In this edition of Ghost Bites:

- The market has gone cold on Prosus, with another drop in the share price after the release of the CEO’s letter

- MTN is the beneficiary of much better macroeconomics in Africa – and the tough story in South Africa confirms how important that is

- Canal+ is inward listing on the JSE in June, but will they find support?

- Bytes Technology has a lot of work to do, with share buybacks giving the market something to smile about.

- In property, MAS is looking to offload some malls, while Spear REIT showed us exactly how profitable a buy-and-flip can be. Octodec’s interim growth needs to be considered carefully.

Bytes finds some support in the market, but it’s not obvious why (JSE: BYI)

Perhaps the share buyback announcement did the trick

With a share price that has shed over 40% of its value in the past 12 months, Bytes Technology needs to find a bottom and then start turning around. The market seemed to like the announcement of results for the year to February 2026, with the share price closing 6.5% higher on the day.

As you will shortly see, the rally is despite the numbers for that period, not because of them.

Revenue was up just 1.6% despite gross invoiced income increasing by 11.5%, so the concerning trajectory in their business model continues. When you are reliant on the crumbs that Microsoft is willing to give you off the edge of the table, it’s a tough place to be.

Gross profit was up by just 2.5%, which wasn’t enough to offset the pressure in expenses. As an example, headcount increased by 6.9% as the company invested in sales and service delivery. This is why operating profit fell by 5.6%.

With HEPS down by 6.1% and a decline in cash conversion rates as a further concern, these numbers were practically devoid of highlights. The increase in the final dividend per share of 1.4% isn’t much of a consolation prize.

So, what did the market like about this update?

One possible explanation is the FY27 outlook, where Bytes is planning to achieve high single-digit to low double-digit growth in gross profit. The anniversary of the Microsoft partner changes is behind them, so they can now grow off their new base.

But even then, the expectation for operating profit is that it will be “broadly flat” due to significant cost pressures. One of the factors highlighted here is a “return to normal bonus levels” – a surprise given the financial performance.

The outlook doesn’t seem great either, does it?

The only other factor that could’ve driven the rally is the announcement of a share buyback programme of up to £25 million. This works out to roughly R550 million vs. a market cap of over R17 billion. It’s helpful, if not a complete game changer.

The other important news is that Andrew Holden will stand down as CFO and be appointed to the newly created role of COO. The company will announce a new CFO in due course.

Ghost Bite: Share buybacks into a depressed market are helpful, but Bytes needs to get costs under control before investors will really climb back in. I personally wouldn’t pay a mid-teens P/E for a “broadly flat” operating profit trajectory.

Canal+ is coming to the JSE (JSE: CNP)

Can they make the MultiChoice acquisition work?

When Canal+ acquired MultiChoice, they promised that they would inward list on the JSE and give South Africans a chance to invest in the story.

I must be honest: most of the headlines I’ve seen since the deal relate to South Africans being very angry about the changes made at DStv, so I’m not sure that the red carpet is going to be rolled out for Canal+’s listing.

Of course, there’s much more to Canal+ than just MultiChoice and its overpriced bouquet of things that people don’t watch anymore. They will need to convince investors of the value of the full portfolio of media assets. This is where things will get interesting for local investors.

With 42 million subscribers and operations in over 70 countries, Canal+ is a serious operation. 18 million of those subscribers are in Europe, so this isn’t just an emerging markets play. But is it a viable competitor to Netflix and the other streamers?

I quite enjoyed this comment in the announcement:

“Due to the Company’s subscription model, its revenues are consistent and predictable.”

Hmmm.

Ghost Bite: The only predictable thing about DStv subscribers is that most of them would cancel if not for the sport. I think Canal+ will have a difficult time convincing South Africans to invest when the listing happens on the 3rd of June. Here’s how Canal+ has performed in London after being spun-off from Vivendi:

MAS is looking to offload some property (JSE: MSP)

There are two potential deals on the table

Here’s an unusual cautionary announcement for you.

MAS Real Estate is in negotiations with two independent parties regarding the disposal of a wholly-owned enclosed mall and six wholly-owned open-air malls. They might do both deals, or one deal, or neither!

This either/or situation is driven by the company’s desire to do at least one transaction to catalyse the value of its property. If the terms aren’t good enough, then they have the flexibility to walk away from both discussions. If the terms are great, they can do both transactions.

Ghost Bite: A combination of (1) balance sheet flexibility and (2) discipline to sell at the right price is an indication of a management team that knows what they are doing from a capital management perspective.

MTN’s convergence of reported and constant currency numbers is a good sign (JSE: MTN)

The African macroeconomic story has stabilised – for now, at least

MTN’s update for the three months to March 2026 features strong growth rates. This isn’t a surprise, as we’ve been kept updated by the release of numbers by each of the underlying subsidiaries in Africa. The latest update simply brings it all together.

With over 312 million customers and operations in 19 markets, MTN is a true giant of the continent. A 5.4% increase in subscribers suggests that the growth journey is far from over.

Voice revenue was up by just 1.3% as reported, or 4.7% on a constant currency basis. Even in many of these frontier markets, the real growth drivers are data revenue and fintech revenue (up 35.4% and 20.0% in constant currency respectively).

Overall, the group achieved service revenue growth of 20.0% as reported, or 21.1% in constant currency. It’s so good to see that the reported numbers aren’t terribly different from the constant currency numbers. This stability in African countries has been a major driver of performance.

EBITDA increased by 27.9% in constant currency, driving a 300 basis points expansion in EBITDA margin to 47.6%.

Notably, fintech transactions increased by 15.8% and their value was up by 32.8%. The growth flywheel in the fintech space is spinning rapidly. This is why MTN is separating out its fintech business in several markets. Aside from giving them more flexibility around ownership and other regulations, this paves the way for MTN to attract strategic partners into the underlying fintech plays.

Another important initiative is the acquisition of IHS, giving MTN more vertical integration as they look to own the infrastructure that they rely on. Being able to do deals like these is good going for a company that was struggling to keep its holding company balance sheet in one piece a few years ago!

Speaking of the balance sheet, the net debt to EBITDA ratio of 0.2x is way below the targeted upper threshold of 1.0x.

No discussion is complete without a quick look at the South African numbers. MTN South Africa’s service revenue was up by just 0.7%, with a drop in voice revenue of 9.6% putting pressure on the numbers. The biggest headache is the prepaid business, where revenue fell by 3.3% year-on-year.

Here’s something that Optasia (JSE: OPA) shareholders should be very careful of: MTN has deliberately scaled back its reliance on XTraTime advances (down 18.3% year-on-year) as they look to “improve the quality and overall health of the base”. Fo with that what you will.

EBITDA fell by a nasty 12.5%, with margin down by 410 basis points to 32.6%. Some of this is due to share-based payments to employees, but the reality is that the South African business is under pressure. If you split out those payments, you’ll still find an EBITDA decline of 8.3% and a margin down 270 basis points to 35.4%.

Ghost Bite: Africa is a treacherous place thanks to macroeconomic and geopolitical risks, but it’s also the only practical source of growth for our telco giants. When things are stable on the continent, the money flows!

Octodec’s interim growth shouldn’t be extrapolated (JSE: OCT)

Instead, focus on the dividend and the guidance

Octodec has an unusual portfolio. Aside from the sizeable residential portfolio (which is already jarring for most REIT investors), there’s also heavy exposure to Gauteng CBDs. These areas aren’t exactly famous for having great infrastructure and safety, so Octodec is playing in spaces where it feels hard to make money.

They are looking to make changes to the portfolio, with the idea being to focus on residential, mini-warehouse industrial parks and neighbourhood convenience shopping centres. An example of a recent major deal is the disposal of Killarney Mall (which is anything but a convenience centre) for R397.5 million, subject to regulatory approval.

You’ll notice that office properties aren’t part of the plan. I don’t blame them, as Octodec’s portfolio sits outside of the classic “P-grade and A-grade” strategy – and even that has been holding on for dear life in the office space. Lower-grade offices are really suffering, with a vacancy rate of 22.2% in Octodec’s portfolio. The 140 basis points increase in that vacancy rate in the past six months is thanks to the City of Tshwane leaving a building.

Based on this backdrop, you might be surprised to learn that distributable earnings per share increased by 11.1% in the six months to February. As exciting as that sounds, the actual distribution per share is only 4% higher.

The net asset value per share increased by 2.4%, so the total return is higher than inflation, but nowhere near as high as the growth in distributable earnings per share.

The outlook for the full year is growth in distributable income per share of between 3% and 5%. That’s much better than the previous guidance of between 0% and 4%. It also shows that the interim growth shouldn’t be extrapolated.

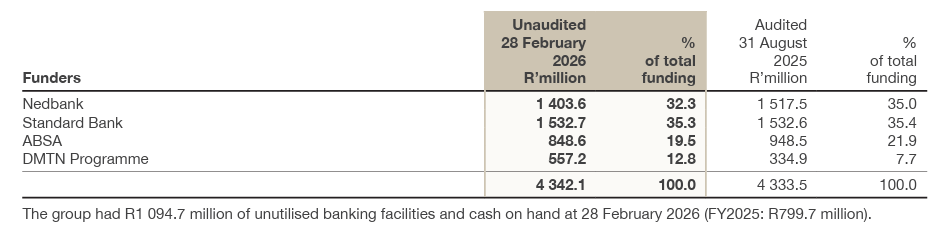

The balance sheet is in decent shape, with a Loan-to-Value (LTV) of 37.3% vs. 37.9% in FY25. I think this was quite a nice table in the results that demonstrates the importance of a spread of funding:

Ghost Bite: On the REIT risk spectrum, Octodec would find itself far along the horizontal axis. With the share price up 60% over 12 months, the relationship between risk and reward has worked out well recently!

The market has gone cold on Prosus (JSE: PRX | JSE: NPN)

Tech companies in the application layer are suffering at the moment

My shares in Prosus fell by another 5.3% on Tuesday after the company released a letter to shareholders by Fabricio Bloisi. The shares are now 41% off the 52-week high!

With that kind of sell-off, you would expect to see a company in absolute crisis. Instead, it feels like Prosus (and Tencent) are mainly the victims of a market scared of technology companies that play in the application layer rather than the infrastructure layer.

In other words, the market wants to own chip and memory makers, not platform players. The Prosus share price pain isn’t unique in the sector, but it does feel particularly amplified by the market’s ongoing distrust of the “Prosus ex-Tencent” portfolio.

But what was in the letter?

Bloisi is promising a “year of execution” in FY27. The group is focusing on AI enhancements across the business, ranging from better recommendation engines through to agentic commerce.

The letter also includes some financial elements. For FY26, Prosus achieved its guidance on revenue and eCommerce-adjusted EBITDA. The letter notes that all of the ecosystems are profitable, with the goal being to build the leading lifestyle ecosystems in LatAm, Europe and India.

And with a comment around the need for “trade-offs” to drive growth, we are reminded that Prosus is now operating in a market where capital is far more expensive than it was during the pandemic.

In Latin America, iFood is the platform that Prosus is building around. This is Bloisi’s legacy and he understands it very well, so I’m not surprised to see this. Synergies are important here, with Despegar running ahead of guidance for revenue from iFood referrals. Travel and pizza seem to pair well!

But this market is anything but easy, with the letter noting that iFood’s competitors are expected to spend more than $1.5 billion this year to win market share. Value-destructive competition is great for consumers and bad for platforms, with Prosus flagging an expected reduction in adjusted EBITDA in FY27 as they invest in the platform. Even though this is probably the right long-term play, the market is in no mood to hear this story.

In Europe, OLX is hitting its adjusted EBITDA targets and taking advantage of a platform that has been enhanced by the La Centrale deal. On the topic of deals, Just Eat Takeaway.com (JET) is going to be a difficult turnaround. JET’s volumes fell 7% year-on-year, but pilot programmes are achieving growth of 25% in some cities. They expect to return JET to growth by the end of the year after four years of decline. Again, this may well be the right long-term play, but the market is especially not keen on platform turnaround stories right now.

In India, PayU is the heart of the ecosystem. India gets just one paragraph in the letter though, so they are playing their cards close to their chest in that business.

Ghost Bite: The share repurchases continue. Personally, I hope they will accelerate with the proceeds of the partial sale of Delivery Hero. With the share price under so much pressure, nothing sends a message like share repurchases.

Spear REIT delivers a buy-and-flip masterclass (JSE: SEA)

This isn’t their usual strategy, but why not make money where you can?

In October 2024, Spear REIT acquired Hamilton House and Chiappini House in the Cape Town CBD for a total of R80.75 million. They’ve now agreed to sell the properties for an estimated R107 million (this could vary slightly depending on date of transfer).

For a long term holder of property, that’s quite the buy-and-flip profit!

The properties were acquired as part of the Western Cape portfolio that Spear bought from Emira Property Fund (JSE: EMI). Like in most garage sales, the stuff you buy will often contain a gem or two that you got at a bargain price.

Spear had to do the work though, with the value unlock play based on the properties being good candidates for redevelopment into residential property. This isn’t where Spear wants to play, so they are recycling the capital into industrial, convenience retail and institutional-grade commercial assets.

Ghost Bite: When management teams are aligned with shareholders and consistently do the right things, everyone wins.

Results of previous poll:

Nibbles:

- Director dealings:

- The non-executive chair of Primary Health Properties (JSE: PHP) bought shares worth around R103k through the reinvestment of dividends.

- If you’re interested in South32 (JSE: S32) and learning more about the metals underpinning the investment story (like copper and zinc), then you can check out the strategy presentation that the CEO will be delivering at a conference this week. You’ll find it here.

- Not all scheme of arrangements achieve shareholder approval. We’ve been reminded of this fact by Mahube Infrastructure (JSE: MHB). The scheme of arrangement regarding the offer by Sustent at R6.00 per share (originally R5.50 per share) was voted down by shareholders. Approximately 65% of votes were cast against the scheme, so it failed by a country mile. This stock was trading below R4.00 per share a year ago, so it’s going to be interesting to see what happens next.

- Oceana Group (JSE: OCG) has decided to extend CEO Neville Brink’s employment contract. The termination date has been pushed out from 31 December 2026 to 31 December 2027. The concern is that this is based on an unsuccessful search for a replacement CEO. Succession planning appears to be lacking here, with Brink having been in the role since 2022.

- Orion Minerals (JSE: ORN) announced the results of resource optimisation drilling. Unless you’re a geologist or mining engineer who understands the importance of a down-dip visible copper sulphide mineralisation, you can skip all the numbers and read the CEO’s commentary. The summary is that the results are “encouraging” but that laboratory testing will give the real answers, with the report due in roughly three weeks.

I like the new format – small insights in a separate section – well done

Thank you!

I really appreciate the Ghost Bite comments, thank you. On a point of order I think the MAS ticker is JSE: MSP (and not JSE: MAS).

Spot on. Will fix that!