In this edition of Ghost Bites:

- Several SA banks enjoy a ratings upgrade from Fitch

- Another potential bidder emerges for Mantengu’s Blue Ridge Platinum

- Anticlimax: PKMI’s bid for MAS shares

- Oando: a vertically integrated energy company that nobody talks about

- Get the Nibbles (including director dealings)

Several SA banks enjoy a ratings upgrade from Fitch (JSE: ABG | JSE: FSR | JSE: INV | JSE: NED | JSE: SBK)

When the sovereign story improves, borrowing gets cheaper for the banking sector

South Africa still has a “junk” or speculative rating from Fitch, but at least things have been moving in the right direction. Fitch recently upgraded our sovereign debt from BB- to BB with a stable outlook.

Why does that matter? Well, apart from driving the cost of borrowing for the country as a whole, it also impacts the cost of borrowing for our corporates.

A South African corporate can have a very good rating by South African standards, but that’s exactly the point: it’s always relative to the sovereign rating. This is especially true for our banks, who have significant exposure to the government and broader economy.

Most of our local banks have all been upgraded from AA+(zaf) to AAA(zaf) by Fitch, with the part in brackets reminding investors that this is a South African debt rating. In other words, this isn’t directly comparable to an international AAA rating.

This should improve the cost of funding for Absa, FirstRand, Investec, Nedbank and Standard Bank, allowing them to be more competitive with their lending terms without sacrificing margin. I couldn’t find anything for Capitec (JSE: CPI) from Fitch, but S&P recently gave that bank an equivalent upgrade anyway.

Ghost Bite: Fiscal policy directly affects the cost of funding for our banks, which in turn impacts the availability and cost of credit for all South Africans. This is one of many reasons why government must always be held accountable for its actions!

Another potential bidder emerges for Mantengu’s Blue Ridge Platinum (JSE: MTU)

But the current potential buyer has an exclusivity in negotiations

Mantengu is in the process of negotiating a potential disposal of Blue Ridge Platinum to Afresources Mining. The ultimate controlling shareholders in that company are not related parties to Mantengu.

Some competitive tension has entered the chat, with an unsolicited offer coming in from a different party at a price that is higher than the Afresources indicative offer. We just don’t know how much higher, as there are no further details in the SENS announcement.

The challenge is that Mantengu had granted an exclusivity to Afresources, so they actually can’t engage on this other offer. This is precisely why buyers ask for exclusivity, and why sellers only grant it under rare circumstances. The removal of flexibility for one party in favour of the other is a key principle in any negotiation.

Will the Afresources offer get over the line? Or will those negotiations fall over, paving the way for this other deal to be negotiated? Keep in mind that even if Afresources doesn’t end up being the buyer, there’s no guarantee that the negotiations with the mystery buyer will be successful.

Ghost Bites: Welcome to the colourful world of corporate finance dealmaking. If this stuff was easy, then M&A specialists wouldn’t make nearly as much money as they do!

Anticlimax: PKMI’s bid for MAS shares (JSE: MAS)

Despite receiving many offers from MAS shareholders, PKMI didn’t acquire any further shares in the end

At the end of June, PKMI announced a bid to acquire up to 30 million MAS shares. It’s worth keeping in mind that the strategy at MAS has shifted fundamentally, with the company no longer focusing purely on property assets. In PKMI’s announcement of the bid, part of the rationale was that MAS shareholders would be given a potential liquidity event if the new strategy doesn’t align with their needs.

Well, so much for that liquidity…despite there being “strong participation” in the bid and selling offers more than twice the bid size (i.e. holders of more than 60 million MAS shares were willing to sell), PKMI elected not to buy any shares at all.

This is because PKMI wasn’t happy with the pricing that shareholders wanted. This means that no clearing price could be established under the bid, so the entire thing falls over. There’s no indication of what a suitable clearing price would’ve been. We also don’t know what prices were indicated by shareholders who wanted to sell.

Ghost Bite: The MAS share price is back to where it started this year, having plummeted during the conflict in Iran. It has been a difficult, sideways story overall.

Oando: a vertically integrated energy company that nobody talks about (JSE: OAO)

Will liquidity in this stock increase over time?

Nigerian energy group Oando has finally caught up on its financials, thanks to the release of results for the year ended December 2025.

This is a vertically integrated energy company, so you’ll see many metrics that you aren’t used to seeing. This includes Barrel of Oil Equivalent Per Day (boepd). Group boepd increased by 32% year-on-year, driven by higher output across crude oil, gas and natural gas liquids (NGL). The full-year impact of the Nigerian Agip Oil Company joint venture consolidation has also been a positive contributor.

As you would expect, an energy company like this has a trading business designed to give them a smoother earnings profile across cycles. Crude oil traded volumes were up by 24%. It will be far more interesting to see how that business performed in the first half of 2026 based on all the chaos in global oil markets!

Trading volumes were down overall though, as the group changed its trading portfolio and got out of certain areas. Short-term pain for long-term gain, hopefully.

The production numbers sound exciting, but those volumes are just one part of the equation. Group revenue actually fell by 22.2% year-on-year, with the trading division driving the biggest decline.

Despite a decline in administrative expenses of 27.2%, operating profit was down by a nasty 58% in FY25.

Thanks to net finance costs decreasing by 43.4%, profit after tax only decreased by 7%. It certainly could’ve been worse.

To add to the strange shape of the income statement, earnings per share increased by 28%. Another positive element is that cash from operating activities swung from a substantial outflow to a decent inflow of N32.3 billion (roughly $23 billion at current rates).

For 2026, which is now halfway done already, the group expects production to increase to between 40,000 and 50,000 boepd. That’s a significant increase from 32,482 boepd in FY25. Supporting this strategy is a planned capex programme of between $90 and $100 million.

Ghost Bite: Above all else, I can’t wait to see what the numbers look like for the first half of the year after the conflict in Iran caused a spike in prices.

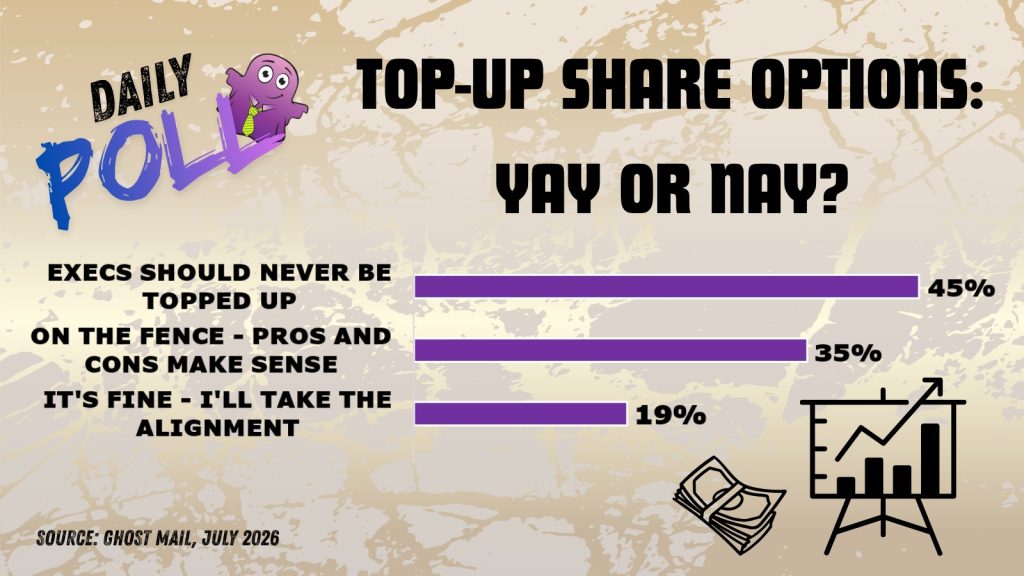

Results of previous poll:

Nibbles:

- Director dealings:

- Here’s a strong bullish signal: the CEO of Clicks (JSE: CKS) bought shares worth almost R4.7 million. A different director also recently purchased shares. It’s worth noting that Clicks is down 29% year-to-date, so this gives some much-needed love to the bull case.

- Two of the founding directors of Dis-Chem (JSE: DCP) sold share awards worth R3.26 million. The announcement doesn’t explicitly say that this was the taxable portion.

- A director of a major subsidiary of 4Sight Holdings (JSE: 4SI) received shares in the company worth R989k. This relates to the previous acquisition of that subsidiary and the related participation of senior managers in the company’s stock awards.

- A family entity linked to the CEO of Spear REIT (JSE: SEA) sold shares worth R500k. This is a broader restructuring need for other family members, rather than a reflection of the CEO’s personal view on the stock. Aside from the SENS being explicit on this, he also reached out to make sure I understood this nuance! I always appreciate engagement from top execs.

- An associate of the CEO of Finbond (JSE: FGL) bought shares worth R446k. Separately, an associate of a non-executive director bought shares worth R390k.

- Acting through Titan Premier Investments, the Wiese family bought shares in Collins Property Group (JSE: CPP) worth R246k.

- A director of Trematon (JSE: TMT) bought shares worth R95k.

- Hulamin (JSE: HLM) announced that the Chairperson of the Board, Paul Baloyi, will no longer hold that office with effect from 6 July 2026 (i.e. immediately). If I understand the announcement correctly, he was removed by the board – a spicy and very unusual thing to happen. Linda Yanta has been appointed to the role on an interim basis. One wonders what has transpired here?