In this edition of Ghost Bites:

- African Media Entertainment is growing in a difficult market

- Aspen is considering share buybacks

- Delta Property Fund is making progress

- Dis-Chem’s valuation makes it a sitting duck

- Nampak was dragged down by the Diversified South Africa business

- At Remgro, Mediclinic is enjoying the benefits of operating and financial leverage

- The SPAR catastrophe continues

African Media Entertainment is growing in a difficult market (JSE: AME)

Radio still has a place out there

Media could well be the toughest game of them all, yet radio remains an appealing option for advertisers. Even with all the streaming options out there (including in our cars these days), people still enjoy local content and presenters.

At first blush, revenue growth of an impressive 14% at African Media Entertainment suggests that radio is doing far more than just putting in a defensive performance. But we need to dig deeper into the segmentals for the real story.

As it turns out, radio broadcasting revenue actually fell by 5% to R206 million. The revenue growth came from the media services business instead, where it jumped from R103 million to R162 million.

The profitability story deviates completely from the revenue trajectory. Radio broadcasting improved its profits from R84 million to R106 million, while the loss in media services worsened from -R1.8 million to -R13.9 million.

Some of this may just come down to internal transfer pricing decisions, as the group is highly vertically integrated.

As an aside, it’s nice to see that Moneyweb has returned to profitability. South Africa needs the better quality financial media houses to survive. Moneyweb is one such example.

Finally, at group level, HEPS was up 17.8% and the divided increased by 11.1%. That’s a good outcome!

Ghost Bite: As I already know from my podcasts, there’s plenty of interest in the authenticity of audio media. Long may that last.

Aspen is considering share buybacks (JSE: APN)

The share price is now 60% higher than the 52-week low

Aspen has completed its exit from Aspen APAC, locking in net proceeds of R27 billion in the process. Thanks to the forex eventually being more favourable than the estimate in the circular, this is higher than the R25 billion that shareholders were expecting.

Not only will these proceeds be used to reduce debt, but also potential share buybacks. Aspen has noted an intention to take advantage of a share price that the board believes is undervalued.

In response, the share price jumped by 7.4%.

Ghost Bite: Capital management doesn’t need to be rocket science. The market loves share buybacks. Chances are good that if you use them, you’re going to be shown some love by investors.

Delta Property Fund is making progress (JSE: DLT)

But they must travel a long, treacherous road

Delta Property Fund is slowly climbing out of a deep, dark hole. Each handful of dirt along the way is a slog of note, with the loan-to-value ratio at the fund improving from 59.5% to 56.7% in the year ended February 2026.

Remember, most funds are operating in a range of 30% to 35%. A ratio of 40% would be considered high. Upper 50s is wild.

This is one of the reasons why the stock is trading at just R0.33 per share despite the net asset value per share being R3.60 (up from R3.40 a year ago). For speculators (and perhaps even value investors looking to add some risk exposure to their portfolio), Delta is becoming more interesting.

One of the biggest issues is that the underlying tenant base is heavily skewed towards the public sector. Government doesn’t always play fair when it comes to leases. Still, Delta managed to increase rental income by 0.9% in this period despite disposals of underlying properties.

Sadly, property operating costs are under immense pressure, driving a 6.4% decline in net operating income. They are doing the best they can in reducing administrative expenses at head office, but there’s not much they can do about utilities, maintenance and other costs.

To show you how sharp this knife’s edge is, the fund generated R591.7 million from operations and had to spend R408 million on finance costs and R103.1 million on debt amortisation payments. That doesn’t exactly leave much fat for capex, let alone returns to shareholders.

They are working hard for their bankers right now. But with a portfolio vacancy rate of 27.3% (better than 31.9% a year ago), there’s plenty of theoretical upside here for shareholders. Unlocking it is much easier said than done.

Ghost Bite: The very last thing they needed at Delta was an increase in local interest rates. There’s a long road ahead for management and shareholders. I don’t think dividends will be a feature of this story for at least the next couple of years.

Dis-Chem’s valuation makes it a sitting duck (JSE: DCP)

Frivolous divisional names and poorly behaved founding family members also don’t help

Dis-Chem has been receiving terrible press recently after a member of the founding family commited PR suicide on X by tackling Redi Tlhabi over Palestine. Regardless of your political views, wading into this kind of mess when your name is synonymous with a large business just isn’t very clever.

I’ve seen enough online “outrage” and “boycotts” in my life to know that these things rarely translate into a sustained negative impact at the tills, but it’s still a good reminder that founding families need to be careful of their public image. Perhaps the best global example is Musk and how his approach has alienated many potential Tesla customers!

Online fights aside, we now have fresh numbers to work with for Dis-Chem. The company released results for the year ended 28 February 2026. With the share price down 7.8% on the day, the market clearly didn’t like something about them.

We don’t have to look too hard to find the issue. Despite revenue being up 9.3% (with 5.3% from comparable stores and the rest from new stores), HEPS fell by 17.3%. The total dividend per share was down by a similar percentage. If you strip out a once-off property gain in the prior period, HEPS fell by 11.7%.

They’ve invested heavily in the ridiculously named “X, bigly labs” part of the business. Other than giving employees a highly embarrassing name to include on their LinkedIn profiles, this part of the business promises to deliver improvements based on big data and other buzzwords.

Don’t underestimate this – data really is the lifeblood of modern retail. It’s costing a lot of money though, with Dis-Chem throwing R330 million at this project (and Dis-Chem Life) during the year. They expect to see net positive returns in FY27, although it’s quite hard to accurately measure the incremental benefit of something like data.

They also spent R115 million to retire the benefit points program and launch Better Rewards. The group has seen an uptick in revenue since the launch.

If you’re willing to reverse out the aforementioned “investment in the ecosystem” and other non-recurring items, then profit before tax was up 20.1%. I think the negative market response tells us exactly how willing investors are to ignore these costs. I would just see them as a cost of doing business in the modern era.

To be fair, accounting rules are not accurately capturing the modern concept of capex. If Dis-Chem invests in a distribution centre or store fittings, they will capitalise this spend and depreciate it over time. But if they build out a data team, it hits the income statement immediately.

The highlight of the update is actually quite a long way down in the SENS announcement. Like-for-like retail sales were 5.3%, while like-for-like payroll costs came in 3.5% higher. This is genuine store-level operating leverage.

Another highlight is wholesale revenue, up 13.1% as Dis-Chem put in a strong performance across the supply to corporate-owned stores and The Local Choice pharmacies. I have now switched from a large Clicks to a small The Local Choice for all my pharmacy needs, and it’s a vastly better experience in my opinion. There really is something to be said for smaller, community pharmacies.

Ghost Bite: On a Price/Earnings multiple of 30.7x, Dis-Chem has little room for error. My concerns relate less to Saltzman family members making bad choices on social media and more to the lofty expectations baked into the share price. Clicks (JSE: CLS) is down 38% over 12 months and is now on a P/E of 16.6x. Sentiment is a fickle thing and Dis-Chem isn’t immune to a similar shift in market opinion.

Nampak was dragged down by the Diversified South Africa business (JSE: NPK)

Beverage Angola did the heavy lifting

Nampak has released results for the six months to March 2026. They aren’t great, with revenue down 1% and normalised EBITDA down 6%. At least there was a 33% decline in net finance costs, so normalised HEPS increased by 9%.

I must note that the reported numbers (i.e. not normalised) are very different, with HEPS down by 40%. There are some major sources of distortion in this number though, like a large COVID insurance claim in the base period and production line relocation costs in this period. The normalised number is a better indication of the real performance, although it’s always a good idea to keep an eye on the once-off items.

The segmentals tell the story, as Diversified South Africa had serious struggles across both seasonal and structural declines in demand. There were also disruptions from customer pack size changes and other issues. Revenue was down by a hideous 18% in this segment, with EBITDA down 44%.

In contrast, Beverage South Africa saw revenue and EBITDA increase by 5% and 4% respectively. But the real superstar was Beverage Angola, with revenue up 30% and normalised EBITDA up 28% (both in ZAR). The local currency performance was even better, with the currency representing an 8% headwind.

The group cash story has improved significantly, with net cash generated from operating activities of R256 million vs. R82 million in the prior period. This helped them reduce net debt (excluding leases) from R3.1 billion to R2.2 billion, a really important step given the current trend in interest rates.

There is no interim dividend. The company has indicated that they are focused on resuming dividends from the end of the year, subject to performance.

Ghost Bite: Nampak’s share price is up 185% over 3 years, yet it is flat over the past 12 months. Don’t let that fool you though – the volatility has been immense, with a 52-week high of R570 and a 52-week low of R420. If you enjoy trading, then this is a chart that delivers plenty of action.

At Remgro, Mediclinic is enjoying the benefits of operating and financial leverage (JSE: REM)

The focus must be on the Southern Africa business

Remgro and MSC acquired Mediclinic back in 2023. To their credit, they’ve kept the market informed on the underlying performance at Mediclinic, instead of just rolling it into the broader Remgro group and reporting it as part of other segments.

Remgro is in the process of swapping the international Mediclinic exposure for local exposure. This elegant deal would give Remgro full ownership of Mediclinic Southern Africa, while MSC would take full ownership of Hirslanden. Perhaps just to keep the negotiations friendly and to avoid putting billionaire noses out of joint, the two businesses were both valued at $950 million.

From a Remgro perspective, this means that the divisions have been reclassified from an accounting perspective, triggering an impairment of $555 million on Hirslanden.

If we dig into Southern Africa, which is the piece that Remgro shareholders should care about, adjusted revenue growth was 12% and adjusted EBITDA was up by 14% (both in USD). In ZAR, which makes the most sense, revenue was up 7% and adjusted EBITDA increased by 8%.

Thanks to the leverage inherent in the bridge from EBITDA to operating profit (depreciation decreased by 3%), the increase in adjusted operating profit was 16% in ZAR.

With net finance costs down by 4% (a further source of leverage), adjusted earnings were up by 25%.

This result was driven by a 1.8% increase in paid patient days and a 4.7% increase in average revenue per bed per day. Growth in these metrics at the top of the income statement does wonderful things by the time you reach the bottom.

Ghost Bite: Remgro’s decision to focus on local assets is yet another example of how sentiment has swung in favour of local capital being put into local operations. The days of being offshore merely for the sake of it are over.

The SPAR catastrophe continues (JSE: SPP)

The share price closed nearly 15% lower on Friday

SPAR management needs to start telling a credible story to the market about a recovery in the stock. The way to build trust is not by releasing a trading statement that required a key metric to be corrected later in the day. Alas, bad proofreading really is the least of the problems in SPAR’s investment case, with the share price now on life support.

For the 26 weeks to 27 March 2026, group revenue growth was just 2.1%. Southern Africa could only manage 1.7%, while Ireland did 3.4% in rand terms (and 2.2% in local currency).

The weak revenue performance was accompanied by a decline of between 20 and 40 basis points in gross margin in Southern Africa. SPAR is a wholesaler, so that’s a significant move off a structurally lower base than you’ll find in the other grocery retailers on the JSE.

Operating profit was down “substantially” vs. the prior period for Southern Africa. Yikes! In Ireland, gross profit and operating profit margins were slightly ahead of the prior period. This is a small consolation prize.

The tepid revenue growth and the pressure on margins is a terrible combination. Group HEPS from continuing operations plummeted by between 50% and 60% for the period. It really is a disaster.

If we dig deeper into Southern Africa, we find Grocery & Liquor with 1.1% growth. That’s a modest acceleration from the 0.8% in the 18 weeks to 30 January 2026. Volumes went backwards, as evidenced by SPAR describing this growth as being below internal selling price inflation.

Retailer loyalty is a key measure, as this metric tells us the extent to which independent retailers are buying from the wholesaler. Describing retailer loyalty as “holding up” isn’t the most helpful disclosure. In a turnaround, the market wants precise numbers as often and as early as possible. The good news is that loyalty in KZN improved year-on-year (again, no numbers given at this stage).

The highlight (by far) is SPAR Health, which grew 26.1% for the 26-week period. They are coming off a small base here, but at least they are growing.

Another positive is Build it, which swung from a 2.3% decline in sales for the 18 weeks to 30 January 2026 to a 1.3% increase for the 26 weeks to 27 March 2026. In other words, they had a very good February and March.

I get extremely concerned when I see things like Black Friday described as a trading anomaly for margins. Yes, stores need to be more promotional and suffer a margin decline over this period, but you can’t stubbornly sit back and do nothing while competing chains offer amazing specials. How will that improve retailer loyalty, if independent retailers aren’t given the tools they need to compete?

If SPAR’s wholesale business was actually working, they would be able to participate in Black Friday in a way that makes economic sense. You cannot fix a retail business by pulling back from key consumer events.

Another worry is the underlying store health. Debtor impairments were up, as were overdue balances. Remember, the debtor in this case is the independent retailer buying from the wholesaler. Those store owners are clearly under a lot of pressure.

Overall, it’s just a disaster. The group is desperately in need of a capital markets day where investors can put management through their paces and feel good about the plans here. Instead, there are a few bullet points promising that things will get better, followed by a caution about rising fuel costs and what that will mean for logistics costs.

Ghost Bite: Detailed results are due for release on 10 June 2026. With the share price closing nearly 15% lower on the day of this trading statement, the market is angry. I hope management will bring their hard hats to the presentation.

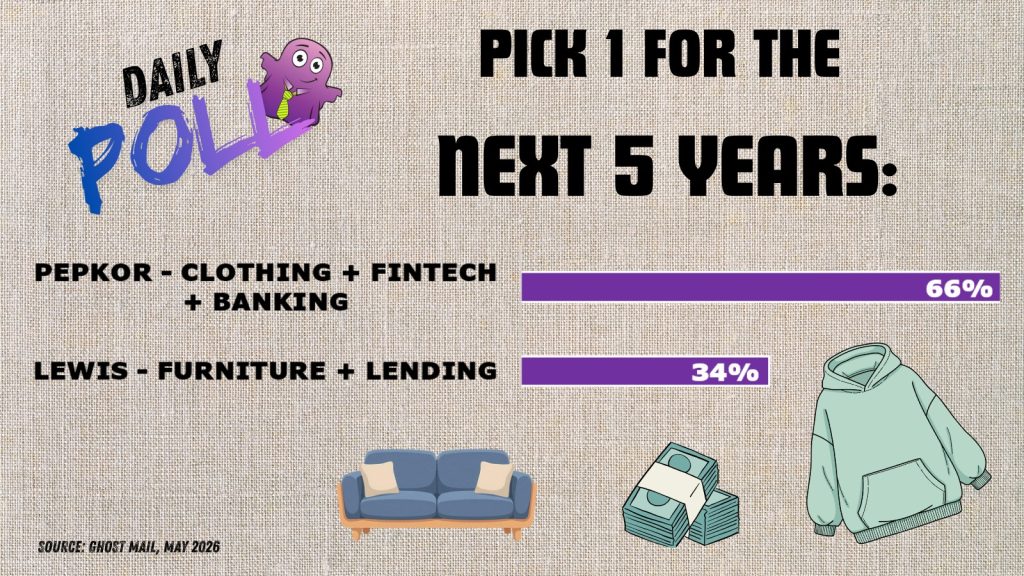

Results from previous poll:

Nibbles:

- Director dealings:

- A director of Harmony Gold (JSE: HAR) sold shares worth R852k.

- I don’t think this has any information value at all for the Shoprite (JSE: SHP) share price, but I still like to include Wiese family transactions as a reminder of what legacy wealth really looks like. The total return swap between family entities has been extended by a week to 8th June. The far more interesting part is that the swap is over shares worth R427.5 million! That’s a big number.

- Orion Minerals (JSE: ORN) has completed the conversion of the IDC loan facility into equity in the subsidiary that holds the Prieska Project. The IDC now has an effective interest of 16.7% in that subsidiary. Separately, Orion has issued the securities for $5.3 million of the latest capital raise, with the remaining $10.1 million expected to be issued shortly.

- Insimbi Industrial (JSE: ISB) released results for the year ended February 2026. Although revenue was up 6% and operating profit increased by 86%, they were still in a net loss position of R22 million (admittedly much better than the net loss in the prior period of R110.5 million). The real problem lies in the cash flow, as net cash from operating activities has swung from an inflow of R61.5 million to an outflow of -R33.9 million. They are operating in a very tough market that doesn’t exactly support the narrative of improving conditions in the local economy. To try to mitigate the pain, operating expenses have been reduced to pre-COVID levels.

- Huge Group (JSE: HUG) has lost half of its value over 3 years, so they aren’t living up to their name. The market still has close to zero interest in the company’s ongoing efforts to be recognised as an investment holding company. Despite reporting a net asset value per share as at February 2026 of around R9.45, the share price is languishing at R1.30. As I’ve said before, as long as they value its preference shares in Huge Connect based on a required rate of return of only 11.25%, the market will continue to disregard the board’s view on net asset value.

- Mahube Infrastructure (JSE: MHB) released results for the year ended February 2026. You won’t see this terribly often, but the company reported negative revenue of -R1 million! This is because the fair value adjustment on financial assets goes through the revenue line in this renewable energy company. The group has swung from a profit of R34 million to a loss of R21.2 million.

- RH Bophelo (JSE: RHB) has limited liquidity in its stock, so the results get a brief mention down here. The numbers for the year ended February 2026 reflect a 2% increase in the tangible net asset value per ordinary share. Importantly, dividends from the underlying investments jumped from R26.1 million to R83.7 million. I’m not sure that HEPS is the best measure of performance here, but I’ll mention that it dropped by 42%.

- In encouraging news, Nedbank (JSE: NED) announced that credit ratings agency Moody’s has revised the outlook from stable to positive. This reflects improvements to Nedbank’s balance sheet, as well as the broader change in the country’s outlook from stable to positive.

- Putprop (JSE: PPR) has agreed to sell 50% in Mamelodi Square to Exemplar REITail (JSE: EXP) for R148 million. The parties have also done a deal for land in Dobsonville with a value of R20 million. The transactions are interdependent i.e. each sale is conditional upon the other. It makes a lot of sense for Exemplar, as this ties in perfectly with their strategy of being close to townships and busy commuter routes. As for Putprop, they plan to redeploy the capital into other income-producing properties.

- Aimia (JSE: AII) has closed the sale of Giovanni Bozzetto for CAD$268.4 million. Thanks to the historical capital tax losses in the company, there’s no tax on this amount. This is the foundation of Aimia’s transition to becoming a “permanent capital vehicle” under the leadership of Rhys Summerton. But the first thing they need to do is offer to repurchase all the outstanding senior unsecured notes, a transaction triggered by the sale of more than 50% of the company’s assets. The aggregate principal amount is $142.6 million. Once the dust settles and the size of the war chest becomes clear, the market will keep a close eye on what Summerton does next.

- Labat Africa (JSE: LAB) has appointed Thembelani Mbolekwana as an independent non-executive director of the company. Labat has been doing some weird things lately, so bringing in an experienced director to be the chairperson of the Audit and Risk Committee is a good step. I still wouldn’t touch this thing at the moment though, as I literally have no idea what they are actually trying to build.

- Visual International (JSE: VIS) has been granted an extension until June 10th to post the circular related to the RAL Trust transaction.

- In the unlikely event that you are waiting with bated breath for Oando (JSE: OAO) to release its results, be aware that they are intended to release the 2025 audited financial statements before June 12th. The Q1 2026 numbers should follow by June 30th.