In this edition of Ghost Bites:

- Clientèle shareholders give the green light to the offer and delisting transactions

- Profitability at Crookes Brothers has collapsed

- KAP: an unexpected boost from the Middle East conflict

- Mantengu is looking to dispose of Blue Ridge Platinum

- Novus has plenty of work to do in its business

- Vunani swings into profits

- Vodacom gave YeboYethu a great year

Clientèle shareholders give the green light to the offer and delisting transactions (JSE: CLI)

The deal is now much closer to meeting all conditions

Financial services group Clientèle is a big step closer to adding its name to the list of companies that have delisted from the JSE due to a stubbornly low valuation.

After an offer and proposed delisting was announced at the end of April this year, the circular was released in mid-May and the meeting was scheduled for 12th June. At that meeting, shareholders voted strongly in favour of the various resolutions required to execute the transaction.

The remaining condition relates to maximum acceptances. When the deal was announced, it looked like Clientèle had irrevocables in place to make sure that this condition would be met. There’s a difference between having irrevocable undertakings and actually achieving the condition though, so investors will have to wait until later this month to know for sure that everything is going ahead.

Ghost Bite: Assuming all goes as planned, the payment date of 29 June will see shareholders (who accepted the offer) paid R19.90 per share. It’s a discount to embedded value, but it’s also significantly higher than the range of R14.00 – R17.00 that the share was stuck in for months before the offer was announced.

Profitability at Crookes Brothers has collapsed (JSE: CKS)

This is another reminder of how tough the agri sector is

Crookes Brothers is one of the very few companies on the JSE that offer exposure to the primary agriculture sector. This is an extraordinarily volatile way to make money, as Mother Nature can be cruel and unpredictable.

The latest numbers prove once more that farming isn’t a guaranteed route to riches. For the year ended March 2026, Crookes Brothers saw its HEPS collapse spectacularly, down by between 93% and 99%!

This leaves them with HEPS of between 2.35 cents and 27.85 cents vs. 425.1 cents in the comparable period. There’s very little trade in the stock, so the share price decline of 27% over the past 12 months probably isn’t the best example of price discovery in action. There’s also an element of the market looking through the wild swings and taking a more moderate approach to the valuation.

The company attributes this decline to lower earnings across all segments. Sugar prices are under pressure, land sales have been delayed and the Macadamia segment is also struggling, as evidenced by a capital impairment of around R256 million in that business. Remember that the impairment isn’t a cash item and is excluded from HEPS, so it’s just an indicator of how tough things are in the underlying business.

Ghost Bite: Farming is an extremely difficult industry. It sits way beyond my personal risk tolerance levels.

KAP: an unexpected boost from the Middle East conflict (JSE: KAP)

Safripol has been helped tremendously by fewer imports

It’s great to see KAP’s earnings moving in the right direction for once. This group tends to always have a headache or two to worry about, leading to a disappointing outcome for investors.

The share price might be up 43% year-to-date, but the total return over 5 years is -28% (yes, including dividends)!

As KAP is a useful barometer for the “real” economy in South Africa, I would love to see a more consistent positive performance from them.

FY26 looks a lot better, with the performance for the 11 months to May 2026 giving the group confidence to indicate that HEPS for the full year will increase by more than 50%.

The base effect is important here. FY25 was awful, with the ramp-up of PG Bison’s new MDF line and major challenges in the local vehicle OEM market. We can confirm this simply by looking at FY24, when KAP generated HEPS of 45.3 cents before plunging to 24.1 cents in FY25.

This means that FY26 is best framed as a partial recovery year. But that’s still a big step in the right direction.

We must touch on Safripol first, as this is arguably the trickiest part of the group for investors to consider. Global overcapacity is a structural issue, with such cheap imports being available that Safripol had to execute two commercial shutdowns at the PET plant in Durban. The sudden improvement in fortunes is thanks to the Middle East conflict, as it reduced imports and improved polymer prices. The second half mitigated some of the pain in the first half, but this doesn’t address the underlying structural risks.

PG Bison increased volumes and made progress in redirecting sales towards higher margin markets. They describe both revenue and operating profit as being “meaningfully higher” than in the prior period. This is a critical growth area for the group, as they’ve increased production capacity by 33% and need to deliver returns on that capex.

Unitrans has been focused on profits rather than revenue, with deliberate decisions to move away from lower margin activities. Although revenue was down, they describe operating profit as having increased “meaningfully”. They believe that there is still room to go here to improve the performance at Unitrans.

Feltex enjoyed an increase in domestic new vehicle assembly volumes. There were also major problems in the base period that didn’t repeat in this financial period, including operational constraints at two local OEMs and the costs of a model changeover. Revenue and operating profit were both higher this year, albeit with a slowdown in the second half relative to the first half.

Sleep Group is the headache this time around, with subdued customer demand and only a marginal increase in revenue despite higher marketing costs. This resulted in a moderate decline in profits.

Optix feels like a chronic problem rather than a headache you can fix with some pills. Although they grew subscriptions, there were lower hardware sales and thus revenue actually declined. Having invested in sales, the operating loss has now increased vs. the prior period.

KAP would do themselves a favour by getting out of Optix. It’s beyond me why that business is even in this group. It just confuses investors and usually has a negative impact on profits as well.

On the balance sheet, management’s target is a net debt reduction of R500 million for FY26. They are plannning a further reduction in FY27, but they didn’t give any specifics.

Ghost Bite: The Middle East situation gave Safripol a very helpful boost. But this is clearly not a structural improvement, and it doesn’t address the risk of imports returning with a vengeance once things normalise. The share price has rallied strongly in recent months, but KAP still has tons of work to do to start delivering consistent earnings growth to investors.

Mantengu is looking to dispose of Blue Ridge Platinum (JSE: MTU)

This is in anticipation of the potential Averi Finance transaction

Mantengu is currently working towards the large Averi Finance transaction that was announced in May. They are happy to streamline the group in the meantime though, including the potential disposal of Blue Ridge Platinum.

The deal isn’t guaranteed at this stage, but Mantengu has received an offer from Afresources Mining for the entire shareholding and related claims in Blue Ridge. The offeror is not a related party to Mantengu.

If my understanding of the announcement is correct, the offer values 100% of Blue Ridge at R50 million. Mantengu has a 70% stake in the asset.

This would be a Category 2 transaction, so shareholders wouldn’t be asked to vote.

Ghost Bite: It was only a year ago that Mantengu was singing the praises of this asset. Times have certainly changed at the company.

Novus has plenty of work to do in its business (JSE: NVS)

Especially with the Mustek distraction almost out of the way

With Novus having run the regulatory gauntlet and come out the other end with a controlling stake of 50.39% in Mustek (JSE: MST), management (and the market) will be able to pay more attention to the rest of the Novus group.

Importantly, the stake in Mustek was only 39.96% at the end of this reporting period, so Novus equity accounted earnings of R26.4 million. Going ahead, they will no doubt account for Mustek on a consolidated basis, especially as they still need to complete the mandatory offer to Mustek shareholders.

The rest of the Novus group needs some love, as performance wasn’t encouraging in the year ended March 2026. Revenue was down 0.7% and adjusted EBITDA was down by 15.2%. To give you a sense of the operating leverage at play here, revenue dipped by R27 million and adjusted EBITDA was down R101 million!

Diluted HEPS is the right metric to consider here, as there are share conversions coming down the line in relation to the Maskew Miller Learning deal. This metric was down 4.4% to 76.59 cents.

Despite the earnings pressure, Novus followed the textbook approach of putting the dividend ahead of everything else. They kept it at 55 cents per share.

If we dig into the divisions, the Print, Publishing & Distribution division increased revenue by 6.8% and operating profit fell by 28.6%. This was despite an improvement in gross margin in this business. I must also note that the divisional performance was skewed by the Publishing & Distribution side being included for the full 12 months vs. just 5 months in the prior year. If you isolate the Print side, revenue was down by 9.9%.

The Education business is looking increasingly like a problem, with revenue down by 18.1% after orders from provincial departments were below expectations. Although adjusted operating profit managed to tick up by 4.4%, this was mainly due to reduced amortisation on intangible assetss.

The Packaging segment saw revenue fall by 5.1%. Thanks to an increase in gross margin, adjusted operating profit increased by 8.9%.

The highlight here is the increase in the closing cash balance from R812 million to almost R1.02 billion. There were improved net working capital inflows in the Print and Education segments as they collected debtors. The net cash increase at year-end was all earmarked for the Mustek deal, so they’ve effectively turned better working capital into a new investment!

Ghost Bite: With numbers like these, I’m not surprised that the share price has been under pressure. Novus will need to show the market a much better story in FY26 if they hope to drive a higher Price/Earnings multiple.

Vunani swings into profits (JSE: VUN)

Full details will be available later this month

Vunani has released a trading statement dealing with the year ended 28 February 2026. There’s very good news for investors, as the company has moved from a loss-making position into profitability.

HEPS is expected to be between 10.9 cents and 11.5 cents, a huge improvement over the headline loss per share of -2.8 cents in the previous period.

The share is trading at R2.00, so there’s still an unrealistically high P/E multiple at play here. But at least earnings have moved in the right direction.

Ghost Bite: It’s always important to wait for detailed results before jumping to any major conclusions about performance. The results are due for release on 23 June.

Vodacom gave YeboYethu a great year (JSE: YYLBEE)

In this case, financial leverage has worked in favour of the structure

YeboYethu is the Vodacom (JSE: VOD) B-BBEE structure. Its only asset is an investment in listed Vodacom shares. This means that the net asset value of the fund changes every single day based the observable price of Vodacom shares.

The value of the debt in the structure (in this case structured as two classes of preference shares) ticks up based on the funding rate attached to those instruments. At YeboYethu, the Class A shares are priced at 68% of prime and the Class B shares are at 70% of prime.

For tax reasons, preference shares are priced as a discount to prime that is usually in line with the effective tax rate. You can essentially think of this as being comparable to traditional debt priced roughly at the prime rate.

Borrowing money to buy shares is risky, but that’s how these B-BBEE structures were all historically structured (to allow for participants who don’t have deep pockets to invest in shares).

The end result? A volatile net asset value in a highly leveraged structure. When Vodacom does well, YeboYethu does extremely well. Conversely, when the Vodacom share price suffers, YeboYethu gets an amplified version of that pain.

The year ended March 2026 is an example of the former, as Vodacom’s share price increased by 15% between March 2025 and March 2026. This is well ahead of the prime lending rate, so the underlying net asset value in YeboYethu increased by a juicy 42%.

Due to the extent of debt, dividends in these structures tend to increase by a more consistent rate. YeboYethu’s final dividend grew by 5%.

Ghost Bite: Analysing these structures is actually more complicated than the underlying shares, as you need a view on Vodacom and then on the balance sheet of YeboYethu itself. More effort could go into actually explaining these economics properly to the market, particularly as these structures are focused on including investors with limited capital and experience.

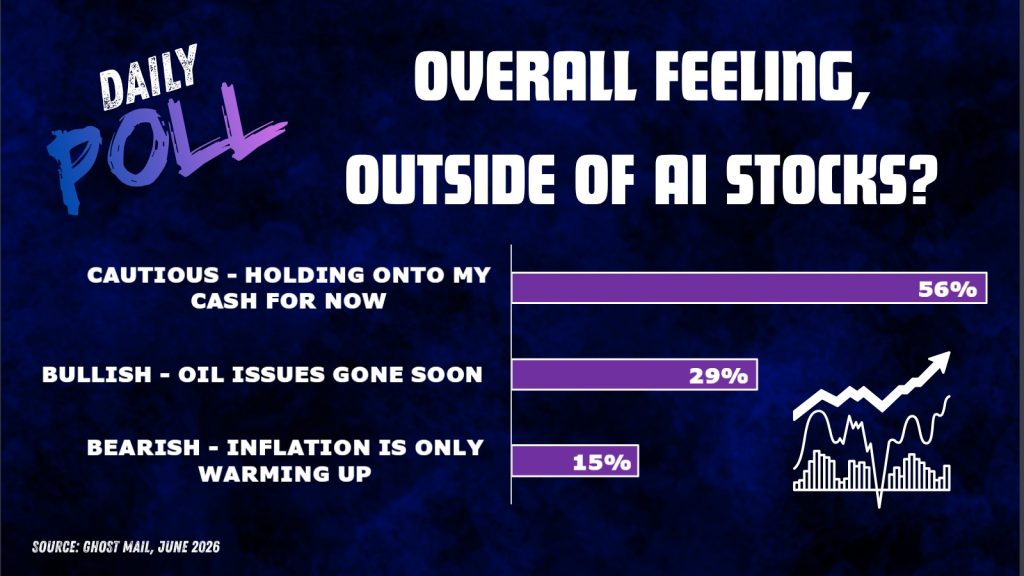

Results of previous poll:

Nibbles:

- Director dealings:

- A director of AVI (JSE: AVI) received share awards and sold the whole lot worth R7.8 million.

- An independent non-executive director of Pepkor (JSE: PPH) bought shares worth R397k.

- A director of a subsidiary of Santova (JSE: SNV) sold shares worth R160k.

- A prescribed officer of Advtech (JSE: ADH) sold shares worth R51k.

- AngloGold Ashanti (JSE: ANG) wants to move forward with the previously announced share repurchase programme of up to $2 billion. Shareholders need to approve it before that happens, with the meeting scheduled for 23 July. The current market cap is R705 billion, so this share buyback would be for roughly 4.5% of shares in issue.

- A new board has been constituted at RMB Holdings (JSE: RMH). The market already knew that the existing directors were planning to stand down in the aftermath of the AttBid offer. The new CEO is Gideon Oosthuizen, with Adriaan van Rooyen joining as CFO – both from Atterbury Property Group. The three independent non-executives are Andrew Brooking (of Java Capital fame), Nicolaas Kruger (ex-CEO of Momentum Metropolitan) and Dr Pine Pienaar (a highly experienced engineer).

- There’s a significant change in the shareholder register of Insimbi Industrial Holdings (JSE: ISB). New Seasons Equity Fund has sold its entire stake in the company. An investment entity called Sugarfields Fund I has bought a 30.41% stake, so they are going straight to a level that is only a few percentage points below the threshold for a mandatory offer! The director representing New Seasons Equity Fund has also resigned from the board. A replacement non-executive director hasn’t been named as yet, but it’s likely that it would be a Sugarfields Fund representative.

- Trustco (JSE: TTO) has received a demand to call a shareholders’ meeting from Riskowitz Capital Management. There’s clearly still no love lost between the board and that investor, with the agenda for the proposed meeting being to appoint a new board of directors. The board is considering the content and validity of the demand and will make a further announcement in due course.

- Sebata Holdings (JSE: SEB) released results for the year ended March 2025. Yes, they really are that far behind in their financial reporting. If you can believe it, HEPS swung from a loss of 102.20 cents to a profit of 100.66 cents! The swing in the numbers is thanks to the company regaining 100% control of the software and water divisions, with effect from 1 July 2024. They previously held 40% in these assets.