In this edition of Ghost Bites:

- Araxi investors have been reminded of the lumpiness in the business

- Jubilee Metals is ramping up the Molefe Mine

Araxi investors have been reminded of the lumpiness in the business (JSE: AXX)

The growth story has suffered a wobbly

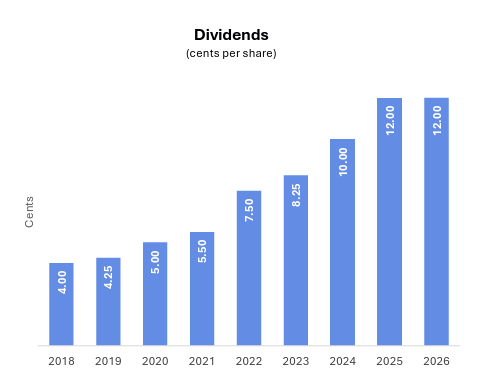

It’s rare to see a single chart doing a great job of explaining the underlying theme in a set of numbers. But I think this one is rather effective:

As you can see, the year ended March 2026 won’t go down as the happiest time in Araxi’s journey.

The period shows us an important risk in the business: the dependence on microchips in payment terminals. As anyone following the tech industry will know, microchips are becoming an increasingly rare and expensive commodity thanks to insatiable demand from the AI sector. This led to a delay in the delivery of a substantial customer order, with revenue from the sale of terminals dropping from R308 million to R230 million.

Another source of lumpy revenue is software licence fees. There was a once-off fee of R42 million in the base period, so this line item fell from R118.5 million to just under R77 million.

Together with general economic headwinds, these issues led to a 6.8% decline in group revenue. EBITDA fell by 16.4% and EBITDA margin contracted by 270 basis points to 24.0%. HEPS was down by a nasty 18.2%.

As a consolation prize, the dividend per share was kept steady at 12 cents per share, as you saw in the chart above. HEPS was 14.37 cents in this period, so there’s not much more wriggle room in that payout ratio.

This is a textbook example of the “stickiness” of dividends and how management teams would rather sell their first-born children than cut the dividend.

Araxi also presents a set of “underlying” numbers that make several adjustments. Other than splitting out that lumpy software fee, they also take out restructuring costs in the Software division, reverse transaction costs for the Pay@ deal and make other fair value and classification adjustments.

If you’re willing to go with that view, then revenue was down 3.6%, but EBITDA was up 5.9% as the margin expanded by 220 basis points. HEPS was up 10.1% through this lens. But don’t get too excited: this “growth” is because the base period looks far less demanding after these adjustments, rather than because FY26 is suddenly excellent. In fact, adjusted HEPS is 14.03 cents on this basis vs 14.37 cents as reported!

If you look through all the noise, there are a couple of highlights worth noting. The first is that despite the delay in terminal deliveries, the number of terminals in the hands of customers has increased by 5.4%. The second highlight I would consider is that the Software division saw a 77% increase in underlying EBITDA thanks to restructuring initiatives.

Still, this isn’t the set of numbers that investors wanted to see as the foundation for the Pay@ deal, in which Araxi has taken a considerable risk on a major acquisition. They’ve acquired an 80% stake for a meaty R1 billion, funded by R200 million of existing cash reserves and R800 million in senior debt. This takes them to a net debt to EBITDA ratio of 1.6x after the closing of the deal.

On a pro-forma basis, the contribution of the Payments division increases from 56% of group revenue to 66%. EBITDA moves up from 93% to 90%. The Pay@ deal takes them much deeper into the fintech and payments infrastructure in South Africa.

Given the complexities of the Software space at the moment, you really have to wonder why they don’t dispose of that business. It’s an even smaller contributor than before, yet it remains capable of dishing up headaches and distracting management. Even with all the work they’ve put in, the “underlying revenue” in Software was down 1.5% year-on-year!

There’s an interesting trend that comes through in the analyst presentation, which was also visible at the Altron (JSE: AEL) Capital Markets Day that I watched online. POS devices (payment terminals) are becoming more than just payment acceptance tools. They now include value-added services like inventory apps, which allow small merchants to track stock on their payment machines. With 64% of revenue in the Payments business being of a recurring nature, it’s critical that Araxi retains customers through delivering innovation.

Ghost Bite: This is a new era for Araxi. Instead of running a fortress balance sheet, they are now in a position where financial leverage can work against them in a weak period. Payment terminal delivery delays may be out of their control, but it’s a reminder of the layers of risk faced by the business during this AI supply crunch. This is going to be an interesting story to watch!

Jubilee Metals is ramping up the Molefe Mine (JSE: JBL)

Will investors like the “hub-and-spoke” development model?

Jubilee Metals released an operational update regarding the Molefe Mine in Zambia. This asset is key to the group’s mine-to-metals copper strategy.

After the successful expansion of Pit 2, run-of-mine deliveries to Sable refinery have recommenced. The targets move up quite quickly, from 6,000tpm in June to 10,000tpm by October 2026.

They are working on the integration of Pits 2 and 3 into a single enlarged open-pit operation. Once this is complete, they should be delivering more than 30,000tpm each quarter, an enormous jump from the previous level of 12,000tpm per quarter.

They describe their strategy in Zambia as being to mine while they explore, which means growing the production and resource base simultaneously. This means on-site ore sorting, processing capabilities and of course the Sable refinery as part of the value chain. They also describe it as a “hub-and-spoke” development model.

Ghost Bite: The share price moved slightly higher on this news, but remains 26% down year-to-date.

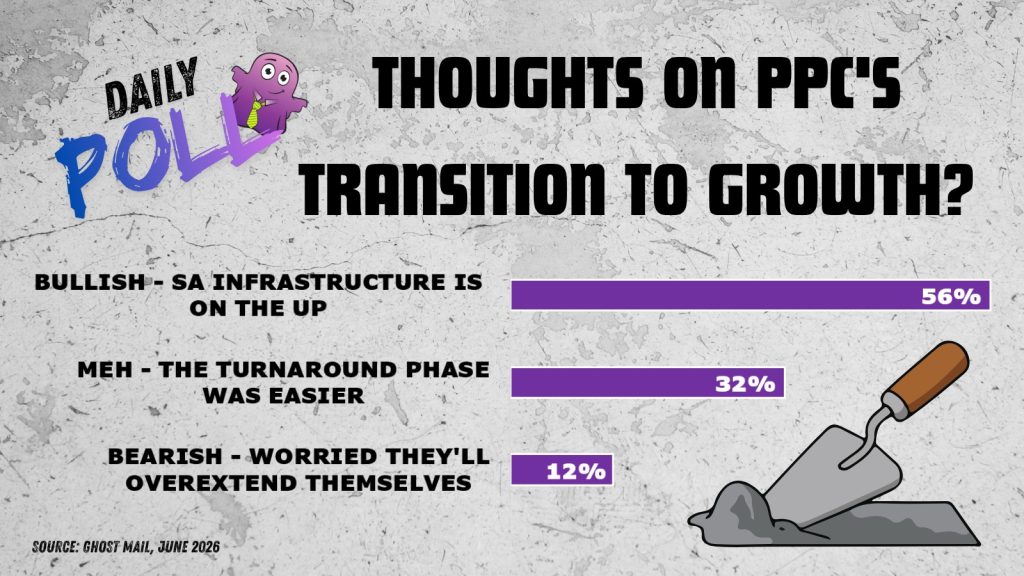

Results of previous poll:

Nibbles:

- Director dealings:

- The financial director of eMedia Holdings (JSE: EMN) bought shares worth R681k. To add to this bullish signal, a handful of other senior execs also bought shares worth around R750k in aggregate.

- An associate of a director of Kumba Iron Ore (JSE: KIO) sold shares worth R85k.

- It’s hardly worth mentioning, but an associate of a director of Finbond (JSE: FGL) bought shares worth R734. And no, there isn’t a “k” missing on the end.

- Brikor (JSE: BIK) released a trading statement dealing with the results for the year ended February 2026. They’ve swung into a loss-making position, with a headline loss per share of between 1.0 cents and 1.2 cents vs. positive HEPS of 0.5 cents in the prior period.

- Wendy Luhabe will resign as the Chairperson of the Pepkor (JSE: PPH) board, a position she has held since December 2020. Ian Kirk (the Lead Independent Director) will serve as the Chairperson until a replacement is named.

- I’m not close to the details on this one at all, but those of you closely following Eastern Platinum (JSE: EPS) will be interested to learn that the Supreme Court of British Columbia has struck out all three claims against the company being made by a particular entity.

Please can you include year performance of JSE all share and top 40 every week

The best place to get indicators is probably Moneyweb – I use their daily indicators page and suggest you do the same!