Balwin: the complexities of moving beyond the building of complexes (JSE: BWN)

There are a number of distortions in the numbers

Balwin has released results for the year ended February 2026. Although revenue was up by an impressive 21% at the property developer, profit was only 9% higher. And by the time we reach HEPS, the increase was just 4%!

Just to confuse investors, the jump in recurring HEPS was 41%.

Seeing such a big difference between HEPS (a regulated calculation) and recurring HEPS (a concept that management decides on) is always tricky for investors. In this case, it looks like the timing of land sale transactions and fair value adjustments to investment property are to blame for the difference.

With Balwin building and holding properties for rental (they have investment property of R506.9 million), I don’t think investors can easily ignore these fair value movements. After all, they are a component of the long-term returns when you decide to hold property!

At least sanity prevailed in whatever Balwin was planning to do with “in-house educational facilities” – I really hope that doesn’t mean that they were thinking of building schools or anything along those lines. Balwin needs to focus with their capital, not create new distractions.

Here’s the metric that investors actually care about: a 22% increase in apartment sales. Balwin Annuity also generated growth in revenue of 25%, contributing 8.1% to group revenue and providing a decent underpin to the results.

Sadly, group gross margin fell from 30% to 27%. Margin on apartments was steady at around 24%, so the decline was driven by the disposal of land parcels in the current and prior year.

Cash generated from operations was a much healthier R198.7 million vs. cash used of R211.5 million in the comparable period. Notably, the loan-to-value ratio improved from 40.4% to 38.1%. Given the need to manage the debt carefully, Balwin hasn’t declared a dividend.

The share price is up by over 70% in the past year, with shareholders looking through the noise and buying the company on a modest P/E.

Boxer is firmly in the winners camp in the grocery market (JSE: BOX)

They’ve made an important point about growth in the upcoming period

Boxer closed 7.7% higher after releasing results for the 52 weeks ended 1 March 2026. The market clearly loved them.

Pick n Pay (JSE: PIK) closed 9% higher, with the market celebrating the look-through exposure in that broken retail story (keep in mind that Pick n Pay has the controlling stake in Boxer).

I’ll just say it again: if Pick n Pay sells more of the Boxer stake to fund its own losses in years to come, then buying Pick n Pay because you like Boxer is about as useful as brushing your teeth with Coke instead of water. I get the play on sum-of-the-parts and all the other arguments, but management is in control of those parts, not you.

Focusing on Boxer, where we have fresh results, we find turnover growth of 9.6% and an increase in trading profit of 14.3%. Trading profit margin expanded from 5.4% to 5.7%. A 30 basis points uplift is meaningful in a business like this!

HEPS unfortunately continues to be impacted by the IPO structure, which led to a vast increase in the number of shares in issue in late 2024. If we just look at headline earnings instead, the increase was 13.2%. In a grocery market where the winners are detaching themselves from the losers, Boxer is clearly a winner.

Perhaps most impressively, the 4.5% like-for-like growth was achieved despite internal selling price deflation of 1.2%. This means that they achieved strong growth in volumes in the existing stores.

They are also expanding rapidly, with 51 net new stores taking the total footprint to 576 stores. With a return on invested capital (ROIC) of 26%, shareholders won’t be unhappy with Boxer following an expansion programme with the 60% of headline earnings that doesn’t get paid out as a cash dividend.

The next financial year will finally be a “clean” period in which all of the IPO distortions would’ve been worked out of the system. Unfortunately, it’s also a period in which the effect of the energy price spike will be felt by consumer businesses.

Boxer has already signalled caution here, noting that growth in the first 9 weeks of the new financial year is slower than they saw towards the end of FY26. Inflation is going to be a feature of the current period.

What is your view on the Pick n Pay value-unlock trade?

Prosus offloads another 5% in Delivery Hero (JSE: PRX | JSE: NPN)

This is part of the commitments made to the European Commission

When the European Commission approved the acquisition by Prosus of Just Eat Takeaway.com, the condition attached to the deal was that Prosus must significantly reduce its shareholding in Delivery Hero. And yes, even the regulator was vague about exactly what that means.

You may recall that Prosus sold 4.5% in Delivery Hero to Uber last month. They’ve now sold another 5% in the company to Aspex Management. The price on this deal is €22 per share, representing a 22% premium to the 30-day VWAP. In case you’re wondering, it’s also better than the €20 per share they got from Uber!

This latest sale unlocks €335 million for Prosus. Together with the disposal to Uber, they’ve turned around €605 million into cash.

Although they aren’t explicit on this in the latest announcement for some reason, it looks like the stake in Delivery Hero is down to roughly 16.8% in the company.

A mixed bag at Raubex: Bauba Resources in the green, but Australia deep in the red (JSE: RBX)

They need to simplify the earnings profile of this group

This won’t exactly go down as a blockbuster period for Raubex. In the year ended 28 February 2026, revenue was up by 4.6% and HEPS increased by just 1.9%. The numbers are going the right way, but not by much.

There’s a significant divergence in the cash vs. profits story. Although operating profit increased by 11.6%, cash generated from operations fell by a significant 30.3%. When you see something like this, you need to go digging into the working capital to see where the money is getting tied up.

In this case, every line in working capital is to blame.

Trade receivables jumped by 17.2% despite such a modest increase in revenue, with average collection days increasing from 38 days to 43 days (a concerning trend). Inventory was 36% higher due to increased ore levels at Bauba Resources. To compound the pressure, we find that trade payables decreased by 10.2%, which means that suppliers were paid faster than before.

Together with an increase in borrowings of 20.6% to fund the acquisition of the Axis Group, Raubex needs to be careful with the balance sheet. Cash and cash equivalents of R1.87 billion was 11.4% lower than the comparable period.

Looking at the segmentals, the good news story is undoubtedly the Materials Handling and Mining division. Although revenue was down 3.2%, operating profit increased dramatically from just R4.2 million to R444.9 million. This takes the division to an operating profit margin of 10.8% – a huge improvement. The order book has nearly doubled, so that should support revenue in the period to come.

Within this segment, Bauba Resources (which Raubex should ideally dispose of) drove most of the volatility. Bauba swung from a loss of R235.8 million to profit of R243.7 million! Perhaps they will now find a buyer.

In Construction Materials, revenue was up 8% but operating profit fell by 13.4%. Raubex blames weather conditions in the first two months of the year and the situation in the ferrochrome sector in South Africa. The order book has increased by an encouraging 40.4%.

Roads and Earthworks put in a steady performance, with revenue up 4.9% and operating profit increasing by 4.3%. The order book dipped by 6.7% though, so keep an eye on that.

In the Infrastructure dividend, revenue was up 30.2% and operating profit jumped by a juicy 42.2%. The order book inched higher by 1.6%, so they need to focus on converting that order book as efficiently as possible.

Finally, in Australia, revenue was down 14.4% and there was a hideous negative swing from operating profit of R303.9 million to an operating loss of R60.4 million. There was a loss of R177 million on a single contract for a major mining client! I really have no idea why South African businesses get hurt so consistently by Australia.

The outlook statement is heavy on narrative (two pages of it!) and light on actual numbers. I wish South African management teams were required to give more detailed financial guidance.

A dependable performance at Redefine Properties (JSE: RDF)

That’s exactly what investors are looking for

Redefine Properties released results for the six months to February 2026. With the dividend per share up by 6.9%, the group has done a solid job of delivering what investors are looking for: returns that give protection against inflation.

Another important metric is the NAV per share, up by 4.3% and adding to the return for shareholders.

With the loan-to-value (LTV) ratio at 40.3%, the balance sheet is in the sweet spot of balancing return on equity vs. debt risk. Most REITs want to run at roughly a 40% LTV.

Despite an operating environment that isn’t exactly supportive of decreasing interest rates or less pressure on consumers (factors that would help REITs), Redefine has bravely raised the full-year earnings outlook. Distributable income per share is expected to grow by between 6% and 7%.

The performance in the first half of the year would no doubt have given them some confidence here. Still, the mid-point of the upgraded guidance suggests a tougher second half to the year vs. the first half.

Vodacom’s Egyptian adventure is working – for now at least (JSE: VOD)

Favourable macroeconomics make a big difference to telcos

Vodacom isn’t sitting back and letting MTN (JSE: MTN) get the lion’s share of Africa. Far from it, in fact.

Vodacom is targeting 275 million customers by 2030. They are currently on 237.3 million, having added 26 million in the past year. There’s a long way to go, but Africa is an exciting place that offers these kinds of opportunities (along with an incredible cocktail of macroeconomic and geopolitical risks).

Customer growth helped boost revenue by 12.9% on a normalised basis. Normalised group EBITDA grew by 14.2%, so there was some margin expansion as well.

Unsurprisingly, Egypt was the most exciting growth story. In local currency, revenue was up 36.2% and EBITDA jumped by 44.5%. As I wrote during my recent travels, Vodafone Egypt billboards are everywhere in that country – and the people seem to be on their phones all the time!

We also discussed my trip and the associated insights in this episode of Magic Markets:

Just contrast this to South Africa where revenue growth was only 2.1%. It’s clear that the South African market is far too mature to be an interesting source of growth for investors.

Safaricom sits somewhere in the middle, with local currency revenue growth of 11.5% and EBITDA growth of 27.9%. Ethiopia is still loss-making at present, but customer growth of 54.2% took them a lot closer to breakeven levels.

The other area to highlight is what Vodacom confusingly calls the “International” segment – consisting of Tanzania, DRC, Lesotho and Mozambique. The latter is a struggle at the moment, but the other three countries helped drive service revenue growth of 14.4% and EBITDA growth of 27.8% (in rands).

Financial services remains a major focus area and opportunity for the telcos in Africa. With a 17.4% increase in customers and a 16.6% increase in transaction values, Vodacom isn’t playing around in this space either.

Vodacom’s growth path is confirmed by recent corporate activity.

There was the recent Maziv fibre deal in South Africa that was extremely difficult to get across the line from a regulatory perspective.

And in December, Vodacom agreed to acquire an additional 20% stake in Safaricom, the East African asset focused on Kenya and Ethiopia. The closing of the Safaricom deal is subject to a court process in Kenya.

Investors should feel good about Vodacom reinvesting their capital at the moment. Return on capital employed has jumped from 23.5% to 27.5%. There’s also plenty of cash making its way back to investors, with the dividend up 18.5% for the full year.

The Vodacom share price closed 4.5% higher on the day, so the market liked these numbers.

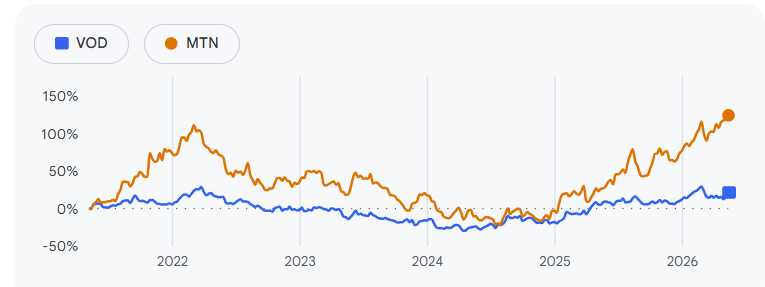

The pandemic and post-pandemic period has been a crazy ride in this sector. There’s an element of the tortoise vs. the hare in this five-year chart of Vodacom vs. MTN:

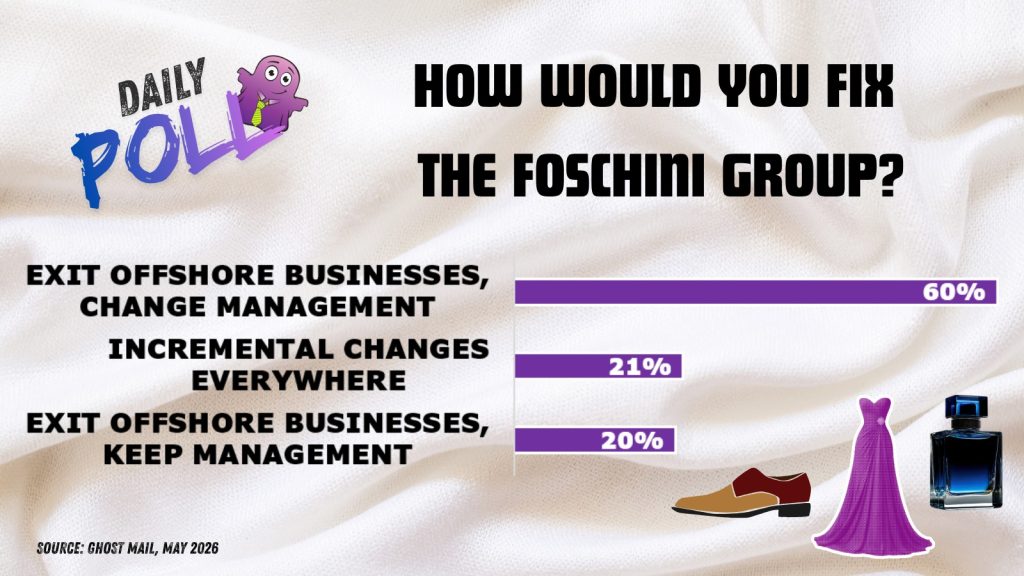

Results of previous poll:

Nibbles:

- Director dealings:

- MTN (JSE: MTN) announced the results of MTN Rwanda for the quarter ended March 2026. They look good, with service revenue up 21.2% and EBITDA increasing by 32.8%. Although capital expenditure only increased by 1.9%, you actually need to separate out the capex excluding leases. On that basis, there was a wild 812.8% increase in capex due to network upgrades, leading to a 6.5% decline in free cash flow!

- Emira Property Fund (JSE: EMI) announced the results of the offer to shareholders in Octodec (JSE: OCT). Through a combination of on-market purchases and the offer itself, Emira now has a 23.5% stake in Octodec. This is a significant minority stake that gives Emira influence (but not control) over the direction that Octodec takes.

- RMB Holdings (JSE: RMH) shareholders aren’t exactly falling over one another to accept the offer by AttBid. At this stage, valid acceptances have only been tendered by holders of 2.87% of shares in issue. This would take the concert parties to 46.52%. The offer is open until 29 May. As I’ve flagged before, shareholders tend to keep their options open until the last minute, so it’s hard to forecast where the final acceptance rates will land.

- ISA Holdings (JSE: ISA) has withdrawn the cautionary announcement related to negotiations with a potential acquirer of a controlling stake in the company. This is exactly why caution was needed in the first place: negotiations often fizzle out.

- Collins Property Group (JSE: CPP) released a trading statement dealing with the year ended February 2026. They expect the distribution per share to be up by between 15% and 20%, comprising a combination of a dividend and a return of capital. Detailed results will be out this week.

- enX Group (JSE: ENX) released a trading statement for the six months to February 2026. The percentage movements aren’t particularly helpful, as the shape of the group has changed dramatically due to asset disposals. But the important point is that revenue in the continuing operations is down by 37%, driven mainly by the timing of lumpy data centre contracts. The continuing operations suffered a headline loss per share of between 2 cents and 4 cents. It will be important to dig into the detailed results once they become available.

- Insimbi Industrial Holdings (JSE: ISB) has released a further trading statement dealing with the year ended February 2026. Although the company is still in a loss-making position, the severity of the losses is diminishing. After reporting a headline loss per share of 6.50 cents in the prior period, they now expect a headline loss per share of between 3.01 cents and 4.07 cents. EBITDA is expected to be at least 45% higher than the R51.1 million in the prior period. Detailed results are expected to be released on 29 May.

- Wesizwe Platinum (JSE: WEZ) has finally released results for the year ended December 2025. There was a massive positive swing in the numbers from a headline loss per share of 12.23 cents (restated) to HEPS of 9.86 cents. They expect to have their new financial systems in place by June, having suffered a cyberattack that led to the suspension of trade in the shares due to the company’s inability to publish financial results. The suspension should be lifted soon after the integrated annual report is published at the end of May.

- Copper 360 (JSE: CPR) has suspended the processing of lower-grade waste material and broken stock at the Rietberg mine. Instead, they will focus their limited resources on underground development activities at the mine over the next few months. This will have an impact on employees at Rietberg, with a labour consultation process having begun. Copper 360 has 12 previously operating mines and 60 identified copper prospects. Perhaps therein lies the problem as much as the opportunity?

- In the latest example of ASP Isotopes (JSE: ISO) using SENS as a PR tool rather than a place for financial updates, they’ve announced that Quantum Leap Energy has entered into a non-binding memorandum of understanding (MOU) with a European nuclear technology company. The great dressing-up of Quantum Leap Energy for its separate listing continues.

Hi. What didn’t the market like about the Prosus CEO letter, that its 7% down.

Thanks so much

Hi – hopefully you saw the answer later in the week. Well, my take on it at least!