and nothing to do with the underlying earnings, that’s for sure.

A pot of gold at Rainbow Chicken – and yes, even a dividend (JSE: RBO)

The volatility in chicken earnings remains breathtaking

If you follow the poultry sector, you’ll know that modest changes in revenue can drive substantial moves in profits. This is because of the operating leverage inherent in the model, as well as the structurally low operating margins that are impacted by modest moves in e.g. gross margin.

What does this look like in practice? Rainbow Chicken’s numbers for the year to June 2025 reflect growth in revenue of 9% and a move in EBITDA margin from 4.4% to 6.7%. By the time you get to HEPS, you find an insane jump of 224%!

Such is the improvement in this sector that there’s even a dividend of 20 cents per share (vs. HEPS of 65.57 cents).

I must remind you that it doesn’t take much for earnings in this sector to very quickly head the other way, so tread carefully. Personally, I prefer to eat chicken rather than invest in it.

Gold and US PGMs gave Sibanye-Stillwater’s earnings a huge boost (JSE: SSW)

There’s a 19-fold increase in headline earnings!

For a long time, I considered myself a bit unlucky in Sibanye. I watched my stake sit in the red for ages, which is unfortunately a feature rather than a bug when it comes to cyclical stocks. Still, the PGM market felt like it took forever to get going.

But where I got extremely lucky was in my decision to take the money and run a month ago. It’s rare in life that you genuinely sell at the top of a chart, so I’ll take the wins where I can. The negative momentum over the past month has been pretty rough, with the share price having dropped by 20% in just a few weeks:

If you think the share price is volatile, wait until you see the earnings. Sibanye released results for the six months to June 2025 and they reflect headline earnings that have gone to the moon, up 19 fold vs. the prior year!

I always skip straight to the segmental reporting to see where the big moves were. The biggest contributor in this period was South African gold, with adjusted EBITDA more than doubling from R2.2 billion to R4.8 billion. That’s only slightly more than South African PGMs, with remarkably consistent adjusted EBITDA of R4.78 billion. So, that’s a strong performance locally.

Looking abroad, the big win was in US PGMs, with both the underground and recycling operations experiencing a huge positive move in earnings. If you add them together, adjusted EBITDA jumped from R635 million to R5.15 billion. A special mention must also go to zinc for an adjusted EBITDA turnaround from a loss of R351 million to profit of R657 million. The remaining ugly duckling is lithium, with a loss of R310 million that is even higher than the loss of R280 million in the comparable period.

Unfortunately, Trump’s One Big Beautiful Bill Act means that the big beautiful S45X10 credits that Sibanye enjoys on PGMs in the US will be phased out between 2031 and 2034. That may sound far away, but mining is a long-term game. This legislative change has driven an impairment of R3.8 billion to Sibanye’s PGM operations.

I must note that there’s an even larger impairment of R5.3 billion to the Keliber lithium project, based on changes to forecast lithium prices. Due to Sibanye’s efforts to have its fingers in many pies, in some cases in contrasting strategies (PGMs vs. battery technology), chances are that some parts of the group are doing well and others are in trouble at any point in time.

Overall though, the group is in a much better place than before. They are taking advantage of the improved market conditions and they are telling a bullish story around cash generation heading into 2026.

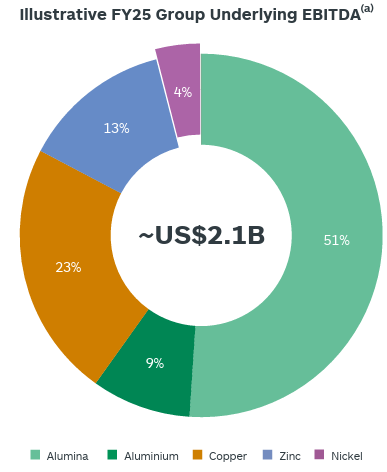

A strong year for South32 (JSE: S32)

Revenue and profits both came in significantly higher

South32 has released results for the year ended June 2025. Revenue from continuing operations was up 17% and the ordinary dividend increased by 71%, so there’s plenty for investors to smile about. Diluted HEPS was 91% higher

The results presentation includes this handy chart that shows how the group made its money in FY25, adjusted for the disposal of Illawarra Metallurgical Coal, the impact of a cyclone on manganese in Australia and a few other bits and pieces:

This gives you a really useful lay of the land. It also shows you just how important alumina and aluminium is to the group. Thankfully, Mozal Aluminium (which is likely to stop producing after March 2026 based on energy availability) is just one part of the group. It contributed 355kt of the total 671kt of aluminium in FY25, so it’s big enough to be an annoying drag on earnings, but definitely not big enough to cause a major issue all by itself.

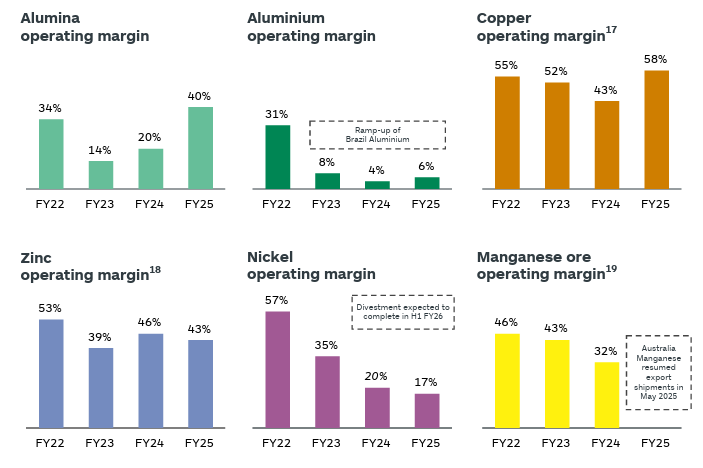

Another interesting view is to see just how different the margins are across these commodities, as shown in these charts:

When people talk about the “mix effect” in margin, this is what they mean. As revenue changes across the underlying businesses, group margins shift based on the changing mix of revenue. The effect is less noticeable in groups with more consistent margins across the segments.

Overall, South32 is telling a bullish story as they head into a new financial year, with significant focus on Worsley Alumina as major growth capex project.

Excellent growth at STADIO shows that tertiary education is firmly a for-profit business (JSE: SDO)

Student growth is expected to remain strong

STADIO has released results for the six months to June 2025. They are really good, with student numbers up 9% in semester 1 and revenue growth of 16%. A mix of price and volumes growth is exactly what investors want to see, along with cost control that has led to a 24% jump in EBITDA. By the time you reach the bottom of the income statement, you’ll find a 28% increase in core HEPS.

With almost 55,000 students currently in the group, they reckon they can reach 80,000 students by 2030. Thanks to having multiple tertiary offerings in the group, I certainly wouldn’t bet against them achieving that target.

STADIO’s share price has tripled in the past 3 years. The underlying growth in tertiary education has certainly helped, but they still needed to deliver on the opportunity.

Have we reached the bottom for Trellidor? (JSE: TRL)

Hopefully the latest financial year is the end of the slide – but the UK is a worry

Trellidor has confirmed that the sale of Taylor Blinds and NMC became effective on 25 August 2025. The final price (after balance sheet adjustments) was R51.9 million. The good news is that a portion of this price will go towards further debt reductions, with the group having made excellent progress in reducing net debt from R146.7 million as at June 2023 to R85.3 million as at December 2024. Based on those dates, you can see that they’ve been in trouble for a while.

Is the pain over yet? Maybe, maybe not. A trading statement dealing with the year ended June 2025 shows us that HEPS will drop by between -5% and -15%, coming in at between 30.6 cents and 34.21 cents. The Trellidor UK division has been a disappointment in this period, which is a worry given the ongoing poor performance of the South African business.

The current share price of R1.92 means a Price/Earnings multiple of mid-single digits. Given the recent track record and now the concern around the UK, I still wouldn’t call that a bargain. Things might get worse for this share price, as evidenced by it closing 11% lower on the day of this announcement on strong volumes.

Is there a worse retailer in South Africa than Truworths? (JSE: TRU)

Sometimes, shares are cheap for a reason

There are some really innovative and interesting retailers in South Africa. Truworths definitely isn’t one of them. About the only positive thing I can say is that they aren’t losing money offshore like some competitors are doing. Office UK grew revenue by 9% in the year ended June 2025. But even with that revenue growth, trading profit (if you adjust for a major once-off in the base) was basically flat.

“Flat” is more than we can say for Truworths Africa, still the biggest contributor to trading profit in the group but not for long at this rate. Revenue went nowhere in this period and trading profit fell by around 16%.

Add these two segments together into a group result and you’ll find sales up by 3.2%, gross margin down 100 basis points to 41.3% and operating margin down 730 basis points to 20%. HEPS dropped by just over 8% to 752.1 cents and the dividend followed suit.

Any highlights? Well, the balance sheet is in a net cash position rather than net debt, but this can often just be due to the timing of working capital movements for retailers.

Truworths is trading on a Price/Earnings multiple of 8x. In my view, that’s still much too high. This is probably the last name I would own in this sector.

Nibbles:

- Director dealings:

- Associates of two director of Renergen (JSE: REN) – including the CEO) sold shares worth R7.8 million.

- The CEO of Grindrod (JSE: GND) – who is shortly leaving the group – sold share awards worth R4.4 million. The announcement isn’t explicit on whether this is the taxable portion or not.

- A director of a major subsidiary of Sasol (JSE: SOL) sold shares worth R501k.

- A non-executive director of Collins Property Group (JSE: CPP) sold shares worth R410k.

- A director of a major subsidiary of PBT Group (JSE: PBG) bought shares in the company worth almost R80k.

- An associate of the CEO of Acsion (JSE: ACS) bought shares worth R42k.

- The CEO of Vunani (JSE: VUN) is still on the bid, buying R2k worth of shares in an illiquid market for the stock.

- Frontier Transport (JSE: FTH) announced that CFO Mark Wilkin will be retiring with effect from August 2025, after roughly four decades with the company! He’s replaced by Ulandy Gribble, who is currently in charge of the numbers at Golden Arrow Bus Services (the largest subsidiary). It’s always good to see an internal succession plan playing out.

- Randgold & Exploration Company (JSE: RNG) released results for the six months to June 2025. This is a tiny listed company, so it just gets a passing mention here. The operating loss improved by 24% to R8.3 million (but that’s still a loss obviously) and the headline loss per share was 8.80 cents.

Note: Ghost Bites is my journal of each day’s news on SENS. It reflects my own opinions and analysis and should only be one part of your research process. Nothing you read here is financial advice. E&OE. Disclaimer.