Some positive momentum at Cashbuild (JSE: CSB)

Cashbuild South Africa had a much better time in Q3

Cashbuild has released an operational update for the third quarter. It’s a goodie, with group sales up 9% year-on-year. This was achieved through a combination of 4% growth in existing stores and 5% growth from new stores.

If you adjust for the various acquisitions and closures, then comparable store growth was 6% for Q3 and 3% year-to-date. That’s a proper acceleration in sales!

In happy news, this 9% growth is thanks to an 8% uptick in volumes for the quarter, with 4% volume growth in existing stores. Selling price inflation was only 0.6%.

Digging deeper, we find that Cashbuild South Africa was up 7% from existing stores in Q3. That’s the highlight for me, as this is the momentum I’ve been waiting for as a shareholder.

The share price is sitting at pretty depressed levels right now:

Are Clicks shareholders rotating from safety to risk? (JSE: CLS)

The P/E multiple is finally coming back down to earth

On the JSE, my observation is that the very best companies are able to support P/E multiples in the low 20s. But you can see numbers closer to 30x for a long time, particularly when the market is in a risk-off mode and only interested in quality companies.

With more growth opportunities emerging on the JSE with each passing day, the P/E at Clicks has become harder to justify. I believe that this is why we saw the share price drop by 8% on Thursday in response to the release of results.

Clicks isn’t exactly executing poorly. Group turnover was up 7.4%, trading margin was maintained at 9.1% and diluted HEPS was up 8.1%. Cash quality of earnings is evident, with the interim dividend up 8.4%.

And with return on equity of 45.7%, shareholders shouldn’t be unhappy with management reinvesting their capital.

If we look deeper, pharmacy sales increased by 8.6% and took their retail pharmacy market share to 24.9% from 24.2%. That’s a quarter of the market in just one group! Importantly, the system issues they had towards the end of 2025 have now been resolved, having impacted retail turnover by roughly 0.9%.

Broader retail turnover was up 7.4%, with comparable stores up only 3.1%. This is where it starts to get really difficult to justify the high P/E. Margin was up 70 basis points, thanks mainly to private label volume growth.

On the wholesale side, distribution turnover was up by 13% and margin declined by 50 basis points.

With retail costs up by 6.1% and distribution costs up by 6.8%, the group trading margin managed to come out flat. The underlying divisions have huge structural differences in margin, with retail running at a trading margin of 10.3% and UPD (wholesale) at just 2.5%!

Share buybacks helped drive the result, with headline earnings up by just 6.4%. Extensive buybacks took HEPS growth to 8.1%. If they want to support the share price, they should ramp up the buybacks now that the shares are trading at a lower valuation.

The outlook for the year ending August 2026 is HEPS growth of between 4% and 9%. The market has spoken about how low this is relative to the P/E multiple, with ugly negative momentum in the Clicks share price.

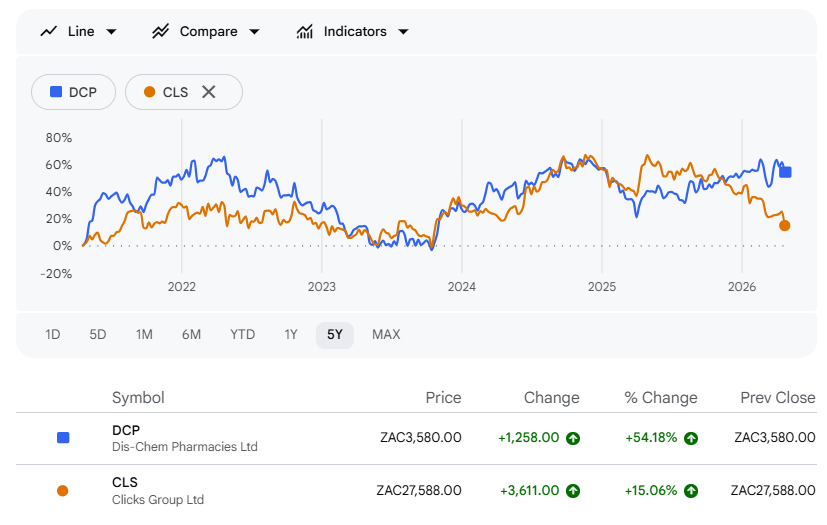

The really interesting chart is to compare Clicks and arch-rival Dis-Chem (JSE: DCP). I’m really enjoying the strategy at the latter at the moment, with plenty of talk around the power of data. The market seems to agree:

But what do you think. Which one would you choose to hold over the next 3 years?

Promising signs at Sasol (JSE: SOL)

And a reminder that having an energy company in South Africa is important

Unsurprisingly, Sasol takes the opportunity in the latest quarter to point out how valuable it is to have a local energy player. With all the conflict and supply worries in the Middle-East, we are able to produce at least some of our fuel (including jet fuel) locally.

The destoning plant has continued to improve coal quality at Sasol, leading to higher coal production for the latest quarter and reduced external coal purchases in the Mining segment.

On the Gas side, Mozambique’s flooding during the quarter was a huge issue. Gas production was down 10%. The related force majeure was lifted in mid-February 2026.

In Fuels, production at Secunda Operations fell by 7% on a sequential basis, i.e. Q3’26 vs. Q2’26. Production is up 8% on a year-to-date basis though.

The Chemicals Africa business enjoyed a 14% increase in revenue on a sequential basis, driven by a 9% increase in volumes and a 4% increase in sales prices. But year-to-date sales revenue is flat, with the basket price offsetting the gains in volumes.

In Chemicals America, sales revenue is up 6% on a sequential basis and 4% on a year-to-date basis. They operated above nameplate capacity during the third quarter – long may that last!

Chemicals Eurasia achieved a 12% uptick in revenue on a sequential basis and 7% year-to-date. A solid uptick in prices drove this outcome.

The outlook is encouraging, with fuel sales volumes growth revised upwards. They now expect 10% to 15% growth instead of 5% to 10%.

Gas production volumes have been revised downwards to an expected drop of 5% to 10% vs. FY25. Previous guidance in Gas was for a dip of 0% to 5%.

To make shareholders feel better, capital expenditure has been revised lower by R2 billion – to an expected range of R20 billion to R22 billion. That’s good news for free cash flow, probably the single most important driver of Sasol’s valuation.

Spear REIT raised their R1 billion in fresh equity with no problems at all (JSE: SEA)

Just look at that pricing!

As mentioned in the previous day’s Ghost Bites, Spear REIT asked the market for R1 billion in fresh equity to support the growth ambitions across new acquisitions and development of existing properties.

The market answered the call with enthusiasm, with the raise being multiple times oversubscribed. The pricing closed at a premium of 0.1% to the 30-day VWAP, an exceptional outcome for the company and for shareholders.

The price of R12.70 per share may be a slight discount to spot, but the 30-day VWAP is an especially important basis for comparison during such a volatile period in markets.

Year-on-year numbers at Valterra Platinum are heavily skewed by previous flooding (JSE: VAL)

The sequential numbers might be the better basis for comparison

Valterra Platinum released a production report for the quarter ended March 2026. With such severe disruptions at Amandelbult in the comparable period (Q1’25), the year-on-year percentage movements aren’t helpful. The very last thing you can do is extrapolate a 78% jump in refined PGM production!

Here’s something that is worth looking at instead: Q1’26 refined PGM production of 778,500 ounces is the lowest number we’ve seen on a rolling 12-month basis. Q2’25 was 954,000 ounces, Q3’25 was 981,500 ounces and Q4’25 was 1,039,400 ounces.

Despite what appears to be a slower start to the year, production guidance for 2026 is intact across volumes and operating costs per ounce. Energy costs based on the Middle East conflict are clearly a risk here.

On the plus side, the average basket price was the highest since Q2’21, driven by sharp increases in ruthenium, platinum and rhodium.

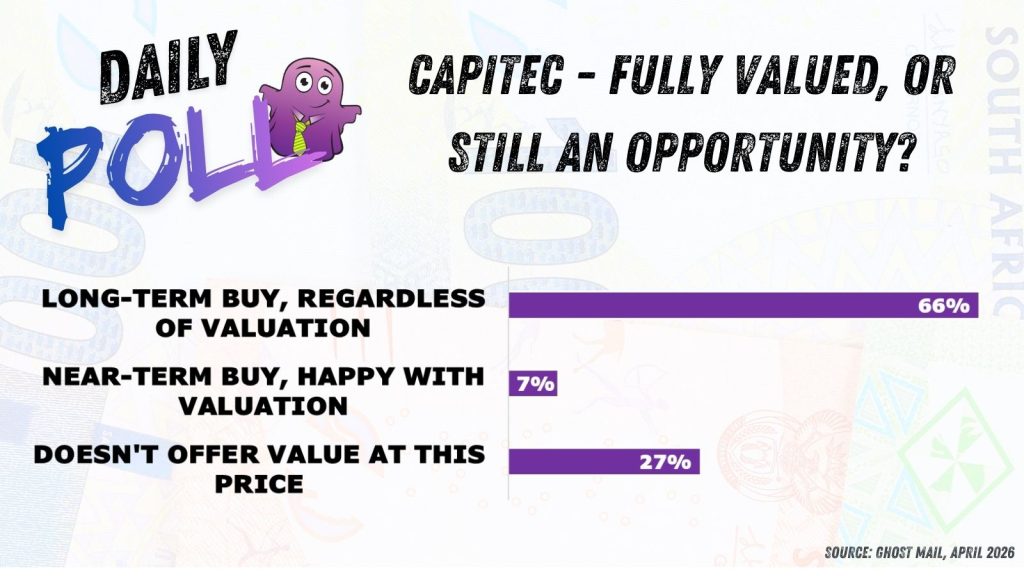

Results of yesterday’s poll:

Nibbles:

- Director dealings:

- A director of Sabvest Capital (JSE: SBP) sold shares worth R584k to settle debt obligations.

- A director of South Ocean Holdings (JSE: SOH) bought shares worth R30k.

- Zeder (JSE: ZED) has released results for the year ended February 2026. The company has made much progress with its value unlock strategy, with the sum-of-the-parts valuation being R1.50 as at the end of Feb. The circular for the sale of Zaad (excluding certain assets) was distributed to shareholders on 31 March 2026. The meeting is scheduled for 30 April. Assuming it all goes through, Zeder’s remaining asset will be an indirect 48.6% interest in May Seed. The strategy will no doubt be to find a buyer for this asset, and distribute the proceeds to shareholders.

- AfroCentric (JSE: ACT) is in the process of trying to sell Activo. That business has been negatively impacted by a key customer, leading to a revision of the terms of the transaction. They are looking at an upfront payment of R100 million, with earnouts up to R90 million. There’s also a potential adjustment based on working capital at the date of the deal closing. It’s a huge drop in price, as the previous terms were based on an upfront payment of R350 million and an earnout of up to R250 million! Ouch.

- ISA Holdings (JSE: ISA) is disposing of a 50% stake in DataProof for R62 million. As you might guess from the name, this is a cybersecurity company. For the six months to August 2025, profit after tax was R7.7 million. For the year to February 2025, profit after tax was R12.3 million. This implies decent underlying growth, although one has to be careful with smaller numbers like these. This is a related party transaction, as the financial director of ISA is also a director of DataProof. You see this kind of thing quite often in small cap land. (Note: an earlier version of Ghost Bites incorrectly noted ISA Holdings as the acquirer, not the seller – my apologies)

- Brimstone (JSE: BRT | JSE: BRN) has proposed a specific repurchase of shares from participants in the “N” ordinary shares scheme. This is due to limited liquidity in the shares. They are looking to repurchase approximately 1.33% of the current N ordinary shares for a maximum investment of R15.8 million.

- Trustco (JSE: TTO) has updated the market on the litigation related to Helios Oryx and the Namibia Revenue Agency (two separate matters). The update is that there is no update, with both matters still going through the courts – just in case you were keeping score for some reason.