Fairvest’s capital raise: have we reached silly season in the property sector? (JSE: FTB | JSE: FTA)

Welcome to oversubscribed raises at a premium to VWAP

Approximately 10 years ago, when I was working in the corporate finance industry, it was incredible to see how much activity there was in the property space. I used to think about the people at Java and how much money they must be making from capital raises alone.

Like all hype cycles, the tide eventually went out and property funds saw a nasty decline in prices. Too much capital had been thrown at weak deals. To make it worse, funds were trading at a premium to book. This meant that the market was pricing in the benefit of future deals, not just the strength of the existing portfolio.

We aren’t there quite yet, but I’m keeping a close eye on things in this sector. The latest capital raise by Fairvest is of concern, as the company announced in the morning that they were looking for R500 million in new B shares. The announcement didn’t even explain what the capital is for, so that’s the first red flag for the sector. When it becomes easy to raise capital, the risks go up.

Here’s the second red flag: the market threw money at Fairvest and the company gladly accepted it, with the raise increased to R900 million. The third red flag is that the pricing is a 5.5% premium to the 30-day VWAP.

At least the final announcement indicated what the capital will be used for: partial settlement for the Muller Group acquisition, ongoing investment in Onepath Investments and debt reduction ahead of pending asset transfers.

The Fairvest B shares are up 39% in the past 12 months. The board is doing the smart thing by raising capital at this level. Investors should be doing the smart thing by becoming even more vigilant in this sector going forwards.

I don’t think we are quite in silly season yet, but we are creeping closer. But what do you think?

Hulamin is selling Hulamin Extrusions (JSE: HLM)

This will help the company focus on the core Rolled Products business

Hulamin has announced the disposal of Hulamin Extrusions to Norsaf ERS, an unrelated party. This deal has been in the works for a while, with Hulamin having previously identified this as a non-core asset. The announcement of this transaction means that Hulamin is no longer trading under cautionary.

It’s not exactly the biggest deal around. The shares are being sold for R10 million and there will be further payments for inventory based on the balance as at 30 October 2026. The inventory balance isn’t expected to exceed R100 million.

Hulamin Extrusions suffered a loss after tax for the year ended December 2025 of R36 million. The acquirer clearly has plans to improve that situation. As for Hulamin, they unlock some capital and bid farewell to an expensive distraction.

This is a Category 2 transaction, so shareholders won’t be asked to vote on the deal.

Impala Platinum still on track for the full year (JSE: IMP)

They sound happy with the third quarter production numbers

Impala Platinum has released a production report covering the three and nine months ended March 2026. The overall narrative is one of a solid third quarter, where group excess inventory has been reduced ahead of expectations.

The quarterly production results at mining groups will always reflect the underlying volatility of the mining sector. For example, 6E production at managed operations was down 2.6% in the three months to March, impacted by smelter maintenance at Zimplats. But Refined 6E production, which includes other mining operations, was up by a juicy 18.8%.

Here’s the number that really counts in terms of generating cash for investors: 6E sales volumes increased by 9.2%.

If we look at the year-to-date numbers, which are smoother based on the longer time frame, we find that 6E production at managed operations was only down by 0.2%. Refined 6E increased by 5.1% (surely a fairer reflection of underlying performance than the 18.8% jump in the third quarter) and sales volumes were up 3.0%.

Importantly, guidance for the full year has been maintained across major operating and capital expenditure metrics.

Mondi’s quarterly EBITDA continues to slide (JSE: MNP)

The trajectory over the past year is concerning

Before I dive into the latest numbers at Mondi, it’s worth showing you what the share prices of Mondi and Sappi (JSE: SAP) have done over the past year:

Now that you’ve braced yourself, let’s look at Mondi’s financial performance in the quarter ended March 2026, which represents the first quarter of the 2026 financial year.

EBITDA of €212 million in Q1’26 is a long way down from €290 million in Q1’25. Technically, if we strip out the forestry fair value gains, then the latest quarter is the slightest possible improvement vs. Q3’26.

But if we keep the fair value movements in, which we probably should, then the latest quarter is the lowest that it’s been over the rolling 12 months.

The problem isn’t related to Mondi’s controllables. Their Corrugated Packaging and Flexible Packaging businesses increased sales volumes in Q1’26 vs. Q4’25, with no planned maintenance shuts. But with lower selling prices and higher energy costs towards the end of the quarter, margin pressure was the only possible outcome.

The sector was already in serious trouble before the conflict in the Middle East. Mondi has noted the risk of energy, raw material and logistics costs. They will put through pricing increases where they can, but those price increases are only expected to take effect in the third quarter of the year.

Mondi fell 9.5% on the day of the announcement.

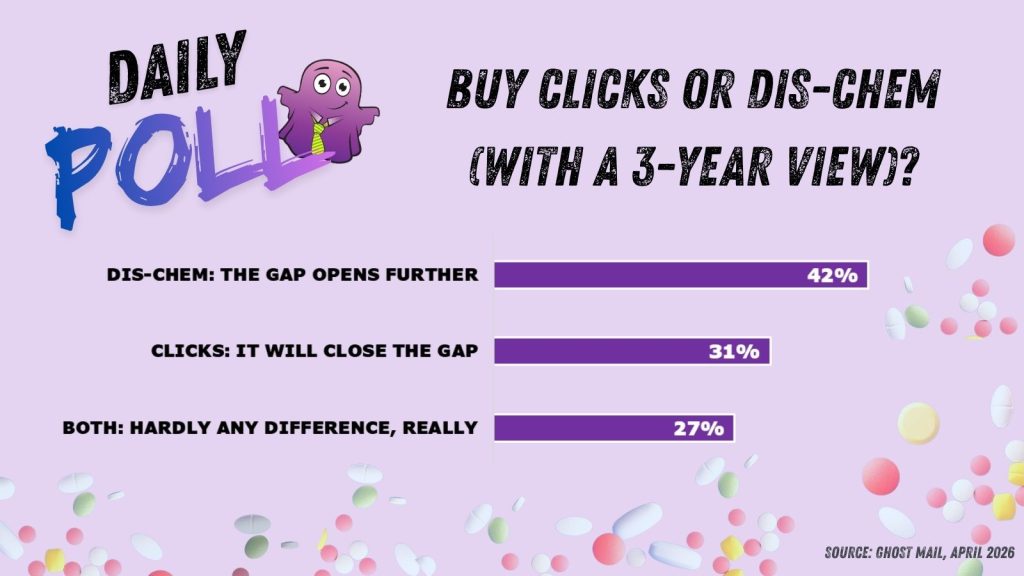

Results of yesterday’s poll:

Nibbles:

- Director dealings:

- A couple of Mpact (JSE: MPT) directors sold only enough shares to cover the tax on share awards, but two other directors sold the entire amount worth R1.9 million in aggregate.

- An associate of a director of South Ocean Holdings (JSE: SOH) bought shares worth R100k.

- Emira Property Fund (JSE: EMI) is busy with a voluntary offer to acquire enough shares in Octodec (JSE: OCT) to take them to a 34.9% stake – just below the threshold for a mandatory offer. The offer price is R16.75 per share. This isn’t stopping Emira from acquiring shares in on-market transactions at the same price. They’ve bought almost 2.9 million shares in the market, so the offer is now for 36.3 million shares instead of the initial 39.2 million shares. In practice, this means that Octodec investors who accept the offer may not end up selling as many shares as they hoped.

- enX Group (JSE: ENX) announced that the TRP Compliance Certificate for Trichem SA’s acquisition of the remaining 75% in West African International from enX has now been received. The deal is therefore unconditional.

- Salungano Group (JSE: SLG) is still trying to catch up on its financial reporting obligations. They’ve released a trading statement for the six months to September 2025, reflecting an increase in HEPS of between 68.48% and 88.48%. Most importantly, they expect to release those interim results this week.

- Lwazi Bam has been appointed by MTN (JSE: MTN) as Chief Risk Officer. This means he is resigning from other non-executive board roles, including at Standard Bank (JSE: SBK) and Valterra Platinum (JSE: VAL).

- Insimbi Industrial Holdings (JSE: ISB) announced an interesting director appointment. Ernest Kwinda, founder of Itai Capital and an ex-RMB corporate financier with plenty of experience, has now joined the board. Is the company looking at doing major transactions in future?