In this edition of Ghost Bites:

- Accelerate Property Fund has suffered a setback on its turnaround journey.

- Deneb has flagged a juicy earnings uplift.

- Stefanutti Stocks shows why it has been one of the most rewarding speculative punts on the JSE in recent years.

A bump on Accelerate Property Fund’s road (JSE: APF)

The stock is back where it started a year ago!

Accelerate Property Fund is a rare example of me taking a position on a speculative stock. It’s worked out well so far, thanks to the incredible progress they’ve made in cleaning up the balance sheet and achieving improved metrics at Fourways Mall.

All looked good until the world started to come to terms with oil at $100/barrel (or more). Now, with yields rising and inflation expectations going up, any marginal property funds are under pressure.

To add insult to injury, the disposal of the Bosveld Bela Bela Shopping Centre by Accelerate for R88 million has fallen through due to the purchaser repudiating the agreement.

Accelerate is looking at options to pursue a damages claim. More importantly, they are now engaging with other potential buyers.

Ghost Bite: The perfect hindsight trade was to sell above R0.70 per share. The stock is now back at R0.50. I’m still more than 20% up at these levels, so I’ll sit tight on this one and allow management to continue with their turnaround efforts despite the macroeconomic pressures.

Deneb flags a juicy earnings uplift (JSE: DNB)

I’m looking forward to the details on this one

Deneb Investments has released a trading statement for the year ended March 2026 that looks very encouraging. HEPS is expected to increase by between 47% and 67%, putting it in a range of 36.8 cents to 41.8 cents.

For context, the share price is R2.53. Deneb is a typical example of a local small cap (on the verge of being a mid cap with a R1.1 billion market cap) with a single-digit P/E multiple. One of the reasons for the low multiple is that Hosken Consolidated Investments (JSE: HCI) has 84% of the shares in the company, so that leaves a very thin layer for public trade.

A lack of liquidity makes it almost impossible for institutional investors to get involved directly in Deneb, so they focus on HCI as an entry point into the group instead.

Ghost Bite: Deneb is interesting, but this is a small part of the HCI empire. A detailed update from the entire group must only be a few days away.

Stefanutti Stocks has richly rewarded punters in recent years (JSE: SSK)

The latest trading statement shows how much things have improved

Stefanutti Stocks has seen its share price skyrocket by 555% in the past three years. They are up 64% year-to-date – an astonishing rally in an otherwise risk-off environment for many risky stocks.

This is a perfect example of why many investors are willing to make a small allocation to turnaround stories and highly speculative plays. When they go well, they more than make up for a few that didn’t! It’s a bit like a venture capital portfolio.

For Stefanutti Stocks, one of the huge wins has been the settlement with Eskom regarding the Kusile Power Project. Net of costs and tax, Stefanutti Stocks received R492 million from Eskom! When you consider that the group market cap is under R1.4 billion, you can see how the prospect of a settlement was a big part of the bull case when the share price was in the doldrums.

The group has also made progress on other corporate actions. These include the disposals of SS-Construcoes (Mocambique) Limitada and Stefanutti Stocks Construction Limited with effect from 12 December 2025. This is why the results for the year ended 28 February 2026 will include continuing and discontinued operations.

Drumroll please… we now arrive at the latest numbers in the trading statement for that period.

For continuing operations, HEPS jumped by between 195% and 215% to a profit of between 369.13 cents and 394.16 cents. For total operations, HEPS was up by between 220% and 240% to between 349.95 cents and 371.82 cents.

Whichever way you cut it, profits have tripled in the past year. This explains the share price move, with the stock currently trading at R7.20.

Be careful of jumping at what looks like a P/E multiple of 2x, as the settlement with Eskom is a non-recurring item that you would want to strip out in assessing the earnings multiple.

Detailed results are expected on 26 May.

Ghost Bite: These trades always look incredible in hindsight. When playing in speculative stocks, it is absolutely critical to spread the risk! I really wasn’t joking in the comparison to venture capital investing, where such investors take many small positions and hope that at least a handful will work out.

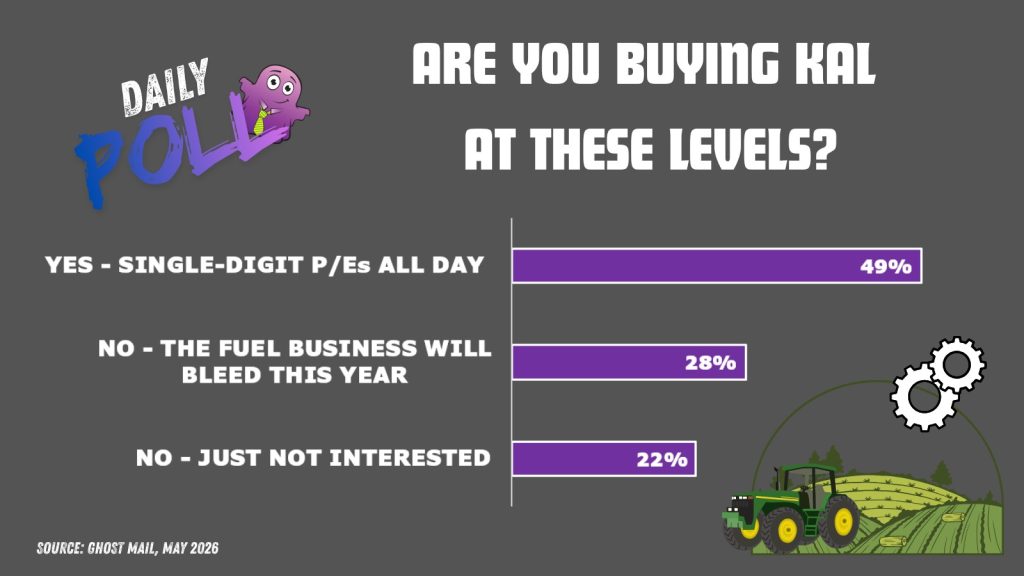

Results of previous poll:

Nibbles:

- Director dealings:

- The CEO of Pan African Resources (JSE: PAN) has unwound a collar structure and sold shares worth R86 million that were pledged as security for a loan. This leaves him with shares worth just over R100 million across his direct and indirect interests.

- The chairman of Shaftesbury Capital (JSE: SHC) bought shares worth £129k.

- The recently appointed CEO of KAL Group (JSE: KAL) bought shares worth R505k.

- The spouse of a director of Cell C (JSE: CCD) bought shares worth R15.2k.

- As a reminder of how deep the debt capital markets are on the JSE, Valterra Platinum (JSE: VAL) has concluded its inaugural auction under the R10 billion Domestic Medium Term Note Programme. It references the ZARONIA rate, which always makes me think of a fictional location in a kids movie! There are various tranches in the auction of R2 billion in notes, with maturity dates from one year to five years. Naturally, the longer-dated debt becomes more expensive. This is the “curve” that people refer to in fixed income investing.

- Eastern Platinum (JSE: JSE) is a rather tricky name on the JSE. There’s very little liquidity in the stock. More importantly, the auditors have been flagging going concern risks for as long as I can remember. In the latest numbers for the first quarter ended March 2026, current liabilities are more than double current assets! Even at current PGM prices, the group was only slightly profitable at mine operating income level. The group is still reporting losses overall. It all comes down to the ramp-up at the Crocodile River Mine, with the biggest concern being that they were below target on run-of-mine tonnages at that mine.

- Newpark REIT (JSE: NRL) has no liquidity in its stock whatsoever. This is rather ironic, as the building occupied by the JSE is one of just three properties in this company’s portfolio! I’ll give the numbers for the year ended 28 February 2026 a passing mention down here, with funds from operations down by a nasty 36.1% and the dividend following suit. The positive is that the loan-to-value ratio has improved significantly, from 43.1% to 37.7%. The company has taken quite a knock from the revised rental agreement with the JSE. The vacancy rate at the adjoining 24 Central building is material though, so there’s room for upside. I used to work in Sandton many years ago and I have such fond memories of that building!

- Look outside quickly and check if it’s going to snow – the suspension of trading in Salungano Group (JSE: SLG) shares has been lifted at last! We were coming up for the three-year anniversary of that suspension in August this year. The company has now fully caught up on its financial reporting.

- There are always a few repurchase programmes in progress on the JSE, but one that hasn’t been given much attention is Tsogo Sun (JSE: TSG). Between 23 March 2026 and 14 May 2026, they’ve repurchased 6.94% of shares in issue! The average price paid is R6.962 per share. The current share price is R6.95. Together with other recent repurchases, they’ve bought back shares representing 8.06% of shares that were in issue at the end of August 2025 when the authority to repurchase shares was obtained at the AGM.

- Here’s something you won’t read every day: the AGM for SAB Zenzele Kabili (JSE: SZK) at the Johannesburg ExpoCentre (Nasrec) was suspended for safety concerns. The announcement doesn’t go into any further details on what happened.