In this edition of Ghost Bites:

- Accelerate Property Fund makes more progress

- Bytes Technology investors will have to be patient

- Capitec sells the rental finance business to Sasfin

- Sappi unlocks some positivity in the market

Accelerate Property Fund makes more progress (JSE: APF)

This is one of the few speculative positions in my portfolio

Accelerate Property Fund is an interesting special situation on the JSE.

The fund has been trading at a vast discount to net asset value (NAV) per share for a variety of reasons. These include questions around whether Fourways Mall can be turned into a success, as well as the historical disputes and legal claims with ex-CEO Michael Georgiou (whose entity Azrapart is now in business rescue, and being managed by the business rescue practitioners).

I bought this stock a while ago based on progress they had made with major disposals like the Portside building. When a fund is trading at such a large discount to NAV, the main thing you want to see is the disposal of properties at a price close to NAV. Portside was a perfect and very large example of this.

Technically, if the fund sold absolutely everything and returned the capital to shareholders, the discount to NAV would close and there would be large gains on the table. In practice, what happens is somewhere in the middle – some of the buildings are disposed of, and the discount partially closes.

To that end, I’m happy to see that Accelerate has sold the BMW Fourways dealership showroom for R174 million to a subsidiary of Toyota. That probably gives us a clue about the future of the cars you’ll find at that property. But more importantly for me and the other Accelerate shareholders, the valuation of that property is R180 million.

This means that Accelerate has achieved close to NAV on this disposal, with a strong disposal yield of 6.4%. It’s a prime property, but I’m still glad that they’ve gotten this price. Nothing is ever guaranteed until the deals are actually done.

In further good news, Accelerate’s distributable earnings for the year ended March 2026 came in between 1.96 cents and 2.31 cents per share. That’s a massive swing from a distributable loss per share of 3.97 cents in the prior period. There’s still no dividend (the company’s balance sheet needs further improvement), but the direction of travel is clear.

The final piece of good news is one that will be the subject of debate. The company has decided to derecognise the obligation of R371 million linked to the rebuilt claim by Azrapart. This is a more aggressive accounting policy than we’ve seen before, so the company must be feeling confident that this claim has no merit. This does mean that the NAV will need to be adjusted by investors based on the risk weighting that they are willing to put on this claim.

Ghost Bite: My average in-price is R0.41 per share and the current price is R0.51. Accelerate has been as high as R0.76 per share. Of course, hindsight has demonstrated that I should’ve sold and re-entered lower down. I remain confident that my position will work out nicely here.

Bytes Technology investors will have to be patient (JSE: BYI)

Income is growing, but operating expenses are soaking up that growth

News broke the other day that VCP has taken a stake of over 5% in Bytes Technology Group. The market would see that as a positive sign. There’s now more information to consider, as Bytes used its AGM as an opportunity to give a brief update on recent trading.

For the first four months of the new financial year, Bytes achieved double-digit growth in gross invoiced income and gross profit. This is across both the private and public sectors.

Sounds wonderful, except operating profit is flat year-on-year. Investing for growth is fine, but one wonders about a strategy in which such strong top-line growth isn’t converting into anything for shareholders.

According to management, this performance is consistent with the company’s outlook, so they are on track with their plans at the moment.

Ghost Bite: Over 90 days, Bytes is up 44%. But on a year-to-date basis, the share price is only up 11%! Talk about perfect market timing for those who bought the selling pressure at the end of March.

Capitec sells the rental finance business to Sasfin (JSE: CPI)

Both financial services houses are sticking to what they are good at

Here’s something interesting, not least of all because it’s the first piece of news I’ve seen on Sasfin in a while.

You may recall that Sasfin was taken private as part of a significant strategic shift away from their traditional banking business and towards the areas in which Sasfin traditionally has strength.

Similarly, Capitec built its group by focusing on the things they are really good at.

The latest transaction is a good example of two financial services companies sticking to their knitting.

Capitec will sell the Capitec Rental Finance business to Sasfin for R201 million. Additionally, Capitec will provide a secured credit facility of R1.6 billion to that business to fund the ongoing rental receivables book. This means that Capitec retains indirect exposure to this segment via a loan, rather than through equity ownership and operating risk.

Capitec originally acquired the Capitec Rental Finance business as part of the Mercantile Bank deal in 2019. They’ve no doubt developed a good understanding of the business over the past 7 years, giving them the confidence to switch from being an equity holder to being a lender.

As for Sasfin, it’s good to see some positive momentum there after the take-private.

Ghost Bite: A R201 million transaction is literally a rounding error vs. Capitec’s market cap of R547 billion. But for Sasfin, this will be an important transaction.

Sappi unlocks some positivity in the market (JSE: SAP)

Recent trading has been better than expected

Sappi closed 15% higher on Thursday after giving the market some hope about the financial prospects of the group.

Previous guidance was that adjusted EBITDA in the third quarter would be lower than in the second quarter. Updated guidance is that group adjusted EBITDA should be broadly in line with the second quarter.

There’s a big difference between going backwards and ending up flat quarter-on-quarter. This is why the market gave this broken stock some love.

This performance was driven by stronger-than-anticipated results in North America, along with the steady ramp-up of Somerset Mill PM2 sales volumes.

Ghost Bite: Sappi is as speculative a stock as you’ll ever find. Even after the 15% jump, the share price is still down 58% year-to-date!

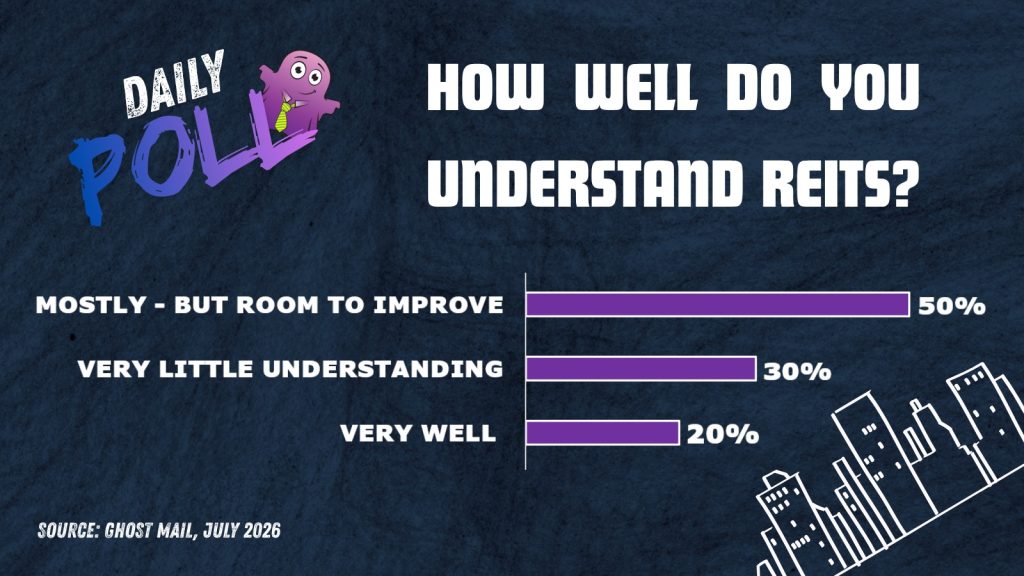

Results of previous poll:

Nibbles:

- Director dealings:

- S&P upgraded the credit rating of NEPI Rockcastle (JSE: NRP) from BBB (with a positive outlook) to BBB+ (with a stable outlook). This is a factor of the company’s strategy and strength of the balance sheet. If you’re interested in learning more, I explained the importance of credit ratings in a video and podcast available here.

- Aspen (JSE: APN) announced that chairman Kuseni Dlamini will step down as Chairman and independent non-executive director. He’s been in that role since 2015, so that’s quite an innings! Ben Kruger will take on the role of Chairman after the AGM in December. Notably, Chris Mortimer is also stepping down as an independent non-executive director. He’s been on the board since 1999!

- Numeral (JSE: XII), one of the most obscure names on the local market, gave an update on its healthcare and biotech segment. Aside from the development of a flagship facility in Kyalami, they’ve also invested into WestMed in the Western Cape. They are exiting Longevity and Isopharm. Also, the shareholding in Cryo-Save was increased to 51% as expected. Financials for the year ended February 2026 are expected to be finalised by mid-July.

- Zeda (JSE: ZZD) has issued additional notes to the value of R1.1 billion under its Domestic Medium-Term Note (DMTN) Programme. They got this done at 5 basis points below price guidance, so that should assist a bit with their cost of funding.

- Sebata Holdings (JSE: SEB) is no longer suspended from trading. There were initially suspended in October 2025 due to failure to release results for the year ended March 2025. They’ve now caught up, so the shares can trade again. With a market cap of under R100 million, I still wouldn’t expect much in the way of traded volumes.

- Two non-executive directors of Cilo Cybin (JSE: CCC) have resigned. Replacements haven’t been named yet. There’s also a change to the company secretary. That’s a lot of governance churn at the same time for a small cap.