Anglo American is the usual mixed bag – and diamonds are now a low margin game (JSE: AGL)

They are working hard towards the implementation of the Teck merger

Anglo American released a production update for the three months to March 2026. We may as well begin with copper, since that’s all the rage at the moment.

The copper-focused merger with Teck Resources is expected to close between September 2026 and March 2027. The final outstanding regulatory milestone is regulatory approval in China, along with other standard closing conditions.

In the meantime, Anglo’s copper production increased by 1% year-on-year, with lower grades at Quellaveco putting the handbrake on a story that was positively impacted by Los Bronces and Collahuasi.

In premium iron ore, production dipped 2%. You can read about Kumba Iron Ore (JSE: KIO), part of the Anglo group, further down in Ghost Bites today. Minas-Rio also experienced a dip in production.

Manganese ore, Anglo’s third and final focus area in terms of producing assets, enjoyed a 118% rebound in production after the tropical cyclone in Australia last year.

We now reach diamonds, the ongoing story of value-destruction disruption. Production increased by 17%, so they’ve clearly given up on hoping that scarcity will drive prices. Something isn’t scarce anymore if it can be grown in a lab.

They expect to produce at a cost of $80/carat, with rough diamond prices down 19% in the quarter, to $101/carat. That’s a weak margin. The glory days for De Beers are well and truly over, as I’ve been flagging for the past few years.

Of course, this doesn’t stop Anglo from entirely avoiding the enormous, trumpeting elephant in the room when they write: “Rough diamond trading conditions continued to be challenged due to ongoing industry, geopolitical and tariff headwinds.“

No. Rough diamond trading conditions suck because lab grown diamonds destroyed the industry. Anglo can do whatever they like to convince us (and a potential buyer of De Beers) otherwise, but the facts are the facts.

Steelmaking coal production fell by 31%, with the Moranbah North incident in March 2025 impacting production ever since. There were also significant weather impacts.

Nickel production dipped by 7% due to maintenance at two of the mines.

So, as you can see, it’s a mixed bag. Despite this, production and unit cost guidance is unchanged for 2026.

CMH banks an impressive jump in earnings (JSE: CMH)

They’ve responded to disruption extremely well

The Chinese (and to a lesser extent, Indian) car invasion has thrown the local and global automotive sector into disarray. Disruption quickly separates the strong from the weak, with CMH proving that they fall into the former category.

For the year ended February 2026, revenue increased 18.6% and operating profit was up 17.1%. HEPS jumped by a delicious 33%!

Interestingly, the cash dividend was much lower in this period despite the jump in earnings. If you read through the detail, you’ll find that this is because of a share repurchase offer that the company undertook towards the end of 2025. The board was disappointed with the outcome of the share repurchase, with only 50% of holders electing to sell their shares.

I think the board should take this as a compliment. Also, the time for buybacks is when the share price is in the doldrums, not when it’s on a strong upswing. We will have to wait and see what the company does with the significant cash pile on the balance sheet.

As a quick look at the segmentals, CMH generated 94% of revenue in the motor retail and distribution business, 5% in car hire and 1% in financial services. But the margins are structurally different across these businesses, so the split for profit before tax looks very different: 49% motor retail, 29% car hire and 13% financial services. For those doing mental maths, 9% of profit before tax sits in the “corporate services and other” bucket.

The star of the show was the motor retail and distribution business, where profit before tax jumped from R164 million to R258 million. It really is an impressive performance for a group that has many non-Chinese and Indian brands in the stable.

What are your views on the motor retail sector?

With one quarter out of the way, Kumba Iron Ore has reiterated full year guidance (JSE: KIO)

Finished stock levels at the port helped support sales growth

Kumba Iron Ore has released a production and sales report for the three months to March 2026.

As always, the company has to manage its business based on what Transnet is actually capable of delivering, with a planned 10-day logistics maintenance shutdown at Transnet scheduled for May.

This is why production was 2% lower year-on-year, as there’s not much value in accelerating production that cannot subsequently be railed to port. There were some challenges with rail transport this quarter as well, with adverse weather washing away a portion of the rail itself. Ore railed to port by Transnet dipped 1% for the quarter.

Thankfully, with high port stock volumes and improved port performance in general, sales actually increased by 3%. Total finished stock decreased from 7.5Mt to 7.2Mt, with 4.7Mt at the mines and 2.5Mt at Saldanha Bay Port.

Iron ore prices were under pressure at the beginning of the quarter, but subsequently showed positive momentum into March.

Kumba’s performance always comes with the caveat of reliance on Transnet. Subject to Transnet performing in line with expectations, Kumba has left guidance for 2026 unchanged.

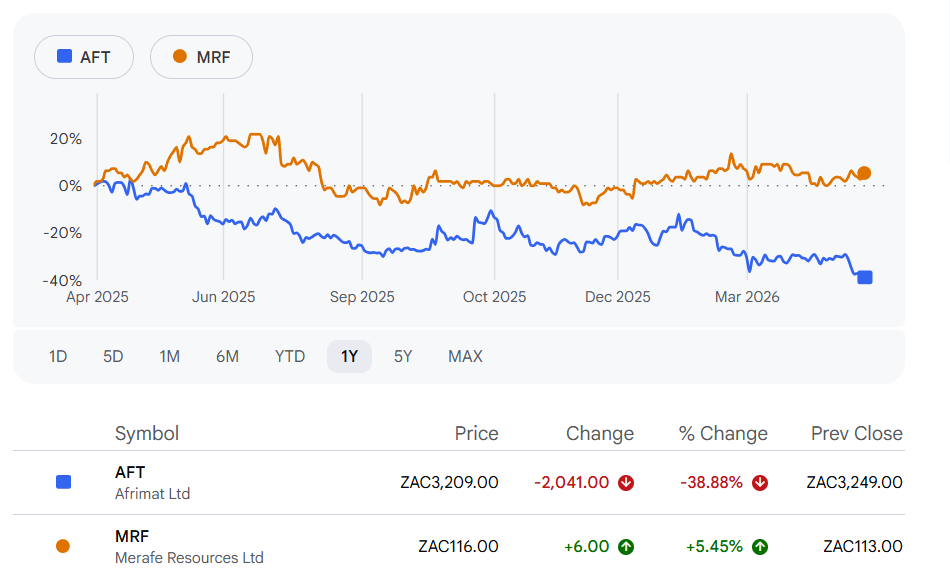

Merafe’s ferrochrome production was negligible in the latest quarter (JSE: MRF)

Chrome ore and PGMs kept things ticking over

Merafe has released a production report for the three months to March 2026. As we know, the ferrochrome smelter industry has been in absolute crisis. This comes through in the form of a 95% drop in year-on-year production.

Remember, Afrimat (JSE: AFT) is just one of the casualties elsewhere in the value chain from this issue.

Merafe’s attributable chrome ore production increased by 2.9% year-on-year, while attributable PGMs concentrate production decreased by 12% due to lower feed tonnages.

The share price is actually 5.5% up over 12 months, with the market believing that a resolution to the smelter crisis is just around the corner. Although Afrimat has broader issues, it’s still amazing to me that Merafe’s share price has been so resilient vs. Afrimat’s nasty drop:

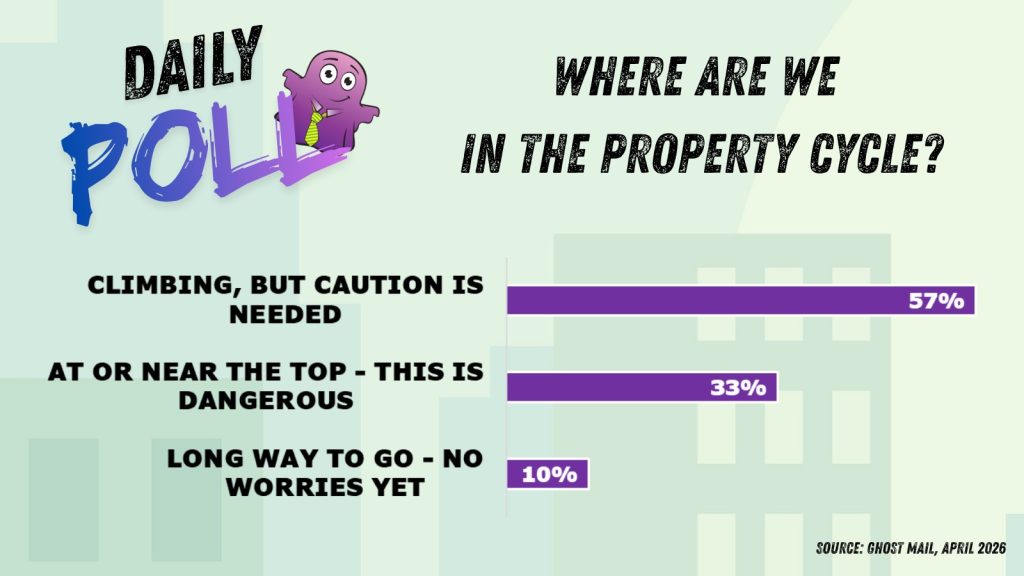

Results of yesterday’s poll:

Nibbles:

- Director dealings:

- An entity related to a non-executive director of Lighthouse Properties (JSE: LTE) sold shares worth R32.2 million.

- A person associated with a director of Mondi (JSE: MNP) bought shares worth around R840k. That’s quite the dip to buy!

- A director of Sabvest Capital (JSE: SBP) sold shares worth R351k to settle debt obligations.

- FirstRand (JSE: FSR) has thrown in the towel on the UK motor commission matter. They have decided not to legally challenge the proposed redress scheme. It sounds like they couldn’t put together a meaningful group of other lenders to act together.

- African Rainbow Minerals (JSE: ARM) has concluded a conditional nickel off-take agreement with Boliden Commercial AB. This is a multi-year deal for the sale of nickel concentrate by the Nkomati Nickel Mine. But no detailed terms are disclosed unfortunately, so there’s not much I can tell you other than the nickel is headed to Finland – home to the only large-scale nickel smelter in Europe.

- RMB Holdings (JSE: RMH) announced that AttBid has bought more shares in the company and how holds 10.86%. The combined holding with Atterbury Property Fund is 43.63%.

- Putprop (JSE: PPR) basically has no liquidity at all in its stock, so the transaction to sell 50% in Corridor Hill for R34.7 million only gets a passing mention down here. The acquirer is Bidvest (JSE: BVT), owner of the current tenant (McCarthy Limited). The last independent valuation in Putprop’s books had the property at R37.6 million.

- Pan African Resources (JSE: PAN) has received court approval for the proposed share capital reduction. This ended up being far more of a mission than anyone thought, as you may recall that the courts weren’t happy with the initial shareholder notice and made Pan African do it again.

- The chair and lead independent director of Grindrod (JSE: GND) are retiring from the board at the end of the AGM in June. This marks the conclusion of Grindrod’s strategy to dispose of non-core assets. Four new independent non-executive directors have been announced. Grindrod has certainly been quite the turnaround story!

- Wesizwe Platinum (JSE: WEZ) is still trying to finish its financials for the year ended December 2025. They have pushed them out to 15 May 2026. Once these are released, the company should be able to follow the process to have the suspension of the shares lifted.