In this edition of Ghost Bites:

- Equites Property Fund and NEPI Rockcastle are good reminders of the strength of REITs

- KAL Group is one of the last “cheap” South African assets

- Karooooo upset the market with its margins this year, but they are playing the long game

- Reunert has been dragged down by its cables business

- Tharisa’s earnings have skyrocketed

- …and there are many, many Nibbles!

Equites Property Fund is delivering mid-single digit growth (JSE: EQU)

This at least gives investors the inflation protection that the REIT sector is known for

Equites Property Fund has released results for the year ended 28 February 2026. Regular readers will know that this fund is in the process of selling its UK assets and bringing the capital home to South Africa.

Distribution per share growth for this period was 5.3% (in line with guidance). This gives investors a reasonable return relative to inflation, although there are REITs that are delivering more at the moment.

The loan-to-value ratio of 35.1% tells us that they have a solid balance sheet, which is important as they have significant ambitions for their development pipeline in South Africa.

With the UK assets being recycled, the South African pipeline will hopefully not require equity capital raises that are dilutive to shareholders. The REIT sector can be a very frustrating place for retail shareholders during periods of capital raising, as we don’t get phoned up bookrunners to buy shares at a discount to the spot price.

The forecast growth in the distribution per share for FY27 is between 5% and 7%. This is an encouraging uplift, informed by the high visibility that Equites enjoys on its earnings thanks to long-term leases.

Ghost Bite: I continue to beat the drum that REITs are a better long-term investment than buy-to-let residential properties.

KAL Group: one of the last “cheap” local assets (JSE: KAL)

Will fuel volumes ruin the party in the second half?

KAL Group’s results for the six months to March 2026 tell a promising story. Revenue was up by 5%, EBITDA climbed by 7.7% and HEPS was 12.5% higher. As the icing on the cake, recurring HEPS increased by 15.1%!

That’s the shape that you want to see on an income statement.

Although net cash from operating activities only increased by 3.9%, the interim dividend per share was up by 25%. The improvement in the balance sheet (net interest bearing debt to equity reduced from 48.4% to 32.9%) would’ve helped justify this decision.

There is an important nuance that needs to be considered. The company has highlighted “exponential” fuel demand in March ahead of expected fuel price increases in April. This helped drive an increase in fuel volumes of 6.7% for the period. In turn, this delivered a whopping 49.2% profit before tax growth in PEG, KAL’s forecourt business.

My concern is that much higher fuel prices will undoubtedly impact volumes. Management’s outlook statement recognises this risk, but they remain bullish about the second half of the year and the longer term prospects.

The other key exposure is of course the broader agriculture business. KAL has specialist retail businesses that depend on the spending power and level of investment by farmers in their crops. It’s almost impossible to forecast this stuff with any accuracy, but one thing to note is that the fuel price spike will impact inflation throughout the value chain.

Ghost Bite: On a single-digit Price/Earnings multiple, KAL Group remains one of the “cheap” assets on the JSE. The share price increase of 13% over the past year is a great return when you add on the dividend as well. Perhaps management’s commitment to focusing on metrics like return on invested capital (ROIC) will help catalyse a higher multiple. But what do you think?

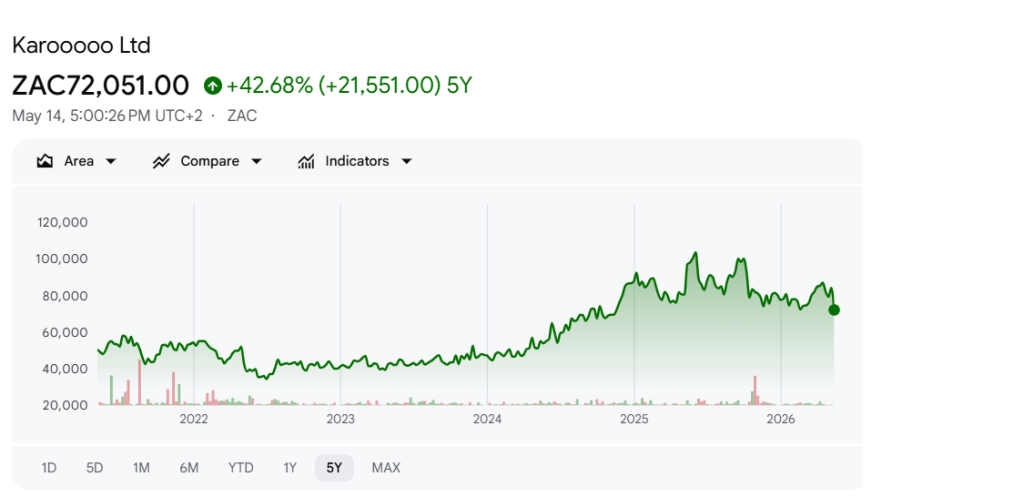

Karooooo’s margins have upset the market (JSE: KRO)

This management team is playing the long game

Karooooo’s results for the quarter ended February 2026 mark the end of the financial year for the group. This means that we must consider fourth quarter and full year results separately.

Starting with the quarter, we find growth in Cartrack subscribers of 16%. Encouragingly, net Cartrack subscriber additions grew by 19% (a measure of the rate of increase, not the size of the total user base). This represents the most subscribers that they’ve ever added in a fourth quarter period.

Subscription revenue for the quarter increased by 18% to R1.28 billion. The logistics side of the business (which they call Delivery-as-a-Service, or DaaS) jumped by 32% to R145 million. It’s much smaller than subscriptions, but becoming more meaningful every day.

But now we reach the bad news: operating profit margin has declined dramatically from 34% to 25%. This is because operating profit at group level has dropped by 12%!

For the full year, Cartrack subscriber numbers increased by 16%, subscription revenue was up 19% and DaaS revenue increased 29%. Operating profit only increased by 8%, as the full year margin declined from 31% to 28% – dragged down by the final quarter of the year.

What has happened here? Well, the same thing that we often see at Karooooo – a front-loading of sales and marketing costs. The company needs to build up its sales infrastructure in order to drive the next wave of growth. In a period of heavy investment, this puts the squeeze on margins.

In 2027, they will reduce the rate of headcount growth as they drive efficiencies and AI adoption.

Guidance for FY27 is subscription revenue growth of between 18% and 24%, with operating margin between 27% and 30%. This suggests a modest uptick in margin at the mid-point of that guidance. Combined with such strong expected revenue growth, that would imply a potentially solid outcome for investors in FY27.

The market isn’t famous for being patient though, with the share price down nearly 10% on the day!

Ghost Bite: Karooooo has been an absolute winner for me over the past few years. My only regret is that I didn’t buy more along the way. My temptation to buy more is increasing, particularly given this share price weakness:

NEPI Rockcastle’s trading metrics look solid (JSE: NRP)

But this isn’t translating into high earnings per share growth

Iconic Eastern European property fund NEPI Rockcastle has updated the market on the first quarter of the year.

Property net operating income increased by 3.2%, with a like-for-like increase in tenant sales (excluding hypermarkets) of 3.8% as a major driver. Footfall was stable, so consumers are still visiting NEPI’s properties despite ongoing eCommerce adoption.

EPRA vacancies are very low at 1.8%, with tenants keen to get a slice of that footfall. This has supported new leasing activity at strong base rents that are 2.2% above indexation (inflation).

One of the interesting strategic focus areas at the group is the accelerated roll-out of solar PV projects. They refer to their energy platform as a “complementary growth driver” for the group, so they are seeing appealing return on capital metrics from this investment. It helps that funding can be raised on preferential terms when there’s an underlying sustainability angle.

Speaking of funding, the loan-to-value of 32.4% sits comfortably below the 35% long-term upper threshold at the group. With a substantial development pipeline over the next three years, having ongoing access to debt at favourable rates will be critical.

No valuations are conducted at the Q1 mark, so there’s no meaningful update on the net asset value per share. The only movements would relate to cash and debt.

Despite all the underlying excitement, guidance for earnings per share growth for the year is around 3%. This is why the share price is flat over the past year, with the market buying NEPI primarily for its yield.

Ghost Bite: Property funds with large development pipelines are hungry for capital. Unless they recycle existing assets, much of this capital will come from shareholders. This leads to more shares being in issue over time, putting downward pressure on earnings per share.

Reunert dragged down by power cables (JSE: RLO)

Earnings have dropped sharply

In Reunert’s trading statement for the six months ended March 2026, shareholders were given the bad news that HEPS from continuing operations will be down by between 20% and 25%. This suggests a range of between 179 cents and 191 cents for interim HEPS.

The actual drop is between 47 cents and 59 cents, with the company attributing 27 cents of this move to the underperformance of the Electrical Engineering segment (and particularly the power cable business).

Weak demand in South Africa and Zambia is an issue, with generally poor infrastructure spend being exacerbated by the increase in raw material commodity prices. The appreciation of the Zambian currency against the US dollar is also an issue. This is a bearish story for the cables business.

Ironically, there’s a 24 cents per share move from IFRS 2 share-based payment expenses linked to the increase in Reunert’s share price. The plan vests in April 2027. If things don’t improve in the cable business, the share incentive plan might be cheaper than they expect!

Ghost Bite: The explosion in data centre demand in this AI era is causing all kinds of difficulties in supply chains. Suppliers will always sell to the highest bidder – and in this case, nobody has more capex available than the hyperscalers. Any product that uses the same inputs (like power cables) is facing immense inflation.

Tharisa’s earnings have skyrocketed (JSE: THA)

There’s no rollercoaster quite like mining

Tharisa’s numbers for the six months ended March reflect an incredible jump vs. the prior period. HEPS is up by between 455.2% and 472.4%, which means an expected range of US 16.1 cents to US 16.6 cents. As I always remind you: when things are good in mining, they are really good.

We had a good idea that this was coming. After all, the commodity prices are no secret.

Ghost Bite: The PGM players are having their time in the sun right now. The key is for them to use their capital wisely to position themselves for the next cycle. In Tharisa’s case, they are investing in underground mining. Extra points for bravery!

Results of previous poll:

Nibbles:

- Director dealings:

- The game of musical shares continues at the Wiese family dinner table, with Titan Fincap and Titan Premier Investments entering into a total return swap over Shoprite (JSE: SHP) shares worth a casual R592 million.

- A director of a major subsidiary of Weaver Fintech (JSE: WVR) sold shares in the group worth R2.2 million. The stock has had an incredible run (it’s been one of my best positions), but it’s important to keep an eye on insiders selling their shares.

- Johnny Copelyn has bought shares in Montauk Renewables (JSE: MKR) worth around R420k.

- The CEO of Dipula Properties (JSE: DIB) has celebrated the strong results by buying R213k worth of shares in the company.

- Given what I’ve been through with the management team of this company, I hate it when Mantengu (JSE: MTU) releases an update that I need to write on. I especially hate it when my concerns about their business prove to be directionally correct. Sublime Technologies, the asset they bought for a miracle price that led to a huge bargain purchase gain, is unable to operate at current Eskom tariffs. They have applied for a new tariff agreement but have yet to receive approval. To their credit, they tried to keep all the staff, but they’ve now had to go into a s189 process as there has been no production of silicon carbide since mid-2025. The broader smelter industry is in crisis in South Africa, so this issue isn’t unique to this asset. Here’s the real point though: don’t you think the sellers of the business took into account the electricity risks when they decided to walk away for a “bargain” price? If Mantengu can get the tariffs they need, then it might still work out to be a great deal (and I hope it does). But the need for professional skepticism remains as important as ever – when you see an enormous bargain purchase gain, you need to ask the tough questions. When a management team responds to those concerns in a highly unusual way, then you need to ask twice as many questions! Hopefully the winds of change have now blown at Mantengu and they will change their approach to dealing with market analysts who ask pertinent question.

- Shaftesbury Capital (JSE: SHC) has delivered a trading update at the AGM. They seem happy with the first quarter of the year, with new leases and renewals both running comfortably ahead of market rents and previous passing rents. Vacancies are very low, with the London West End continuing to attract shoppers and tenants alike. With 4.6% of the portfolio under refurbishment, Shaftesbury is investing heavily in its portfolio. The loan to value ratio is only 17%, so they have the balance sheet to do it.

- Finbond (JSE: FGL) has released a further trading statement dealing with the year ended February 2026. The initial trading statement noted a swing from a headline loss per share of 1.9 cents to positive HEPS of at least 2.9 cents. The updated range for HEPS is between 5.01 cents and 5.39 cents, so that’s quite a lot better than initially indicated! It’s still a long way off the share price of R1.13, though.

- Clientèle (JSE: CLI) has released the circular for the previously announced offer and delisting. With the shares trading at a stubbornly high discount to the embedded value per share, the company has seen the opportunity to move away from the listed environment. Based on an expected payment date of 29 June, the price will be R19.90 – a premium of 25.47% to the 30-day VWAP. This is a pretty standard premium for a buyout offer. You can read the circular here.

- Labat Africa (JSE: LAB) has released a cautionary announcement regarding the potential acquisition of the remaining 24.5% in Classic International Trading. They highlight that it’s because of the strong results produced by both Classic and Labat. Ideally, you would only want to see a company moving from a controlling position to a 100% stake under certain conditions. One would be if there are synergies that need to be unlocked that require the minorities to be out of the way. Alternatively, it’s a good idea if the acquisition price is highly attractive. But in the absence of those factors, it’s generally a weaker use of capital vs. finding other opportunities. Until a detailed terms announcement is released (if they go ahead), we won’t know whether this is a promising transaction or not.

- I don’t usually comment on independent director movements, but sometimes they are relevant. Hyprop (JSE: HYP) announced that Kevin Ellerine has resigned from the board to “pursue personal interests”. Those interests may well involve transactions with Hyprop itself, with Ellerine managing the future conflict of interest proactively.

- Attacq (JSE: ATT) has concluded the appointment of Peter de Villiers as the company’s permanent CFO. Having engaged with him on a recent Unlock the Stock, I’m not surprised to see this at all.

- Visual International (JSE: VIS) is in talks with Serowe Industries. Serowe might subscribe for up to 34.9% of the issued shares of Visual for R60 million. An extension has been granted until 30 June 2026 to allow Serowe to conclude the due diligence work. The valuation work has apparently already been concluded.

- Emira Property Fund (JSE: EMI) has been buying up Octodec (JSE: OCT) shares through a combination of off-market deals, on-market trades and a formal voluntary offer. With the offer having been accepted by holders of 2.2% of Octodec shares, Emira’s stake is up to 23.5% of shares in issue.

- Shuka Minerals (JSE: SKA) has commenced the Phase 1 drilling programme at the No.2 ore body at the Kabwe Zinc Mine. The company plans to increase the existing resource by 50% based on drilling work this year.

- Aimia (JSE: AII) is renewing its Normal Course Issue Bid – a terribly fancy way (in Canada) of saying that they are doing share buybacks. The board has authorised the repurchase of up to 10% of shares in issue in an effort to reduce the discount between the share price and the NAV per share.

- In case you somehow think that South Africa is the only land of dicey ethics, then here’s an update from Globe Trade Centre (JSE: GTC) – perhaps the most obscure name of all on the JSE. Preliminary findings of an internal investigation identified indications of irregularities, in connection with the acquisition of assets in Germany. Detailed findings will be communicated in due course. At this stage, it sounds like someone might be deep in the schnitzel.

- Cafca Limited (JSE: CAC) literally has no liquidity at all in its stock. The Zimbabwean cable manufacturing company has released interims for the six months to March. It’s no surprise that the numbers are reported in US dollars instead of Zimbabwe Gold. Thanks to copper and aluminium volumes, Cafca’s volumes were up 14% year-on-year and revenue grew by 24%. This took profit after tax up by 211%. And no, I’m not sure why this cabling company is making money and others are struggling!